PNNT - PennantPark Investment: Strong Performance Monthly Dividend But Over-Diversified Portfolio

2023-09-18 08:30:23 ET

Summary

- PennantPark is a BDC with a robust balance sheet with relatively low leverage and adequate liquidity.

- The company pays generous dividends and intends to switch to monthly distributions.

- The company is deeply undervalued based on the dividend discount model. Besides that, compared to its NAV, its current stock price offers a two-digit margin of safety.

- Despite that, I give PNNT a hold rating for two reasons: high exposure to equity and too diversified a portfolio without focus.

Thesis

PennantPark Investment Corporation ( PNNT ) is a diversified BDC paying generous dividends. Last quarter's results are excellent, and the company`s management plans monthly dividend distributions. PNNT`s balance sheet is clean and provides adequate liquidity. The company is deeply undervalued based on the dividend discount model. Besides that, compared to its NAV, its current stock price offers a two-digit margin of safety.

Despite that, I give PNNT a hold rating for two reasons: high exposure to equity and too diversified a portfolio without focus.

Company Overview

Pennant is a business development company ((BDC)) positioned predominantly in companies supported by middle-market private equity sponsors. The company invests in all tiers of the capital structure, from non-controlling equity to senior secured loans to subordinated debt. The target size funding (senior secured loans, subordinated debt, and other investments) is totaling between $10 and $100 million in any given deal.

