PAXS - PAXS: Continuing Failure To Cover The Distribution

2023-12-15 16:39:40 ET

Summary

- PIMCO Access Income Fund offers a current yield of 12.71% and trades at a discount on net asset value.

- The PAXS closed-end fund's performance over the past five months has been worse than expected due to changing market sentiment and rising interest rates.

- The market may be overpricing bonds, as the December FOMC meeting did not suggest interest rate cuts of the magnitude currently priced into the market.

- The fund's high level of leverage may be a drag on its performance, as it is underperforming the aggregate bond index even as long-term rates have fallen over the past month.

- The fund is failing to cover its distribution pretty consistently, and destroying its net asset value in the process.

The PIMCO Access Income Fund ( PAXS ) is a closed-end fund aka CEF that income-focused investors can employ in pursuit of their goals. As is the case with most PIMCO funds, this one certainly does reasonably well on the income front, as its 12.71% current yield is easily in line with most other quality fixed-income funds. This fund also tends to be somewhat more reasonably priced than most of the funds from PIMCO, as it actually trades at a discount on net asset value. However, this fund’s discount is not nearly as large as the double-digit discounts that we sometimes see with comparable funds from other fund houses. Nevertheless, it tends to offer a pretty good deal for a PIMCO fund.

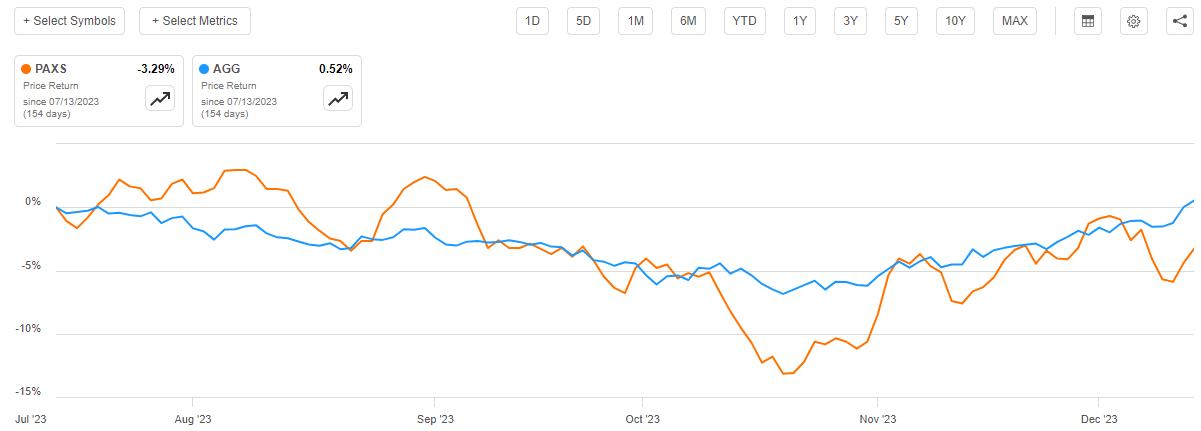

As regular readers can likely recall, we last discussed the PIMCO Access Income Fund back in the middle of July. It would hardly be an overstatement to say that the overall market environment has changed since that time. The market has begun pricing in at least six interest rate cuts next year, although in its statement on Wednesday, the Federal Reserve guided to a maximum of three interest rate cuts. This switch in market sentiment came only after a few months of pessimism and rising interest rates, so the fund’s price performance over the past five months since my previous article was published has not been as good as might be expected. Over that period, shares of this fund are down 3.29%, which compares quite poorly to the 0.52% gain of the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

