PTALF - PetroTal: Could Sinopec Get Involved In Block 107?

2023-08-15 11:08:05 ET

Summary

- PetroTal posted a record Q2'23 in terms of production and announced a special dividend.

- PetroTal is looking for a partner for the development of the highly prospective Block 107 in Peru.

- The potential partner should have sufficient CAPEX budget and preferably experience in doing business in Peru.

- I think that Sinopec fits these criteria, and possible involvement in Block 107 may even be seen as expanding China’s influence in Peru.

- The new largest shareholder of PetroTal has a history of doing business in China, which may be another clue for the case of possible future Sinopec involvement.

I’ve covered PetroTal ( PTALF ) ( TAL:CA ) a few times before, with my most recent June article rating it a Buy here . Usually I focus my analysis to the operational performance of the company, which is related to Block 95 or more specifically the Bretana field. Regarding that, PetroTal achieved a record quarter, surpassing 19kboe of daily production and delivering strong numbers in terms of net income and free funds flow. However, in this article, I’ll focus on the prospective Block 107, which could theoretically double production. PetroTal is reportedly looking for a farm-out partner in developing this field and I’m going to present the case as to why the China Petroleum & Chemical Corporation ( SNPMF ) a.k.a. Sinopec could get involved in the project. I’d like to state up-front that there’s no official information available in the public domain that there are any negotiations between PetroTal and Sinopec as of this time. So the article is basically me speculating on the possibility and why I think that Sinopec could eventually be interested in working with PetroTal on Block 107.

Solid Q2'23 performance

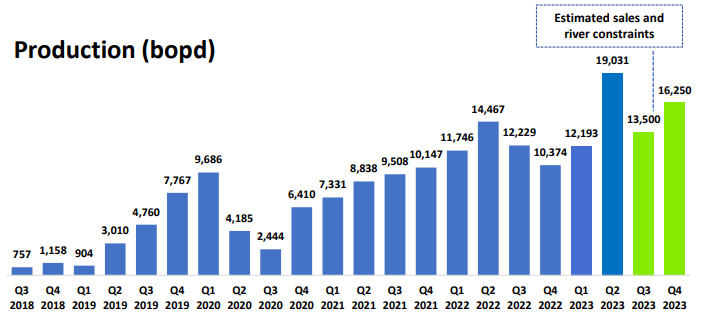

PetroTal achieved record production in Q2’23, exceeding 19kboe (+31.5% YoY) of daily production, despite having to dea l with a temporary riv er blockade in June. Average sales contracted price was US$77.29 (-30.6% YoY). This allowed PetroTal to realize netbacks of US$45.53/barrel, compared to US$74.13/barrel a year ago. Note, that the drop compared to last year is due to base effects, as oil prices were well into triple digit territory in Q2’22. Net income for Q2’23 came at US$46.6M (-44.7% YoY), while free funds flow amounted to US$37.7M (-37.9% YoY).

{kind=link}

The financial position of PetroTal solidified further, as it ended the quarter at a net surplus of US$97.5M. In light of all these, management decided to pay a special dividend of US$0.01/share in addition to the quarterly US$0.015/share for a total of US$0.025/share.

Going forward, Q3’23 is shaping to be much weaker in terms of production as river levels have fallen, restricting barging capacity. Still, the company has a large enough cash pile and continues to repurchase shares almost daily.

Block 107 overview

Block 107 is located to the south-west of the operating Block 95 and is in a closed proximity to Lima. In Block 107, the primary areas of interest are the Osheki and Kametza areas, which have a combined mean estimate of prospective resources on an unrisked basis of 534MMboe. While this estimate could very possibly be reduced as the area is getting explored, for reference the operating Bretana field has 3P reserve estimate of 168MMboe. It has to be noted that Gran Tierra Energy ( GTE ) has 20% back-in working interest in Block 107.

{kind=link}

Osheki-Kametza prospect overview ( PetroTal )

PetroTal needs a development partner

However, the development of this prospect will be a costly endeavor and for that reason, PetroTal is looking for a farm-out partner. The topic was brought in the Q1’23 earnings call and the CEO – Manolo Zúñiga gave the following answer, regarding a question on potential partners for Block 107:

We are still working to obtain the permit to do the actual exploration well in Canada. And we may be able to obtain that permit as soon as we get more approval as well to move forward. We may be able to drill that well by -- before year-end 2024. I would give you a surprise that goes into 2025. I imagine and I have mentioned this several times in the past . As we get closer to drill the well, we may have people coming to calling us. In the meantime, I don't think people are going to have other looking at Block 107.

