PNNT - PennantPark Investment: Should You Buy The 13% Yield For 2024?

2023-11-27 15:34:27 ET

Summary

- PennantPark Investment is currently changing hands at a 15% discount to fiscal 2023 fourth quarter NAV per share.

- NAV dipped by $1.28 from its year-ago figure as PNNT's investment portfolio also realized a more defensive positioning.

- NII per share of $0.24 fully covers the dividend, but a near-term dividend raise seems unlikely.

Whether PennantPark Investment ( PNNT ) is a buy for 2024 will depend on your outlook for the year. The business development company has been aggressively deleveraging, with net sales and repayments for its full-year 2023 of $418.6 million outpacing new investments of $275.4 million . The BDC's investment portfolio at fair value at the end of its fiscal 2023 fourth quarter stood at $1.001 billion, down roughly $225 million from $1.226 billion in the year-ago quarter. PNNT's debt-to-equity ratio has also been dropping, falling to 1.029x at the end of the fourth quarter, down from a near-term peak of 1.38x at the end of its first quarter. This deleveraging comes as CME's 30-Day Fed Funds futures pricing data places the probability of any further interest rate hikes at near zero . The Fed is likely done, is set to declare a win over inflation early next year, and could follow through with a 25 basis point cut to the Fed funds rate currently at 5.25% to 5.50% sometime in the summer of 2024.

PNNT is on track to get this ratio below 1x for its fiscal 2024 first quarter, a level that would be below much of its middle-market credit peers. Its sister BDC PennantPark Floating Rate ( PFLT ) has a 0.76x debt-to-equity ratio. It seems as though PNNT is positioning itself for more economic volatility and possibly a recession next year. Critically, the continued paydown and reduction of its investment portfolio when combined with a drop in interest rates next year will mean a lower base for its investment income earning power.

| Quarter Ended September 30, 2023 |

| Quarter Ended September 30, 2022 |

| Purchases of investments |

| $61.1 million |

| $134.4 million |

| Sales and repayments of investments |

| $138.2 million |

| $175.6 million |

The BDC's credit portfolio was 95% floating-rate investments and 5% fixed-rate investments at the end of its fourth quarter for what was a 13% weighted average yield on interest-bearing debt investments. This was up by 220 basis points over a year-ago comp of 10.8% with the floating component of its debt portfolio slightly down from 96%. It's also important to note that whilst net investments during the fourth quarter were negative at $77.1 million, sales and repayments of $138.2 million included $47.6 million of sales to its unconsolidated joint venture PennantPark Senior Loan Fund ("PSLF"). PNNT has a $164.4 million investment in PSLF at fair value.

