PFFD - PFFD: Higher For Longer Interest Rates Detrimental To Preferred Shares

2023-10-03 12:26:30 ET

Summary

- PFFD provides exposure to a broad index of preferred securities. However, broad indices are financials heavy, as they are the largest issuers of preferred shares.

- Since the root cause of the March regional bank crisis, higher interest rates, have not been resolved, I believe systemic risks still remain.

- I recommend investors seeking preferred share exposure to consider the PFXF ETF as an alternative, as it excludes financials.

Following up on a cautious article on Global X U.S. Preferred ETF ( PFFD ) I penned a few months ago, I continue to believe investors should exercise caution on the PFFD ETF due to the recent surge in long-term interest rates.

The root cause of the March regional bank crisis was higher long-term interest rates causing unrealized securities losses in bank balance sheets prompting bank runs. With interest rates materially higher now compared to March, I believe the systemic risks have increased.

Brief Fund Overview

First, for those not familiar with the PFFD ETF, the Global X U.S. Preferred ETF tracks the ICE BofA Diversified Core U.S. Preferred Securities Index ("Index") to deliver broad exposure to preferred shares in the U.S. market. PFFD's index includes floating rate, variable, and fixed-rate preferreds and is market-cap weighted, with a single issuer cap of 10%.

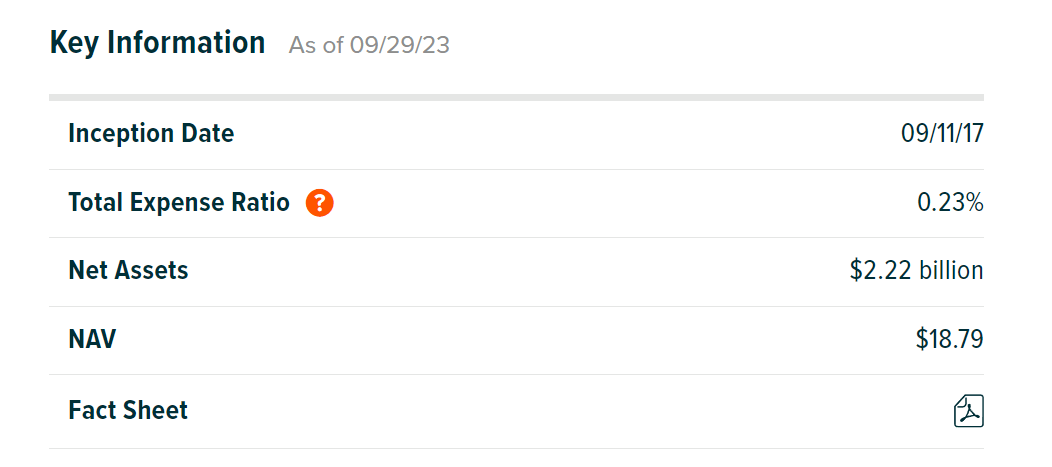

The PFFD ETF has $2.2 billion in assets and charges a low 0.23% expense ratio (Figure 1).

