PNNT - PennantPark Investment: Buy For Dividend Treat As Cyclical

2023-12-04 05:12:11 ET

Summary

- PennantPark Investment Corporation is a business development company that primarily invests in smaller, non-public companies in the core middle market.

- PNNT's main attraction is its dividend, currently around 13%, making it a potential buy for income investors.

- The company has weathered challenging environments, such as the Great Recession and COVID, but its dividend may fluctuate based on interest rate cycles.

PennantPark Investment Corporation ( PNNT ) is a business development company or BDC. As such, it primarily invests in smaller, non-public companies, giving owners of PNNT exposure to those opportunities. PennantPark's primary target is the core middle market, which it defines as businesses whose earnings range between $10m and $50m annually. These investments are typically secured loans, often with equity co-investments.

Like many BDCs, it is also a registered investment company or RIC. Similar to a REIT, RICs must distribute 90% of their earnings as a dividend to shareholders. PNNT's primary attraction is, therefore, its dividend, and I will make the case that PNNT is a BUY for those that like its yield, currently around 13%, provided that they find the downside of cyclical risk to be acceptable.

History

Hitting the Ground Running (2007 - 2012)

The company was founded in 2007 by Art Penn. Shortly after being incorporated in 2007, capital markets began feeling the strain of the subprime mortgage crisis that began that year. While this posed challenges, it opened a wide door for a business looking for middle market players in need of capital. In their 2009 annual report, they wrote:

The overall leveraged finance market has continued to experience pressure which has resulted in depreciation on some of our existing assets and improved risk/reward environment for new investments. We did not experience compromised liquidity during the turmoil in the global credit markets because of our ability to sell our senior secured loans and availability under our credit facility and our ability to access the capital markets to sell common stock.

The company was well positioned to seize on an investment opportunity that presented itself, as traditional lenders (whose balance sheets were devastated by toxic assets) were unable or unwilling to invest in these middle market companies. This created greater demand for PennantPark's capital, allowing them to invest with higher yields, more collateral, and stronger covenants.

PennantPark captured quality customers during this period and built up from there. It reported 38 different companies in its overall portfolio at the end of 2007 and 54 in 2012. As the company took off, it began to deliver on its mission to distribute dividends.

{kind=link}

Middle Years (2013 - 2019)

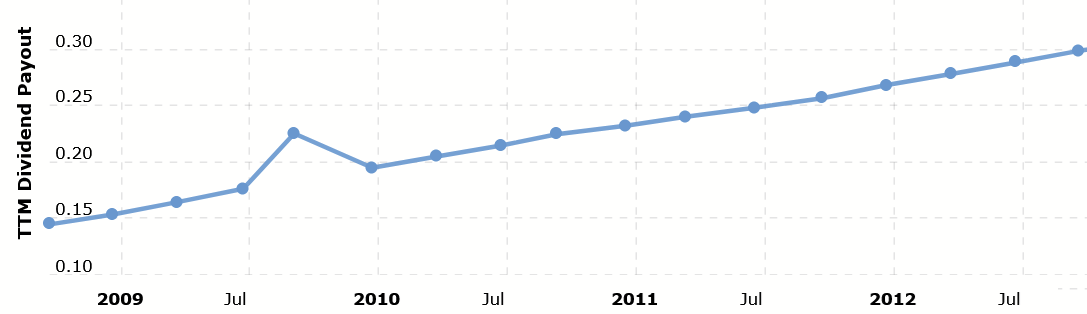

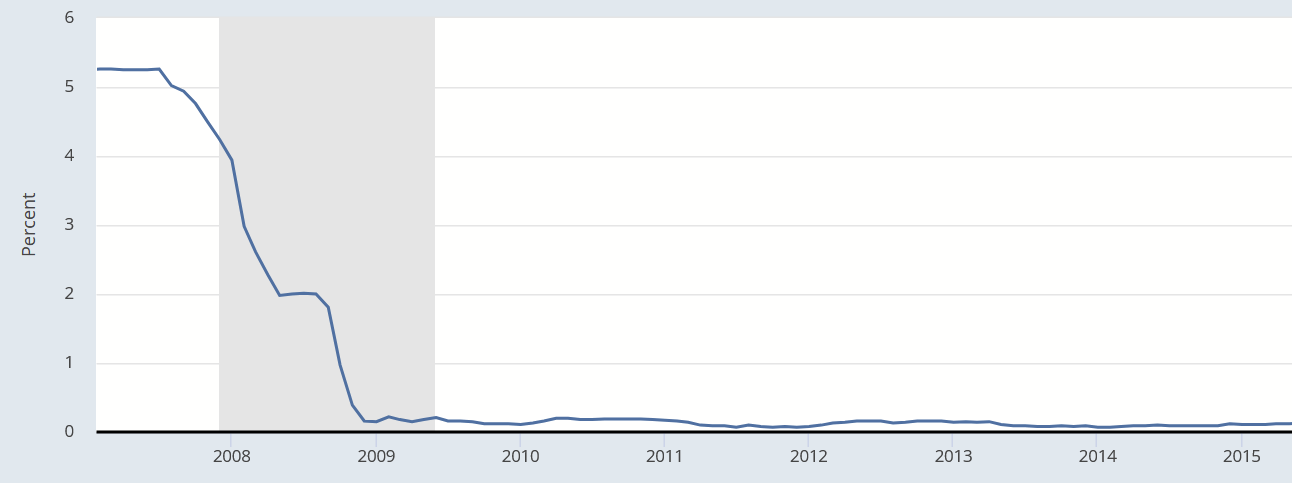

This period saw the peak of its annual dividend and was accompanied by continued growth of its customer base and a shift from fixed-rate debt toward variable. Fixed accounted for as 61% of their loans in 2011 to only 13% by 2019. Considering low interest rates had fallen to near-zero, it's not a surprise they made this shift.

