PFL - PFL: Market Appears Exuberant So Caution Could Be Advisable

2023-12-05 12:17:59 ET

Summary

- PIMCO Income Strategy Fund offers a high level of income with a double-digit distribution yield of 11.94%.

- The PFL closed-end fund's share price has increased by 7.49% in the past two months, outperforming the Bloomberg U.S. Aggregate Bond Index.

- The fund's objective is to provide current income while preserving capital, primarily investing in bonds with a small allocation to common equities.

- The fund appears as though it is covering its distribution right now, although it failed to accomplish this during the most recent fiscal year.

- The fund's share price has been outperforming its NAV recently, which is making it look pretty expensive.

The PIMCO Income Strategy Fund ( PFL ) is a closed-end fund, or CEF, that investors can employ in order to obtain an incredibly high level of income. As is the case with most of PIMCO’s closed-end funds, the PIMCO Income Strategy Fund has a double-digit distribution yield that works out to 11.94% at the current price. A few years ago, this would have been a bad sign. Prior to 2022 or so, any time a fund managed to obtain a double-digit distribution yield, it was a sign that the market expected that it would soon have to cut the distribution. However, that is not the case in today’s much higher interest-rate world. In fact, the fund’s current yield is roughly in line with that of most fixed-income funds today.

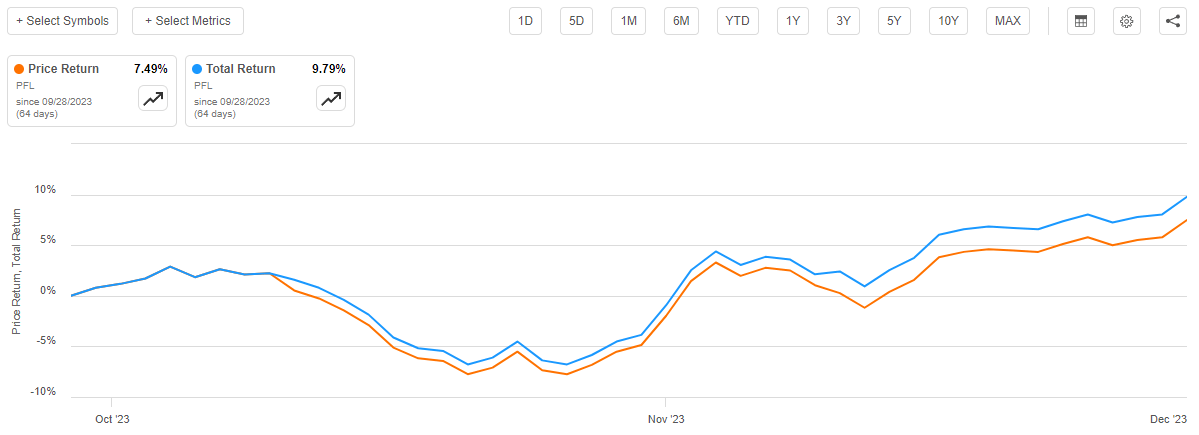

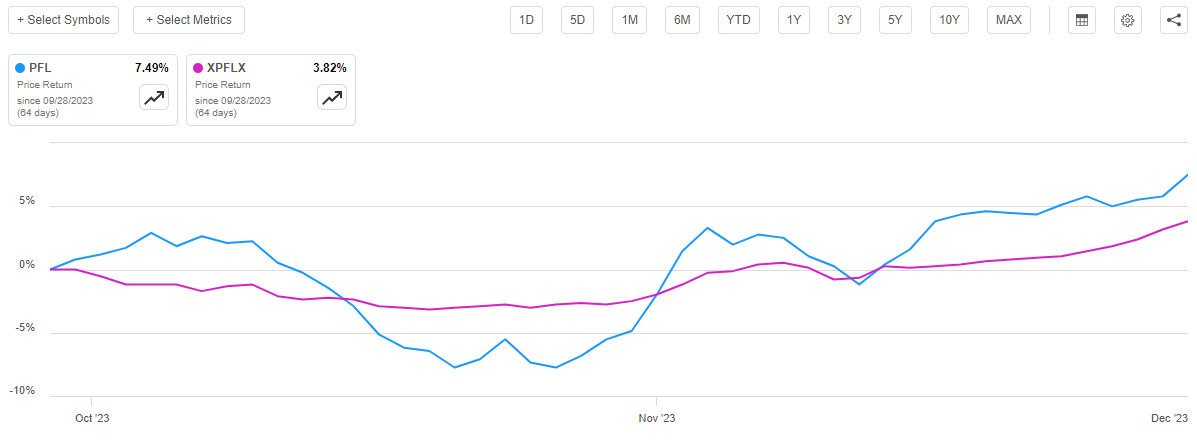

As regular readers will undoubtedly recall, we last discussed this fund around the end of September. Although that was only two months ago, it almost feels like a completely different time as interest rates were rising in September as opposed to the decline that we have seen over the past month. This decline in interest rates has had a positive impact on this fund’s share price and market performance over the past two months. As we can see here, the PIMCO Income Strategy Fund’s share price is up 7.49% and investors who purchased the fund on the date that my last article was published are up 9.79% since the date of publication:

