PAXS - PFN: This Popular Bond Fund May Be Riskier Than Believed

2023-12-17 03:57:00 ET

Summary

- The PIMCO Income Strategy Fund II is a popular way for investors to earn a high level of income.

- The fund yields 12.15% at the current share price, but it failed to cover it in the most recent fiscal year.

- The fund has been performing very well over the past few months, but the market appears optimistic on the magnitude of the 2024 rate cuts.

- The fund can switch between floating-rate and fixed-rate securities, but it compares very poorly against other options in this respect.

- The fund currently trades at a slight premium, which may not be justified considering the risks here.

The PIMCO Income Strategy Fund II ( PFN ) is a closed-end fund that income-focused investors can employ in pursuit of their goals of earning a very high level of current income from the assets in their portfolios. As is the case with most of PIMCO’s fixed-income funds, this one boasts a very attractive double-digit yield, so it certainly manages to perform admirably at that task. As of the time of writing, the PIMCO Income Strategy Fund II has a 12.15% distribution yield. Here is how this compares to PIMCO’s other closed-end funds:

| Fund |

| Current Distribution Yield |

| PIMCO Income Strategy Fund II |

| 12.15% |

| PIMCO Income Strategy Fund ( PFL ) |

| 11.74% |

| PIMCO Dynamic Income Opportunities Fund ( PDO ) |

| 12.61% |

| PIMCO Access Income Fund ( PAXS ) |

| 12.71% |

| PIMCO PCM Fund ( PCM ) |

| 11.66% |

This clearly confirms that most of PIMCO’s funds have relatively comparable yields. This is not particularly surprising considering that all of them are investing in fixed-income vehicles and basically rely on the same basic research as everything else bearing the name of this fund house. As such, income investors do not really have to sacrifice much in the way of yield by favoring the PIMCO Income Strategy Fund II as opposed to its sister funds.

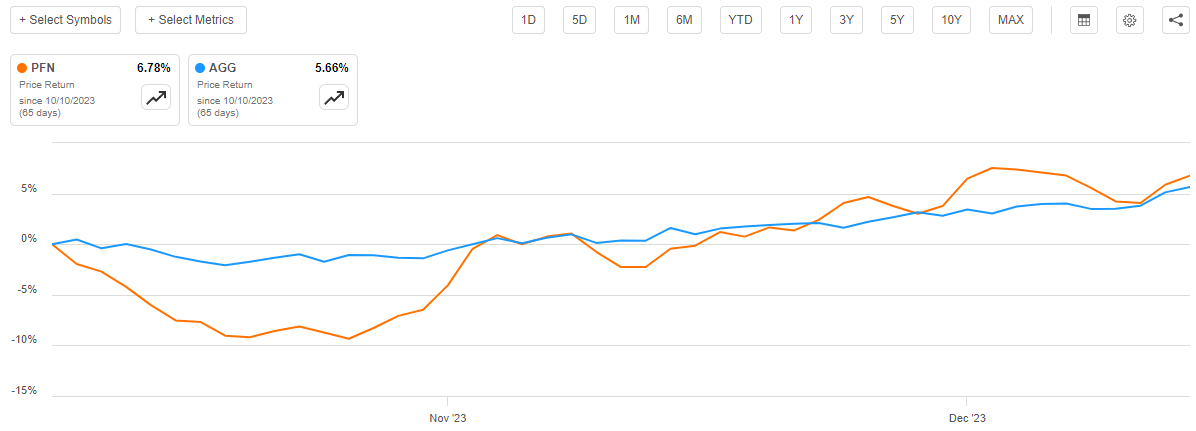

As regular readers can likely recall, we previously discussed this fund in the middle of October. The bond market has generally been very strong since that time, as investors generally started front-running the Federal Reserve in anticipation of a pivot and interest rate cuts next year. This has driven up the share price of this fund fairly significantly, as shares of the PIMCO Income Strategy Fund II are up 6.78% since the date that my previous article on this fund was published. This was quite a bit better than the 5.66% price appreciation that the Bloomberg U.S. Aggregate Bond Index ( AGG ) delivered over the same period:

{kind=link}

However, it is possible that the market has got ahead of itself. While the Federal Reserve did guide for interest rate cuts at its meeting earlier this week, the projections provided by the Federal Open Market Committee still indicate a desire on the part of the central bank to keep financial conditions much tighter than the market is projecting. As such, anyone purchasing the fund at today’s price may be exposing themselves to a very real risk that the recent gains will reverse at some point next year. With that said though, many income investors are more interested in how well the fund can sustain its distribution than they are in worrying about minor short-term price swings so we will be sure to pay special attention to that in our analysis.

Let us investigate and see if purchasing this fund could make sense today.

About The Fund

According to the fund’s website , the PIMCO Income Strategy Fund II has the objective of providing its investors with a high level of current income while ensuring the preservation of capital. This makes a lot of sense for a fixed-income fund. In fact, a number of bond funds of both the open-ended and closed-ended varieties have this as their objective. It makes a lot of sense when we consider how bonds work. After all, as I explained in my previous article on this fund:

This is a very common objective for a bond fund, as bond investors who are willing to hold their assets until maturity are guaranteed not to lose money unless they are foolish enough to purchase a bond when it has a negative yield-to-maturity.

