PSMMF - Persimmon: Homebuilding From The U.K. I'd 'Buy' At Single Digits

2023-11-07 14:20:00 ET

Summary

- Persimmon Plc is a U.K. homebuilder with a strong foundation and no net debt.

- The company is experiencing declining margins due to inflation in building material costs, but still has a profitable business model.

- The current valuation of Persimmon Plc is low, but the company requires a more attractive valuation to justify investment.

- I enter the company coverage giving the company a "HOLD", and a conservative price target.

Dear readers/followers,

My forays into the UK market have been more rare than I'd like. I own shares in companies like Legal & General Group Plc ( OTCPK:LGGNY ) and Rolls-Royce Holdings plc ( OTCPK:RYCEF ), but overall my investments in our island-based neighbor have been few - at least so far.

In this article, I'm going to introduce you to Persimmon Plc ( OTCPK:PSMMF ) ( OTCPK:PSMMY ). I can already hear some of you asking what I am thinking - investing in a British homebuilder in this environment. Well, everyone needs homes - and the UK is no exception. If Persimmon PCL is a qualitative business, then I can give it a price for a conservative upside, and we could make money from such an investment.

In this article, I'll get into the business model and specifics of Persimmon - because we're going to have to wait for a reversal for this company. That's what we're investing in - a company in an obvious slump, experiencing a cyclical downturn related to macro.

Let's see what we have going for us here as investors.

Persimmon Plc - Plenty to potentially like, some risks exist

So, Persimmon Plc has a 50+ year history, and its name, while odd, comes from a horse that won a Derby in the 19th century for the future king Edward VII.

Persimmon, to get into company fundamentals has several advantages. First, due to its current cash and leverage balance, the company has no net debt. It's a net cash company, with an interest coverage of over 52x. In this environment, that is superb. The company also has a working business model, that while seeing declines on a historical basis and certainly being in a valuation trough at this time, still performs with good/average gross, operating, and net margins. The company manages an average, double-digit net margin and is certainly profitable.

It also, due to its valuation and its dividend tradition, has a very high yield. It's at 7%+ at a payout ratio of less than 60%. (more on that dividend later, as the company has recently established a new dividend base)

{kind=link}

So, on the positive side, Persimmon Plc is a very foundationally strong company. It's unlikely to see fundamental deterioration.

Yes, the company's margins are declining - and its valuation is declining as a result of this, with revenue down on a per-share base, and the ROIC being lower than the current average WACC. However, that is to be expected - most companies in this sector, including Swedish ones, are currently seeing variations of the same trends.

The company operates under a whole host of brands - where Persimmon Homes is one of the most popular. However, the company also has:

- Charles Church , focusing on more premium homes in markets that demand premium products.

- Westbury Partnerships focuses on social housing in the affordable/budget sector. These homes are sold to housing associations.

- Space4 , manufacturing timber frames.

- Brickworks , the arm producing concrete bricks, and supplying only the company's operations, with a 2022 output of 53M bricks.

- Tileworks , the company's own production of roof tiles.

- FibreNest is the company's own broadband service business.

If you're used to American home construction business models, some of these operational specifics may be unfamiliar to you.

While Persimmon Plc based on its operating history including events of not paying suppliers, and being accused of delivering substandard home quality can be called somewhat of a "scandal-troubled operator", the company is trying to clean both its quality and customer satisfaction track record, with recent impressive trends.