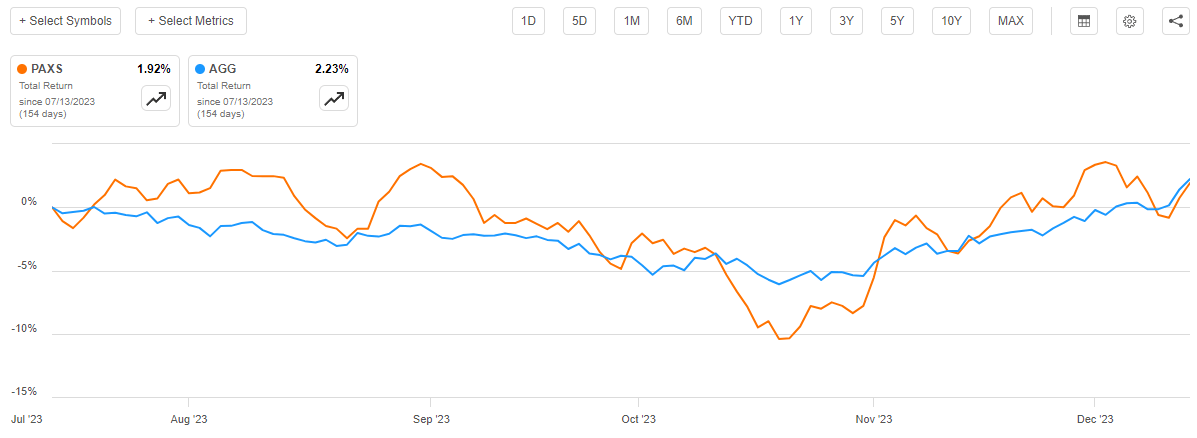

This is something that may be discouraging for potential investors. After all, nobody likes to lose money. However, one of the characteristics of funds like the PIMCO Access Income Fund is that they pay most to all of their investment profits out to the shareholders in the form of distributions. As such, the distributions paid by these funds tend to be quite large and can frequently compensate for declines in the fund’s share price. When we take the distributions into account, investors in the PIMCO Access Income Fund are actually up by 1.92% since the date that my previous article on this fund was published. That is, unfortunately, still worse than investors in the Bloomberg U.S. Aggregate Bond Index have fared:

{kind=link}

This is certainly disappointing, although the fact that the PIMCO fund has a substantially higher yield than the index might still prove to be appealing to some investors who are primarily focused on the generation of income. More importantly, if the Federal Reserve does cut interest rates next year, it could prove to be good for bond funds like this one, although at this point the potential interest rate cuts are almost certainly priced into the fund’s shares.

About The Fund

According to the fund’s website , the PIMCO Access Income Fund has the primary objective of providing its investors with a high level of current income. The fund has the secondary objective of achieving capital appreciation. The first of these objectives is pretty normal for a bond fund, but the second one is rather strange. As I pointed out in a recent article ,

Bonds do not deliver capital appreciation indefinitely. Bond prices do go up when interest rates go down, but that is about it. There is a limit as to how far interest rates can decline since nobody will ever lend money at a negative nominal rate. In fact, after the problems that have been caused by the easy money policies of the past two decades, it seems rather unlikely that the central bank will ever let the real interest rate drop below zero percent.

Thus, there is a hard limit as to the amount of capital appreciation that can be achieved by investing in bonds. While it is certainly possible to grow the size of a bond portfolio organically by using coupon payments or bond trading profits to buy more bonds, essentially reinvesting the investment returns, most closed-end funds do not do this. Rather, the way that investors can achieve long-term or indefinite capital appreciation from a fund like this is to reinvest the distributions that it pays out. That, naturally, will reduce the amount of income that the investor can use for their own purposes but the yield on this fund is high enough that it probably feasible to use part of the distribution to finance your own lifestyle while using the remainder for reinvestment into this fund or another one.

The description of this fund’s strategy on the webpage suggests that it is a dynamic or tactical bond fund as opposed to one that simply invests in fixed-coupon bonds. Per the webpage:

The Fund seeks to achieve its investment objectives by utilizing a dynamic asset allocation strategy among multiple sectors in the global public and private credit markets, including corporate debt, mortgage-related and other asset-backed instruments, government and sovereign debt, taxable municipal bonds and other fixed-, variable, and floating-rate income-producing securities of U.S. and foreign issuers, including emerging market issuers and real estate-related investments (“real estate investments”). The Fund may invest without limitation in in investment grade debt securities and below investment grade debt securities (commonly referred to as “high yield securities” or “junk bonds”), including securities of stressed, distressed, or defaulted issuers.