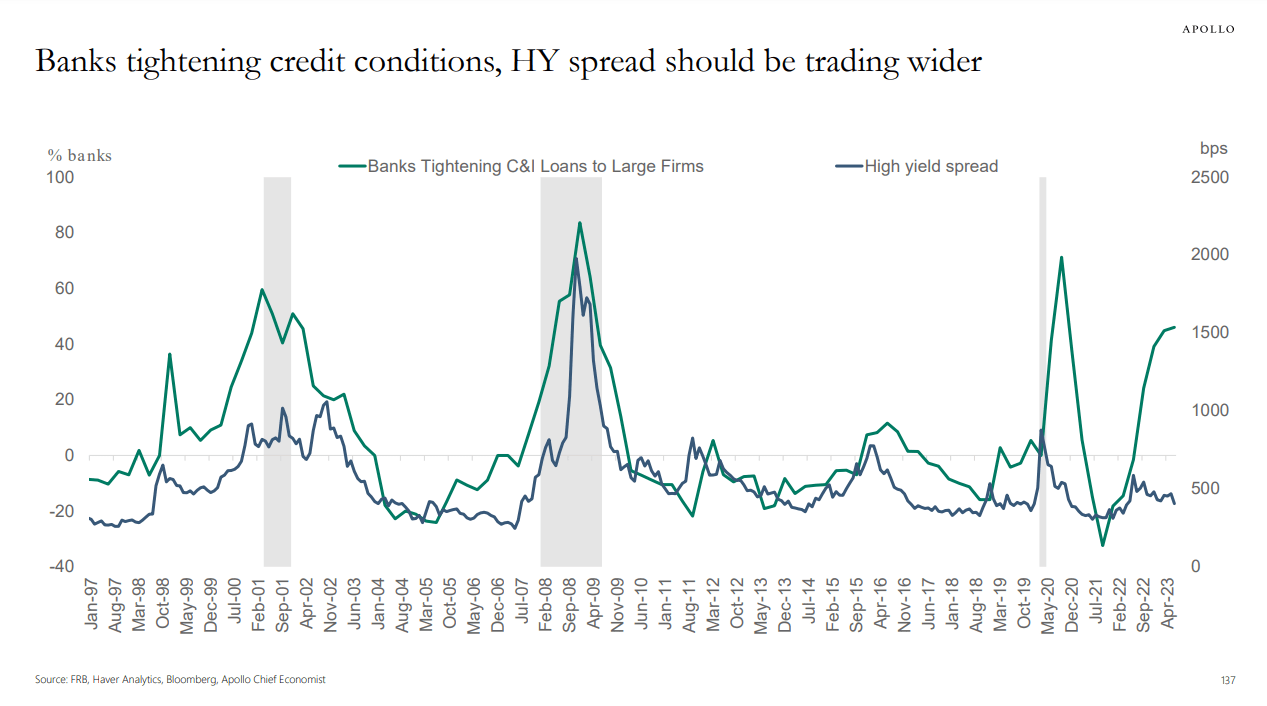

BDCs, like Pennant Park, are intriguing investments since they profit from the pressures on the banking system. Basel Accords put riskier corporate loan assets out of favor while overweight sovereign bond instruments, banks cannot make the optimal risk-reward investments. As a result, most banks have boosted their sovereign securities holdings over the past ten years while reducing their commercial loans as a percentage of deposits. The latest issues with the regional banks added extra pressure on banks' lending operations.

The image below from the Apollo Global shows the tightening lending conditions:

{kind=link}

While the high yield spreads are far from past peaks, the lending conditions are tightening quickly. These dynamics push starving-for-funds businesses to seek BDC as Pennant.

