RCM - Pediatrix: Unable To Deploy Capital Tied Up In Cash Conversion Cycle Reiterate Hold

2023-08-08 08:21:03 ET

Summary

- Pediatrix Medical Group's Q2 FY'23 numbers fell short of internal expectations.

- The company's financials, business economics, current sentiment, and valuation pose notable headwinds for future capital growth, in my view.

- Sentiment is neutral, with downward revisions to earnings estimates and minimal demand for calls, supporting a hold rating.

- Net-net, reiterate hold.

Investment update

Pediatrix Medical Group ( MD ) posted its Q2 FY'23 numbers last week, and on detailed examination, there is much to be desired for the company's investment prospects.

Based on the analysis shown here today, it is of my belief MD is not an investment-grade company at this point. The revenue cycle management ("RCM") overhang I detailed in my last two publications remains in situ (see: here , and here ). This continues to impact the P&L, and is clamping the degree of earnings/cash flow growth I'd expect to see to be long its equity stock. Net-net reiterate hold, eyeing $1.35Bn market valuation, or $16.35 per share.

Figure 1. MD vs. equity benchmark divergence remains, yet is narrowing with recent corrections.

Data: Updata

Updates to critical facts

Starting with the latest numbers, there are notable headwinds that limit the investment upside going forward in my view. These relate to the company's financials, its business economics, current sentiment, and valuation.

1. Q2 numbers softer than expected

Starting with the company's latest numbers , MD missed consensus estimates at the bottom line. It clipped $500mm in turnover on adj. EBITDA of $59mm and $0.40 in adj. earnings. Revenues were therefore up just 280bps YoY, well behind where I need MD to be in order to advocate a buy.

Moreover, the company projects $245mm in adj. EBITDA for the year, meaning it is ~40% of the way there at the halfway mark (the YTD number is $91.177mm). As such, it expects the remaining 60% of projections from the remainder of the year.

The question is whether this is feasible or not. As an exercise, I've gone back and checked the potential seasonality of MD's pre-tax income since 2020 and observed where it stood at H1 and then H2 along the way up until last quarter. As you'll note, it is at ~40% of projected EBITDA isn't unusual for the company at H1 of any given year (in the last 3 at least). It was at the same mark in 2021, for example. Therefore, $240mm could very well be the number to look for FY'23.

Figure 2.

Note: The percentage of EBITDA booked at each half-year period (H1 and H2, respectively) are shown via the blue bars. The actual reported EBITDA is shown in black, and is presented in '. (Data: Author, MD SEC Filings)

Breaking down the top-line, I'd call out the following:

- Same-unit revenue (those units booking sales in at least Q2 this year and Q2 FY'22) were up ~320bps and brought in an additional $15.3mm.

- Just 60bps of this growth, or c.$3mm, was related to patient service volumes. The remainder stemmed from "net reimbursement-related factors", namely, the company's incentive compensation plan.

- As a headwind, the 60bps growth in patient volumes was the net figure after baking in declines in its hospital paediatric services.

- Salaries and clinical compensation costs, booked under the continuing operations line, were up 7% to $354mm. This disaggregates to $13mm more in salaries and $10mm extra in incentive compensation.

Therefore, you've got an extra $35.5mm in incentive and personnel-related costs on just $14mm growth in turnover. This tells me these costs have added a lot of overhead while adding little value.

2. Collections improving, but not there yet

If you've been following the MD story to date you'd know it has faced troubles in integrating R1 RCM ( RCM ) to provide its RCM services (I've rated RCM a buy in the last 3 publications, see the latest here ). Specifically, billing and cash collection have been impacted enough to crimp sales and free cash flow growth.

To illustrate the hurdles MD must overcome here, I've outlined several critical elements in Figure 3:

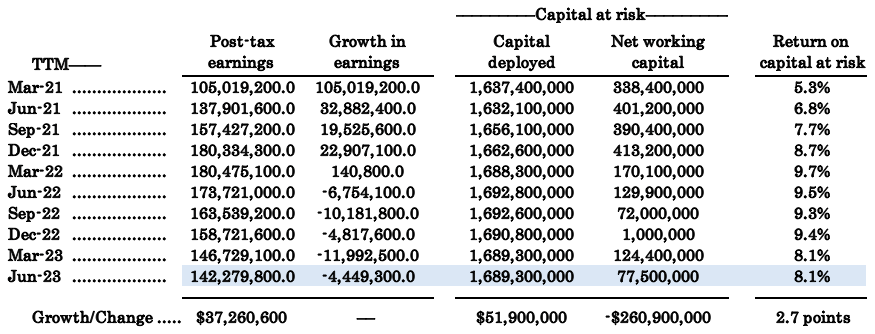

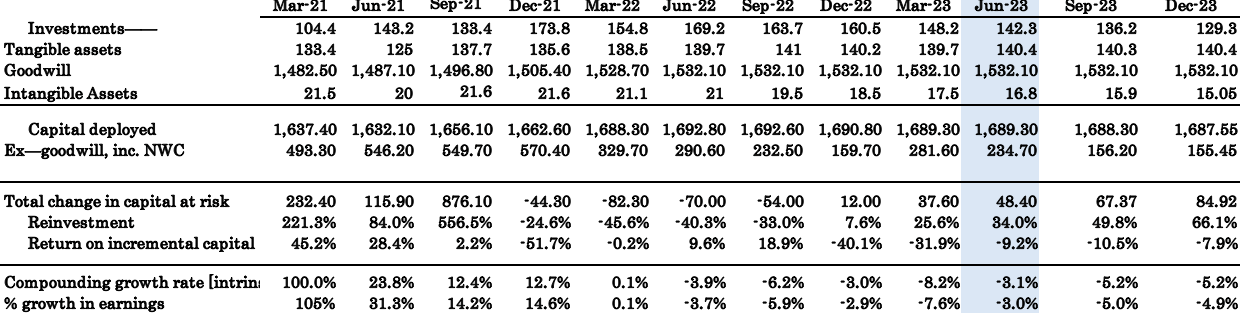

- Just looking at the capital deployed over the last 2-years, from March 2021-date, it has invested an additional $51.9mm to growing the business.

- It has produced an additional $37.3mm after-tax income off this, a reasonable rate of return, had we not had to include all the cash tied up in working capital.

- Doing so, you'll note the company has realized ~5-9% trailing return on all capital at risk each period. I am looking for my companies to beat the market return on capital, benchmarked at 12% given the long-term market averages.

The economic earnings - ROIC less 12% - MD has produced over this time, therefore, have hovered in the realms of negative 4-5%, and thus not an attractive proposition in my eyes. Given that market returns closely resemble business returns over the long term, a return on capital below the market benchmark of 12% is an opportunity cost, and thus destructive to the company's valuation (this is shown later).

Figure 3.

{kind=link}

Most critical to this piece of the discussion is the observance on NWC delta as it relates to the company's RCM. Collections have increased in the last two periods, with the company converting ~$29mm from accounts receivable to cash this YTD. This shows that days AR outstanding reduced to 49 days, from 53 days in December last year.

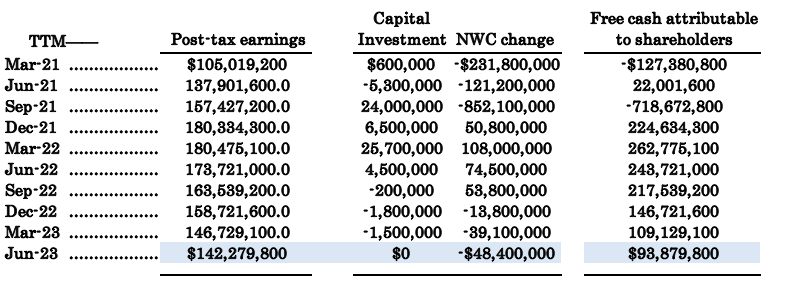

On a TTM basis, you'll note the cash outflows this has resulted in for the company from December FY'22, below. In total, it had an additional $100.8mm tied up in working capital as a result of this (TTM values). That's $100mm less for shareholders, or to be put back into more profitable ventures, instead of being held up in the cash conversion cycle.

Figure 4.