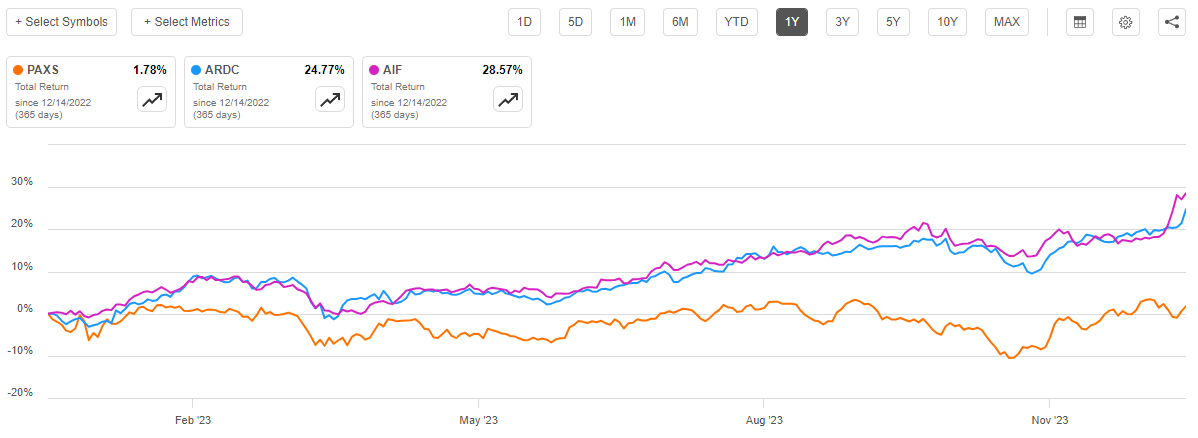

As we can see, the fund explicitly states that it can change its allocation based on prevailing market conditions. This is a big advantage in today’s market. After all, over the past three years or so, those funds that have been able to increase their exposure to floating-rate securities at the expense of fixed-rate debt generally outperformed traditional bond funds. This is because they were able to avoid the losses that came along with rising interest rates. The reverse is likely to be true if interest rates do indeed decline over the next year or two. After all, floating-rate securities do not benefit when interest rates fall as their prices remain relatively stable but the amount that they pay their investors goes down. Meanwhile, fixed-rate securities see their prices increase when interest rates go down. The fund’s description of its strategy on its website suggests that it can alter its composition to take advantage of either environment. However, its total return over the past year has been absolutely terrible compared to other funds that switch between floating-rate and fixed-rate securities:

{kind=link}

As we can see here, the Apollo Tactical Income Fund ( AIF ) and the Ares Dynamic Credit Allocation Fund ( ARDC ), which are two of the best funds for any interest rate environment, have substantially outperformed the PIMCO Access Income Fund. This strongly suggests that the fund’s managers have not been taking advantage of its ability to invest in floating-rate securities despite the fact that these securities have substantially outperformed traditional bonds since the end of the pandemic.

A look at the fund’s portfolio suggests the same thing. Here is the fund’s current asset allocation across debt classifications:

Fund Fact Sheet

The fund does not state which of these are fixed-rate securities compared to floating-rate securities, but it seems likely that they are nearly all interest-rate sensitive fixed-rate securities. After all, 47.1% of the portfolio consists of mortgage-backed securities. These are almost always fixed-rate securities. The 13.2% allocation to short-duration instruments should help the fund protect itself against interest-rate risk, but that is not a large enough weighting to offset the fact that all of these other things will decline in price when interest rates increase.