{kind=link}

This compares to a 2.87% increase in the Bloomberg U.S. Aggregate Bond Index ( AGG ) over the same period. As such, it might be possible that the PIMCO Income Strategy Fund has become overbought in response to the decline in long-term interest rates. After all, the fund’s net asset value is only up 3.82% over the same period. This would not be uncommon for a PIMCO fund though, as funds from this fund house tend to outperform during bond market rallies.

Naturally, though, we should investigate further and see if purchasing this fund today makes any sense. After all, anyone buying today will not benefit from the price appreciation that the fund has seen over the past two months.

About The Fund

According to the fund’s website , the PIMCO Income Strategy Fund has the objective of providing its investors with a very high level of current income while still ensuring the preservation of capital. This is not an especially surprising objective. After all, PIMCO is incredibly well known and well respected as a fixed-income house. As such, we expect that most of its funds will be invested in bonds or other fixed-income securities, which is certainly the case with this fund. As we can see here, 157.56% of the fund’s net assets are invested in bonds, although it does have a surprisingly large 6.55% weighting to common equities:

CEF Connect

This objective makes sense because bonds are by their very nature a current income vehicle. As I explained in my previous article on this fund:

A bond investor purchases a bond at face value, receives regular coupon payments that serve as income, and then receives the face value back when the bond matures. Over its lifetime, the only investment return that is delivered by the bond is the coupon payments. There are no net capital gains over time because bonds have no inherent link to the growth and prosperity of the issuing company.

As bonds have no net capital gains over time, it would not really make sense for the fund to have capital appreciation or total return as its objective. Current income makes sense though because that is how bonds deliver all of their net investment returns.