{kind=link}

The company's variable loans are floating rates, which establishes a floor but allows them to ride the upside as prevailing interest rates increase during a loan's lifetime.

In 2017, the company's annual dividend fell from $1.12 to $0.72. Management forewarned this in the Q4 2016 earnings call:

With regard to our dividend, our Board and management regularly evaluate the earnings power of the company relative to the dividend. Given the continued weakness in energy and overall yield compression in the market, we've concluded in consultation with our Board that it is prudent to pay our $0.28 per share dividend for the December 2016 quarter and then reduce the dividend to $0.18 per share for the March 2017 quarter.

We're all personally disappointed regarding this reduction, which is our first dividend reduction in our nearly 10-year history, in spite of the fact that we went public prior to the great recession. This is undertaken with a great consideration and we believe it is the right decision at this time. This should allow us to return to the environment, where we expect to continually earn or exceed our dividend through net investment income with gains contributing to long-term NAV growth.

Simply put, the risk-reward opportunities, for a variety of reasons, resulted in lower earnings. The company did not become unprofitable, but this period proved the limits of dividend growth.

Recent Years (2020 - Present)

The onset of the COVID pandemic in 2020 strained PNNT's portfolio. They remained profitable, but earnings were still lower. The quarterly dividend had to be cut again to $0.12. In their 2020 10K, they reported:

Investment income for the year ended September 30, 2020 was $100.2 million and was attributable to $63.4 million from first lien secured debt, $25.9 million from second lien secured debt and $8.7 million from subordinated debt and $2.2 from preferred and common equity. The decrease in investment income over the prior year was primarily due to a decrease in LIBOR as well as an increase in our equity portfolio.

The cut therefore had more to do with this. Only two companies were on non-accrual for that year, accounting for less than 5% of their portfolio and too little to explain that much of a dividend decrease. These factors indicate that PennantPark's portfolio was structured with a mind to capital preservation first and foremost, which it successfully accomplished. The issue, of course, was the yield.

With deals declining in 2020, new investments picked up in 2021 like never before. As Penn himself mused in retrospection :

I'm positive on dealmaking, but I don't think it'll be gangbusters like it was in 2021.

PennantPark weathered the initial storm and was ready to move with lower interest rates than on the eve of COVID. Overall portfolio jumped from 80 to 97 companies and $1.08b to $1.26b in assets between 2020 and 2021. The annual dividend remained at $0.48 per share.

Art Penn (PennantPark.com)

2022 and 2023 allowed PNNT to benefit from these new originations and the subsequent rise in prevailing interest rates. The annual dividend rose to $0.60 in 2022 and $0.735 in 2023. This context has solidly played into the strength of a portfolio like PennantPark's. The portfolio also grew to 129 companies. Responding to shareholder wishes, they began breaking up the dividend from a quarterly distribution to monthly (at the same annual rate).

Operations

Let's take a look at the current shape of the company.

Manager

The company is managed externally by PennantPark Investment Advisers, which is basically Art Penn and his team. It was also formed in 2007 and similarly manages the investments of PNNT's sister company, PennantPark Floating Rate Capital ( PFLT ). It boasts an average of 25 years of experience across its staff.

{kind=link}

Base management and performance-based incentive fees range between a fourth and a fifth of annual investment income, meaning that they compete strongly with PNNT's dividend potential. In the past, however, the Adviser has voluntarily waived a portion of its fees in times of distress or if they believe an investment was a disappointment, such as when they waived 16% of their base fee between 2015 and 2017.

Investment Strategy

PennantPark has consistently described its approach like that of value investing, with Penn himself sometimes referring to this label ( see tail-end of opening remarks). As such, they prefer to invest in businesses that:

- Have strong competitive positions

- Provide steady cash flows

- Allow for safety of principal and solid exit plans

- Offer attractive returns on that capital

The company targets the "core middle market" for investment because it believes this area is underserved, which allows it to demand more attractive yields with lesser downside.