Thus, despite the description of the fund’s strategy that is provided on both the fund’s website and in its fact sheet , this fund appears to be acting much like a traditional bond fund. The fund states that it can invest in floating-rate senior loans, collateralized loan obligations, and things like that but this does not appear to be the case. This is not the best allocation for a rising interest rate environment, which certainly explains why it has been underperforming the Apollo and Ares funds which are much better positioned to navigate the environment that we have seen over the past three years.

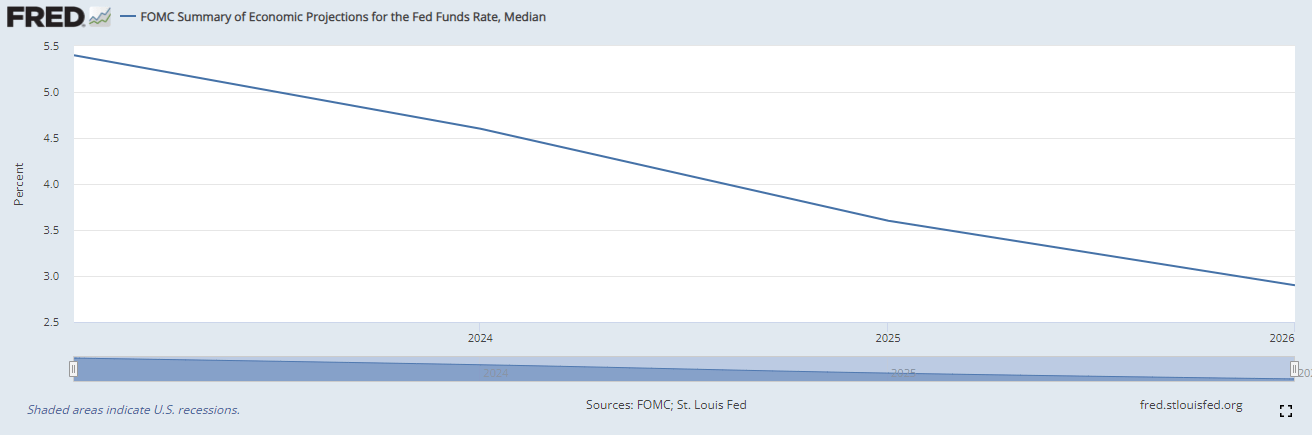

With that said the fund’s portfolio is quite well-positioned to take advantage of an environment in which interest rates are falling. After all, bond prices rise when interest rates decline. The Federal Reserve implied earlier this week that the federal funds rate will probably be reduced over the next twelve months. The Federal Open Market Committee’s dot plot projected a federal funds rate of 4.625% at year-end 2024:

{kind=link}

That implies three interest rate cuts of 25 basis points each over the course of the year. This is obviously a favorable outlook for fixed-rate bonds, such as the ones held by this fund. However, the market has already priced this in and then some. The market has priced in six interest rate cuts over the next twelve months based on the current action in the federal funds futures market. Thus, there is still the potential for disappointment here, despite the fact that the rate cuts should drive up the price of the securities in this fund. After all, if the market is pricing in six interest rate cuts and the Federal Reserve only delivers three, then it suggests that bond prices are currently too high, and the fund will end up taking some losses as the market is disappointed.

