PFN - PFN: A Year Later The Bull Case Is Still Hard To Make

2023-08-01 23:43:00 ET

Summary

- The article evaluates the PIMCO Income Strategy Fund II as an investment option.

- There is merit to owning as an equity hedge and for a more risk-on-income play. But challenges put some pressure on that thesis.

- PFN's value has not significantly changed since last year, and I recommend holding rather than buying.

Main Thesis & Background

The purpose of this article is to evaluate the PIMCO Income Strategy Fund II ( PFN ) as an investment option. The fund's objective is "to seek high current income, consistent with the preservation of capital." The fund achieves this by employing a multi-sector approach, investing in a diversified portfolio of floating and/or fixed-rate debt instruments in both investment-grade and junk level credit.

This is a fund I continuously have on my radar, along with most of the PIMCO CEF family. I considered buying it at this same time last year but ultimately felt the value just wasn't there. While I saw some merit as an income play, I felt total return would be pressured and I was completely spot-on in that assessment over time:

Fund Performance (Seeking Alpha)

As equities have continued to climb in 2023 I have been on the lookout for alternative investments and/or equity hedges to protect my gains. This led me back around to PFN for consideration. Unfortunately, I don't see much of a change for PFN compared to last year. There are some positive attributes, but also some negatives that lead me to believe "hold" remains the right call. I will explain why in detail below.

Still Charges A Premium (Albeit A Smaller One)

One immediate sore spot for me is the fund's valuation. At time of writing (8/1), PFN is sitting with a premium to NAV at right around 5%. This is on the cusp of the premium level where I generally start to see limited value and this CEF is no exception to this rule:

PFN's Facts (PIMCO)

The good news is the fund's premium has come down a bit over the past year. Back in August 2022, when I wrote the prior review, PFN had a premium in excess of 8%. This was a clear "avoid" flag for me personally. At 5%, it is not as dangerous, and it shows that most of the loss PFN has experienced has simply been to premium reduction rather than a deteriorating underlying value. That helps support the idea that current owners of this fund hold on.

Ultimately this attribute is a bit subjective. On the one hand it shows the danger of buying funds at a premium. Over the last year PFN pumped out a high income stream and held up reasonably well. But premium compression left investors worse off than it they had simply held cash. On the other hand it exemplifies a sharply cheaper buy-in price now. This could mean the worst is over and gains could be ahead - especially if the yield stays constant. With other PIMCO CEFs trading at substantially higher premiums, this is definitely a possibility. This pull-push scenario is central to supporting my "hold" rating.

Could This Be A Hedge?

Looking at the macro-backdrop is a key reason why I even gave PFN (or any debt fund for that matter) consideration right now. The equity market has been very rewarding over 2023 and I certainly don't want to mess with a good thing! Yet, I am getting to the point where I want to protect my calendar year gains. This means shifting to cash, limiting my new buys, and, of importance to this review, considering bonds and other debt funds.

There are multiple reasons for this. Aside from equities simply moving very far, very fast this year, sentiment is making a similar move. That is more concerning to me than absolute values of the major indices. When I see sentiment get too one directional, I get cautious and ready to start taking the opposite side of the bet.

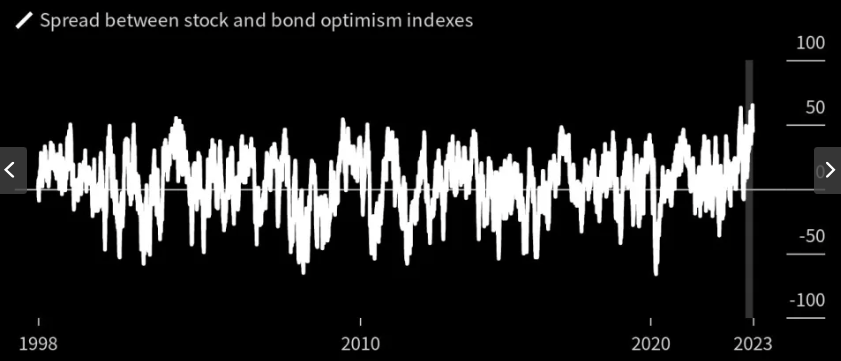

I believe we are approaching those levels currently as sentiment for equities (in comparison to bonds) has reached its largest spread in over two decades:

Stock Optimism (versus bonds) (Bloomberg)

{kind=link}

The point to emphasize here is this is not solely relevant to PFN. I do see this spread between equities and bonds as a theme to rotate in to fixed or floating rate debt instruments. That could provide a boost to PFN to be fair. But that is also true for the plethora of options investors have in this space. Therefore, while this can go in the "plus" column for PFN, there have to be other compelling factors to make me choose this particular CEF. That is the struggle I am having with this fund at the moment.

High Yield Credit Showing Mixed Signals Too

I will now shift my attention to the high yield credit market. This is of paramount important to PFN because it represents over 42% of total fund assets. So it is clearly going to drive gains or losses for this fund over all. And something else to note is that this figure has risen from 34% since last August. This makes high yield credit an increasingly important sector for buyers/investors of the fund:

PFN's Sector Breakdown (PIMCO)

With this reality I am especially critical of the high yield sector because it is overweight in this fund. I (or any investor) will want to be extremely confident in this sector before buying PFN - otherwise this is clearly not the right fund for you!

