PNNT - PennantPark: Attractive Yield At A Discount

2023-10-13 10:18:56 ET

Summary

- Pennant Park Investment (PNNT) has a seasoned investment team whose portfolio has shown resilience during market crises.

- The firm's portfolio is currently benefiting from rising interest rates, given its floating-rate investments.

- The stock is trading at a discount to NAV and offers a high yield, making it an attractive option for investors.

Trading at a discount to NAV and benefiting from rising interest rates, PennantPark Investment ( PNNT ) looks like a nice option for investors looking for a high yield.

Company Profile

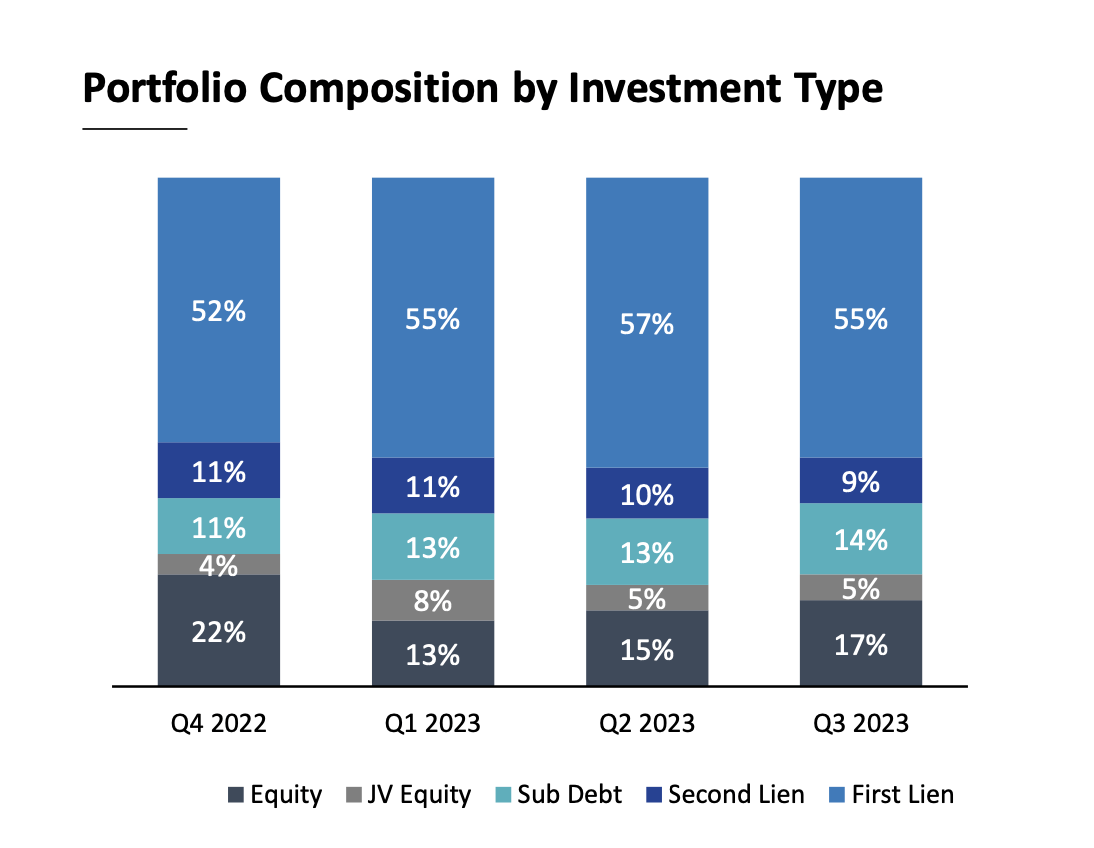

PNNT is a business development corp ((BDC)) that invests in the debt and equity of middle-market companies. The firm will invest across the capital structure, with investments in first lien secured debt, second lien secured debt, subordinated debt and equity. At the end of June, about 55% of its investments were in first lien secured debt, 17% was in equity, 14% was in subordinated debt, 9% was in second lien debt, and 5% was in JV equity.

{kind=link}

PNNT has a diversified portfolio, with investments in 129 different companies. Its average investment size is $8.3 million. The company will invest across a variety of sectors. It is largest at the end of Q3 was Business Services at 18.7%, followed by Healthcare, Education & Childcare at 12.0%, Consumer Products at 8.8%, Distribution at 6.2%, and Media at 5.5%.

The firm also has an unconsolidated joint venture with Pantheon Ventures called PennantPark Senior Loan Fund (PSFL) where in invests in directly originated middle-market first lien loans. This portfolio has investments from 92 companies with an average investment of $8.6 million. All loans are first lien and floating rate.

Opportunities & Risks

The stock of a BDC is only as good as its investment portfolio, which is in many cases is only as good as the firm’s investment team. PNNT is headed by Arthur Penn, who has overseen the firm since he founded it and took it public in 2007. The fact that it is still around and paying robust dividends after a number of market crises over the past 15 years, including the housing collapse and Covid, shows a seasoned team that can navigate tough markets.