The exception to this rule is if the issuing entity defaults, but such events are fairly rare.

As such, all that a bond fund really needs to do in order to ensure that it maintains the value of its principal is to purchase bonds and then hold them until maturity. There are a few bond funds that are occasionally seen in employer-sponsored retirement accounts that do exactly this. The total return produced by most of these funds tends to be fairly low, especially today since they have a substantial weighting towards those bonds purchased over the past decade or so when rates were much lower than today, but that strategy does pretty well at avoiding the loss of money.

Most of PIMCO’s funds do not use a buy-and-hold strategy, and the PIMCO Income Strategy Fund II is no exception to this rule. The fund’s 33.00% annual turnover suggests that it is engaging in some trading activity, although it is certainly not trading assets nearly as much as an equity fund might. This is nice as it helps to keep the fund’s expenses down since it costs money to trade bonds or any other assets. Its expenses are still substantially higher than an index fund, though:

{kind=link}

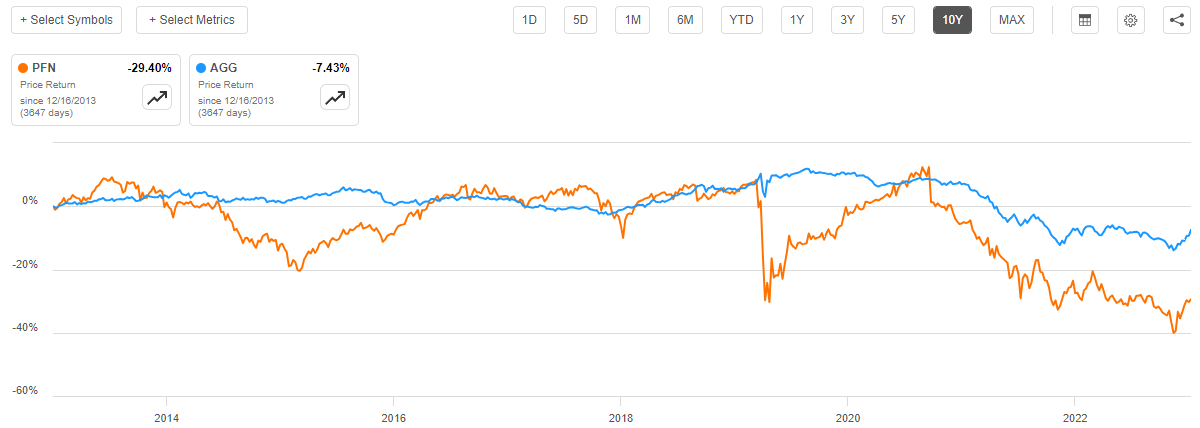

The 4.09% expense ratio that we see here certainly appears to be very steep, although it might be worth it if the fund is able to deliver a return that is suitably above that of the market. This fund does appear to be doing fairly well at this task, as long as we include the distributions that it pays out as part of the return. As we can see here, over the past ten years, the share price of the PIMCO Income Strategy Fund II has declined by 29.40% compared to a 7.43% decline in the Bloomberg U.S. Aggregate Bond Index:

{kind=link}

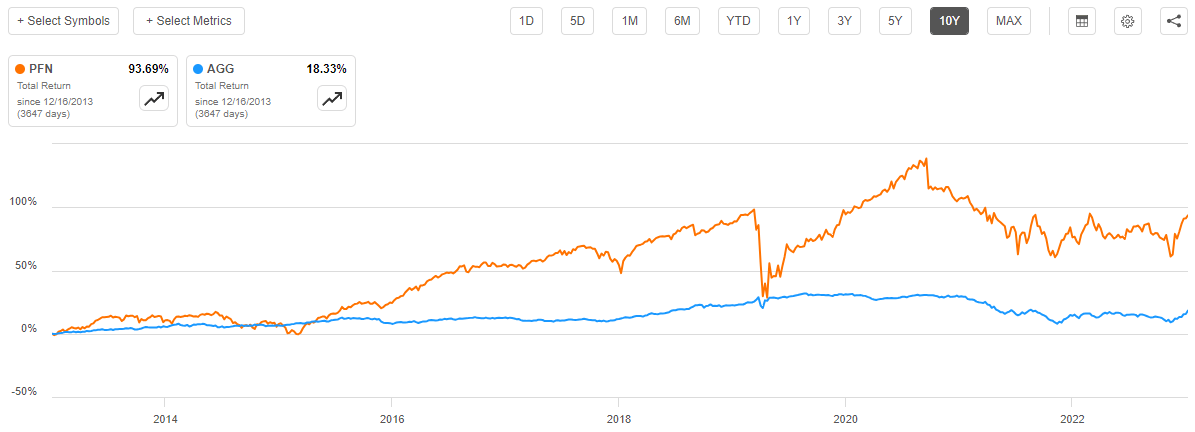

However, when we consider the distributions that the two assets have paid out over the period, the PIMCO Income Strategy Fund II beats the index by a country mile. Over the past ten years, investors in the PIMCO Income Strategy Fund II have gained 93.69% compared to an 18.33% gain in the Bloomberg U.S. Aggregate Bond Index fund:

{kind=link}

This shows the advantage that leveraged bond funds have had over unleveraged funds over the past decade, in which money was exceptionally cheap and yields were very low. It also seems likely that this fund will be the preferred investment for most investors since ultimately total return is far more important than just the price performance for anyone who is seeking to grow their wealth.