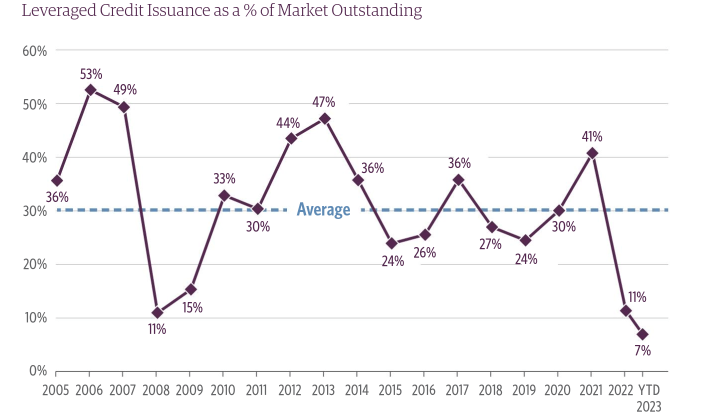

With that in mind, I have some concerns about the outlook for this sector as a whole. This is not unique to PFN in isolation. I would have these concerns for any CEF (or ETF) that held a lot of non-investment grade assets. But it is relevant here as a result. One development that immediate comes to mind is the amount of credit issuance for leveraged credit (loans) that make up the bulk of PFN's portfolio. There has been a big pullback in capital availability, and history suggests this scenario typically precedes an uptick in defaults across this space (with most occurring in high yield rated securities):

Leveraged Credit Issuance (% of market outstanding) (Guggenheim)

{kind=link}

This is not a guarantee by any means. But it is a warning sign. If macro-conditions deteriorate, rates stay here, and credit availability is tight, then defaults and delinquencies are likely to increase. It is hard to see a way around that. If so, the underlying assets of PFN will see their values come under pressure and that will in turn limit the opportunity for investors.

What this boils down to is that companies that didn't hedge interest rate risk - especially in highly leveraged sectors - could struggle to service their debt and they will have limited options for refinancing. In environments when capital is readily available, issuers can simply access new credit streams to pay off the maturing loans. But if credit is not available and that debt is due - they have to pay it or go in to some level of delinquency. Not a pleasant thought for investors in this debt.

Income Metrics Leave Much To Be Desired

Some of the challenge I mentioned in the prior paragraph is starting to weave its way in to PFN's actual income outlook already in my view. Specifically, coverage ratios are quite weak and the fund does not have any UNII balance to hedge against a continued downturn in income production:

{kind=link}

This is a key concern for me since buying for income is a primary reason for owning PFN. If the income isn't safe, then the buy case is difficult to make. Given the headwind of weak income metrics, it makes me curious why someone would want to pay a premium price for this fund. It is not a strategy I would advocate for and reaffirms my neutral outlook going forward.

Is High Yield A Value Play?

My next thought against looks back at the high yield sector on a global basis - as PFN does invest in both US and non-US assets. With this in mind - is there value in this space right now? Is there merit to owning this sector as an equity hedge, or just owning it outright for other reasons, because it is under-valued?

On this front, I would suggest no. I am not saying this is a bad investment idea. I don't want to give that impression. I see merit to owning this sector, and PFN by extension, as a risk-on, high income play. But the question is around value. Is this an undervalued corner of the market? Based on current spreads that does not appear to be the case:

Current Spreads (Global High Yield) (Barclays)

What I draw from this is from a valuation perspective the opportunity here is reasonable. Spreads suggest a normalized income - value proposition and that is not a clear buy or sell sign. When this is the case, I think this is yet again another attribute that is supportive of my "hold" rating.

Defaults Have Been Ticking Up

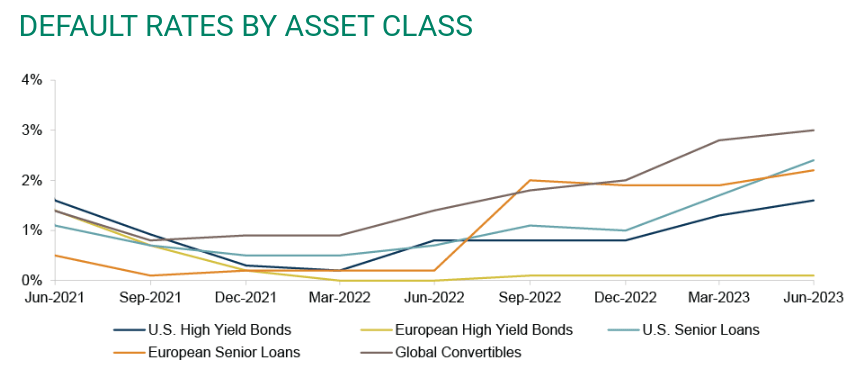

My final point looks at another area of concern and that is actual defaults. Both high yield bonds - domestic and foreign - as well as loans are seeing an uptick in defaults over the calendar year. That is not an encouraging sign:

Default Rates (By Sector) (Credit Suisse)

{kind=link}

The good news is that default rates are still quite low. While they are up noticeably, that is from rock bottom levels in 2022 and early 2023. So the uptick is not a massive concern at the moment - unless it continues.

And that is the rub. Will it continue? Given weakening macro-fundamentals and tighten credit availability it very well might. This means that the high income and potential for capital appreciation need to be weighed carefully against the possibility of a recession and increasing default/delinquency figures. This is a backdrop readers should weigh very carefully before they make any decisions with respect to PFN.

Bottom-Line

PFN has seen a modest loss over the past year and there continue to be reasons for concern in the months ahead. The pressure on leveraged funds with an inverted yield curve remains, the premium to NAV makes the fund a richly priced option, and global high yield products are seeing some weakness. There is a buy case for those who want income and are willing to take above-average risks, but that may not be right for more risk-off and passive investors. Due to this dynamic, I don't see the merit to an upgrade here. I will keep the "hold" rating in place for the second half of 2023 unless something fundamentally changes.

For further details see:

PFN: A Year Later, The Bull Case Is Still Hard To Make