BTDPY - Persimmon: Homebuilder In Attractive U.K. Market

2023-08-10 08:17:15 ET

Summary

- Persimmon Plc is a leading house builder in the United Kingdom.

- Persimmon has grown its revenue at a CAGR of 8%, reflecting attractive industry dynamics in the UK.

- We are bullish on the UK housing market given the systemic issues, such as the under-supply of homes and its attractive qualities which encourage positive migration.

- Margins and distributions are strong.

- Persimmon is trading in line with its historical average EBITDA multiple, which is seemingly pricing in a swift and uneventful recovery. This undervalues risk in our view.

Investment thesis

Our current investment thesis is:

- We believe the UK housing market to be attractive due to strong population growth, attractive economic conditions contributing to net migration, and a demand/supply deficit contributing to steady value appreciation.

- Persimmon is positioned perfectly to partake in this long-term. Its margins are attractive and we see no operational concern with the business.

- The issue is the coming 12-24 months due to current economic conditions.

- Our issue with the stock price is that it is already pricing in an easy recovery, which is bizarre even if conditions are improving.

Company description

Persimmon Plc ( PSMMF ) is a leading house builder in the United Kingdom. The company constructs and sells various types of housing.

It offers family homes under the Persimmon Homes brand, premium homes under the Charles Church brand, and social housing under the Westbury Partnerships brand.

Persimmon also provides broadband services through its FibreNest brand and manufactures timber frame components such as insulated wall panels and roof cassettes under the Space4 brand. Additionally, the company produces concrete bricks and roof tiles.

Share price

Persimmon's share price has experienced a monumental decline following what was a consistent upward trend. This is due to a change in market conditions, which could contribute to a difficult few years for the coming.

Financial analysis

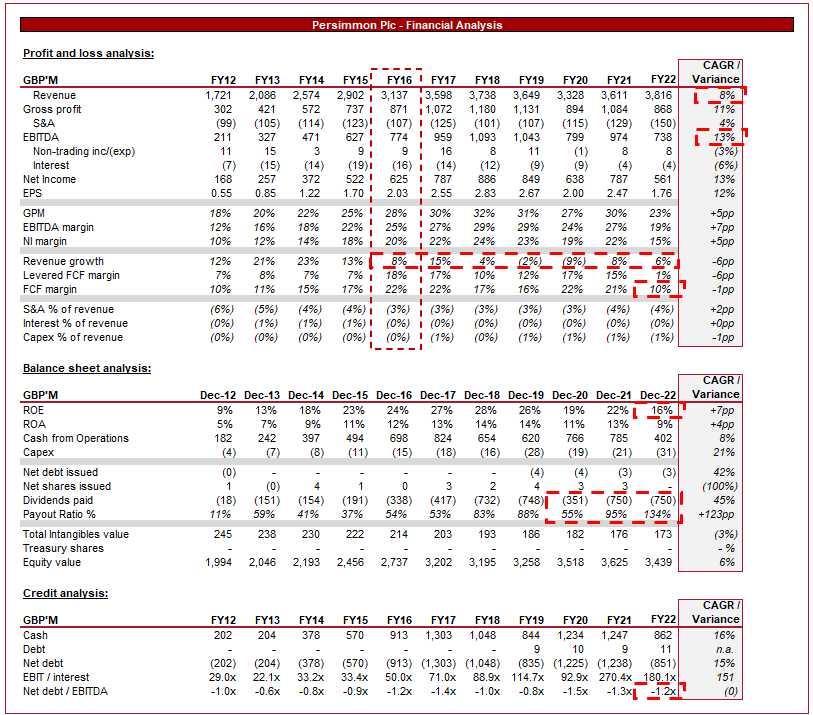

Persimmon financial performance (Capital IQ)

{kind=link}

Presented above is Persimmon's financial performance for the last decade.

Revenue

Persimmon has grown its revenue at a CAGR of 8% across the last decade, reflecting a period of consistent growth.

Before conducting a detailed review of Persimmon, it is valuable to briefly understand the UK's housing market.

The UK housing market has historically been extremely resilient while producing consistently healthy value appreciation. This is due in large part to two primary reasons. Firstly, the historic strength of the country, be it economically, militarily, or from a legal perspective. These factors have contributed to inward migration and healthy population growth. The second factor is the size of the UK. Despite having a population of c.67.3m (similar to France), the UK is less than half the size of France and is even smaller than New Zealand (5m population). For this reason, the balance between supply and demand has always been weighted toward demand, especially given the culture of home ownership. It is incredibly difficult to estimate the number of homes required to meet parity, but estimates suggest England alone requires c.340k new homes each year, with current levels closer to 233k.

For these reasons, we are bullish on the UK housing market. As each year progresses, this deficit continues to climb, which will only contribute to rising house prices. This is attractive for homebuilders as demand is key to generating long-term returns through building, even if they do not actively seek to build and rent. Also, from a downside perspective, the risk is substantially reduced when home prices generally trend up.

Given we are discussing the UK economy, it is worth touching on Brexit. The UK voted to leave the European Union in 2016, contributing to an extended period of negative sentiment toward the country. Politics aside, global investors are concerned the UK could lose its economic value. This has contributed to reduced investment in the country, much of which goes straight into properties (given the value appreciation). Now, millionaires are not buying Persimmon properties, but they are taking up supply. Secondly, Brexit raises the concern that reduced migration to the UK could contribute to softening demand for properties. We highlighted above the point at which Brexit was voted for, with Persimmon's growth post being noticeably lower. This is muddied by Covid-19 but certainly shows some impact. Regarding net migration, the UK remains a net importer of people and has reached a record level . This is because (again, politics aside) the UK is in desperate need of people to fill gaps in the workforce. We consider the wider impact of Brexit to be an issue but the degree is overblown we feel.