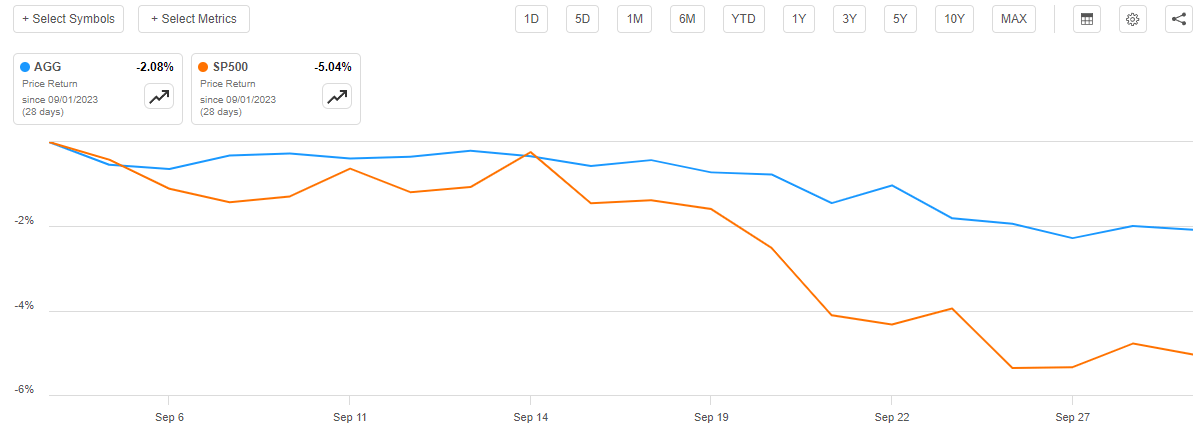

Interestingly, the fund has reduced its bond weighting recently. In the previous article, we saw that 176.94% of the fund’s net assets were allocated to bonds alongside a 5.98% common stock weighting. Thus, the fund has greatly decreased its bond weighting while increasing its common stock weighting. It is possible that this was not done intentionally, as having the stocks greatly outperform bonds might have had that effect, but this is probably not very likely. As we can see above, CEF Connect’s asset allocation chart for this fund is dated September 30, 2023. The chart in the previous article on the fund was dated August 31, 2023. As such, the changes that we see to the fund’s asset allocation occurred during the month of September. During the month of September 2023, the S&P 500 Index (SP500) was down 5.04% but the Bloomberg U.S. Aggregate Bond Index was only down 2.08%:

{kind=link}

As such, the logical conclusion here is that the bonds in this fund’s portfolio probably outperformed the common stocks. We should not expect that the common stock weighting would have increased during the period if all of the changes were simply based on market performance.

That is especially true when we consider the common stocks that this fund is invested in. The fund’s annual report states that the fund’s common equities are mostly drilling companies and financials:

Fund Annual Report

With that said, we do not know for certain that Drillco Holding Lux SA is a foreign energy company. The fund has it listed as an industrial company, not as an energy firm. The annual report includes no description of what exactly this company does or really any details about it. However, there is something called a “DrillCo” transaction that occasionally occurs in the energy space. It is basically a private joint venture between an energy producer and a private equity investor. Frost Brown Todd, a law firm that has some expertise in these transactions, explains on its website :

In a DrillCo transaction, an investor agrees to fund all or a significant portion of the drilling costs for a certain number of wells in exchange for a percentage interest in the oil and gas lease or the well, which is called a working interest. The drilling costs that the working interest owner funds include a portion of the costs associated with the exploration, drilling, and production of a well.

In a DrillCo transaction, an operator contributes acreage, and the private equity investor contributes cash to cover most of or all of the costs associated with drilling oil wells. In exchange for putting up the capital, the investor earns and is assigned a working interest in the wells drilled.

It is possible that Drillco Holding Lux is simply a private company that purchased a working interest in some oil wells and was invested in by this fund. The iShares Global Energy ETF ( IXC ) was up 0.71% during the month of September, so it is certainly conceivable that this particular position outperformed the bonds in the portfolio and thus increased the fund’s stock position month-over-month. However, as this appears to be a private company that is not traded on any exchange, there is no way that we can be certain of this.

However, the fund only has a 35.00% annual turnover, so it does not appear that it is engaging in a significant amount of trading activity that would have affected its asset allocation to the degree that we see here. That is not an especially high turnover for a fixed-income fund, although it is not the lowest ratio in the industry. It is also relatively in line with other PIMCO funds, as was seen in my previous article on this fund. As such, the fund should not have extraordinarily high trading expenses that naturally place a burden on the fund’s management.

As mentioned earlier in this article, the PIMCO Income Strategy Fund has delivered a remarkably strong performance in recent weeks due to the market’s expectations that the Federal Reserve will cut rates over the next year. The federal funds futures market is currently pricing in 125 basis points of cuts next year, and some analysts are expecting far more aggressive cuts than that. For example, Swiss banking giant UBS expects 275 basis points of cuts next year. According to Business Insider :

The US economy will slip into recession next year – and that’ll lead to the Federal Reserve bringing in steep interest rate cuts, according to one top European bank.