Note: Negative changes in NWC represent cash OUTFLOWS, and vice-versa. (Data: Author, MD SEC Filings)

{kind=link}

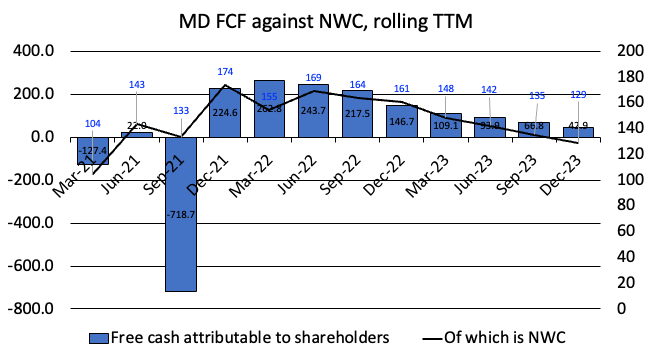

As a result, even with the marginal improvements in free cash attributable to shareholders each period, the bulk of delta each way is still resulting from changes in NWC density and thus not related to factors such as sales growth, return on capital deployed, or even efficiencies. It is more a working capital function. Nothing in my analysis suggests these trends will reverse in the medium term. This isn't the kind of business economics I'd like to position against.

Figure 5.

{kind=link}

3. Sentiment unsupportive

Positive (or negative, for that matter) changes in sentiment are critical to see a stock reprice higher (lower). Neutral sentiment is a function of the same things. We observe MD's neutral sentiment in a few ways.

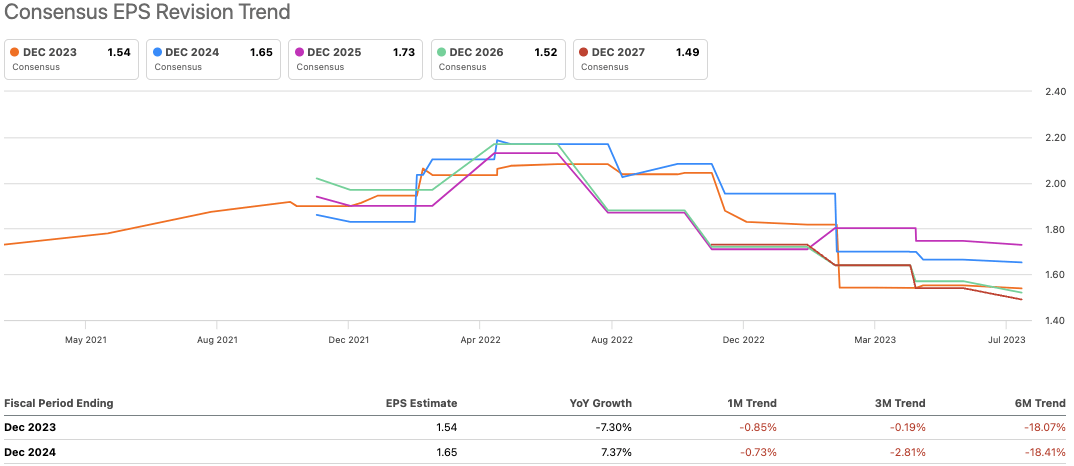

One, the revisions to Wall Street estimates. Granted, there is often a lag on these, so I'd expect some of these to change further into the weeks ahead following MD's numbers. Still, there is no denying the trend on analyst estimates has been pushing lower for the last 3 months. There have been 3 revisions down to earnings over this time, and consensus sees $1.54 per share in FY'23, down 7%, with $1.65 in FY'24, just a 7% upside. These aren't attractive growth percentages in my view. A whole substrata of the market populous use these numbers, so we've got terrific insights here.

Figure 6.

{kind=link}

Two, options-generated data suggests investors are positioned neutrally at best. Put contracts expiring in both August and September have the most open interest around the $15 strike depth. There's minimal demand on the calls ladder to offset this. Moving to September alone, all demand is on $15 on a call/put parity. This may reflect a condor strategy to capture premiums where investors expect the stock to push sideways into congestion. Or, it may just suggest balanced positioning for in-the-money contracts. Either way, both support a neutral view.

Three, the stock trades roughly in line with all its respective moving averages. That it trades in this range tells me it is trading basically in line with its average price points at each of these durations (10, 50, 100, and 200 days, respectively). Trading at the average price means investors aren't throwing bids above the price line at any respective time frame, thus supporting a neutral view.

4. Valuations corroborate neutral view

Investors are parting ways with their MD stock cheaply at 9.5x forward earnings. Some 'relative value' investors might see some opportunity in these compressed multiples. But I'm not convinced. The market does a pretty good job at pricing the laggards, and all we've discussed thus far implies the company may deserve to trade at a 53% discount to the sector at 9.5x forward.