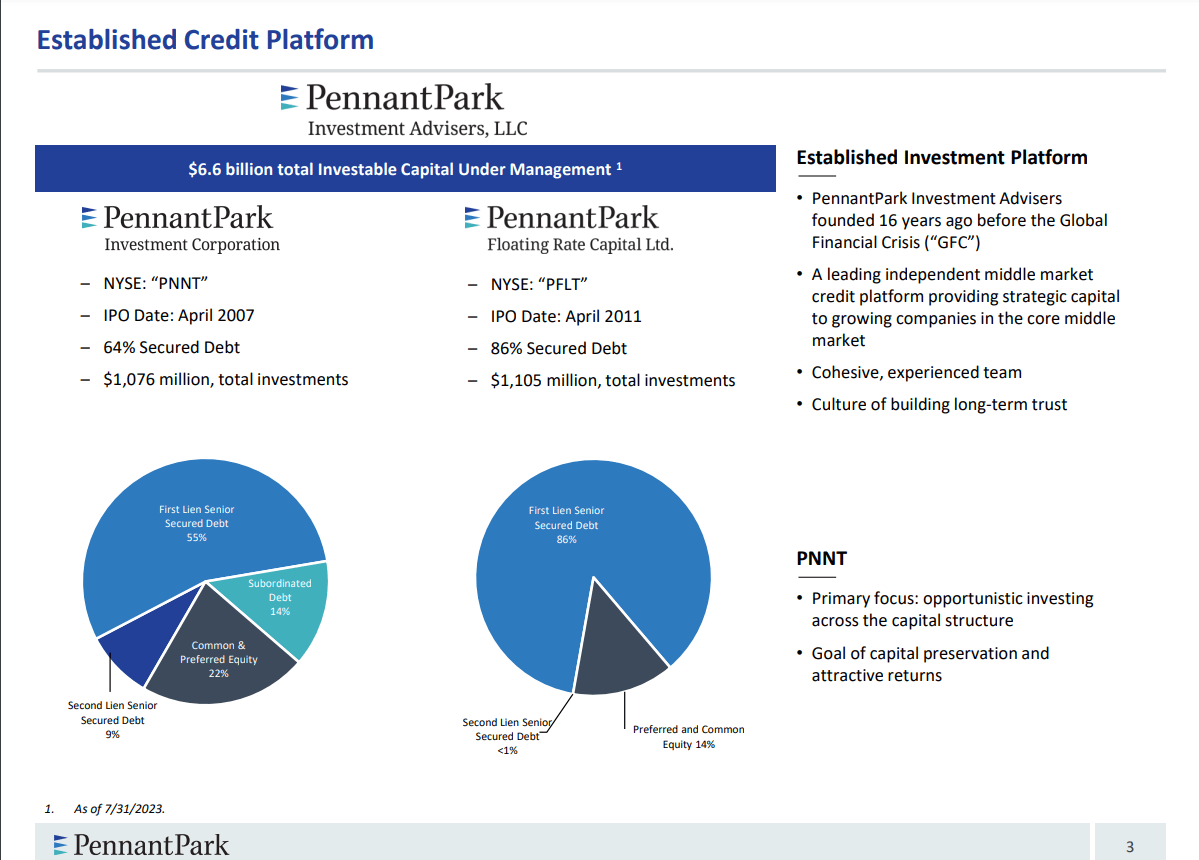

Pennant`s portfolio is distributed as follows: first-lien senior secured loans comprise around 55% of its portfolio, second-lien senior secured debt makes up about 9%, subordinated debt 14 %, and equity 22 %. The image from the last presentation shows the company portfolio.

{kind=link}

I am not keen on the sizable exposure to stocks, with common and preferred shares making up about 22% of its