UBS said Tuesday that it’s expecting the Fed to respond to falling inflation and an economic slump by slashing rates by an eye-popping 275 basis points – nearly four times the 75-basis-point reduction the market is currently expecting.

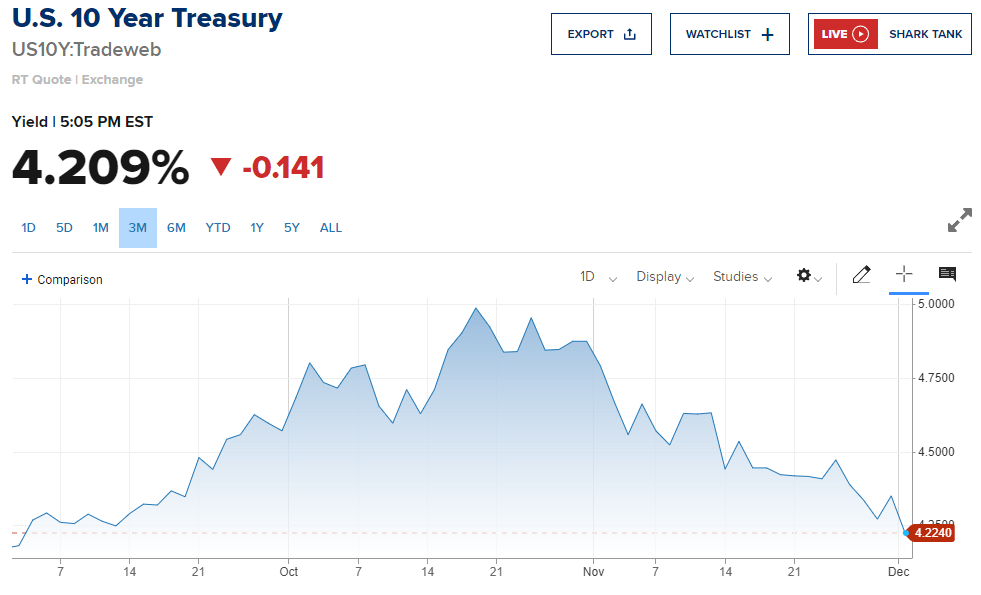

There are other banks that are not as aggressive with their rate cut predictions, but pretty much everybody is expecting that the Federal Reserve will significantly reduce the federal funds rate next year. This is the reason why the yield of the ten-year U.S. Treasury (US10Y) has fallen from 4.9880% in mid-October to 4.209% today:

{kind=link}

Basically, investors are so convinced that interest rates will be much lower a year from now than they are today that they are willing to lock up money for ten years at a 100-basis-point discount to today’s levels.

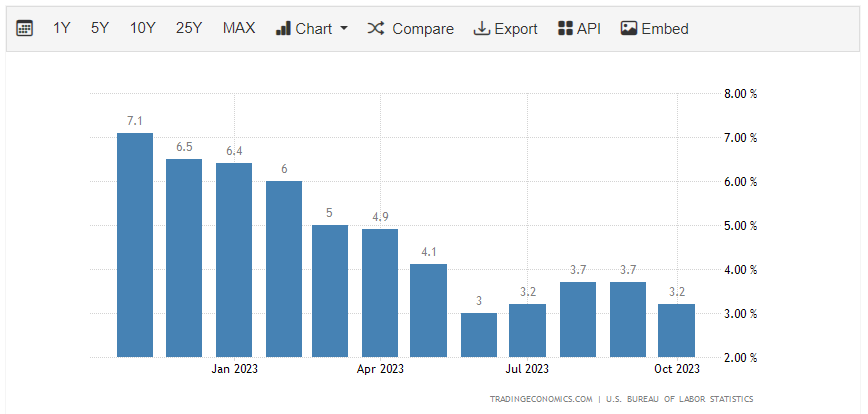

However, the officials at the Federal Reserve are not so convinced that interest rates will be cut to anywhere close to the magnitude that the market is expecting. First of all, despite all of the spin about falling inflation, the year-over-year increase in the consumer price index is still much higher than the Federal Reserve’s target of 2%. The most recent inflation report puts the year-over-year increase in the aggregate price level at 3.2%:

{kind=link}

The core consumer price index, which excludes volatile food and energy prices, is still running at a 4% annual growth rate. That is double the Federal Reserve’s long-term target, and central bank officials have long maintained that they will not cut interest rates until inflation is sustainably under 2%. It is difficult to see how that will happen outside of a severe recession, and it is a fair bet that the policymakers in Washington, D.C. will do everything in their power to avoid a recession during a presidential election year.

Thus, despite the market’s conviction that a recession is imminent and will cause interest rates to be cut, there is no guarantee that this will be the case. The shares of the PIMCO Income Strategy Fund have been driven up by much more than the performance of its portfolio justifies over the past two months, and it will almost certainly give up these gains if the market is incorrect about the rate cuts. However, if the market is correct, and a recession does occur that forces the central bank to cut rates, the fund’s shares could still have some room to run. It might be a good idea to hedge a position in this fund with a good floating-rate fund or a dynamic income fund just in case. A position like that would allow for investment profits regardless of the direction of interest rates.

Leverage

As we saw earlier in this article, the PIMCO Income Strategy Fund has more than 100% of its net assets invested in bonds. It is able to do this because of the fund’s use of leverage. I explained how this works in my previous article on this fund:

In short, the fund will borrow money and then use that borrowed money to purchase bonds and other debt securities. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case. With that said though, the beneficial effects of leverage are not as great today as they were two years ago when interest rates were at 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not taking on too much leverage because that would expose us to too much risk. I generally do not like to see any fund have leverage exceeding a third as a percentage of its assets for that reason.

As of the time of writing, the PIMCO Income Strategy Fund has leveraged assets comprising 25.39% of its overall portfolio. This is considerably less than the 26.13% leverage ratio that the fund had the last time that we discussed it, which makes a lot of sense because the fund’s net asset value is up. As mentioned in the introduction, the PIMCO Income Strategy Fund has seen its net asset value per share increase by 3.82% since the date that the prior article was published:

{kind=link}

We can immediately see that this is less than the fund’s share price appreciation over the same period, which could become important when we attempt to value this fund later in this article. The fact that its net asset value is up though means that static leverage would account for a smaller percentage of the fund’s overall portfolio. This is exactly what we see here.

As was the case the last time that we discussed this fund, its leverage represents a pretty good balance between risk and reward. We should not have to worry too much about the fund’s use of debt right now.

Distribution Analysis

As mentioned earlier in this article, the PIMCO Income Strategy Fund has the primary objective of providing its investors with a very high level of current income. In pursuance of this objective, the fund invests in a portfolio that primarily consists of both junk and investment-grade bonds. These securities deliver the majority of their returns in the form of direct payments to the investors, and as of right now tend to have fairly high yields. For example, the Bloomberg High Yield Very Liquid Index ( JNK ) has an average yield-to-maturity of 8.44% right now. The fund collects the payments that it receives from these assets and combines them with any capital gains that it manages to realize by trading bonds prior to maturity. The fund employs leverage to allow it to control more securities than it otherwise could based solely on its net assets, which allows it to boost the payments that it has coming in. The fund then pays out all of the money that it receives from these various activities to the shareholders, net of its own expenses. As such, we might expect that this fund would have a remarkably high current yield.