{kind=link}

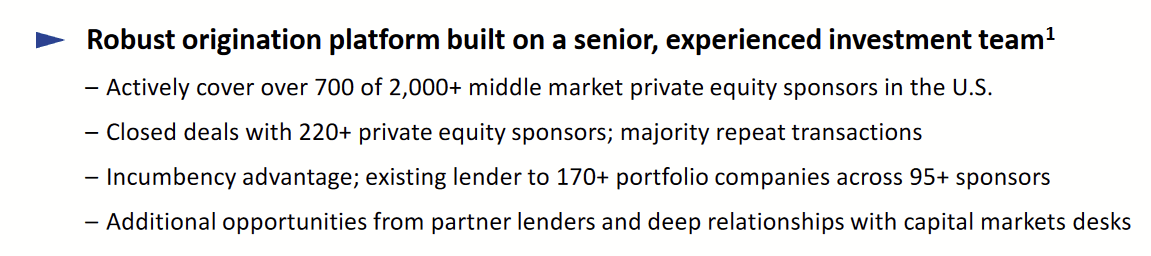

Capital commitments typically range between $10m and $100m in size. These investments are made after a thorough process of due diligence that spans weeks and involves interviews with management, reviews of financial data, on-site visits, and background checks, among other things. The company declines a large majority of potential investments, choosing only those who have sufficiently proved their strengths. After making the investment, PennantPark closely monitors its companies, sometimes collaborating with their companies extensively.

Many of the debt investments come with a small co-investment in equity, which allows PNNT to ride growth as a company goes from $10m in earnings toward the $50m end of the range, the gains of which provide new capital and higher distributable earnings.

Portfolio

June 2023 Company Presentation

Consistent with its goal of capital preservation, the portfolio often has around two-thirds of its investments in secured debt (first or second lien), giving it priority in repayment and sufficient collateral. The interest on these loans, as of 2023, is almost entirely floating rate and has benefited from recent hikes.

Equity typically makes up between a fourth and a fifth of the portfolio, of which a chunk are investments they make in their joint ventures (JV), which themselves originate first lien loans with floating rates.

Spread across 129 companies in dozens of industries, it's difficult to characterize, but PennantPark typically aims for companies it views as non-cyclical and resistant to macro-factors. This is why it performed quite well over the past few years, in spite of challenges.

A Look to the Future

With a shift to monthly distributions, PNNT is orienting itself toward income investors. $0.07 a month annualizes to $0.84, putting the current yield (about 13%) into a middle range compared to its historical low of $0.48 and the high of $1.12.

Non-accrual rarely being a problem, rate fluctuations have been the main influence on the dividend, both cuts and increases. This means today's buyers will need to be comfortable with potential fluctuation in their income over the years. Let's get a handle on that.

{kind=link}

Most of PNNT's debt is fixed-rate, meaning that a decline in rates would cause their portfolio's floating-rate yields to decline faster than their interest expense. In the table above, the company has generously shown the estimated impact on annual net interest income by rate fluctuations on the current portfolio. A shift of one percent would roughly amount to a change in EPS by about 8 cents, meaning the dividend impact would likely be about 7 cents. With that, we can get a basic estimate of how one's income would be affected.

Author's display of historical data (10Q and 10K Data)

In my own table, I show what the impact on annual income would be if these assumptions played out, showing what the dividend would be and how that would affect a capital base of $100K invested on 12/1/2023's closing price of $6.46. I also threw in their dividend's all-time low.

This does assume the portfolio remains consistent, and new originations will be impacted differently. For example, if PNNT originates more fixed-rate loans at these high rates, then they will be less affected. Similarly, it also assumes that the company does not refinance any of its own debt, in order to reduce its own interest expense.

I believe an income investor can reasonably expect to receive about $13K in income with $100K invested for the near future if they accept how low it can go.

{kind=link}

Considering the deep relationships PennantPark has with its portfolio companies, many of which are a decade old, it has a solid understanding of their fundamentals by now, and capital preservation is in the DNA of the portfolio. I believe the real question is ultimately how high or low the yields will be over time.

Risks

Declining Rates

I essentially stated this already, but might as well reiterate. Declining interest rates will reduce net interest income on a floating-rate portfolio, which means lower dividends unless something else in the portfolio conveniently improves earnings.

Recession

If a recession does occur, even if it seems less likely now, the danger here is in how it would halt originations, similar to how 2020 slowed things down. PNNT's portfolio is designed to avoid capital loss, but if originations stall enough, earnings would slow down, and share prices of PNNT would likely drop and make it difficult for income investors to reallocate to another income source without a loss.

Return of Big Lenders

What drives PNNT's returns, even when rates are low, is the abandonment of the core middle market by larger entities, like big banks, particularly in the aftermath of the Great Recession. Even if rates are going PennantPark's way and there are no non-accruals or defaults, the re-entry other lenders with larger pools of capital would make the space more competitive and weaken the returns and covenants they can command on their new originations.

Conclusion

PennantPark Investment Corporation is a company that has survived or even flourished in challenging environments, such as the Great Recession and COVID. Yet, it has been affected by interest rate cycles. While PNNT is unlikely to go to zero, the income it provides will shift based on this. Today's buyers can get an attractive 13% dividend, some of the best it's ever yielded on price, but the longer they hold it, the more I think there will be years where it yields less (if temporarily).

There is more to analyze and discuss with this company, certainly, but I think income investors know most of what they need to know. If the cyclical downside is still enough to meet your income needs, then PNNT is an easy BUY.

For further details see:

PennantPark Investment: Buy For Dividend, Treat As Cyclical