portfolio. Although this is not necessarily an issue, it can be tough to assess shares in smaller middle-market companies appropriately, and the market frequently discounts such investments because of this inherent uncertainty. Conversely, an equity component gives additional asymmetry to the potential returns.

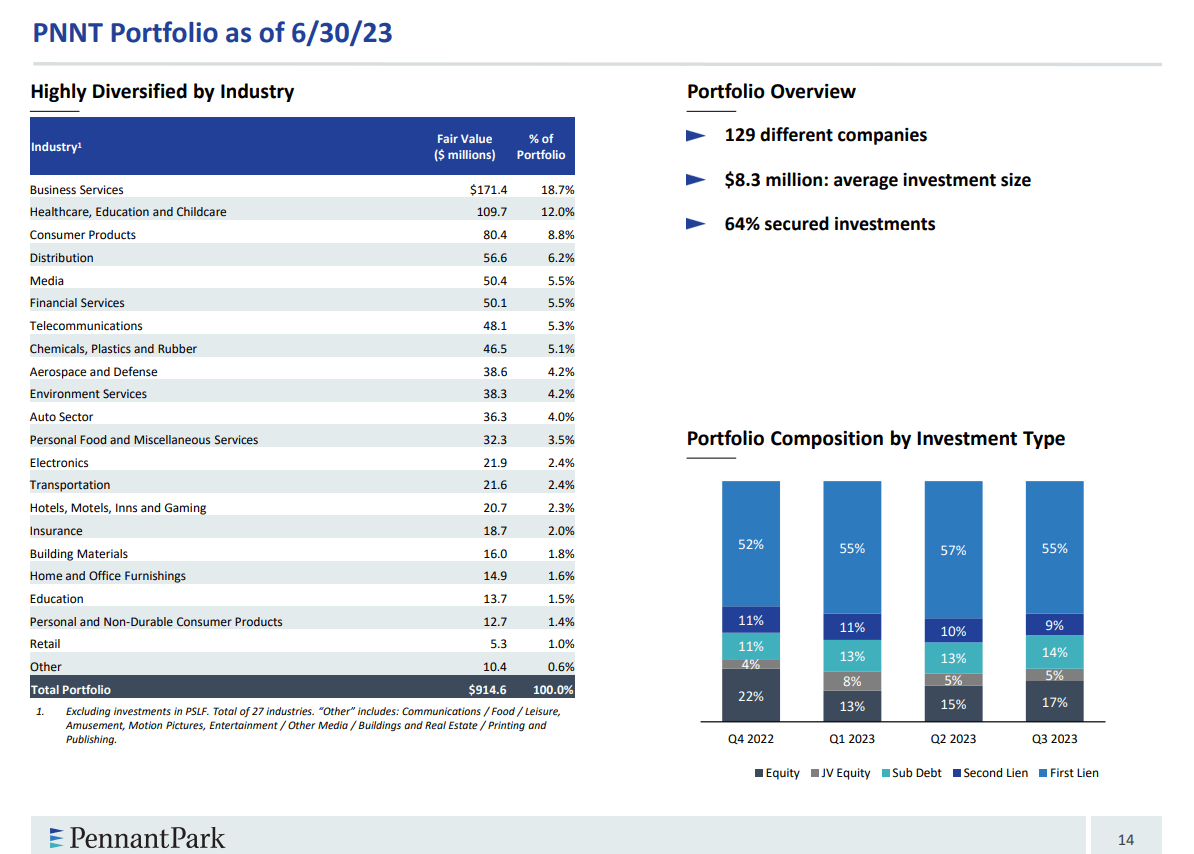

The image below gives more details about company portfolio diversification by industry:

{kind=link}

Two segments carry more weight: business service and healthcare, education, and childcare. The rest are distributed among various businesses.

I do not see considerable diversification as an advantage. As an investor, I follow the principles of concentrated diversification, i.e., invest in a few industries where I have deep knowledge. PNNT`s portfolio covers almost all economic sectors. You need to narrow your focus as an investor to build expertise to take well-researched decisions or at least less uneducated ones. I apply the same rule when I analyze investment vehicles and BDCs. Supermarket portfolios are a major red flag for me. That said, companies focused on a few industries with low correlation have better odds first to survive and later to succeed in the long term.

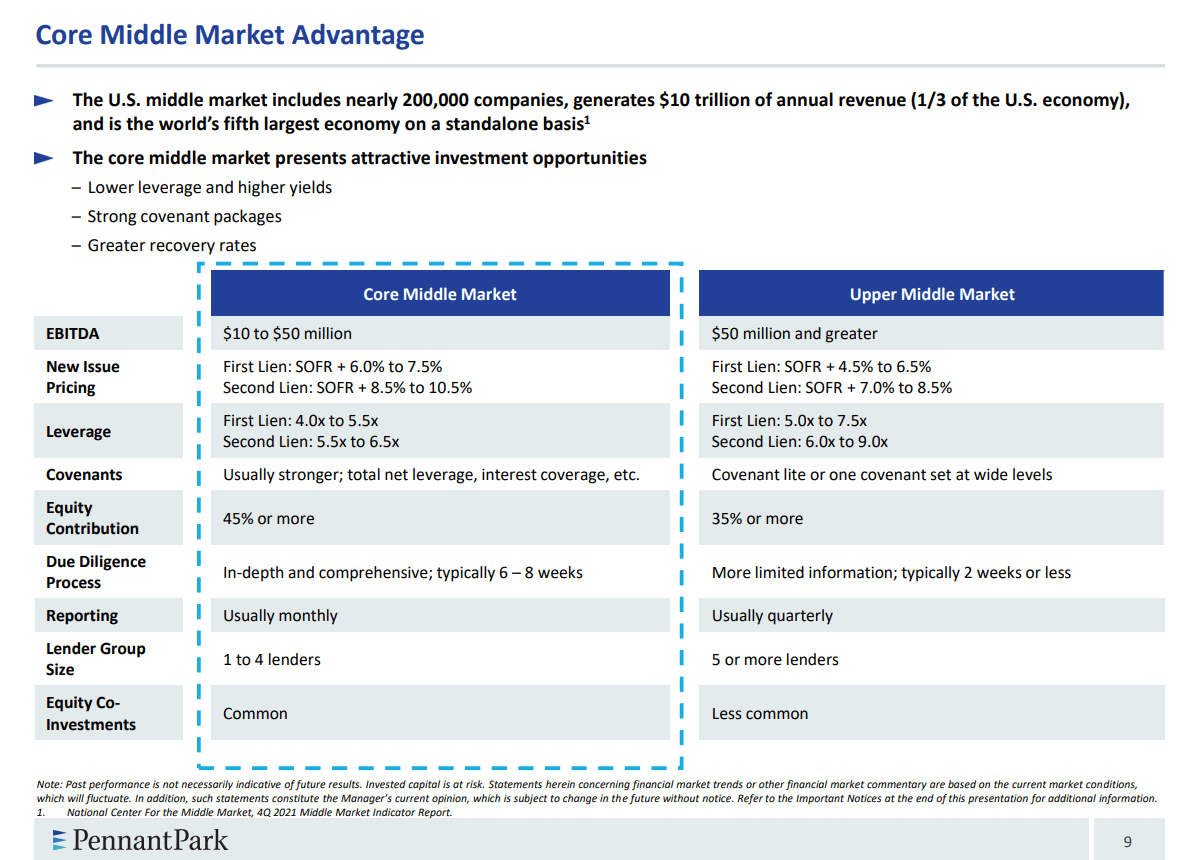

The company has growth prospects considering the middle market, its main field. The image below gives an overview of the current situation.

{kind=link}

As seen above, PNNT has a systematic approach to potential investments. The accent is on first and second-lien debt. In a hopeful move, it has committed to bringing the equity investment portion of its portfolio down to about 10% of the total portfolio value. This shift away from stock investments is, in my opinion, a good thing. The equity portfolio has probably been a drag on the stock despite these decent returns and has added to the discount to NAV. The management appears to be aware of this.

Q2 Performance

Except for a few odd instances in certain areas, including retail, the performance of the underlying companies to which loans have been advanced has generally been by expectations. Below are some numbers from the last company presentation .

{kind=link}

The retail industry's difficulties may continue due to the tendency of middle-class customers to lower non-essential spending due to continuously higher-than-normal inflation levels. Consumer products and services comprise roughly 13.6% of PNNT's portfolio and are most likely the industry that investors should pay particular attention to in the coming quarters.