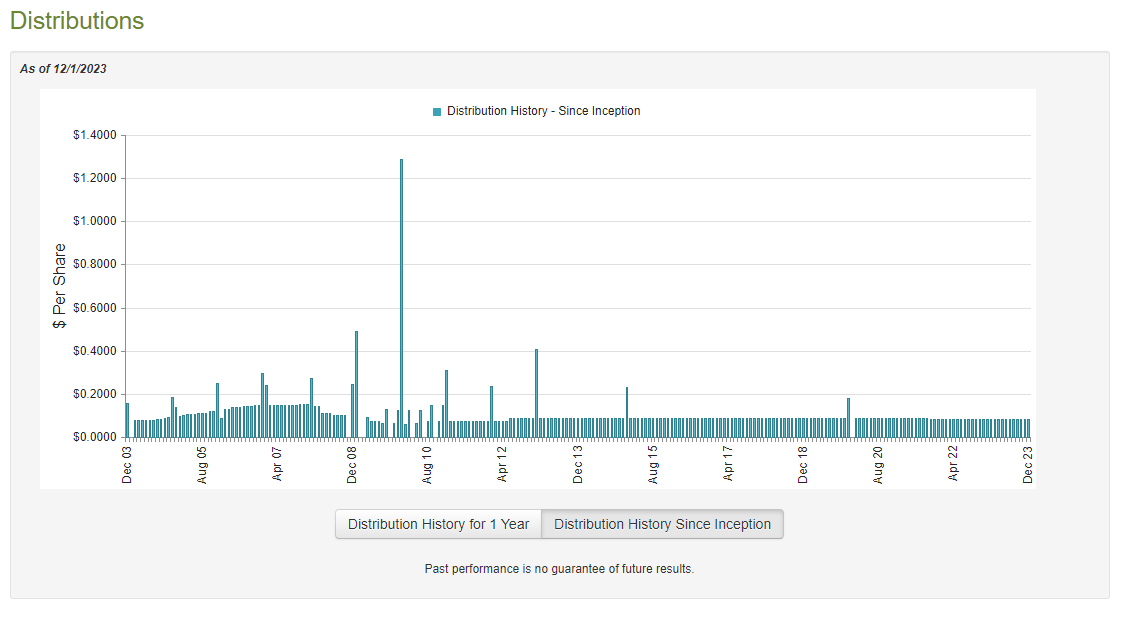

That is certainly the case, as the PIMCO Income Strategy Fund pays a monthly distribution of $0.0814 per share ($0.9768 per share annually), which gives it an 11.94% yield at the current share price. This is reasonably in line with PIMCO’s other funds, as well as most other fixed-income funds currently on the market. This fund’s distribution history is a bit better than that of most other funds though, as it has tried to keep a very stable distribution over the past decade:

{kind=link}

We can see that the fund only made one distribution cut in the past ten years, and otherwise has proven to be remarkably stable over time. This is somewhat surprising as that is a feat that very few other fixed-income funds have managed to achieve. That is something that we want to investigate, as it seems strange that the fund could pull off a task that few other funds have been able to accomplish. It also seems a bit strange that the fund could maintain its distribution in both 2022 and 2023 despite the rapid rise in interest rates and the pressure that was placed on bond valuations. After all, just about every bond fund took losses during this period and had to cut their distributions in order to avoid having the distributions be destructive to the fund’s net asset value.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report (linked earlier) corresponds to the full-year period that ended on June 30, 2023. This is a pretty good period for the report to cover, as it will give us a good idea of how well the fund performed during the bond bear market that characterized the second half of 2022 as well as the euphoria that erupted in the first half of 2023 when investors and market participants began to expect near-term rate cuts. While those near-term rate cuts never actually transpired, the fund still might have had some opportunities to sell appreciated assets at a profit.

During the full-year period, the PIMCO Income Strategy Fund received $40.115 million in interest and $328,000 in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $40.471 million during the period. The fund paid its expenses out of this amount, which left it with $31.979 million available for investors. Unfortunately, this was not sufficient to cover the $36.222 million that the fund paid out in distributions during the period. That is likely to be concerning at first glance as we would generally like a fixed-income fund to be able to fully fund its distributions out of the net investment income. This one clearly failed to accomplish this.