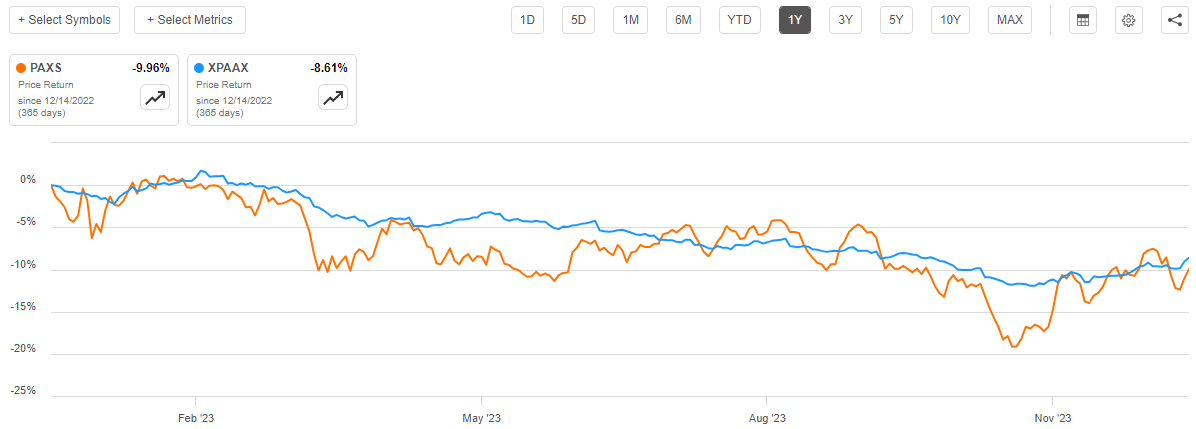

Fortunately, this is one of the few PIMCO funds that has not seen its share price outperform its portfolio over the past year. As we can see here, the fund’s net asset value per share has declined by 8.61% over the past twelve months, but the fund’s share price is actually down 9.96%:

{kind=link}

This reduces some of the inherent risk here since buying at a premium always has the potential to amplify an investor’s losses if a thesis does not play out. In this case, the risk is that the Federal Reserve will follow through on its own projections instead of what the market currently expects. Curiously though, we can see that this fund’s net asset value per share has not increased significantly over the past month, which has generally been characterized by the market pricing in the expected interest rate cuts. Indeed, over the past thirty days, the fund’s net asset value per share is only up 2.46% but the Bloomberg U.S. Aggregate Bond Index is up 4.42%. That certainly reduces the appeal of this fund somewhat, especially given that PIMCO’s reputation tends to make its funds a bit more expensive than comparable funds available from other fund houses.

Leverage

As is the case with most closed-end funds, the PIMCO Access Income Fund employs leverage as a method of boosting the effective yield of the fund’s portfolio. It also should boost the fund’s price performance during a period of falling interest rates. I explained how this works in my previous article on this fund:

In short, the fund borrows money and uses that borrowed money to purchase bonds and similar fixed-income assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will normally be the case. With that said though, this strategy is much less effective today with market rates above 5% than it was three years ago when rates were just barely above 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to an outsized amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of assets for this reason.

As of the time of writing, the PIMCO Access Income Fund has leveraged assets comprising 44.25% of its portfolio. This is one of the highest levels of leverage possessed by any closed-end fund in any sector. While fixed-income funds can ordinarily carry a higher level of leverage than equity funds, this is still high enough to give any risk-averse income-seeking investor pause. The fund’s leverage is down somewhat from the 47.23% leverage that it had back in July, but it is still concerning. There are other funds that can be purchased that do not have such leverage and the risks accompanying that leverage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the PIMCO Access Income Fund is to provide its shareholders with a very high level of current income. This makes a great deal of sense for a fixed-income fund considering that these securities are primarily income vehicles. The fund invests in a variety of these securities from issuers both in the United States and abroad and pools the money that it receives from its coupon payments. The fund employs leverage to amplify the income that it receives from the securities since the leverage allows it to control more bonds than it could purchase simply by relying on its equity alone. The fund combines all of the money that it receives via these coupon payments with any profits that it manages to realize by exploiting price swings that accompany changes in interest rates. The fund then pays all of this money out to its shareholders, net of its own expenses. As bonds have fairly high yields in today’s environment, we might expect that this strategy will allow the fund’s shares to boast a very high yield as well.