{kind=link}

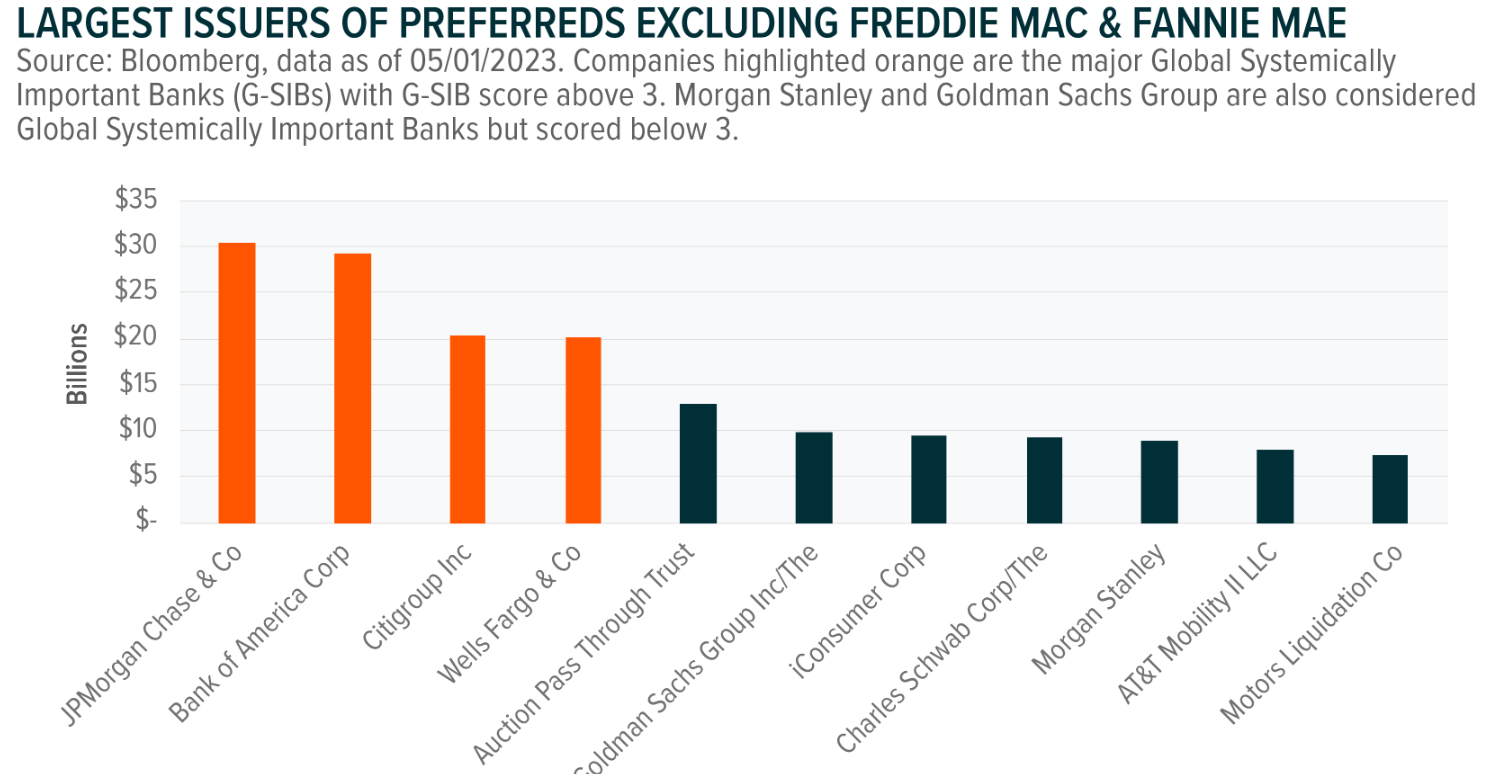

Since the largest issuers of preferred shares are often financial companies like JPMorgan and Bank of America, PFFD's portfolio is likewise dominated by financials exposure (Figure 2).

Figure 2 - Largest issuer of preferred shares are financial companies (globalxetfs.com)

{kind=link}

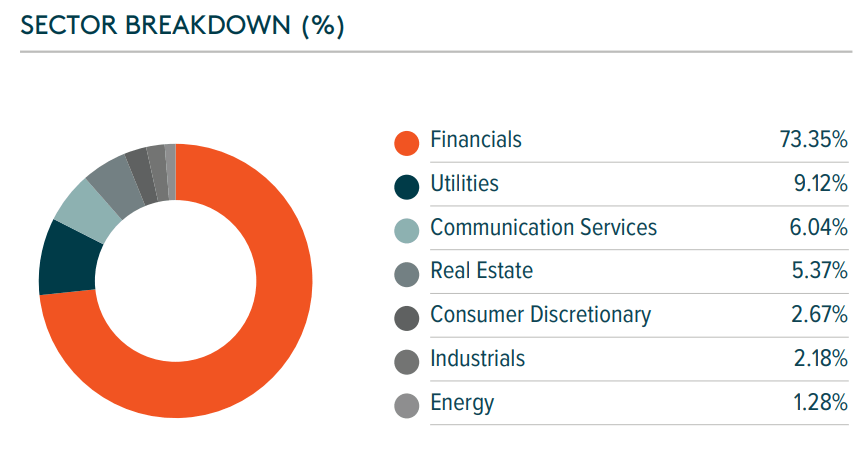

Overall, more than 73% of PFFD's portfolio is invested in the Financials sector with Utilities being a distant second at 9% as of August 31, 2023 (Figure 3).

{kind=link}

Regional Bank Crisis Redux?

My main concern with the PFFD ETF is its enormous exposure to the Financials sector. Readers may recall that in March, U.S. regional banks suffered a massive run on confidence as investors questioned the soundness of their balance sheets and depositors rushed to pull their money from the regional banks.