PNNT tends to invest in companies that generate between $10-50 million in EBITDA, so they are on the smaller side. Smaller companies, even in more resilient industries, can be more prone to economic conditions, as they generally have less resources. PNNT is also providing debt, and these companies tend to have a fair amount of leverage of between 4-6.5x.

Meanwhile, PNNT also takes on leverage itself. As such, strong underwriting is of utmost importance, and investments going bad is one of the biggest risks a BDC faces. On that end, the company currently only has one investment on non-accrual status, representing 1% of the cost of its portfolio and 0% on a fair value basis. Loans are put on non-accrual status when a portfolio company misses payments by 30 days or more.

PNNT has generally been good with underwriting and protecting capital. During the height of Covid, it has only two portfolio companies out of 80 on non-accrual status on September 30 th 2020, although they did represent 4.9% of its portfolio at fair value. Given that difficult period, that is pretty impressive. Currently, all of its originated first lien loans had meaningful covenants, which the company attributed to its default rate during COVID being so strong. However, the firm is not perfect and has made some mistakes in the past, particularly in the energy sector.

Of its debt investment, about 96% of its loans are floating rate, which should benefit the firm in the current environment. The company has seen its weighted average yield to maturity increase to 12.7%, up 12.1% from last quarter and 9.3% from last year. It was originating new loans with an average yield of 12.6%. Those are some nice returns.

The risk, of course, is if the Fed shifts course and starts cutting rates, or the heavy interest rates become too burdensome for its portfolio companies. Right now, the latter does not seem to be in the imminent future, as the Fed continues to focus on cooling inflation.

Commenting on the current market environment on its Q2 earnings call , CEO Arthur Penn said:

“Now let me turn to the current market environment. From an overall perspective, in this market environment of inflation, rising interest rates, geopolitical risk and a potentially weakening economy, we are well positioned as a lender focused on capital preservation in the United States where floating interest rates on our loans can protect against rising interest rates and inflation. We continue to believe that our focus on the core middle market provides to the company with attractive investment opportunities where we are important strategic capital to our borrowers. We have a long-term track record of generating value by successfully financing high-growth middle market companies in 5 key sectors. These are sectors where we have substantial domain expertise, know the right questions to ask and have an excellent track record. They are: Business services, consumer, government services and defense, Healthcare and software and technology. These sectors have also been recession resilient and tend to generate strong free cash flow. In our software vertical, we don't have any exposure to ARR loans. In many cases, we are typically part of the first institutional capital into a company and the loans that we provide are important strategic capital that fuel the growth and help that $10 million to $20 million EBITDA company grow to $30 million, $40 million, $50 million of EBITDA or more.”

PNNT also generally likes to make equity co-investments when it invests in a portfolio company to be able to participate in its upside. Since its inception, the firm has generated an IRR of 26% and a multiple on invested capital of 2.2x. Now, how a portfolio company is performing can affect the carrying value of both equity investments as well as its debt investments. This is in turn can cause its NAV (net asset value) to go up or down. Last quarter, the company saw its adjusted NAV rise 3.1% to $7.67 from $7.44.

However, earlier this year it saw a big decline in NAV due mostly to a long-time investment in RAM Energy going south. Earlier in the year, it had meaningfully written it up, only to see a disappointing well result and sales process. This was a legacy investment, and PNNT now shies away from investing in energy companies.

Finding attractive investment opportunities is another opportunity and risk type of situation. In certain environments, deal flow can dry up, while its others, a BDC like PNNT can find a lot of attractive opportunities. When the latter happens, it often gets better rates and terms. That appears to be the case now, with the firm saying for new deals that “leverage is lower, spreads and upfront fees are higher, and covenants are tighter.” PNNT’s JV gives it even more opportunities to pursue deals.

Conclusion

Similar to mortgage REITs, I like to value BDCs based on a price to book multiple. On that basis, PNNT is trading at a 0.83x adjusted book. That’s a nice discount, especially considering that book value has stabilized and has now started to go up after the issues with the RAM investment, which has been closed.

At the same time, PNNT continues to see its net investment income ((NII)) climb along with interest rates given its floating rate loans investments. The company has also moved to a monthly dividend payment recently, increasing its dividend by 5% and declaring a 7-cent a month dividend for October. That’s good for a 13.2% yield. With core NII per share of 22 cents last quarter, the dividend has a coverage ratio of 1.05x.

Overall, I find PNNT’s valuation and yield attractive, and think it could have solid upside to close to book value, to go along with its current 13% yield. As such, I will start the stock off with a “Buy.”

The biggest risk for the company would be a shift at the Fed if they suddenly start lowering rates, or an economic slowdown that puts stress on its portfolio companies.

For further details see:

PennantPark: Attractive Yield At A Discount