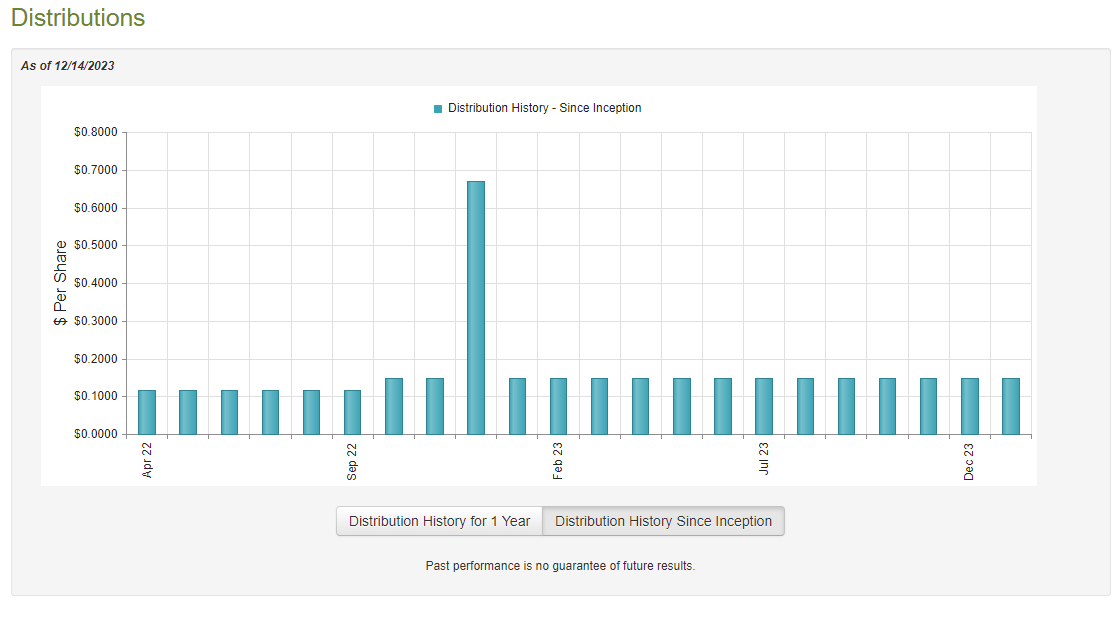

This is certainly the case, as the PIMCO Access Income Fund currently pays a monthly distribution of $0.1494 per share ($1.7928 per share annually), which gives it a 12.71% yield at the current share price. The fund has been remarkably consistent with respect to its distribution over the years. In fact, it increased its distribution late last year and has kept it at the same level since that time:

{kind=link}

This stands in stark contrast to the distribution history of most fixed-income funds. After all, the majority of the funds in this sector that are not heavily weighted to floating-rate loans have had to reduce their distributions due to the losses that they took in 2022. The fact that this one has not had to reduce its payout is something that we should therefore investigate, as it seems quite strange that it would be able to pull off a feat that few other funds were able to accomplish.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on June 30, 2023. This is a much newer report than the one that we had available to us the last time that we discussed this fund, which is quite nice to see. After all, the last time that we discussed this fund, it strongly appeared that the fund could not sustain its distribution, let alone afford the distribution increase that it implemented at the end of last year. However, the first half of 2023 was somewhat more friendly towards bond funds than 2022 was, as the market pushed down long-term interest rates in anticipation of a Federal Reserve pivot. That could have given the fund the opportunity to realize some gains by selling appreciated bonds into a relatively friendly market. This report will give us a good idea of how well the fund performed at accomplishing this task, which hopefully improved its distribution coverage.

During the full-year period, the PIMCO Access Income Fund received $119.969 million in interest along with $2.252 million in dividends from the assets in its portfolio. This gives the fund a total investment income of $122.221 million during the period. The fund paid its expenses out of this amount, which left it with $79.679 million available for the shareholders. That was, unfortunately, nowhere near enough to cover the $98.875 million that the fund paid out in distributions. At first glance, this is almost certainly going to be very concerning, as we would normally like to see a fixed-income fund fully fund its distribution out of net investment income.

