PAXS - PCM Fund: Pushing All-Time High Premium

2023-04-26 13:55:48 ET

Summary

- We tend to avoid funds when they trade at significantly outsized premiums.

- PCM is pushing near all-time high premiums in an area of the market that is susceptible to performing poorly in a bad economy.

- Due to an excessive premium, the distribution isn't even that enticing, and the sustainability is questionable at this time.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on April 25th, 2023.

Investors in PCM Fund (PCM) are really pushing their luck with the fund's current premium. We are reaching an all-time high premium while distribution sustainability is in question. Further, the distribution yield isn't even enticing in the first place with such an elevated premium. That's not even to mention the incredible risks at the moment for this highly leveraged fund that invests ~50% of its portfolio in non-agency MBS.

Thanks to the excessive premium pushing higher, the actual results for this fund, including its distribution since our last update , have been about flat.

PCM Performance Since Prior Update (Seeking Alpha)

However, you take away the premium expansion, and the results would have been firmly negative. This can be measured by the fund's total NAV return performance since that update.

For all these reasons, PCM should probably be avoided, and investors in the fund should consider exiting. I rarely come out with completely negative articles on funds, as I can often see some reason why investors may continue to remain invested. However, in this case, I simply can't find the positive case.

The Basics

- 1-Year Z-score: 2.73

- Premium: 42.48%

- Distribution Yield: 9.94%

- Expense Ratio: 1.68%

- Leverage: 48.40%

- Managed Assets: $156 million

- Structure: Perpetual

PCM is a lot like the other PIMCO offerings. Basically, they are all multisector bond funds with the flexibility to invest just about anywhere, anytime and anyhow. More specifically, though, the fund's primary objective is "high current income" with a secondary "capital gain disposition of assets as a secondary objective."

To achieve that, "the fund has the ability to invest in agency-guaranteed mortgage-backed securities, private-label mortgage-backed securities, investment-grade corporate debt securities, high yield corporate debt securities and commercial mortgage-backed securities." This pushes the fund often, but not always, into a heavier allocation to MBS holdings. At this time, it is roughly 52.74% of the market value percentage of the fund. High-yield credit makes up the second-highest exposure.

The fund has continued to shrink in terms of total managed assets as the actual underlying portfolio lost value, and they paid out an excessive distribution. So an already high effective leverage ratio simply moved even higher. In the last year, their borrowings went from around $84 million down to $67.6 million more recently.

For most PIMCO funds, high leverage is how they naturally operate, but during down periods that can be detrimental as they deleverage. The costs of their borrowings have also increased considerably in the last year as rates moved higher. The latest rates of their reverse repurchase agreements from their last available semi-annual report show anything from around 4-6%.

The fund's expense ratio comes to 1.68% but goes up to 4.73% when including leverage expenses.

Horror Show Reincarnate

With a fund like PCM, we can draw on past results to kind of reflect what could happen to this fund. To be fair, these are quite different funds. Additionally, history is never a guarantee of future performance; with that caveat, we can look towards its sister funds, PIMCO Global StocksPLUS&Income ( PGP ) and PIMCO High Income Fund ( PHK ).

These funds remain relevant because they had a similar history that PCM looks set to go through. PCM has maintained its high distribution rate even though it is unsustainable similar to PGP and PHK. PGP and PHK also traded at elevated premiums while investors were clinging to their high distributions. However, each cut brought a lower and lower premium for each of these funds.

Check out these horror shows in the charts of PGP and PHK below.

Ycharts Ycharts

We see this time and again, too. Funds that trade at unsustainable premiums paying unsustainable distribution rates often have poor endings. Each cut brings a lower and lower premium. PGP and PHK are certainly on the extreme end of these examples.

The problem with a reduced premium is that investors who bought ten years ago are looking at either negative or severely lackluster results on a total share price basis. That is with the reinvestment of distributions over the last decade. At the same time, their total NAV returns were still okay. It was simply due to massive premium declines that saw investors come out on the short end of the stick.

Ycharts

That's precisely why PCM looks precarious today as it pushes to an all-time high premium.

