BIZD - PCF: Lack Of Transparency A Big Negative

2023-07-26 19:07:01 ET

Summary

- Investors today are in desperate need of income in order to sustain their standard of living in the face of the current inflation crisis.

- High Income Securities Fund invests in a portfolio of BDCs and CEFs to provide its investors with a very high level of current income.

- It is surprisingly difficult to get information about this closed-end fund as management is not very transparent and various online sources differ.

- The PCF fund recently cut its distribution for the third time since early 2020 and it is uncertain if the new distribution will prove sustainable.

- The fund is trading at a very large discount to the net asset value.

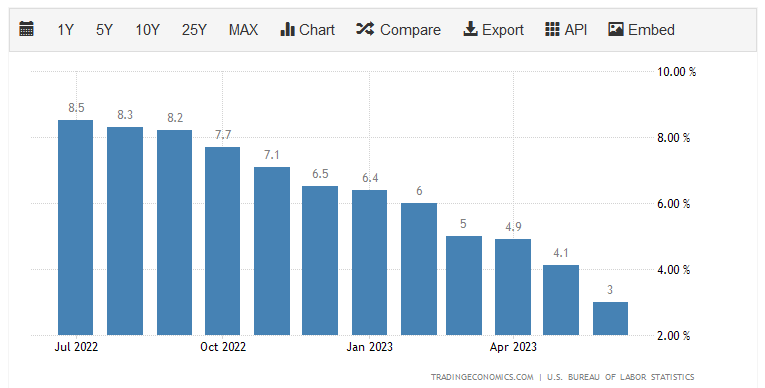

There can be little doubt that one of the biggest problems facing the average American today is the rapidly rising cost of living. This is clearly evidenced by the consumer price index, which claims to measure the price of a basket of goods that the average person in the United States regularly purchases. As we can see here, this index has increased by at least 3% year-over-year during each of the past twelve months:

{kind=link}

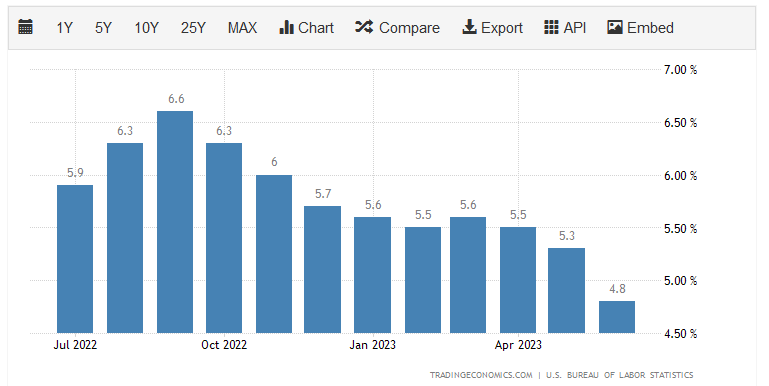

Generally, economists consider a 2% annual growth rate to be the maximum inflation rate for a sustainable economy. Thus, we can clearly see that the official figures are well above that. In fact though, as I have pointed out before, the actual picture is even worse because the consumer price index is being suppressed due to energy prices being lower this year than they were last year. If we exclude energy prices from the index, then the year-over-year inflation rate looks much worse:

{kind=link}

As we can clearly see, all of these figures are more than double the 2% rate that is considered healthy. The fact that prices are rising so quickly, and more quickly than wages, has strained the budget of many Americans to the point where people have resorted to things such as dumpster diving and pawning possessions to make ends meet. I discussed this in a recent blog post . In short, people are absolutely desperate for any source of income today to maintain their lifestyles.

