LBRT - Patterson-UTI Grows With NexTier Merger

2024-01-15 10:53:37 ET

Summary

- Oilfield service company Patterson-UTI’s market capitalization is $4.3 billion, and it pays a 3.1% dividend.

- The company’s merger-of-equals with NexTier (55% PTEN/45% NexTier) will enhance cash flow and EBITDA. Its acquisition of Ulterra adds an interesting bit of technology.

- Oilfield services is a very competitive sector. With producers (customers) merging and already reining in drilling costs, expect revenues to remain challenged.

Contract driller Patterson-UTI Energy ( PTEN ) is classically dependent on US drilling activity, so it is a volatile second derivative of oil (and natural gas) prices and consequent drilling activity levels. PTEN operates in all major basins, but its largest emphasis is in the prolific west Texas-eastern New Mexico Permian.

Investors should be aware Seeking Alpha's quant rating system has flagged Patterson-UTI for negative EPS revisions and decelerating momentum.

The company made a significant merger-of-equals with NexTier and an acquisition of bit specialist Ulterra in the oilfield services sector: PTEN's market capitalization is 38% larger than a year ago . Its stock price is -29% lower . Factors include a decline in drilling activity and share issuance for acquisitions.

Although companies are drilling less, the wells they drill are more efficient. PTEN's CEO Andy Hendricks has said fewer rigs require more workers . On top of this, consolidation among producers has led and will lead to trimmed drilling activity.

Still, the basic underlying technological fact is that horizontal wells decline very quickly. Even for companies looking to just maintain (not grow) existing production volumes from horizontal shale wells, continued drilling capex is necessary.

For dividend-hunters, Patterson-UTI offers a modest 3.1% dividend that may become more attractive should interest rates fall. I recommend the company's stock to those looking for capital appreciation in this volatile sector.

Macro

Market activity will hinge on Federal Reserve interest rate decisions. Some rate cuts are expected in 2024. Rate cuts will both reduce debt finance costs directly and make dividend yields more attractive by comparison.

Recent months have been notable for the large number of producer mergers and acquisitions. Consolidation and cyclical redirection toward Tier 1 prospects have led to reduced drilling, albeit with longer laterals and resulting in all-time high US oil production.

Although not all have been regulatorily approved nor closed, these transactions include:

- Chesapeake ( CHK )-Southwestern ( SWN )

- Exxon Mobil ( XOM )-Pioneer Resources ( PXD )

- Chevron ( CVX )-Hess ( HES )

- Civitas ( CIVI )-three private Permian companies

- Occidental ( OXY )-CrownRock (private)

- Permian Resources ( PR )-Earthstone ( ESTE )

- Ovintiv ( OVV )-three private Permian companies

- APA ( APA )-Callon Petroleum ( CPE )

Other factors include large supply-demand issues such as OPEC+ production and Chinese demand.

Current US federal energy policy is to prefer renewables and block the production and use of thermal fuels-coal, natural gas, oil--with a variety of regulations. For example, some in the Biden administration are discussing the idea of limiting LNG export growth .

Acquisitions of Ulterra and Merger with NexTier

In July 2023, PTEN acquired drill bit company Ulterra for $370 million in cash and 34.9 million shares of Patterson-UTI stock. The deal was thus estimated to be worth $780 million . Ulterra is known for its polycrystalline diamond compact (PDC) drill bits. Anticipated 2023 EBITDA for Ulterra was $160 million to $180 million . Ulterra's growing presence in the Middle Eastern drilling market was seen as beneficial for Patterson-UTI.

The merger of equals between Patterson-UTI and NexTier Oilfield Solutions , Inc. with an estimated $5.4 billion of combined enterprise value was announced in June 2023. After shareholder approval in August 2023 , each shareholder of NexTier received 0.752 shares of Patterson-UTI stock per share of NexTier. Legacy Patterson-UTI shareholders owned 55% and former NexTier shareholders owned 45% of the combined, larger Patterson-UTI.

According to the Patterson-UTI announcement, "On an annualized combined basis as of the first quarter of 2023, the combined company generated approximately $6.9 billion of revenue, $1.9 billion in adjusted EBITDA and improved free cash flow generation."

The transaction was expected to be accretive to earnings per share and free cash flow in 2024.