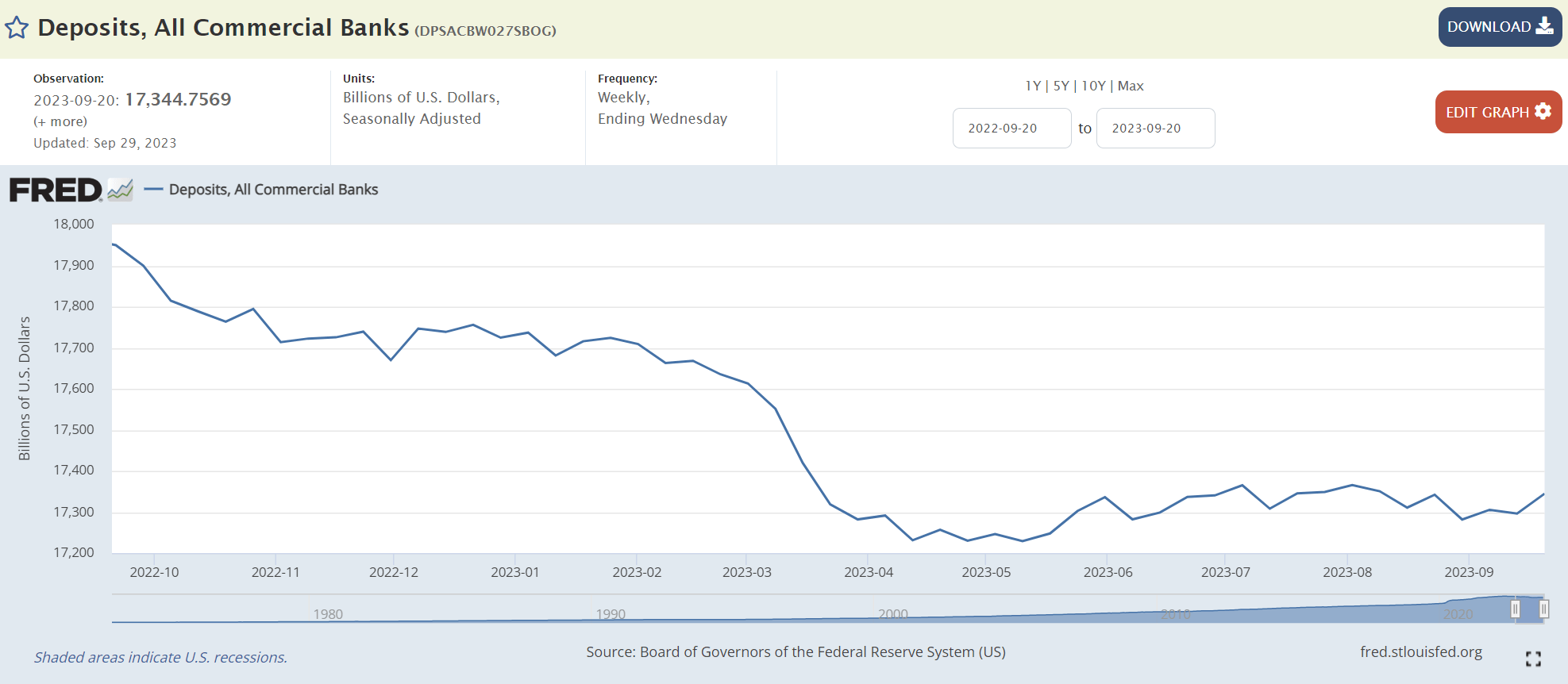

While the twin problems are no longer acute, they have not been resolved either. For example, if we look at the commercial bank deposits, we can see that commercial bank deposits have not fully recovered the outflows from March. Measured against deposits at the end of 2022, commercial bank deposits are still down approximately $380 billion, at $17.34 trillion as of September 20 (Figure 4).

Figure 4 - Commercial bank deposits have not recovered March outflows (St. Louis Fed)