| Investment |

| Percent of total |

| First lien secured debt |

| $527.7 million |

| 52.67% |

| Second lien secured debt |

| $80.4 million |

| 8.02% |

| Subordinated debt (including $102.3 million in PSLF) |

| $156.2 million |

| 15.60% |

| Preferred and common equity (including $62.1 million in PSLF) |

| $237.6 million |

| 23.71% |

| $1,001.9 million |

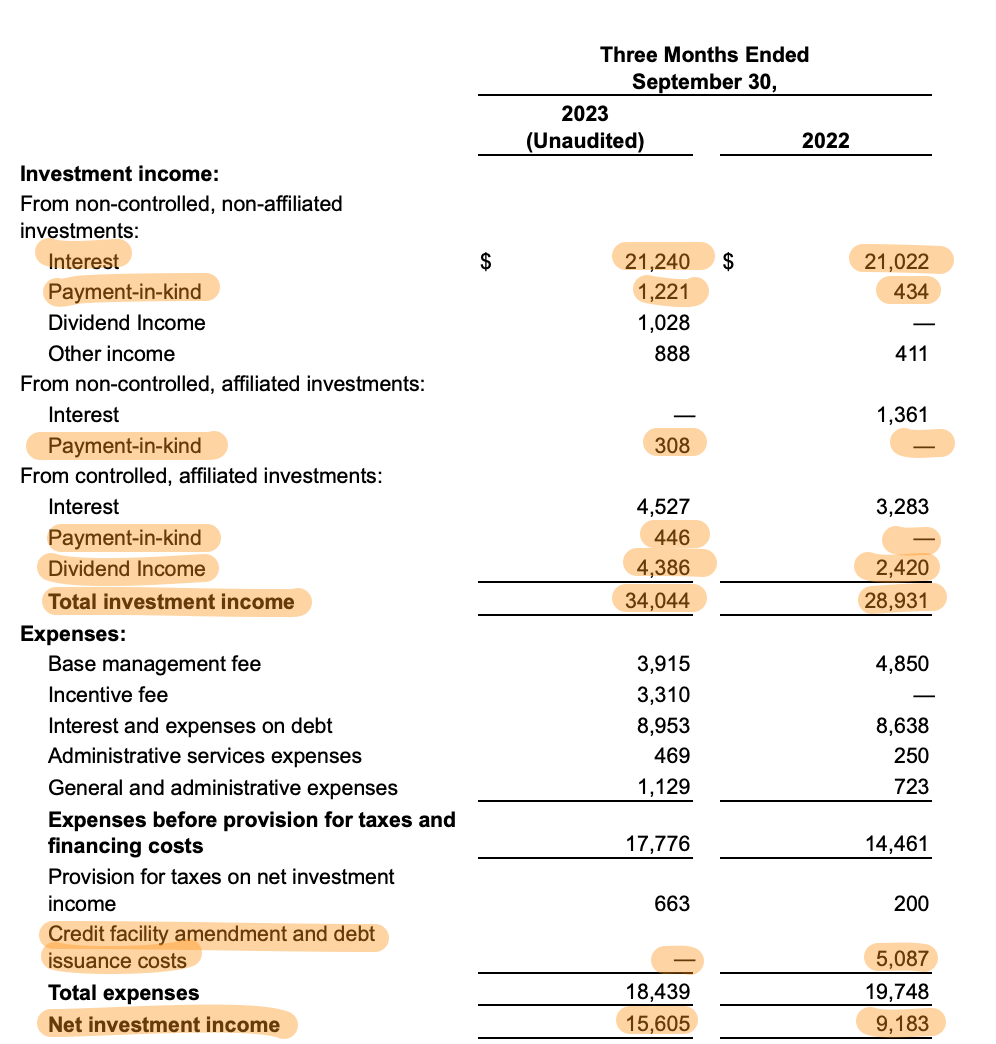

Investment Income, Payment-In-Kind, And Dividend

PNNT Fiscal 2023 Fourth Quarter Earnings Report

{kind=link}

PNNT recorded a total investment income of $34.04 million for its fourth quarter, up 18% from a year ago. The interest income component of this at $25.77 million was essentially flat from $25.67 million in the year-ago comp with growth being driven by dividend income which was up 81% year-over-year. There was a growth in payment-in-kind income to $1.98 million, 5.8% of total investment income, from 1.5% of the total in the year-ago period. This nearly 4x increase is substantial and reflects a macroeconomic environment for US middle market companies that are having to contend with higher interest rates on their debt just as the specter of a recession looms.

PNNT Fiscal 2023 Fourth Quarter Earnings Report

{kind=link}

PNNT pays out its dividends every month, last declaring a $0.07 per share distribution, unchanged from prior and for a 13% annualized forward dividend yield. This came on the back of a GAAP net investment income of $15.6 million for the fourth quarter, around $0.24 per share and up from $0.14 per share in the year-ago comp for 10 cents per share of growth. I last covered the ticker in the summer after the 5% dividend hike and the switch to monthly dividend distributions. However, another near-term hike is unlikely on the back of the more heavily defensively positioned portfolio.