{kind=link}

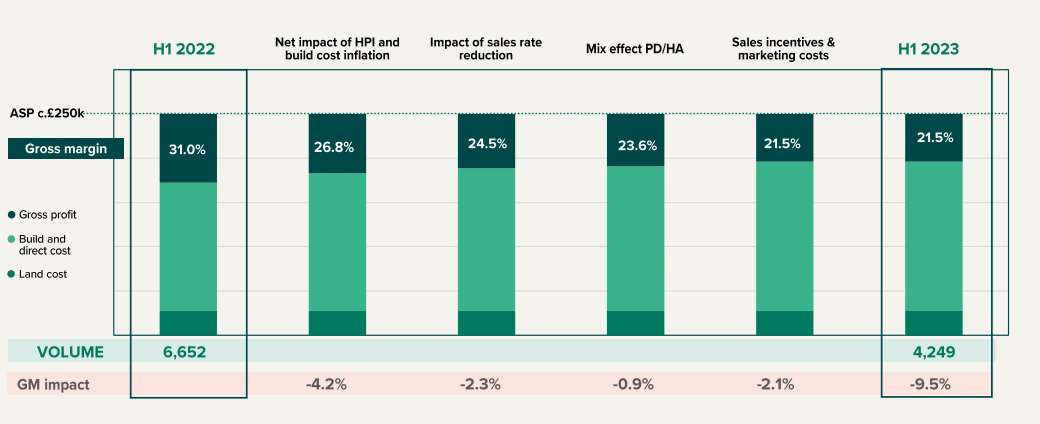

The company's home completion trends and sales are actually rather good when we look at the overall European trends. The company expects a full-year home delivery of 9,000 total homes, with a focus on margin over volume. 1H23 completion was in line with this target while reflecting the lower forward order book. The sequential trends are up however £1.4B sold in June versus £1.04B sold in January of 2023.

However, let's be clear - the company's declining margins are significant - both from a volume decrease perspective and from gross margins, due to inflation in building material costs and other OpEx.

Persimmon Plc IR (Persimmon Plc IR)

From that perspective, Persimmon is seeing exactly the same issues as other homebuilders and construction companies at this time. However, with growing (sequentially) sales and a good "baseline" sort of earnings - because let's make it clear, this company is nowhere near going profit-negative, I would still say Persimmon is doing quite well.

Persimmon is also quite an interesting study of just how severe the reductions in margins have been in this industry.

{kind=link}

And like every other company in the sector, the company experiences the current conundrum of affordability being the key issue. Given cost increases, the company can't sell cheap, and in the UK, the 36+ year mortgages have increased to 49% of first-time buyers. As a comparison, this number in 2022 was 35%.

The company's trends are very challenging, and we've seen this sort of impact reflected in the company's overall valuation. What I mean is that in a period of 3 years, Persimmon Plc has lost 62% of its market cap/share price, at a negative 27.8% CAGR.

I have stayed far away from this company for some time - but there comes a point where every company is interesting. For an example, and even an example specific to the UK, I want you to look at my work with Rolls-Royce, where I made triple-digit RoR in less than a year.

Persimmon Plc share price (TIKR.com)

Looking at the trends above, you can see that the market has been heavily punishing the company for the macro as well as for how the company has been handling the current situation - even if there is only so much the company could have done differently. We're now at an overall market cap of just above £3.5B.

The company decided in 2022 to rebase its dividend. it's now at a base of 60p (that's £0.6), which at forward earnings even during the trough of £0.8 remains well-covered. Remember, that £0.8/share is currently as "bad" as things are expected to go. It also means that even after this conservative rebasing, the current yield for Persimmon Plc is 5.4%, which is somewhat above the risk-free rate.

My arguments for why Persimmon Plc might be a good investment for you are through-cyclic. The company is one of the UK's premier homebuilders. It's extremely well capitalized, with less than 6% debt/cap , and it's at a net cash position. This is a superb starting position to go from.

It has an impressive degree of vertical integration in its business model - it produces its own bricks and tiles, as well as the internet, and through this is able to offset some if not all of the worst cost increases. The company's appeal in the finance world can be confirmed by looking at the recent debt the company raised, a £700M facility through a 5-bank consortium. The company's NAV as of the half-year period is more than £10/share, which means that the current valuation is very close to NAV, and while its ROE and ROACE are down, it's still very firmly in the positive.

Despite being firmly in the negative, and looking rather bad, Persimmon very much has a working, profitable business model.