{kind=link}

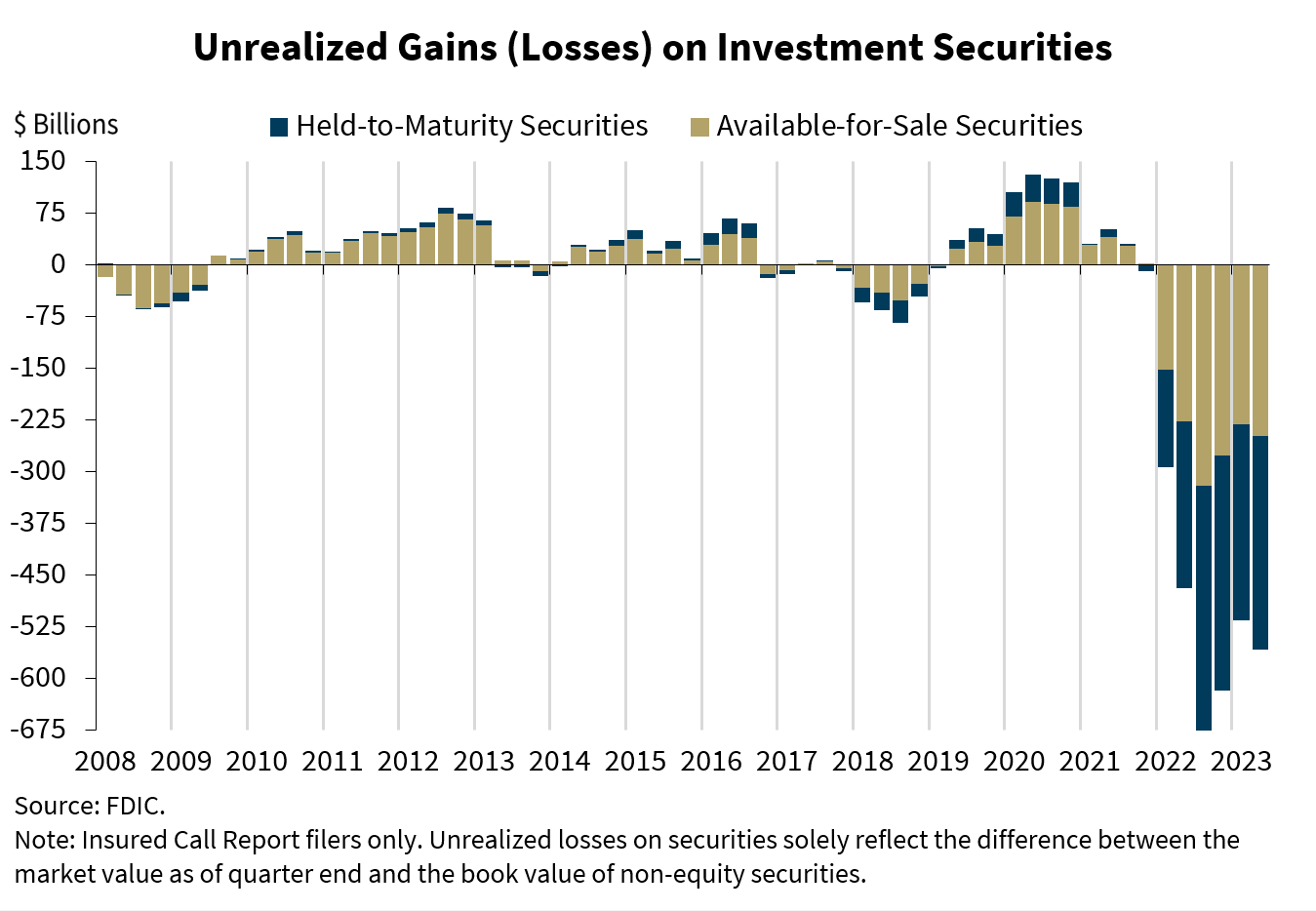

More importantly, the root cause of the regional bank crisis were unrealized losses on investment securities caused by rising interest rates. As of the end of Q2/2023, commercial banks had $558 billion in unrealized losses on their balance sheets, an increase of 8.3% QoQ according to latest data from the FDIC (Figure 5).

Figure 5 - Unrealized securities losses is still a major issue (FDIC)