Third Quarter 2023 Results and Guidance

In 3Q'23 Patterson-UTI's quarterly reporting included 30 days of reporting for NexTier Oil Solutions and 48 days of reporting for Ulterra. Total revenue was $1.0 billion but net income was $0.1 million or effectively $0.00/share . This included $70 million of merger expenses offset by recognition of $29 million of previously deferred revenue.

Adjusted net income was $55 million, or $0.20/share and adjusted EBITDA was $227 million. Note that both of these exclude merger and acquisition expenses and include recognition of previously deferred revenue.

According to Andy Hendricks, PTEN's CEO, "The integrations of NexTier and Ulterra into Patterson-UTI are on track. We have a clear line of sight to deliver at least $200 million in annualized synergies from the NexTier transaction alone by the first quarter of 2025."

Looking at 4Q'23, "We believe our sequential activity will outperform the industry average in the fourth quarter. We expect U.S. Contract Drilling revenue per day of $35,400 and costs per day of $19,300, resulting in adjusted gross margin per operating day of $16,100."

For 4Q'23, the company expected Completion Services adjusted gross margin of about $200 million and Drilling Products adjusted gross margin of $30 million.

Operations and Strategy

The number of Patterson-UTI rigs operating tends to follow the oil price but with a lag and not proportionately, reflecting public producers' recent focus on return of capital to shareholders, greater drilling efficiency, and consolidation by acquisition.

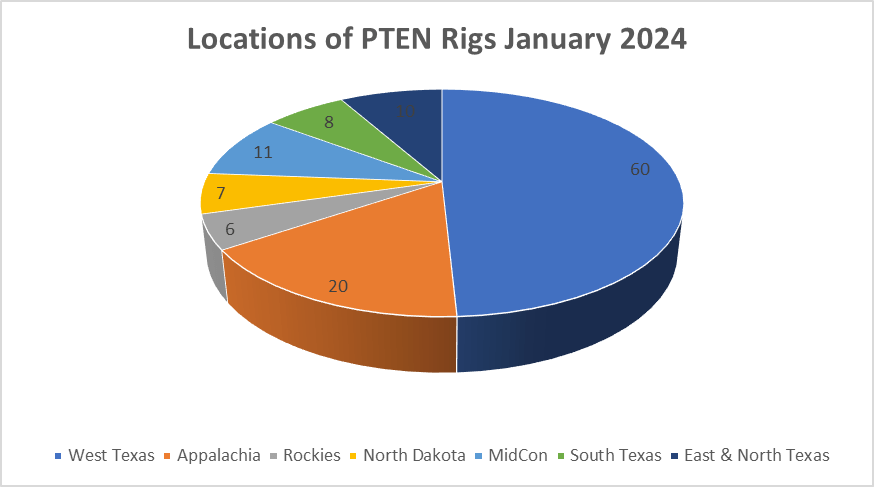

The company reports it had 118 rigs operating in 4Q'23 .

Per the company's rig summary about half of operating rigs are working in the Permian basin.

{kind=link}

Patterson-UTI has revamped its segment reporting from contract drilling, pressure pumping, and directional drilling to a) drilling services, b) completion services, and c) drilling products.

The company's new business alignments are shown below.

1) Drilling Services:

- U.S. and International Contract Drilling

- MS Directional Drilling

- Superior QC

- Current Power

- Warrior Drilling Equipment

2) Completion Services:

- Universal Pressure Pumping

- NexTier Oilfield Solutions

3) Drilling Products:

- Ulterra Drilling Technologies

4) Other:

- Great Plains Oilfield Rentals

- Petroleum.