Ycharts

The Catalyst To Kick Off The Horror Show

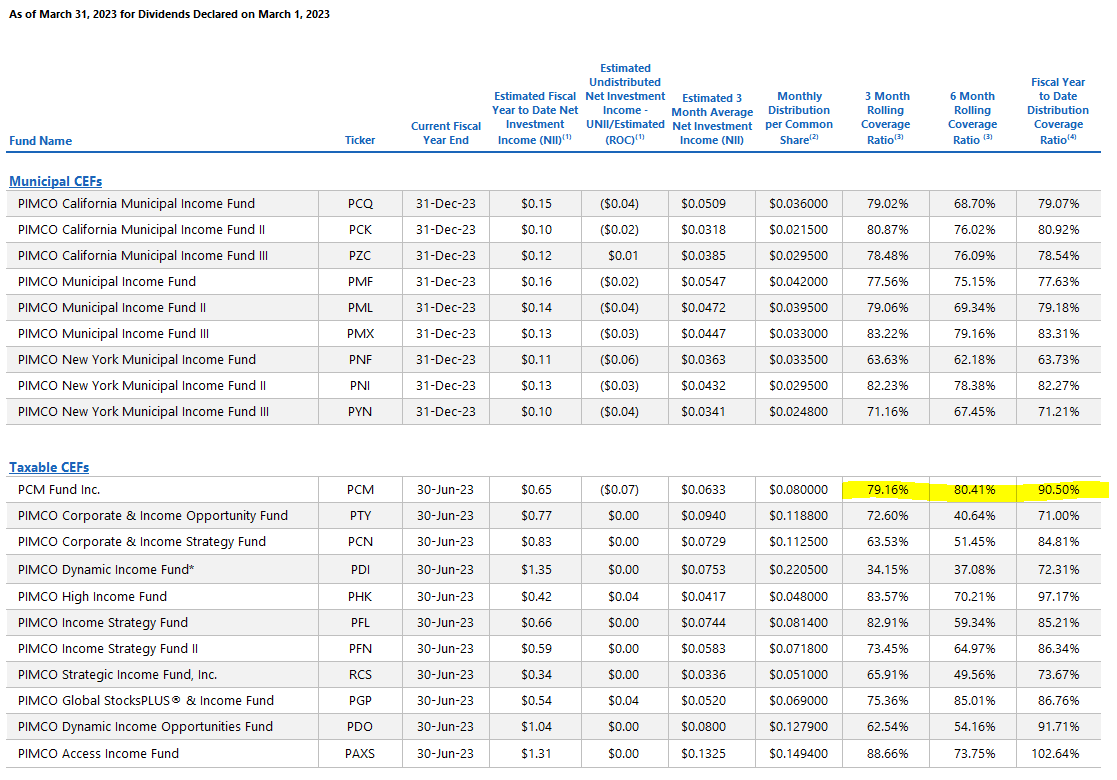

The latest UNII report from PIMCO shows that none of the PIMCO funds are excelling. However, only PCM is also carrying the characteristic of an exceptionally out-of-the-ordinary premium. The other PIMCO funds have poor coverage but also mirror that with below-ordinary discount/premium levels.

This distribution coverage also dropped sharply from the ~113% 3-month rolling coverage ratio we saw in our prior update. The impacts of leverage seem to be taking their toll, both in terms of higher costs and lower amounts. However, some timing is always going to play a factor.

{kind=link}

The other piece of this that I find quite interesting is that normally investors do chase high yields. However, due to this excessive premium, the fund's actual distribution rate currently is 9.94%. Compare that to the fund's distribution NAV yield of 14.16%. That 14.16% plus the fund's expense ratio is what they have to earn to maintain the current rate and consider it sustainable or covered.

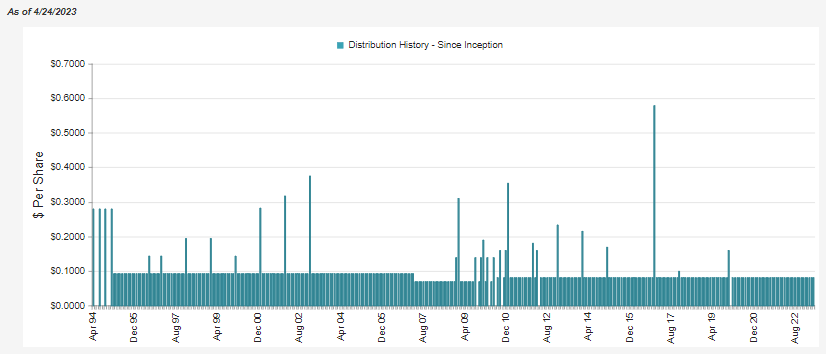

The steady distribution is fairly attractive, but for these reasons, I find the current levels unsustainable.

{kind=link}

If we get into a recession within the next year, the fund's heavy emphasis on non-agency MBS could put further pressure on the fund. PCM is almost focused entirely on below-investment-grade forms of fixed income, which will see higher defaults overall. Combining that with the potential for more deleveraging in an adverse economy, PCM looks risky but is priced as though it's bulletproof.

PCM Portfolio Allocation (PIMCO)

Conclusion

PCM looks to be incredibly richly valued at an incredibly precarious time for its distribution. PCM should probably be avoided at this time. History showed us the horror show that can play out through its sister funds PHK and PGP over the last decade.

While the PIMCO suite isn't showing strong distribution coverage on any of their funds, funds such as PIMCO Dynamic Income Opportunities Fund ( PDO ) or PIMCO Access Income (PAXS) are showing much more favorable valuations. They are at discounts and actually carry distribution rates higher than PCM.

However, due to trading at slight discounts, the NAV distribution rates are still coming in lower at 11.92% and 11.79%, respectively. While those may need to be trimmed, the downside moves would be anticipated to be much lower, and the adjustments are likely to be much less than a fund that is carrying a 14.16% NAV distribution rate.

Sticking to the same area of mortgages, there is also Western Asset Mortgage Opportunity Fund ( DMO ). I'm not overly optimistic about that fund either, but its valuation is much more tempting. Once again, its distribution rate is higher relative to PCM, while the NAV distribution rate is also substantially lower. It also isn't covering its distribution, but the idea would be it's already at a hefty discount, and a cut could be much less.

Will PCM cut its distribution? Who knows. That is anyone's guess, but we can clearly see the ugly results that its peers went through should they do so at the current valuation.

For further details see:

PCM Fund: Pushing All-Time High Premium