{kind=link}

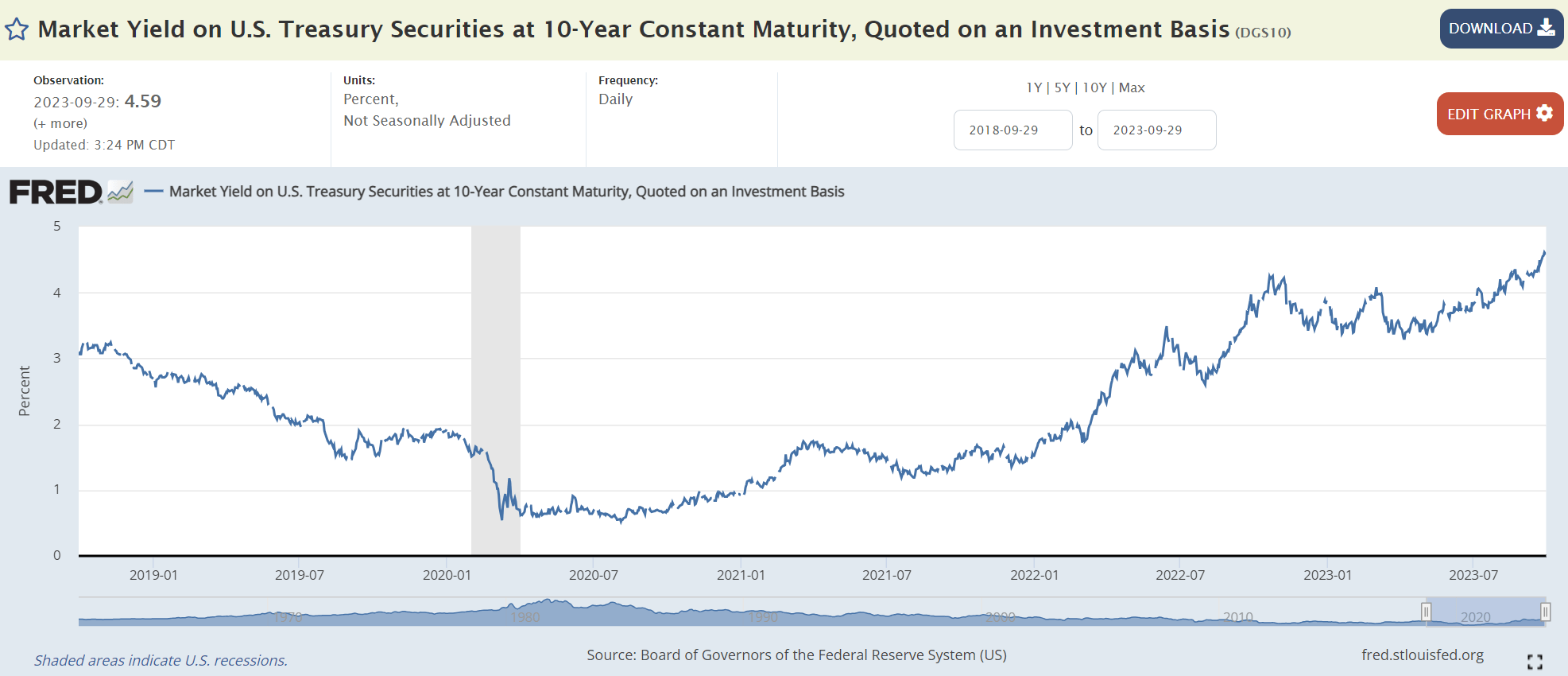

However, since the end of Q2, long-term treasury yields have continued to surge higher, with the 10Yr treasury yield recently touching 4.6%, far above their October 2022 peaks (Figure 6).

Figure 6 - 10Yr treasury yields have continued to surge higher (St. Louis Fed)

{kind=link}

If the unrealized losses on bank balance sheets were to be measured in real time, it is very likely that current unrealized losses would far exceed Q3/2022's peak of $690 billion, as the 10Yr yield was only 3.8% on September 30, 2022.

Bank Preferred Shares Have 'Gap Risk'

One major issue with financial preferred shares is that they are very prone to 'gap risk' , i.e., for a long period of time, financial preferred shares pay their contracted dividends and their valuations fluctuate very little. However, a systemic problem like the regional bank crisis can develop quickly and financial preferred shares can lose 100% of their value virtually overnight.

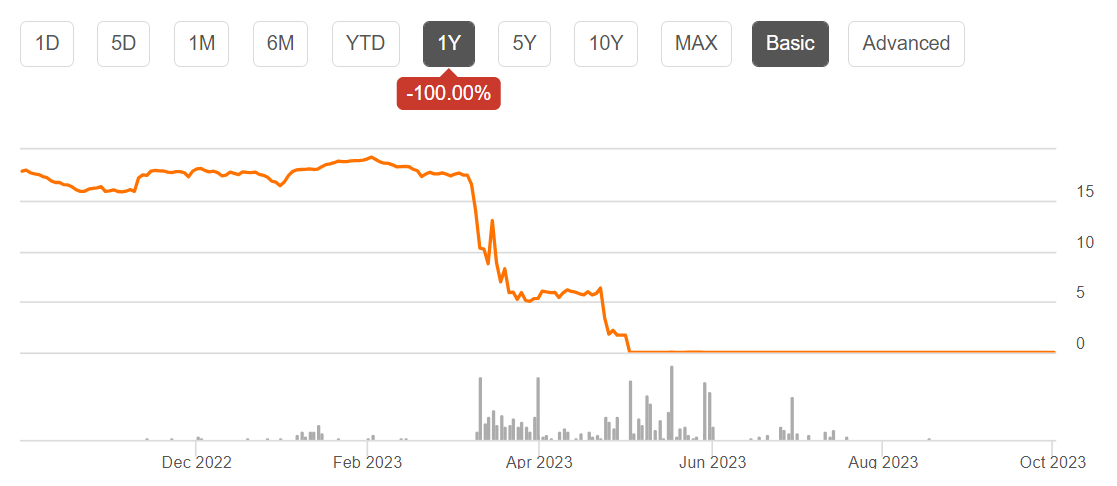

For example, preferred shares of First Republic Bank, one of the victims of this year's regional bank crisis, had traded between $16-19 for much of last year. Then almost overnight, they collapsed to $5 and then $0, as the bank was taken over by the FDIC and sold to JPMorgan (Figure 7).