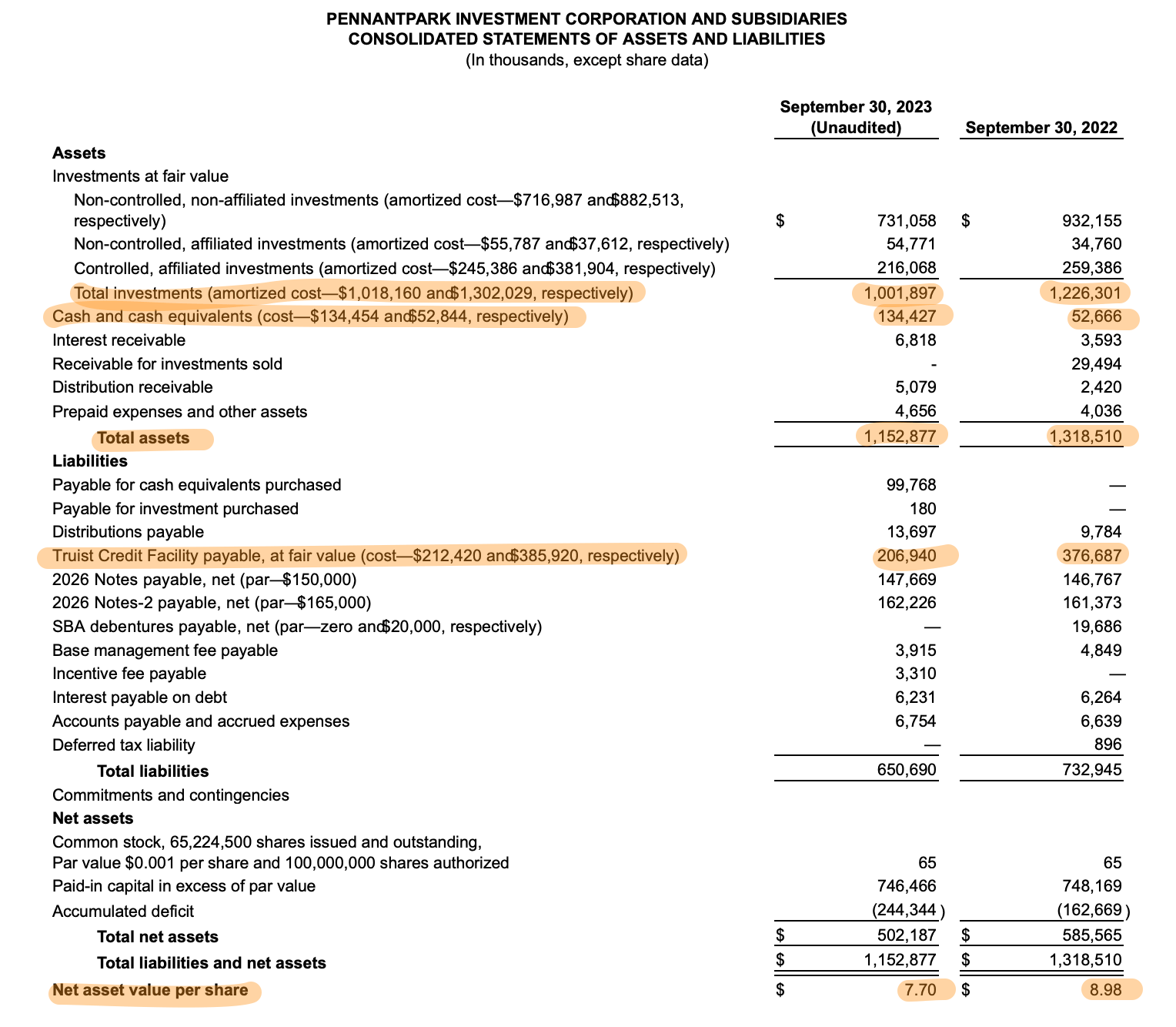

Non-accruals And Net Asset Value

PNNT is currently covering its dividend with NII by 114%, an 88% payout ratio. The BDC has an insignificant amount of spillover income with a flat and declining Fed funds rate and a portfolio with a lower earnings base as PIK income increases are set to form challenges. However, PNNT only had one portfolio company on non-accrual at the end of the fourth quarter, this was 1% of their total investment portfolio at amortized cost and zero percent at fair value.

PNNT Fiscal 2023 Fourth Quarter Earnings Report

{kind=link}

The BDC also reported an NAV of $502.2 million, around $7.70 per share, and down substantially by around $1.28 from $8.98 per share in the year-ago period. This substantial dip has meant the BDC continues to trade at a discount to NAV of around 15%. The continued dip of NAV keeps me away from this ticker, even with the monthly distribution teaser. Lower leverage and near-zero loans on non-accrual status do mean the ticker is a hold.

For further details see:

PennantPark Investment: Should You Buy The 13% Yield For 2024?