AQNU - PFFA: Leverage Hits Returns Again

Summary

- PFFA is one of the more popular actively managed preferred share ETFs.

- While the fund has shown moments of brilliance, overall performance has been poor since inception.

- Leverage came to particularly bite in 2022 and we look at what lies ahead.

Virtus InfraCap U.S. Preferred Stock ETF (PFFA) is one of the more popular actively managed funds in the preferred share space. The fund has over $460 million in net assets and is quite liquid with a daily trading volume of about 150,000 shares. That volume is far ahead of most individual preferred securities and investors can trade this without worrying about having undue slippage.

The appeal has also come primarily from what the main alternative is on the menu, iShares Preferred and Income Securities ETF (PFF). While PFFA has been actively managed, PFF adheres to the index. Indexing of course has its advantages, but in the world of preferred shares, there are actual disadvantages. Many including us, have documented cases of PFF owning incorrect securities and also buying or selling them at inopportune times. PFF has also owned mandatory convertible issues way above fair value , an error you would expect a simple calculator would eliminate. Obviously a fund like PFFA that is not tied down to a broken methodology should do better. In that area, PFFA has had a modicum of success. We look at why the fund has still delivered very poor returns and where we see this going in 2023.

The Setup

PFFA has been setup as an income fund primarily although it does aim for capital appreciation as a secondary objective. According to its fact sheet, it stays in the more liquid space of the preferred share Universe by aiming for companies with a market capitalization of over $100 million. We think this refers to the total size of the company's entire equity offerings and definitely not the individual preferred share size. Key emphasis is on active management coupled with what it calls modest leverage, of 20-30%.

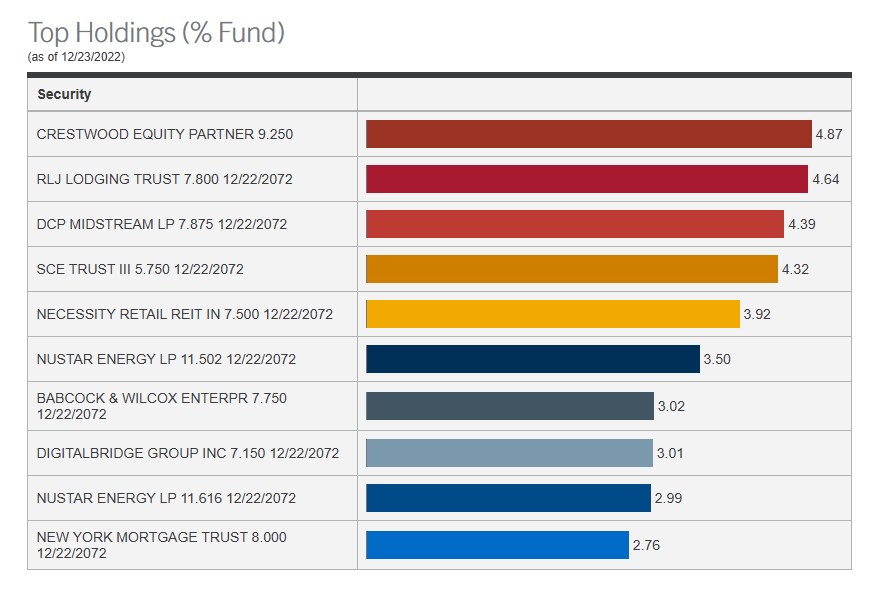

Holdings

At last check, PFFA had a very concentrated set of securities in the top 10 with more than 37% of the fund's assets invested in them.

{kind=link}

The fund clearly is favoring the energy sector and holds among others, the NuStar Energy LP ( NS ) preferred shares which we have recently covered. One other thing that stands out here is that they all are very high yielding at present. The two NuStar securities for example yield in excess of 11% at present. Those two are currently on a floating rate schedule, but the majority of holdings are fixed rates and won't move to a floating rate at any point.

Another thing that stands out here is that they are all under par value/callable value. This prevents any unpleasant valuation adjustments in case of an unexpected call, and also creates upside potential in case of lower rates down the line. Another advantage of investors is the avoidance of K-1s. Buying MLP securities (including their preferreds) directly, subjects investors to the dreaded K-1, which most equate with the bubonic plague. PFFA allows a convenient 1099 instead.

Leverage & Fees

PFFA is currently dialing up the leverage to the top end of their stated range. Based on last available data, we are looking at about 32% leverage.

PFFA Positions As Of Dec 23 2022

{kind=link}

Interestingly, PFFA presents this number in relation to net assets. That is $146 million of leverage is 31.89% of $460 million in net assets. In contrast, closed end funds do the opposite. Here is PIMCO Corporate & Income Opportunity ( PTY ) with its leverage.

PTY Cef Connect

Effective leverage is shown as 40.77% of CEF Connect and that is saying that $967 million is 40.77% of $2.372 billion in total assets. Had PTY's leverage been shown as a percentage of net assets, we would see effective leverage as 68.9%. Our point here is to make sure investors are doing an apples to apples comparison as PFFA's leverage numbers are at the lower end of the spectrum.

