MD - Pediatrix: RCM Overhang Now Too Heavy Revise To Hold

Summary

- Repositioning cross-asset and equity-focused portfolios has been a challenging affair in the latter half of FY22.

- Such has been the case for longs of MD, where the investment debate how now is negatively skewed to the downside.

- MD is faced with a series of hurdles to ramp up its billing and collection processes following its RCM transition.

- There are now more selective opportunities for efficient capital allocation elsewhere.

- Revise rating from buy down to hold, price target range $14–$15.

Investment Summary

Repositioning cross-asset and equity-focused portfolios has been a challenging affair for active investors in the latter half of FY22. A series of thematic rotations [both into and out of various sectors/factors] has coupled with volatility and broad-based selling across risk assets. With the main drivers of asset returns now tied to a culmination of macroeconomic forces [namely, central bank tightening, liquidity, global capital allocation and of course, inflation data] its unsurprising to see some of our healthcare longs turn against the grain in the near-term. On this point, and in the interests of efficient capital allocation, it is essential to trim losing positions swiftly and redistribute the cash to more selective opportunities.

Such has been the case for our position in Pediatrix Medical Group ( MD ), where the investment debate how now is negatively skewed itself to the downside. Following our last two publications on MD [see here , and also here ], where we were bullish, we've observed the company miss key growth percentages in its latest numbers and this trend looks as if it were to extend into the coming 12 month period as well. Considering these points, I'm here today to discuss our latest examination findings on MD, and demonstrate why we've revised our call on the stock from a buy to hold for the time being.

As a reminder, our bullish thesis on MD was built on the following main factors:

- MD's bottom-line fundamentals looked increasingly attractive at the time.

- The company's transaction volume remained relatively sturdy amid an increasing cost of capital.

- Divergence in forward EPS estimates to share price, potentially resulting in a re-rating to the upside.

- Valuations also supportive at $33 per share from internal calculus.

Switching to the present form, the bulk of these upside drivers have either reversed of left the party, resulting in a substantial hangover for the MD share price. Net-net, we revise our rating from a buy to hold, hoping to re-enter on the improvement of broad-market, company fundamentals.

MD's Q3 misses not even a near hit...yikes

The headline takeout from MD's latest set of numbers was that it missed internal, consensus revenue estimates by a staggering amount, with EPS falling behind by $0.11 per share, or 15% to the downside.

In a disheartening performance, revenue of $489.92mm slipped 60bps YoY, with the deficiency of ~$22mm versus consensus as mentioned. Similarly, we'd also advise that adjusted EBITDA missed the mark by approximately $19 million.

The worse-than-expected growth period was underlined by the difficulties MD continues to face in its transition of integrating R1 RCM (NASDAQ: RCM ) as its provider of revenue cycle management ("RCM") services. [Note: we've covered R1 in detail previously, rating it a buy. To view this publication, click here .]

As you may or may not recall, the pair signed a definitive agreement in 2021 for R1 to provide enterprise RCM services for MD. To date, MD hasn't managed to successfully integrate the new system into its core operations, but has experienced a series of pitfalls regarding the same over the last two quarters. Whereas previously, we had projected MD to deliver on this new transition, we've yet to see this convert to top-bottom line growth. Instead, it's been quite the opposite in FY22 [Exhibit 1].

Exhibit 1. MD continues to face headwinds from its RCM transition. Trailing FCF yields creeping up, however, still lagging FY21 numbers substantially

Data: HBI, Refinitiv Eikon, Koyfin

{kind=link}

In turn, MD is faced with a series of hurdles to ramp up its billing and collection processes, thereby hurting cash flow and revenue gains in this last and future period[s]. Problem is, this trend has been in situ for basically the entirety of this year, and we estimate it will have an impulse effect into the coming 12 months. We'd note, this YTD, the estimated detrimental impact on revenue from these headwinds lies in a range of $25mm-$30mm [~$0.36/share], and a decrease in adjusted EBITDA of $15mm-$17mm [~$0.20/share].