{kind=link}

Illustrative production profile of Osheki-Kametza ( PetroTal )

An illustrative production profile of the Osheki-Kametza at assumed 50% WI, reveals that it could approximately double PetroTal’s production. The fact that the company has presented the profile of the field under an assumption of 50% WI is yet another pointer towards their intention to bring in a partner and also gives a guess about the percentage that management is willing to give.

Why Sinopec could get involved with Block 107?

I think the potential farm-out partner in Block 107 should be a company that has a substantial budget for exploration and development, meaning it should likely be a bigger company than PetroTal. What’s more betting the vast majority of one’s exploration/development budget on a single outside project won’t make a lot of sense, so ideally the partner should be a large company, which is willing to risk part of its CAPEX spending on Block 107. Also, it would make sense for the potential partner to have some experience of doing business in Peru, as this comes with risks on its own.

{kind=link}

Oil producers in Peru (Petroperu)

Looking at the current oil producers in Peru, one seems to perfectly fit the above criteria – CNCP Peru, which is the Peruvian subsidiary of Sinopec. It’s the current owner and operator of Block X, out of which the company gets around 9.8kboe of daily production. This makes Sinopec the second biggest oil producer in Peru, after PetroTal.

{kind=link}

Sinopec's upstream production (Sinopec)

The Chinese company is one of the biggest Asian integrated energy companies with operations in all segments of elements of the oil&gas supply chain – upstream, midstream and downstream. As far as the upstream segment in Q1’23 Sinopec produced more than 1.34Mboe on a daily basis out of which 755.3k barrels/day were oil. In that context, prospective production from a new oil field that could add around 20k barrels/day is negligible. However, currently the vast majority of production comes from within China and only about 83k barrels of oil /day are from overseas. As far as financial strength, Sinopec has a huge CAPEX budget, which could easily fit funding for the exploration/development of prospects the size of Block 107.

{kind=link}

Sinopec's CAPEX budget (Sinopec)

It’s important to note, that Sinopec is a majority state owned and through it China could try to increase its presence and influence in certain regions. While South America is not the primary focus of China as of now, the Asian country is increasing its investments there through the Belt And Road Initiative. So even from geopolitical point of view, further investment in Peru, through Sinopec could increase China’s influence in the South American country.

PetroTal’s new biggest shareholder may be another link to China

As of recently, the biggest chunk of PetroTal’s shares was held by the investment company – Meridian Capital. However, following a series of transactions in May and June, including the exercise of warrants, now the largest shareholder is Mr. Askar Alshinbayev with a share of approximately 23.5% of PetroTal. At current market prices of US$0.57/share, his stake is worth close to US$125M. The acquisition of such large stake suggests that Mr. Alshinbayev has quite strong conviction in PetroTal’s future.

Askar Alshinbayev bio (askaralshinbayev.com)

Looking at his own website, it appears that besides being a co-founder of Meridian Capital, he has experience doing business in China. The fact of someone with connections in China has decided to acquire such large package of PetroTal’s shares may be another clue of a possible future involvement of Sinopec.

Valuation

In terms of valuation, PetroTal remains on the cheaper side within the LATAM oil&gas producers, despite having an impressive production growth profile, comparable to that of Vista Energy ( VIST ). With the addition of the special dividend to the quarterly amount of US$0.015/share, the dividend yield is north of 12%, which is quite high even for an energy company. I maintain a bullish stance on PetroTal and have increased my position recently.

{kind=link}

Shareholder return focus ( PetroTal )

As far as the subject of this article, if Sinopec or other farm-out partner for Block 107 is being announced, it could be a game-changer for PetroTal and could lead to significant share price appreciation.

Conclusion

PetroTal is looking for a farm-out partner for the highly prospective Block 107. After considering the characteristics that the potential partner is likely to possess, I think that a company that fits the description is Sinopec. The Chinese giant already has established operations in Peru, while its CAPEX budget is quite large and could easily fit any potential expenses related to exploration/development in assets in similar size of Block 107. As Sinopec is state owned, such potential involvement could be seen as expanding Chinese influence in Peru.

For further details see:

PetroTal: Could Sinopec Get Involved In Block 107?