Government initiatives and policies play a significant role in shaping the UK housebuilding industry. The UK government has introduced various schemes to support the construction of new homes as a means of closing the deficit, such as Help to Buy and the Affordable Housing Program. These initiatives provide financial assistance to buyers and developers, stimulating demand and incentivizing housebuilding activities. Persimmon continues to benefit from this and could see policy change given the nose dive in new-build activity.

The housebuilding industry is highly sensitive to economic conditions and namely interest rates. Economic conditions dictate the financial strength of consumers, as well as confidence in future prospects, which will have a material impact on the decision to purchase a property. We are less concerned by a traditional recession as most businesses face issues, home builders are not unique. A large increase in interest rates is a concern, however. Following a decade of record-low rates, the Bank of England has been steadfast in raising rates, with current inflation levels implying further hikes are ahead.

This has materially impacted consumers' finances, deterring the purchase of properties. Many consumers will seek to wait until rates decline and others will be priced out for many more years. This is a serious issue for Persimmon as it has contributed to a freefall in the number of properties being transacted.

Our view is that rates will likely decline at the start of 2024, reaching <2% by the end of said year. This remains a moving target, however, given the stubbornness of inflation.

The following are key quotes from Persimmon's most recent trading update.

" The Group traded in line with expectations during the first quarter. As previously announced, the forward sales position at 1 January 2023 was £1.0bn, down 36% year-on-year. "

" This reduced forward sales position led to a 42% reduction in Group completions in the first quarter to 1,136 homes (Q1 2022: 1,950 homes). "

Persimmon does see reason to be positive, however.

" Trading over recent weeks has offered some signs of encouragement with visitor numbers up, cancellation levels normalising and sales rates continuing the steady improvement evident since the start of the year. "

" Longer-term, we see excellent opportunities for the business and we have a good pipeline of new sites expected to come through for 2024."

"With this growth in outlets, and signs that the improvement in consumer confidence is being sustained, we anticipate a return to volume growth and expansion of margins in 2024 ."

Our view is that FY23 will likely be an incredibly difficult year, which is clear to see, with sales down 37-42%. We believe Persimmon could come at the lower end of this, although we are less confident that volume growth will come as soon as 2024.

Long term, we remain confident in the health of the UK housing market, as history suggests it is a mistake to bet against it.

Margin

Persimmon's margins are highly attractive, with the company consistently achieving >22% EBITDA-M and >18% NIM.

This has slightly slipped in FY22 but likely reflects the partial impact of high interest rate conditions. We believe Persimmon can return to this level given the heightened home prices in the country.

Balance sheet

Persimmon has a robust balance sheet, electing against the use of debt to fund operations. This is a reasonable position given the cyclical nature of the industry. This means we are not concerned by a material slowdown in the business from a solvency perspective.

Distributions have come in the way of dividends, growing at an impressive level in line with EPS.

Outlook

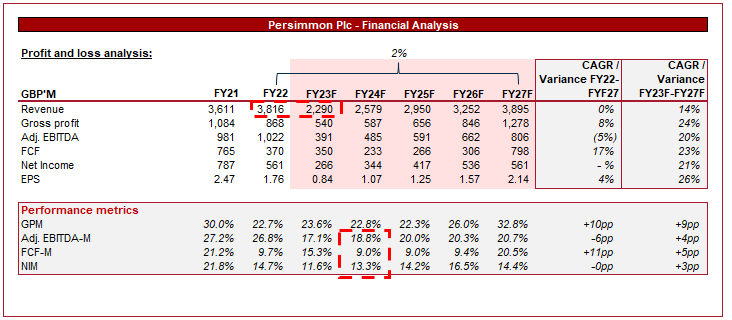

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting an almost 40% decline in sales FY23F, reflecting the monumental decline in demand. Across the medium term, Revenue is expected to return to its FY22 level by FY27. This is reflecting a bearish view given the rapid deterioration in demand in the last 2 quarters.

In the company's H1 results (released today), it posted a (36)% decline in properties sold and a (30)% decline in revenue, YoY. Further, new housing GPM has declined from 30% to 21.5%. The average selling price has remained robust, but this is a reflection of a mix toward larger property sales, likely due to resilience in the higher income bracket. We consider this a good performance, as it outperforms the current analyst estimate and suggests the "bottom" may have been reached, or at least is imminent. This does inherently reflect how uncertain the market is and the difficulty with making forward expectations.

Our view is that H2'23 will be another difficult period, especially with additional rate hikes, but see conditions improving from H2'24 onward.

Valuation

Valuation (Seeking Alpha)

Persimmon is currently trading at 7x NTM EBITDA, which is in line with its historical average despite the significantly weaker economic conditions. This is unusual and implies investors are softening to the risks around an extended housing bear market.

In comparison, Barratt (BTDPF) is trading at a discount to its historical average, and Taylor Wimpey (TWODF) is in line at 7x.

This implies Persimmon's share price includes a recovery to healthy levels fairly quickly with little risk. This does not seem reasonable as risks remain.

Final thoughts

We are bullish on the UK housing market long term, given its strength in the face of numerous global and local headwinds. Persimmon is positioned perfectly to benefit from this, with extensive expertise and experience. The current decline in share price did represent an opportunity for investors, but with the share price now implying no upside compared to historical trading, we believe improvement is priced in.

Investors considering Persimmon long-term would benefit from remaining patient, as there is a risk the stock is dead money for at least another 6-9 months.

For further details see:

Persimmon: Homebuilder In Attractive U.K. Market