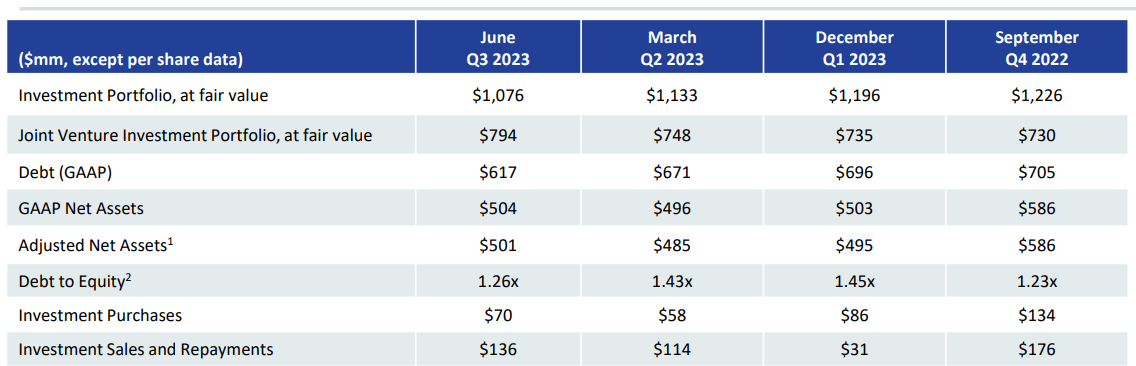

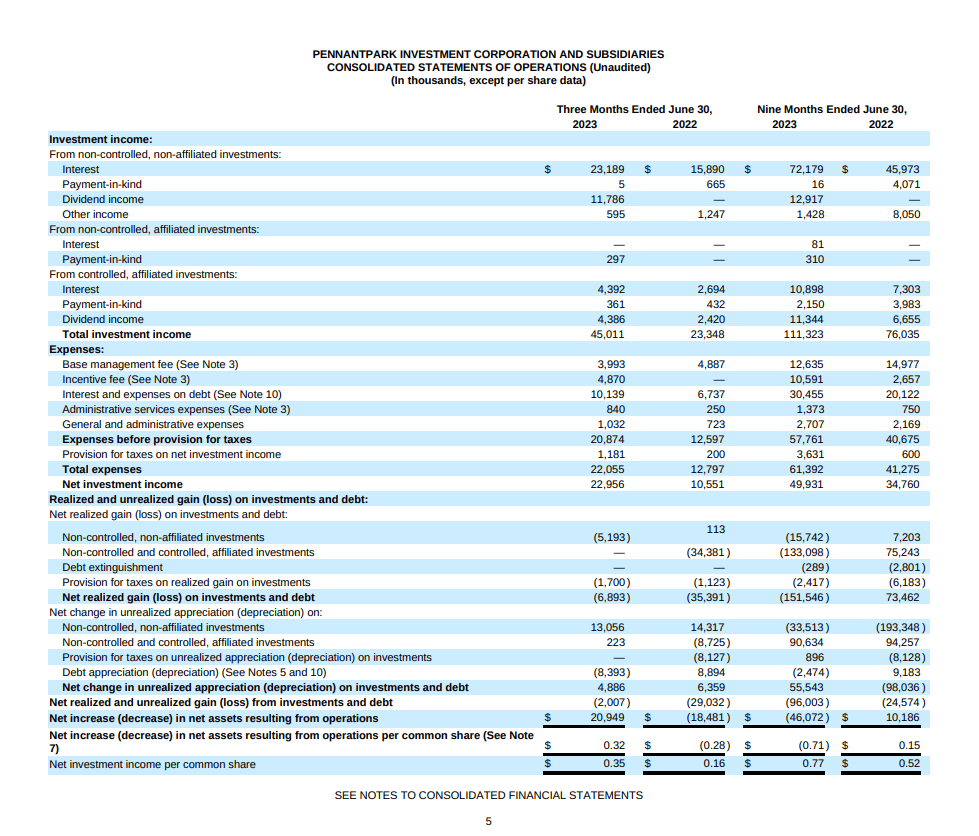

Investment income for the three and nine months ended June 30, 2023, was $45.0 million and $111.3 million, respectively. This was due to first lien secured debt of $24.1 million and $72.7 million, second lien secured debt of $3.5 million and $10.9 million, subordinate debt of $1.2 million and $3.4 million, and preferred and common equity of $16.2 million and $24.3 million, respectively. The cost yield of PNNT`s debt portfolio increased over the same period last year, and a dividend related to its equity investment in Dominion Voting Systems was a significant factor in the increase in investment income. The image below from the last financial report gives more details about the company`s results.

{kind=link}

While the investment income was rising, the expenses were declining compared with last year on a three-month and nine-month basis. The company realized considerable NII growth.

Company Financials

The company’s balance sheet provides enough liquidity in case of economic downturns or borrower issues. The table below shows some metrics I use to examine balance sheet quality. The data is taken from the last financial report, Q2 2023 .

| Quick ratio |

| 2.2 |

| Current ratio |

| 1.3 |

| Long-term debt/Equity |

| 100 % |

| Total debt/Equity |

| 100 % |

| Total liabilities/Total assets |

| 50 % |

Pennant's balance sheet has average metrics for the industry. The positive signs are relatively low leverage and adequate liquidity.

Given the strong results in the last company report, Pennant's profitability has increased despite the difficult quarters of the previous year.

| Interest income TTM /EV |

| 10.4 % |

| Dividend Income TTM/EV |

| 6.2 % |

| Gross Margin |

| 100 % |

| FCF Margin |

| 62.62 % |

| ROE |

| 20.7 % |

| ROI |

| 6.79 % |

Pennant has the intention to switch to monthly dividends in the future. This is expected to happen without increasing the monthly distribution, which is now scheduled to be $0.07 per share.

{kind=link}

Every quarter of 2023 has seen an increase in dividends due to the transition to monthly payments. After subtracting $0.13 in one-time dividend income from the Dominion stock investment, core NII for the third quarter was $0.22 per share. In light of this, the BDC returns 95.4% of core NII to its common shareholders.

Valuation

To calculate the PNNT value with the Dividend Discount Model, I have to measure the price of the company's equity and levered beta.

To obtain those numbers, I use the following steps and assumptions:

- Risk-free rate equals the 5Y average of USA long-term Government bond Rate, 2.2%.