{kind=link}

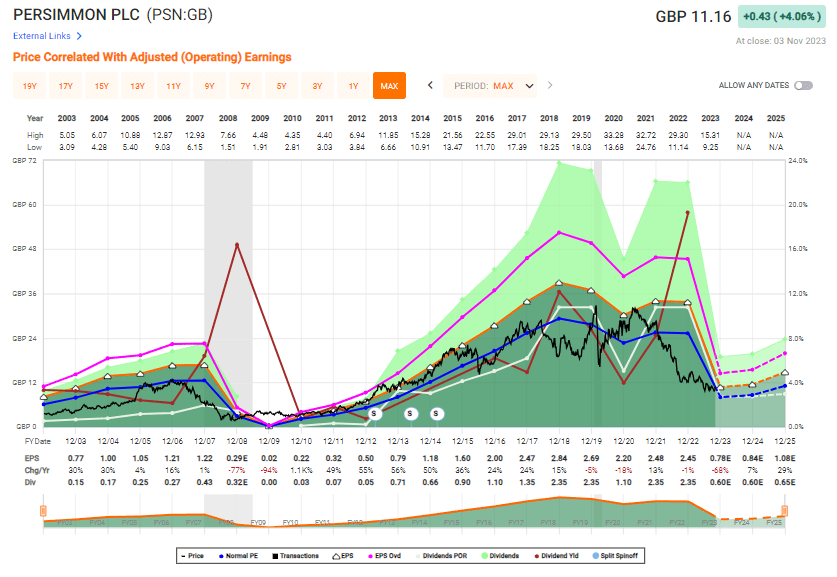

The literal only way, in terms of valuation, that Persimmon could be this cheap over time is if you only value the company at tangible book or net asset values on a current basis (which I by the way, usually do). If you use any other method of valuation, be it standard graham, sector-average PS values, projected FCF implications, or historical data, the implication here is that the company could be worth at least double the current price, or even somewhere to £30/share. And before you call that insane, look at this graph.

Persimmon Plc Valuation - We're in a trough

{kind=link}

What you see is a price that more often than not outside of a recession was closer to £20-£30/share than not. Any time you could buy this company in the last 20 years, and if you're willing to hold, you'd have come out on top. It's my general view that this is a likely scenario for the future as well.

I will say, with clarity, that Persimmon is not a great company during recessions, and I believe we're heading into one. As you can see, recovery here can take 4-5 years. But I don't need to tell you what you could see in terms of returns if you bought PSN during the GFC - we're taking annualized of 30-40%, or 2,400% RoR in less than 12 years.

So, as usual, it's all about that valuation.

The main question for Persimmon Plc I want to field is whether the company is a fundamentally safe investment - and yes, for the long-term I believe this to be the case.

The next question obviously becomes at what price we want to buy Persimmon, given that we've seen the company trough down to 2 quid per share and below during recessions. I don't believe £2/share to be realistic, but I do think the company could go lower.

However, like most businesses today, and this is the reason why I don't think things will be as serious as during GFC, companies are much better capitalized today. That includes Persimmon.

However, there is a valuation problem. Because the company tends to trade at 10-12x P/E, the most upside you can see from Persimmon today is around 7-10% annualized - at least until 2025E. That means that in order for Persimmon to give us the outperformance we're looking for the company either has to do better than expected, or we need to hold it for longer than 2025E, when this reverses.

Or, as I choose to do, wait for a cheaper share price. I am experienced with this in UK companies when it comes to Rolls-Royce. If you manage to pick the company up at a cheap enough price, then this investment could become a real 15-30% annualized stock.

But for that, you can't, unfortunately, buy at £11/share. Now with these forecasts and not in this macro.

Despite all of the positives for the company, and there are many, the valuation currently breaks my thesis here, making it a clear "HOLD". Analysts are, as you might expect, more positive than that. 17 analysts follow the company and go from £9.8 on the low side to £23 on the high side. Out of those 17 however, only 3 are at a "BUY" recommendation, despite an average PT of £13/share. That's a lack of conviction for the company I find interesting.

But it's also illustrative of why I consider the company to be a "BUY" at a single-digit share price.

I'm putting my introductory share price for Persimmon at £9.8/share, adding my voice to the lowest range here.

I also firmly believe that if you're interested in investing in Persimmon Plc, you should definitely go for the native PSN ticker, not one of the thinly traded ADRs that are available.

Until the company reaches a new valuation, my thesis for Persimmon Plc is as follows.

Thesis

- Persimmon Plc is one of UK/Britain's leading homebuilders. It has an attractive set of fundamentals, little to no debt, impressive vertical integration, a massive land bank, and a good track record working with the intricacies of the British system. If I were to invest in British homebuilding, then Persimmon Plc would be at the top of my list.

- However, the company requires an attractive valuation in order to justify me risking my capital. At the current levels, the company barely manages to under conservative estimates scrape together a double-digit upside. I could literally get almost 9% from an investment-graded pref stock - which makes this sort of investment an absolute no-go in this macro.

- I want Persimmon stocks at a single-digit share price if I am to invest, and I give the company a price target, at the intro here, of £9.8/share for the native.

- This makes the company at this time of November 2023, a "HOLD".

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic and high enough upside based on earnings growth or multiple expansions/reversions.

This company currently fulfills 3 out of 5, making it a "HOLD" for me.

For further details see:

Persimmon: Homebuilding From The U.K., I'd 'Buy' At Single Digits