Figure 7 - FRC preferred shares were wiped out virtually overnight (Seeking Alpha)

{kind=link}

While I am not suggesting that major money center banks like JPMorgan and Bank of America will 'go under' like First Republic Bank did in May, the risk of financial contagion from systemic risks is always present. In 2008 during the Great Financial Crisis, many financial giants like Lehman Brothers and AIG failed and their preferred shareholders were wiped out.

Furthermore, outside the money center banks, PFFD has plenty of exposure in smaller regional lenders like PACW and AXS that do not enjoy the implicit backing of the U.S. government.

Alternative To PFFD

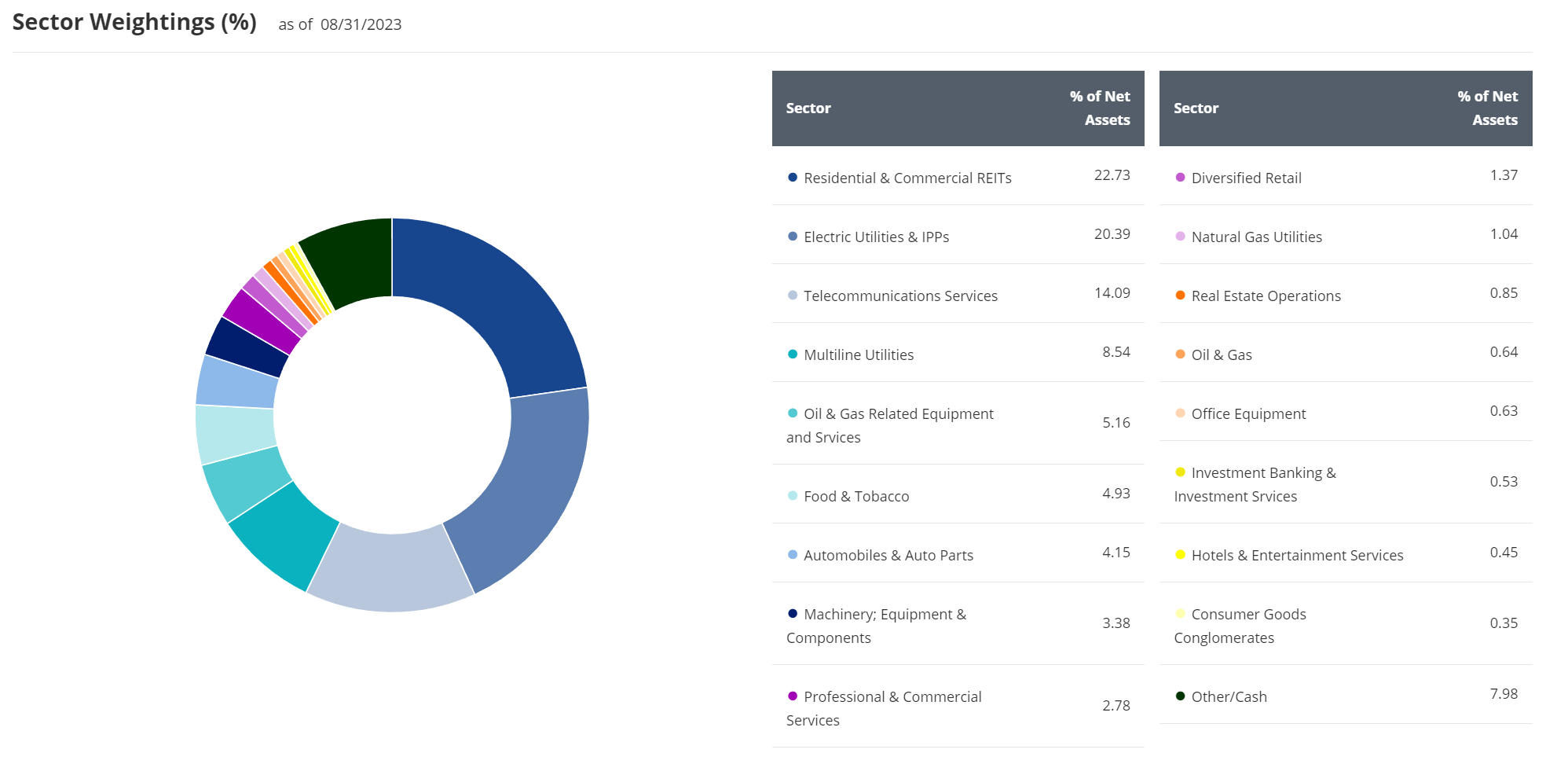

Instead of the financials-heavy PFFD, I recommend investors who want to invest in the preferred share asset class to consider the VanEck Preferred Securities ex Financials ETF ( PFXF ). PFXF, as its name suggests, invests in a portfolio of preferred shares of companies in diverse sectors, excluding financials (Figure 8).