- Growth rate, g, equals the 5Y average of the USA long-term Government bond Rate, 2.2%.

- US's equity risk premium is 5.0 %.

- PNNT’ unlevered Beta 0.71

- PNNT Debt/Equity ratio 122 %.

- The US`s effective tax rate is 25 %.

- PNNT dividend ((TTM)) $ 0.75

- Calculate Levered Beta with the formula below:

Levered Beta = Unlevered Beta * (1+D*(1-T)/E).

2. Calculate the discount rate (discount rate as the cost of equity) using the resulting value for leveraged beta. The formula I use is:

Cost of Equity = Risk-Free Rate + (Levered Beta * Equity Risk Premium).

3. Calculate the Terminal Value of dividends considering the Cost of Equity and Expected dividend growth:

Terminal Value = Dividend per share * (1 + expected dividend growth) / (Cost of Equity – Expected Dividend Growth)

4. Calculate the Present Value of Terminal Value assuming a constant discount rate for ten years.

For PNNT, I get the following results:

Intrinsic value per share = $ 22.64

Current Market price = $ 6.46 on Sept 16, 2023

Based on the dividend discount model, PNNT is deeply undervalued. The current market price offers a 72 % margin of safety.

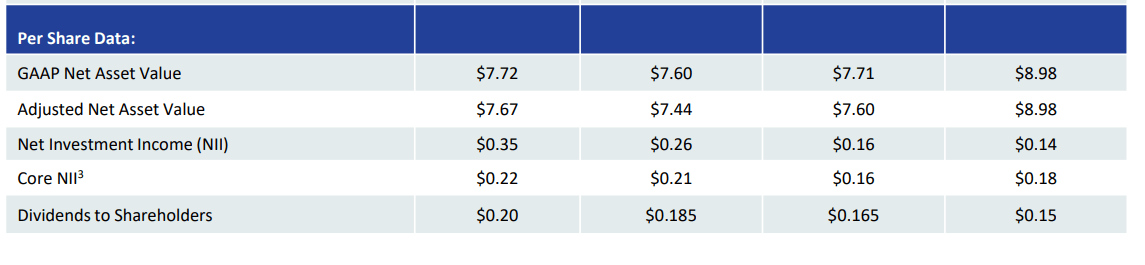

The image below is from the last company presentation . It shows PNNT GAAP Net Asset Value and adjusted NAV.

{kind=link}

A double-digit discount to NAV makes this a hold, even though the monthly move is expected to generate some shareholder excitement. PNNT offers the second-highest discount to NAV among the major BDCs. However, this is an improvement compared to its 3-year average discount to NAV of nearly 32%. Even though I don't think PNNT will trade above NAV soon, the stock's revaluation to a level closer to NAV might be significantly aided by a decrease in the percentage of its portfolio invested in equities.

Risks

PNNT carries typical risks for BDC, such as liquidity and credit risks. However, the relatively high exposure to equities brings additional market risk to its portfolio. On top of that, I add the operational risk, given the sheer diversification across sectors and industries. As mentioned, I preach and practice highly concentrated diversification in a few industries where I have extensive knowledge. The opposite, trying to be everywhere, usually means a lack of expertise in any of the businesses the company invests in. PNNT is not an exception. Pennant, however, has a healthy balance sheet with good liquidity ratios. The credit risk relates to the company`s borrowers' ability to meet debt obligations. The broad diversification mitigates that risk.

Conclusion

PennantPark Investment Corporation pays generous dividends, and the company`s management plans monthly dividend distributions. Considering the strong performance last quarter, PNNT might have the required funds. The company is deeply undervalued based on the dividend discount model. Besides that, compared to its NAV, it offers a digit margin of safety. Despite that, I give PNNT a hold rating for two reasons: high exposure to equity and too diversified a portfolio without focus.

For further details see:

PennantPark Investment: Strong Performance, Monthly Dividend, But Over-Diversified Portfolio