I'd also point out that investors have basically priced no premium to the company's net assets, instead trading it at 1.16x its book value. It would make sense too, because so much of MD's capital is tied up as working capital, not as intangible or tangible assets. This tells me the market does not value the company's net assets highly - contrary to my first principles investing style. I want to buy companies where the market values its operating capital and book value at obscene multiples, given the profits each produces for its investors. Not the case here.

Further, a company can compound its intrinsic value roughly at the rate of its returns on capital and the amount it reinvests at these rates of return (i.e.: compounding value = ROIC x reinvestment rate). A few points on this for MD:

- Its after-tax earnings growth has closely matched the compounding rate of return outlined above. I've used the incremental returns on capital to capture the periodic movements.

- Critically, I've penalized the company for its goodwill charge, as it is a transfer of wealth from MD shareholders to all target shareholders.

- What is concerning in my view, is that when you strip out the goodwill capital charge, the company only boasts a meagre $234mm in capital invested (inc. NWC). That's only 13.2% of its entire capital commitments, meaning the remaining 86.8% stems from goodwill, a non-cash, non-operating asset. That equals a negative tangible book value of $606mm as well, by the way.

- Moving forward, my assumptions have a further decline in intrinsic value by ~5% per quarter into H2 FY'23.

As a result, I do not see a major reversal in equity value on the back of this.

Figure 7. Note: Estimates into H2 FY'23

{kind=link}

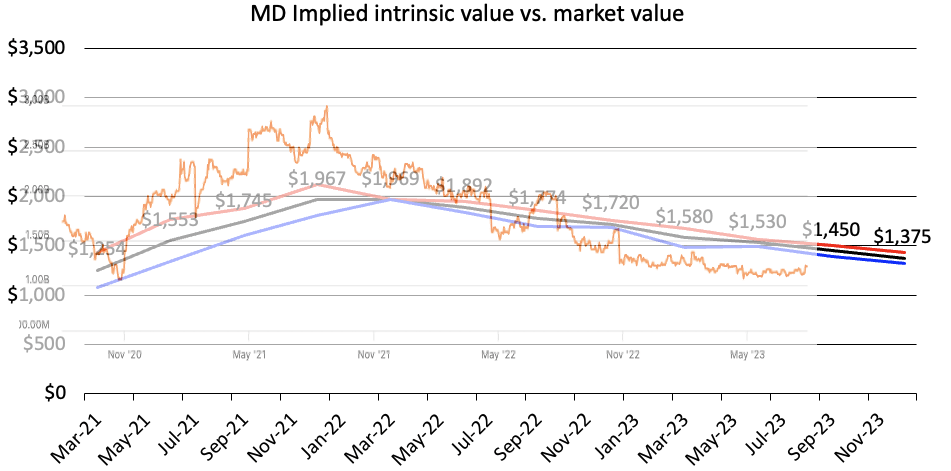

You can see how this may or may not play out in Figure 8. Based on the implied calculus above, I've got the company pushing an implied market value of ~$1.35Bn by FY'23, with a standard deviation of $1.428 and $1.3Bn to the upside and downside respectively. This is within range of the current market value, and thus it would appear, on my assumptions, the market has more or less correctly discounted the company's value at its current mark of ~$1.21Bn as I write. This supports a neutral view.

Figure 8.

Note: The image is the market cap line (orange), retrieved from Seeking Alpha, superimposed over the implied intrinsic value line (black). This is why the image is slightly faded. One standard deviation above and below are shown in red and blue, respectively.

{kind=link}

In short

As seen in this report, I've stuck the probe in multiple times at multiple angles for MD and found little to suggest it is a resounding buy. Instead, my estimates are that its cash collection headwinds may continue in the medium term, hindering its ability to deploy capital and produce additional profits at attractive rates of return. I've got the company throwing off $43mm in owner earnings this year, just a 3.5% forward FCF yield if buying it today. That, and the fact it still has so much capital tied up in its cash conversion cycle hinder my investment cortex from firing up and executing a position here. MD has a lot to do in order to convince us it is an investment-grade company in my view. Net-net, reiterate hold.

For further details see:

Pediatrix: Unable To Deploy Capital Tied Up In Cash Conversion Cycle, Reiterate Hold