However, there are other methods through which the fund can obtain the money that it requires to cover the distribution. For example, the fund might have been able to make some profits by exploiting interest rate changes and trading securities. Unfortunately, the fund failed miserably at that task during the full-year period. The PIMCO Income Strategy Fund reported net realized losses of $7.689 million and had another $9.012 million in net unrealized losses over the year. Overall, the fund’s net assets declined by $1.265 million after accounting for all inflows and outflows during the period. Admittedly, this does not seem that bad, but the only reason why the decline was not worse is that this fund conducted a $19.502 million capital raise during the period. Its net asset decline would have been worse in the absence of this raise.

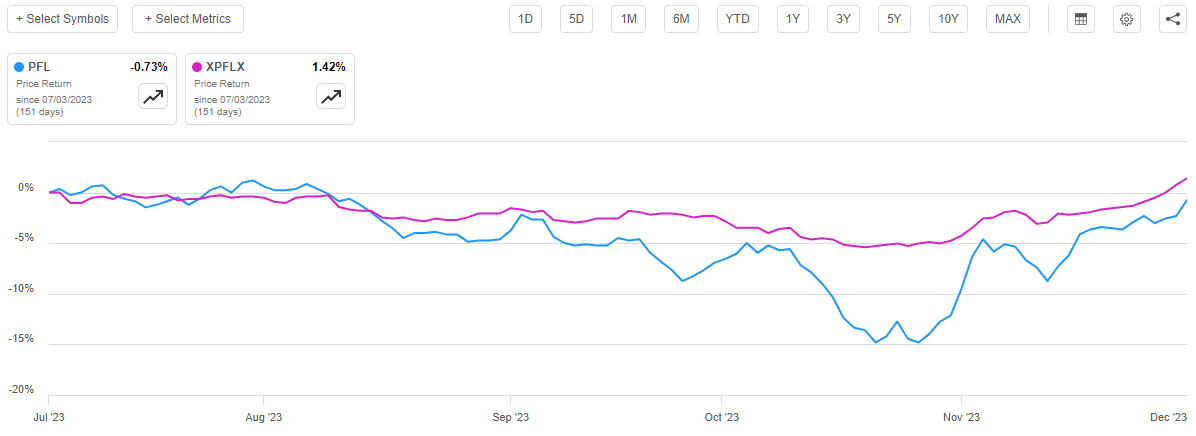

Overall, the fund failed to cover its distribution during the most recent full-year period, which is concerning. There might be some reason for optimism, however. As we can see here, the fund’s net asset value per share is actually up 1.42% since July 1, 2023:

{kind=link}

This indicates that the fund has managed to fully cover its distributions during its most recent fiscal year. If indeed it proves to be the case that interest rates continue to decline over the next several months, the distribution could be in pretty good shape. There is no guarantee that this will be the case, however.

Valuation

As of November 30, 2023 (the most recent date for which data is currently available), the PIMCO Income Strategy Fund has a net asset value of $7.83 per share but the shares trade for $8.18 each. This gives the fund’s shares a 4.47% premium on net asset value at the current price. That is quite a bit worse than the 2.16% discount that the shares have had on average over the past month, and it is almost certainly caused by the fund’s shares outperforming the fund’s portfolio over the past two months or so. As such, it might be advisable to employ caution when purchasing this fund, as it looks like the shares are overpriced.

Conclusion

In conclusion, the PIMCO Income Strategy Fund is a pretty popular fund among income investors and could be reasonably well positioned to deliver gains if long-term interest rates continue to decline and push up bond prices. It does appear that there is a certain amount of exuberance surrounding this particular fund, though, as PIMCO Income Strategy Fund’s recent share price gains have been far in excess of the performance of its underlying portfolio. As there is no guarantee that the market is correct about the magnitude of the potential interest rate cuts next year, it might be advisable to be cautious about buying the fund unless it starts trading at a discount.

For further details see:

PFL: Market Appears Exuberant, So Caution Could Be Advisable