PNNT - PennantPark Investment: Not Ticking All The Necessary Boxes For A Solid Defense

2024-01-07 03:01:03 ET

Summary

- PennantPark Investment Corporation is a BDC with a portfolio structure that includes a higher proportion of risky investments compared to its peers.

- Approximately 52% of PNNT's portfolio is in first-lien senior secured debt, while the rest is distributed across subordinated debt, second-lien, and common and preferred equity.

- PNNT has strong diversification on an industry-level and stable credit quality, but its thin margin of safety in dividend coverage and portfolio composition makes it less attractive for long-term investment.

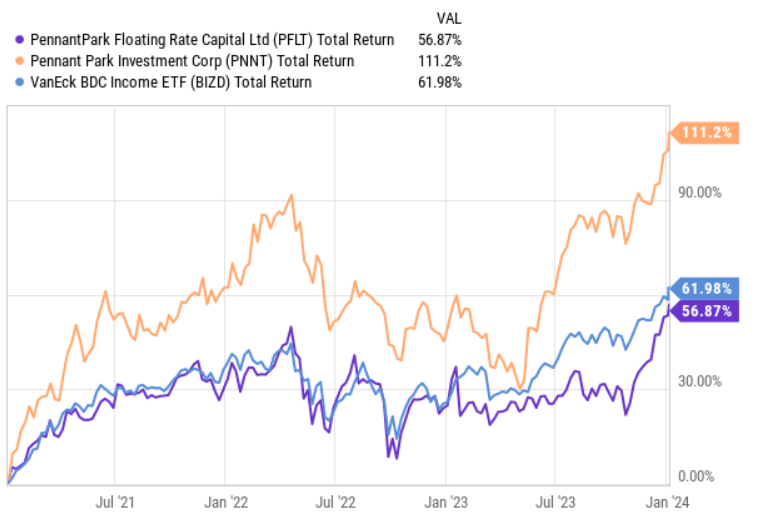

Relatively recently I wrote an article on PennantPark Floating Rate Capital ( PFLT ), where I outlined a couple of critical elements, which differentiated PFLT from most of the BDCs in terms of how defensive it is despite providing ~10% dividend yield. In a nutshell, I considered PFLT as one of the most conservatively structured BDCs out there carrying the right mix between potential returns and risk mitigation going into 2024, when the risk of finally experiencing some corporate defaults is not negligible.

Now, my focus in this article is on a very closely related BDC - PennantPark Investment Corporation ( PNNT ).

Conceptually, PNNT is also similar to PFLT given that it is a BDC, which invests across the entire capital structure in middle market companies with solid management teams, competitive market positions, and already strong cash flow generation.

There are, however, a couple of important differences, which, in my opinion, render PNNT less attractive. And I say that even knowing that PNNT has managed to register significant alpha relative to the overall BDC market and PFLT in the past three-year period (on a total return basis).

{kind=link}

Let me now explain why I think that while PNNT is a solid BDC with some great characteristic, it is still not an optimal vehicle to go long in this moment.

Thesis

In my view, PNNT's portfolio structure is the single most concerning element, which makes it hard to have a full conviction on experiencing solid returns going forward.

Namely, as of the latest quarter , PNNT held only 52% of its portfolio in first lien senior secured debt with the remaining chunk of the AuM being distributed across inherently more risky investment types such as subordinated debt, second lien and common & preferred equity.

PNNT Investor Presentation

In the context of the overall BDC market and PNNT's peers, having roughly half of the total portfolio in first lien could be easily considered a notable deviation from the norm. It means that whatever remains left inherently introduces higher risk for the investors in the case of elevated corporate defaults or in general struggling economy.

I would also underscore the fact that ~25% of the portfolio is associated with common & preferred equity, which might be an additional area of concern in the case of market volatility and financial distress, as these assets stand first in line in terms of absorbing losses and protecting capital structures (via reduced or cancelled dividends and equity dilution).

Having said that, the rest of the portfolio looks rather solid with several layers of inherent protection.

For example, PNNT is very well-diversified on an industry-level, where the single largest category accounts for less than 15% of the total portfolio value.