PFFA's expenses and fees are reasonable for an actively managed fund.

{kind=link}

PFF charges just 0.45%. but considering the weird moves we have seen that fund make, we would not be interested if the management gave us an annual 0.45% credit for investing. PFFA's reasonable fees though understate the current run-rate though. Interest expenses are on the rise as they respond with a lag to LIBOR.

Interest is charged at the 3 Month LIBOR (London Interbank Offered Rate) plus an additional percentage rate on the amount borrowed. The Agreements have an on-demand commitment term. For the period ended April 30, 2022, the average daily borrowings under the Agreements and the weighted average interest rate were $161,390,015 and 1.43%, respectively

Source: PFFA Semi-Annual Report

Basic math here will tell you that with 30% borrowings and 5% LIBOR rate, we are looking at close to 1.8% expense ratio just from the borrowing portion. We are assuming a 1% spread for PFFA which is probably conservative. So total expense ratio should move to about 2.6% in 2023.

Performance

For all the extra effort put into the fund, the total returns have been quite disappointing. PFFA has delivered total returns of 9.85% since inception and this of course includes the large distributions.

In fact the returns are about what you expect if you tacked on leverage on top of PFF. PFFA has also delivered the returns with extremely high volatility. For example, for that extra 2.7% total return over 4.5 years (0.6% annualized) you had a far worse drawdown in 2020.

Even if you give COVID-19 induced despondency a pass, PFFA has far sharper drawdowns compared to the index.

The latest one took away the bulk of the alpha that the fund was tracking to date.

Verdict

To understand our verdict, you have to get what got us here. 2021 was in general a time where we heavily panned preferred share funds and other fixed income ETFs. We saw them return-free risk and PFFA was also setup in a similar manner. By holding many preferred shares way above par, it was guaranteed that the fund's total returns would be under its distribution . We pivoted to a positive stance on fixed income securities around May of 2022, where we felt that they can start becoming part of a diversified portfolio. Unfortunately, PFFA's returns have been quite terrible since even our bullish pivot.

Returns Since Last PFFA Article

That was a very poor call on our part after correctly avoiding this fund through a very risky period. The failure came from primarily leverage chewing up returns during periods of high volatility.

{kind=link}

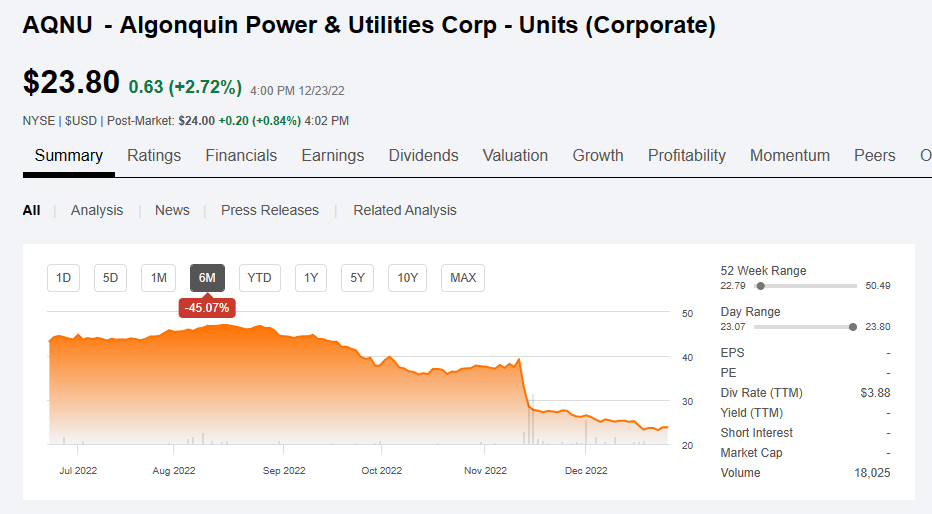

PFFA also owned some moderately sized positions like Algonquin Power & Utilities Corp - Units ( AQNU ) which were proxy equity plays (rather than preferred equity plays) and underperformed drastically.

{kind=link}

So where do we go with this now?

Our stance on fixed income has improved even further and we are finding more quality bargains. We think PFFA delivers positive returns from here as well, although at this point we really don't see the merit in chasing a leveraged fund when you can get 7% plus returns in preferred shares with lower volatility. The Brookfield preferred shares for example offer plenty of income without the risks. Sure, you can get more for PFFA and the distribution yield is now 10.8%. But you are taking more credit and leverage risk for that and you have to balance that versus the fund's annual total returns of 2.2% since inception. We are still giving it a buy rating as we think total returns will be positive and exceed that of the S&P 500 ( SPY ). We don't own it though and have no plans to buy the fund.

We strongly recommend you have a Merry Christmas and a Happy New Year.

For further details see:

PFFA: Leverage Hits Returns Again