As investors, we are certainly not immune to this. After all, we have bills to pay and require food for sustenance just like anyone else. In addition, we might want to enjoy a few of the luxuries that life has to offer. All of these things cost considerably more than they did only two years ago. Fortunately, we do have some ways through which we can obtain the extra income that we need to maintain our lifestyles. One of the best ways to accomplish this is by putting our money to work for us by buying shares of a closed-end fund aka CEF that specializes in the generation of income. These funds are unfortunately not very well followed in the media and many investment advisors are unfamiliar with them. As such, it can be difficult to obtain the information that we would really like to have to make an informed investment decision. This is a shame because closed-end funds offer advantages over familiar open-ended and exchange-traded funds. In particular, a closed-end fund is able to use certain strategies that have the effect of boosting its effective yield well beyond that of any of the underlying assets.

In this article, we will discuss the High Income Securities Fund ( PCF ), which currently boasts an 11.27% yield. This is clearly a high enough yield to get the attention of anyone that is seeking income from their portfolios. However, as I have pointed out in the past, anytime a fund's distribution yield passes double-digit levels, it is a sign that the market expects that the fund may soon have to cut its payout. As such, we will want to pay special attention to the fund's finances. I have discussed this fund before, but a few months have passed since that time, so obviously many things have changed. This article will focus specifically on those changes as well as provide an updated analysis of the fund's financial condition. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

The webpage for this fund is fairly spartan, as I pointed out in my last article on it. In fact, the webpage does not even have a fact sheet that can be downloaded. This makes this the only closed-end fund I have seen that does not include such a document on its webpage. Interestingly, there is no prospectus either that would explain what the fund's overall goal and strategy are. Morningstar does have a basic overview of the fund, however. Here is what that investment research firm states about this fund:

The fund's investment objective is to provide high current income as a primary objective and capital appreciation as a secondary objective. The investment committee currently manages the fund's assets with a focus on discounted securities of income-oriented closed-end investment companies and business development companies. The fund's objective is pursued by primarily investing, under normal circumstances, at least 80% of its net assets in fixed income securities, including debt instruments, convertible securities and preferred stocks.

This is something of a strange description as it specifically mentions a focus on other closed-end funds and business development companies but then states that 80% of the fund's assets will be invested in fixed-income securities. That makes no real sense, and in fact, the fund's semi-annual report says that fixed-income securities are quite rare in the fund. Here is the composition of the fund according to the most recent financial report:

| Asset |

| Percentage of Holdings |

| Business Development Companies |

| 20.52% |

| Closed-End Funds |

| 38.63% |

| Special Purpose Acquisition Vehicles |

| 17.06% |

| Real Estate Investment Trusts |

| 2.09% |

| Preferred Stock |

| 12.54% |

| Liquidating Trusts |

| 0.14% |

| Corporate Obligations (Debt) |

| 0.43% |

| Rights |

| 0.02% |

| Warrants |

| 0.09% |

| Money Market Funds |

| 8.16% |

The only things on this list that could possibly be considered fixed-income securities do not come anywhere close to the 80% of assets that the Morningstar description states. While it is true that both business development companies and closed-end funds can invest in fixed-income assets, they are not required to and a look at the actual portfolio reveals that there are a number of equity closed-end funds in the portfolio.

In particular, the fund has exposure to the Center Coast Brookfield MLP & Energy Income Fund ( CEN ), the Cushing MLP & Infrastructure Total Return Fund ( SRV ), the NXG NextGen Infrastructure Income Fund ( NXG ), the Saba Capital Income & Opportunities Fund ( BRW ), the Tortoise Energy Independence Fund ( NDP ), and the Tortoise Power and Energy Infrastructure Fund ( TPZ ). There are also a few blended funds in the portfolio that can invest in things other than traditional fixed-income securities. Morningstar actually confirms that the fund's bond holdings are minimal:

Morningstar

I do not know then why some sources are claiming that this fund will be investing at least 80% of its assets in fixed-income securities. It most certainly is not doing that.