PNNT Investor Presentation

It is not that often when we would see ~ 20% to 30% concentration in the largest industry among the BDC players. Moreover, the industries themselves are positively biased towards having relatively straightforward business models, implying greater safety from the lender perspective (this is not that surprising given PNNT's investment focus on cash generating businesses).

Credit quality wise, PNNT's seems to be quite stable, with some very strong indication of resiliency. According to Art Penn - Chairman and Chief Executive Officer (as per the latest earnings call ):

Credit quality of the portfolio is stable. We had no new non-accruals in the quarter ended September 30th. As of September 30, the portfolio's weighted average leverage ratio through our debt security was 5x and despite the steep increase in base rates over the past 12 months, the portfolio's weighted average interest coverage ratio at September 30 was 2.3x.

The portfolio's weighted average interest coverage ratio of 2.3x could be easily viewed as one of the safest in the BDC space and also on an absolute level indicating strong ability of the underlying businesses to cover both principal and interest of their loans (which include PNNT's investments as well).

{kind=link}

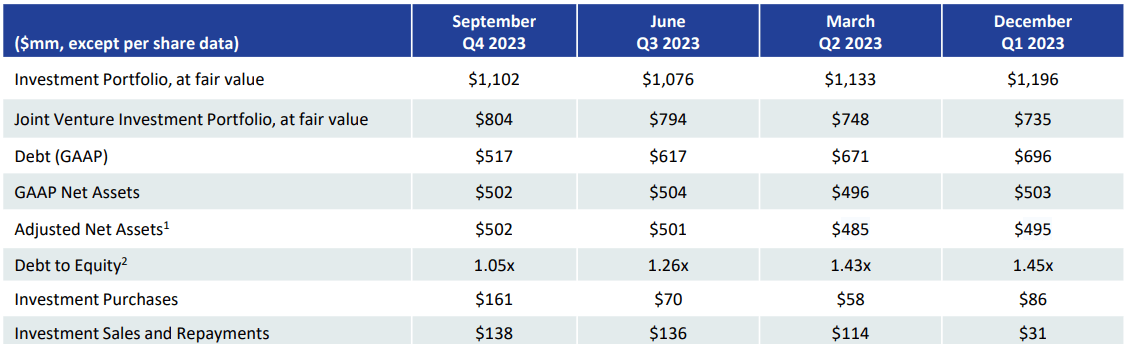

Plus, if we look at the table above, we can notice how PNNT has been consistent in its efforts to optimize the balance sheet by bringing down the debt to equity from 1.45x (Q1, 2023) to 1.05x in Q4, 2023.

This is a significant change, where PNNT has essentially gone from being overleveraged to having a debt load, which is lower than the BDC average .

{kind=link}

Nevertheless, there is one more nuance, which make me uneasy going long PNNT. It is a relatively thin margin of safety when it comes to PNNT's ability to accommodate the dividend payments with the underlying core NII generation.

In other words, in the past four quarters, PNNT has just barely covered its dividend from the received cash flows of the portfolio investments. For example, in Q1, 2023 the dividend coverage stood at 103% indicating that the incoming cash flows were insufficient to safely cover the distributions.

The bottom line

All in all, PNNT is a sound BDC and embodies several layers of protection that are not that common in the overall BDC market (e.g., interest rate coverage ratio of the underlying portfolio companies at 2.3x, debt to equity level at 1.05x, industry diversification through cash generating businesses).

However, the combination of ca. 50% of the portfolio being located outside of the conservative senior secured first lien investments and a very minor margin of safety on the dividend coverage end bring a bit elevated risk into the equation.

Considering the above and that PNNT yields 11.7% (at nearly exhausted dividend coverage ratio), which is just ~100 basis points above the sector average , I would skip going long PNNT and instead focus on BDCs, which are more concentrated in first lien category, have similar defensive characteristics at the same or higher yield levels (or even slightly lower yield as long as that is justified with an increased protection).

For further details see:

PennantPark Investment: Not Ticking All The Necessary Boxes For A Solid Defense