As a result of these growth compressors, the company has now implemented strategies to reduce overhead expenses at the corporate level. These efforts are anticipated to result in annual savings of $12mm-$14mm in general and administrative ("G&A") expenses, starting in Q4 this year. What this means for future growth in operating leverage, earnings, and free cash conversion remains to be seen, but it's certainly a risk factor in our opinion.

Moreover, it's worth highlighting that, despite exiting Q3 at 2.9x leverage [adjusted EBITDA/debt], plus management's efforts in utilizing "$88mm in operating cash flow" to repay its outstanding credit revolver in Q3, MD still has an overall debt service of $739mm, ~35% higher than 12 months ago. Certainly, it looks set to cover its interest payments, but trading at 1.4x book value looks far less appealing with a debt/equity of c.95%.

Consequently, the case for MD to deliver meaningful EPS upside looking ahead is substantially weaker in our opinion. Without the bottom-line growth in the investment debate, our buy thesis is therefore nullified.

Additionally, we don't see the company's challenges concerning its RCM to avail anytime soon, posing greater risk to capital appreciation in its share price. An outperformance in this regard would, however, be an upside risk in the investment debate.

MD technicals and valuation

As you'll see in the chart below the stock has broken key support levels and now trades in a sideways consolidation. Whereas we were hoping for the stock to break past the 50% retracement level in the Fibonacci series below, it broke the floor of support in November and hasn't recovered since. At the same time, buying volume is drying up substantially.

The presence of sideways price action and declining volume is evidence of heavy resistance in our opinion.

Exhibit 2. MD Weekly price action, breaking key support levels, with volume eroding and price action flat

{kind=link}

It's no wonder, therefore, to see shares trading below cloud support, with the lag line in heavily bearish territory. Further headwinds are observed via the declining on balance volume trend and sub-par momentum studies. Again, this is supportive of our change in thesis.

Exhibit 3. Trading below cloud support with lack of support from long-term volume, momentum studies

Data: Updata

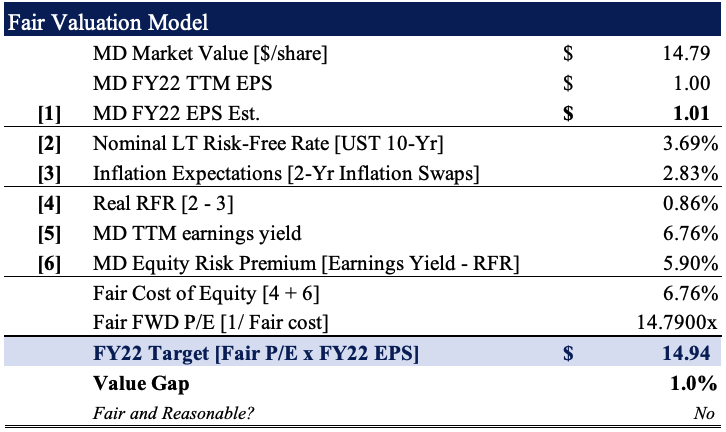

We therefore have technically and fundamentally derived price targets hovering around the $14-$15 mark, around 50% behind our previous objectives. This is formed by our FY22 EPS growth assumptions of $1.01, well below consensus estimates. We arrive at this number with FY22 sales estimates of $1.96Bn on adjusted EBITDA of $240mm. Alas, these targets also confirm our neutral viewpoint.

Exhibit 4. Fair forward P/E of 14.8x FY22 EPS Est. $1.01 = $14.94

{kind=link}

Exhibit 5. Targets around the $14.10 mark yet to be activated, with downside targets to $6.60

Data: Updata

In short

In the absence of previous growth drivers we had identified as potential catalysts to MD's share price, there is no option but to revise our thesis to a hold. Chief to the revision is the company's challenges in integrating its new RCM systems, which have dragged on for the entirety of this year. It gets to the point where it's a question of opportunity cost, and where capital can be allocated more efficiently elsewhere. Rate hold, price target range $14-$15.

For further details see:

Pediatrix: RCM Overhang Now Too Heavy, Revise To Hold