Oil and Gas Prices

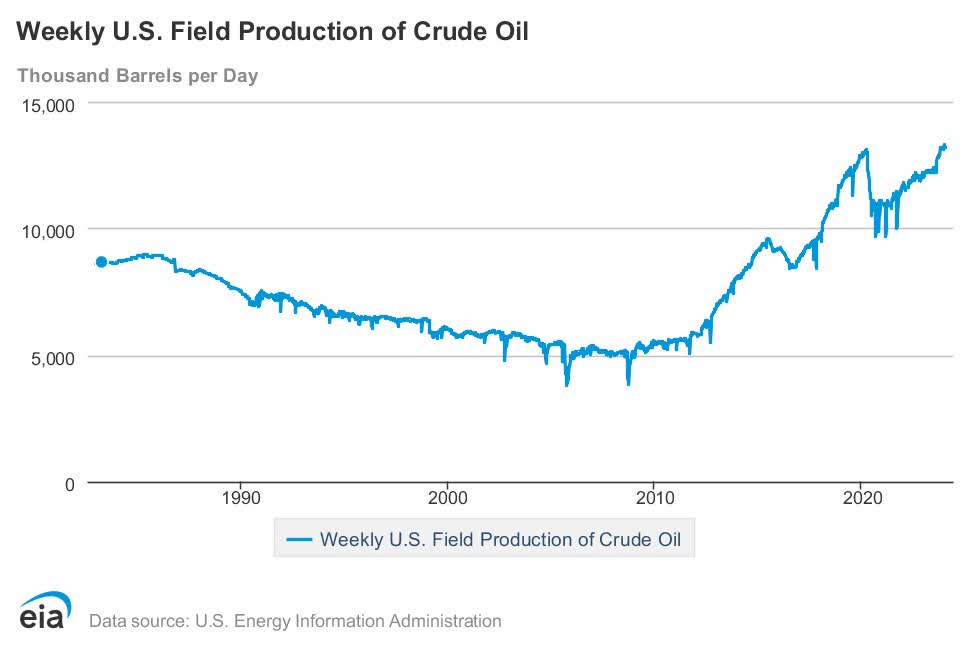

The primary driver of PTEN's activity is the oil price, although the company is also subject to producers' activity levels. Many public companies have prioritized return of capital to shareholders over increased rates of drilling. Drilling has also become more efficient, requiring fewer rigs but resulting in new highs in US oil production, for example.

Lower natural gas prices have dampened gas drilling.

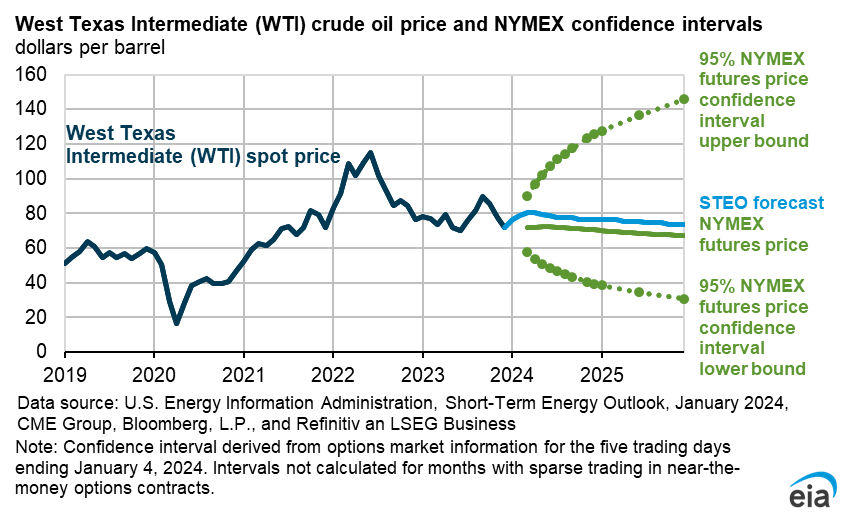

January 12, 2024, closing West Texas Intermediate ((WTI)) futures oil price (February 2024 delivery) was $72.68/barrel. The Henry Hub natural gas futures price, also for February 2024 delivery, was $3.31/MMBTU.

The Energy Information Administration ((EIA)) forecasts higher oil production: 13.2 million BPD in 2024 and 13.4 million BPD in 2025 compared to current production of 13.2 million BPD for the week ending January 5, 2024.

{kind=link}

The EIA's Short Term Energy Outlook (STEO) 5-95 confidence interval for WTI prices at year-end 2025 ranges between $30/bbl and $145/bbl and the expected price path declines slightly.

{kind=link}

Competitors

Patterson-UTI is headquartered in Houston, Texas.

US competitors include companies like Baker Hughes ( BKR ), Halliburton ( HAL ), Helmerich & Payne ( HP ), Liberty Oilfield Services ( LBRT ), Nabors Industries ( NBR ), NOV Inc. ( NOV ), ProPetro Holding ( PUMP ), and Weatherford ( WFRD ). SLB ( SLB ) is a global competitor.

Governance

On January 1, 2024, Institutional Shareholder Services ranked Patterson-UTI's overall governance as 1, with sub-scores of audit (2), board (2), shareholder rights (3), and compensation (1). In this ranking a 1 indicates lower governance risk and a 10 indicates higher governance risk, so the overall rating is excellent.