With that said, the fact that this fund invests heavily in both closed-end funds and business development companies does fit both with its name and with the stated objective of providing investors with a very high level of current income. This is because both types of assets are very well known for the incredibly high yields that they pay out. As of the time of writing, the Saba Closed-End Funds ETF ( CEFS ) boasts a 10.37% yield and the Van Eck BDC Income ETF ( BIZD ) yields 10.82%. These are therefore among the only asset classes available in the market that deliver higher yields than an ordinary money market fund. They are also among the only things that actually deliver a positive real yield since the market as a whole is rather overvalued, and as such the inflation rate exceeds the yield of most asset classes. Unfortunately, the special purpose acquisition companies that comprised 17.06% of the portfolio as of the most recent earnings report are not nearly as attractive in terms of yield. They can deliver a decent total return if the sponsor manages to acquire the right company, though. As I pointed out in a recent article though, most special-purpose acquisition companies do not make particularly good investments over time. I would honestly be much happier if this fund were to ditch its allocation to these things completely and just invest in business development companies and closed-end funds that actually produce income.

One thing that we do note here is that the fund's allocation to preferred stocks has decreased since the last time that we discussed it. Back in March, the most recent data that was available about the fund's holdings was from August 2022. At that time, the fund had a 20.64% allocation to preferred stock. That figure has declined to 12.54% as of February 28, 2023, which is the date of the fund's most recent financial report. This is not exactly a bad move considering that interest rates seem poised to trend upward further, which will have a negative impact on the fixed-income markets and the price of preferred stock. In addition, the yields on most preferred issues are inferior to those of both business development companies and closed-end funds so the fund's shift to other assets could improve its income profile.

The fund's management appears to be betting on this overall scenario, since it greatly increased its allocation to money market funds (going from 3.86% to 8.16% over the period), which is the only asset category in the fund's portfolio that actually benefits from rising rates. The slightly higher allocation to closed-end funds and business development companies will also increase the fund's income slightly so that is something that we should be able to appreciate as investors.

Curiously, the change in the fund's holdings from preferred stock to money market funds has not resulted in a substantial turnover. The semi-annual report states that the High Income Securities Fund had a portfolio turnover of 27% for the six-month period that ended on February 28, 2023, which is not particularly high for a closed-end fund. The reason that this is important is that it costs money to trade assets, and these costs are billed directly to the fund's shareholders. This creates a drag on the performance of the portfolio and makes management's job more difficult. After all, the fund's managers need to earn sufficient returns to cover these excess costs and still deliver a performance that is acceptable to the fund's investors. The higher the fund's expenses, the larger the return that is necessary to accomplish this. In most cases, this results in actively-managed funds failing to beat comparable index funds.

Admittedly though, there is no index fund that is a direct comparison for the High Income Securities Fund. The fund's performance does look somewhat disappointing compared to many other things right now though as it is down 15.80% over the past twelve months:

{kind=link}

The fund's high yield does offset much of this decline, but it still delivered a negative total return over the period. This compares quite poorly to the S&P 500 Index (SP500) over the same period. Still, admittedly it is not totally out of line with the preferred stock and income securities index ( PFF ) or even the Bloomberg U.S. Aggregate Bond Index ( AGG ), which both beat this fund in terms of total return but not ridiculously so. The High Income Securities Fund also has a substantially higher yield than either of these indices, so the lower performance might be acceptable to an investor that is seeking income. We can see this quite clearly here:

{kind=link}

As we can clearly see, the High Income Securities Fund did deliver a worse total return than either of the indices, but the difference is not as much as might be expected. As the closed-end fund has a substantially higher yield, an investor that is desperately in need of income might opt to buy that fund over the indices.

Leverage

In the introduction to this article, I stated that closed-end funds such as the High Income Securities Fund have the ability to employ certain strategies that can boost the effective yields of their portfolios well beyond that of any of the underlying assets or indeed pretty much anything else in the market. One of these strategies is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase closed-end funds, business development companies, and other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. That could be one reason why this fund underperformed the indices during a period of rising interest rates. As such, we want to ensure that the fund does not employ too much leverage since that would expose us to an outsized amount of risk. I do not typically like to see a fund's leverage exceed a third as a percentage of its assets for this reason. Fortunately, the High Income Securities Fund currently satisfies this requirement as its levered assets consist of 1.06% of the portfolio as of the time of writing:

Morningstar

This is well below the level that I find acceptable. It is important to note though that while this fund may not have an excessive amount of leverage, it is invested in closed-end funds and business development companies that may employ leverage themselves. Thus, the actual impact of leverage on the portfolio's performance is almost certainly greater than the 1.06% level would imply. For its part though, this fund appears to be striking a reasonable balance between risk and reward.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the High Income Securities Fund is to provide its investors with a very high level of current income. In order to accomplish that task, the fund invests in a portfolio of closed-end funds, business development companies, and similar things that have very high yields. The fund takes that a step further and applies a layer of leverage to boost the effective yield of the assets. The fund then pays out all of its income to its investors. As such, we might assume that this fund will have a very high yield itself. This is indeed the case as the fund pays out a monthly dividend of $0.0604 per share ($0.7248 per share annually), which gives it an 11.27% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over time as it cut it back in January, following a string of cuts dating back to 2020.

The fact that the fund's distribution has not been particularly consistent might reduce its appeal in the eyes of those investors that are seeking a safe and secure source of income to use to pay their bills or cover their lifestyles. However, it is important to keep in mind that anyone buying today will receive the current distribution at the current yield. As such, the fund's past is not the most important consideration since a new buyer will not be negatively impacted by it. The most important thing today is the fund's ability to sustain its current distribution going forward. Let us investigate this.

Fortunately, we do have a somewhat recent document that we can consult for the purposes of our analysis. The fund's most recent financial report is the already mentioned semi-annual report corresponding to the six-month period ending on February 28, 2023. As such, it will not include any information about the fund's performance over the past few months. However, the document is much newer than the one that we had available to us the last time that we discussed this fund. It will also include information about the fund's performance around the end of 2022, which was a rather challenging time for income securities.

During the six-month period, the High Income Securities Fund received $4,571,493 in dividends along with $234,492 in interest from the securities in its portfolio. This gives the fund a total investment income of $4,805,985 during the period. The fund paid its expenses out of this amount, which left it with $4,184,430 available for the shareholders.

This was, unfortunately, not nearly enough to cover the $7,236,575 that the fund paid out in distributions during the period. At first glance, this is somewhat concerning since we usually like a fund to be able to cover its distributions out of net investment income.

However, a fund like this does have other methods that can be employed to obtain the money that it needs to cover its distributions. For example, it might have capital gains that can be paid out. The fund also receives distributions from other closed-end funds that might be classified as return of capital and so not included in net investment income. Unfortunately, the fund failed in this task on net as it reported net realized losses of $1,828,955 and had another $794,109 net unrealized losses.

Overall, the fund's assets declined by $5,675,209 over the six-month period after accounting for all inflows and outflows. This is obviously very concerning and explains why the fund cut its distribution earlier this year. The fund failed to cover its distributions through February, but it is uncertain how sustainable the new distribution will be. We will have to wait until its full-year report is released in a few months to update our analysis.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the High Income Securities Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of July 21, 2023 (the most recent date for which data is available as of the time of writing), the High Income Securities Fund had a net asset value of $7.49 per share but the shares currently trade for $6.44 each. This gives the fund's shares a 14.02% discount on the net asset value. This is better than the 13.02% discount that the shares have averaged over the past month, so the price certainly appears to be acceptable today.

Conclusion

In conclusion, the High Income Securities Fund is much less transparent than I would like to see. The fund's webpage is spartan and does not even include a downloadable fact sheet or prospectus, and much of the information listed about the fund's strategy from other sources appears to be incorrect. This is not a fixed-income fund, despite what some sources claim, but it is instead a fund of funds that invests mostly in business development companies and closed-end funds. It does appear to fulfill its goal of delivering a high level of income for the shareholders, though, as its assets are invested in things that generally deliver a high yield to shareholders. The biggest question here is whether or not the distribution will prove to be sustainable at the new level, and we do not have an answer to that question just yet. The fund is trading at a huge discount, but the lack of transparency and uncertainty about the distribution are still making me avoid it.

For further details see:

PCF: Lack Of Transparency A Big Negative