{kind=link}

While PFXF will still suffer from drawdowns due to rising interest rates (fixed coupon preferred shares trade like bonds and are sensitive to rising interest rates), non-financial sector preferred shares usually do not have the same level of systemic risk as financial sector preferred shares.

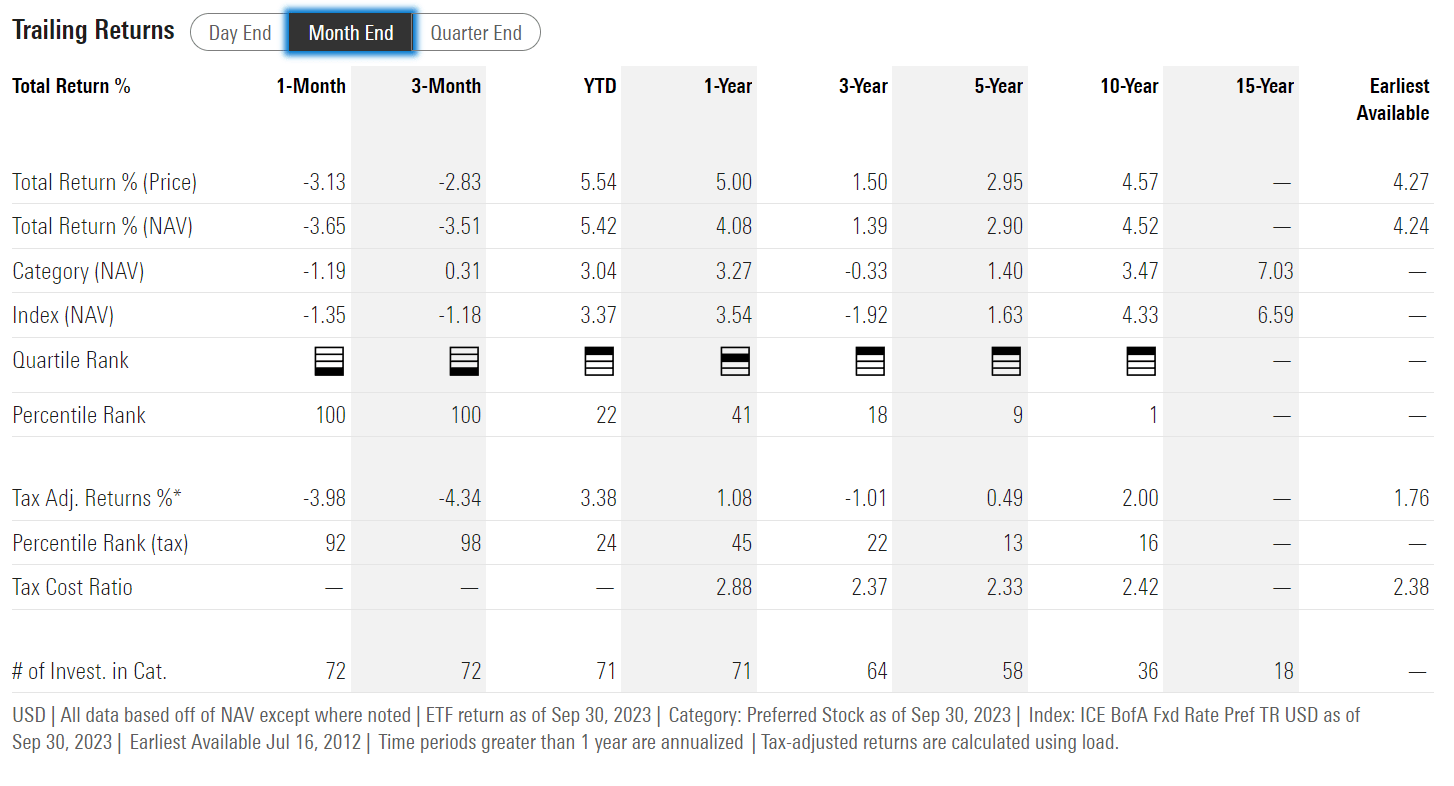

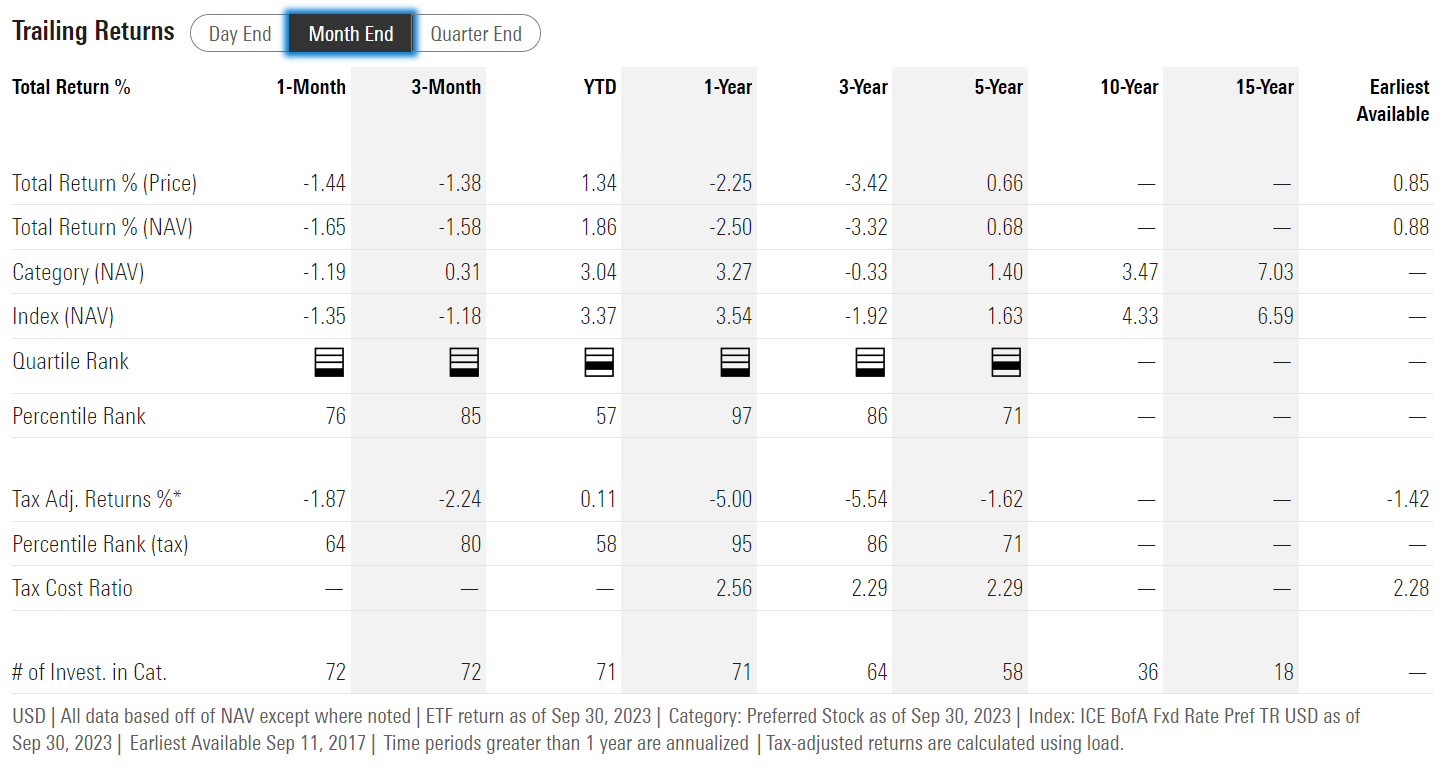

Comparing their performances, the PFXF ETF has outperformed the PFFD ETF on a 1-year, 3-year, and 5-year basis (Figure 9 and 10).

{kind=link}

{kind=link}

PFXF is currently paying a trailing 7.4% yield while PFFD only has a 6.7% trailing yield.

I last wrote about the PFXF here .

Conclusion

With 'higher for longer' interest rates, I continue to recommend investors take a cautious approach with the PFFD ETF. Simply put, the root cause of the recent regional bank crisis has not been resolved and may have gotten worse, as long-term interest rates are now materially higher than they were in March. The PFFD, with its 73% exposure to financial sector preferred shares, is prone to systemic risk.

Instead of the PFFD, I would recommend investors seeking preferred share exposure to consider the PFXF ETF, which invests in a diversified portfolio of preferred shares, excluding the financials sector. I rate the PFFD ETF a hold .

For further details see:

PFFD: Higher For Longer Interest Rates Detrimental To Preferred Shares