Shorts were 8.0% of float on December 29, 2023.

Insiders held 1.9% of shares.

Patterson-UTI's beta is 2.25, well above the market level of 1.0 but in line with a company whose activity is a derivative of volatile US oil and gas prices.

On September 29, 2023, the five large institutional stockholders, some of which represent index fund investments that match the overall market, were BlackRock (13.4%), Vanguard (10.4%), Blackstone (8.4%), and Dimensional Fund Advisors and Macquarie Group, each with 4.2%.

BlackRock and Macquarie are signatories to the Net Zero Asset Managers initiative , a group that as of December 4, 2023, manages $57 trillion in assets worldwide and which limits hydrocarbon investment via its commitment to achieve net zero alignment by 2050 or sooner.

Six directors from legacy PTEN and five from NexTier comprise PTEN's new board. The president and chief executive of NexTier, Robert Drummond, became the vice chair of the combined companies, which continue to be called Patterson-UTI.

Financial and Stock Highlights

With a January 12, 2024, closing stock price of $10.28/share, market capitalization is $4.3 billion, up 38% from $3.1 billion a year ago. The stock price is lower than a year ago, but the share count is much higher, nearly double due to the use of shares for acquisitions.

Trailing twelve months' EPS is $1.24 for a current price/earnings ratio of 8.3. The averages of analysts' 2023 and 2024 EPS estimates are $1.12 and $1.22, respectively for a forward P/E ratio range of 8.4-9.2.

The 52-week price range is $9.70-$17.62 per share, so the closing price of $10.27/share is 58% of the one-year high and 61% of the one-year target of $16.79/share.

The dividend of $0.32/share yields 3.1% at the current share price. The company also has a share buyback program which it is expected to re-authorize.

Mean analyst rating is a 2.1, or "buy," from twenty-eight analysts. At least one analyst considers it significantly undervalued.

At September 30, 2023, from the most recent 10-Q filing PTEN had $2.56 billion in liabilities, including $1.23 billion of long-term debt. With $7.42 billion in assets the liability-to-asset ratio is 35%.

The long-term debt comprises:

- $482.5 million of 3.95% senior notes maturing in 2028

- $345 million of 5.15% senior notes maturing in 2029 and

- $400 million of 7.15% senior notes maturing in 2033.

The ratio of enterprise value to EBITDA is 5.6, or well below the maximum of 10.0, suggesting a bargain.

The book value of $11.62/share is larger than the market value, suggesting investor pessimism.

Positive and Negative Risks

Patterson-UTI's activity is a function of both oil prices and the intensity of drilling at any given price level.

A positive risk is that horizontal wells decline quickly. Companies seeking to hold production level must do more drilling than they would for production from vertical wells.

Another positive risk is that companies of all different sizes can contract for the drilling of onshore non-conventional wells. This contrasts with the large commitments of hundreds of millions or even billions of dollars required for offshore wells.

A negative risk is that oil and gas drilling and consumption is currently discouraged through a large variety of regulations and regulatory proposals from a hydrocarbon-unfriendly federal (and some states') government.

Recommendations for Patterson-UTI

Contract drillers are the sharp end of the spear-needed either much or little depending on prices--something of which investors should be mindful since it can contribute to extreme business and stock price volatility.

Nonetheless, Patterson-UTI has an excellent governance score and has made a business-synergistic merger with NexTier and an accretive acquisition of Ulterra.

Given consolidation in the upstream sector, focus on capital returns to investors, and improved efficiency requiring fewer rigs, reductions in oilfield service activity have already been occurring for several months.

The company offers a reasonable debt level. It has reasonable forward-price earnings and a bargain EV/EBITDA ratio that can be expected to improve further as NexTier is fully integrated into the company. PTEN is also investor-friendly, offering both a fixed dividend and share buybacks.

Dividend-hunters may find Patterson-UTI more attractive if competitive rates fall. I recommend Patterson-UTI to investors seeking capital appreciation in oilfield service stocks who are comfortable with the sector's volatility. The expansion via Ulterra drill bits and the merger-of-equals combination with NexTier appear likely to add good upside to future earnings and cash flow. This will be more evident in 4Q'23 and 2024 results.

patenergy.com

For further details see:

Patterson-UTI Grows With NexTier Merger