However, there are other methods through which the fund can obtain the money that it requires to cover its distribution. For example, it might have been able to earn some trading profits by taking advantage of favorable swings in interest rates and bond prices. Unfortunately, this fund failed miserably at that task during the full-year period. The PIMCO Access Income Fund reported net realized losses of $50.054 million along with $33.804 million net unrealized losses. Overall, the fund’s net assets declined by $102.762 million after accounting for all inflows and outflows during the period. This strongly suggests that the fund cannot afford the distribution that it is paying out, which makes its management’s decision to raise the payout late last year rather confusing.

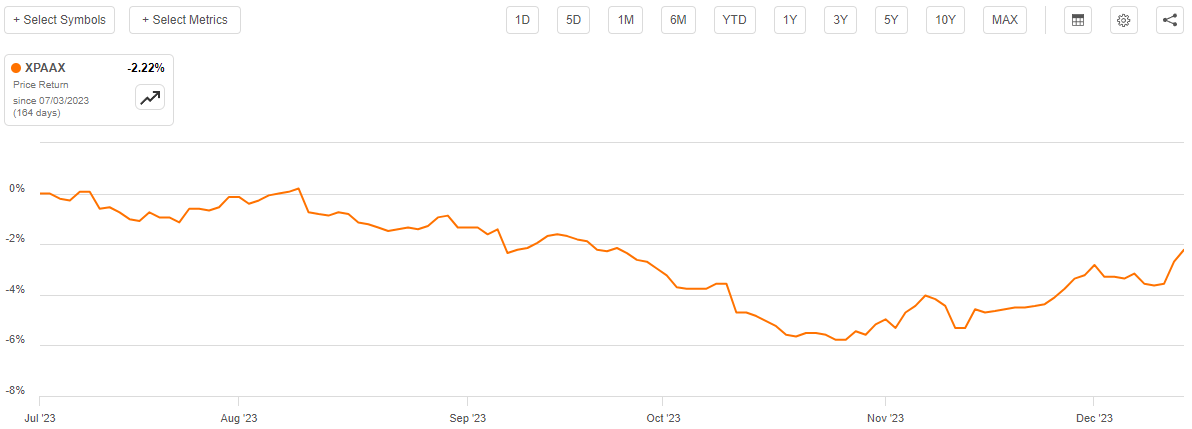

The fund appears to continue to struggle with covering its distribution. As we can see here, the fund’s net asset value per share has declined by 2.22% since July 1, 2023:

{kind=link}

This is the period of time that has passed since the end date of the fund’s most recent financial report. If it had succeeded in covering the distributions that it has paid out since that date, this amount would be flat or increasing, but that is not the case. This suggests that this fund is distributing far more money than it is earning from its investment portfolio. That destroys the fund’s net asset value and as such is not sustainable over any sort of extended period. It also makes it much more difficult for the fund to earn the returns that are needed to sustain its distribution once the market improves. Overall, this is a bad sign.

Valuation

As of December 14, 2023 (the most recent date for which data is currently available), the PIMCO Access Income Fund has a net asset value of $14.55 per share but the shares currently trade for $13.97 per share. This gives the fund’s shares a 3.99% discount on net asset value at the current price. This is one of the only PIMCO funds that trades at a discount, and the current price is more attractive than the 0.07% discount that the fund’s shares have averaged over the past month. However, when we consider the fact that the fund is failing to cover its distribution and the fact that bond prices may be elevated, the current discount does not seem sufficiently large to take on the potential risks here.

Conclusion

In conclusion, the PIMCO Access Income Fund is a multi-sector bond fund that does not invest in floating-rate or variable-rate loans, despite the description that the fund provides in its documentation. This is not necessarily a bad thing, as the fund is positioned well for a falling interest rate environment, which the Federal Reserve suggests is a very real possibility over the next twelve months.

However, the central bank is suggesting much higher terminal rates than the market, which suggests that bonds in general may be overpriced. That presents a real risk to investors who are purchasing PIMCO Access Income Fund today, as does the fact that this fund appears to be paying out a larger distribution than it can afford. As such, it may make sense to sit on the sidelines for now.

For further details see:

PAXS: Continuing Failure To Cover The Distribution