On its website, PIMCO states that this fund can invest in both traditional fixed-coupon bonds and floating-rate loan securities:

The fund has the flexibility to allocate assets in varying proportions among floating- and fixed-rate debt instruments, as well as among investment-grade and non-investment-grade securities. It may focus more heavily or exclusively on an asset class at any time, based on assessments of relative values, market conditions, and other factors.

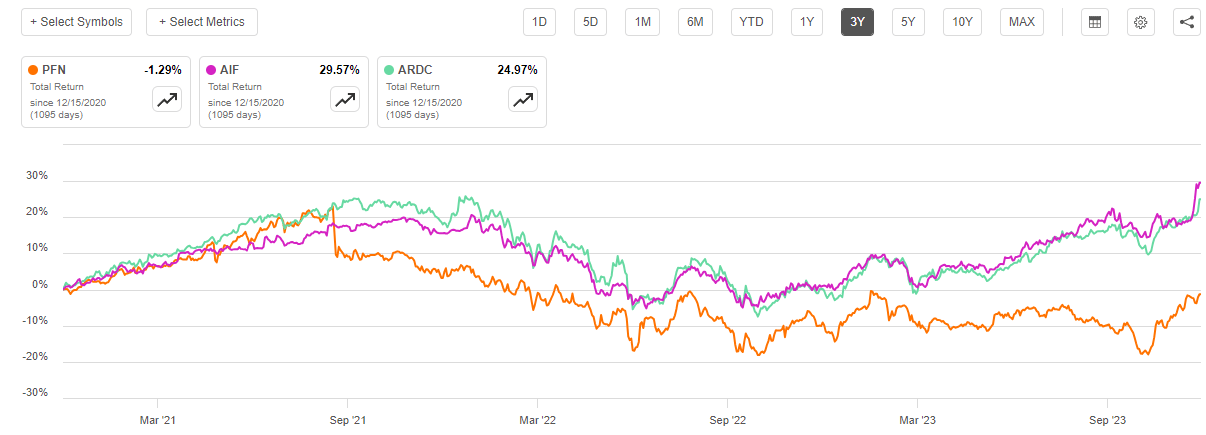

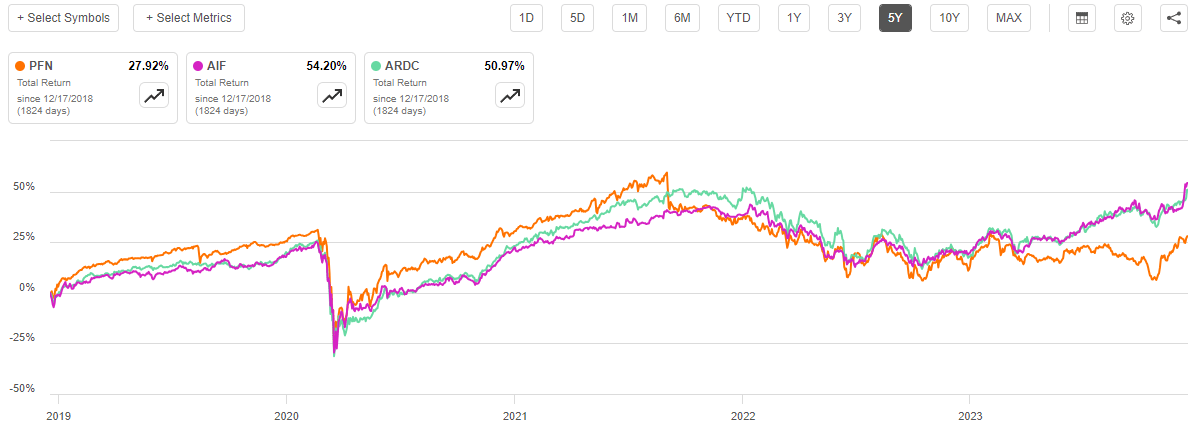

It does not appear that this fund is employing this flexibility to allocate its assets among floating-rate debt and fixed-rate debt instruments to the degree that it should. If it was, then its performance should have been much better than it actually delivered over the past three years. For example, take a look at how this fund’s total return compared to the Apollo Tactical Income Fund ( AIF ) and the Ares Dynamic Credit Allocation Fund ( ARDC ) over the past three years:

{kind=link}

As we can see, both the Ares and the Apollo funds delivered strong positive returns over the period, but investors in the PIMCO Income Strategy Fund II fund lost money even when we consider the distributions that the fund paid out over the period. We see the same thing over the past five years, although in this case investors in the PIMCO fund actually did make money:

{kind=link}

As I have noted in previous articles on both the Ares and the Apollo funds, they actually do take advantage of their ability to invest in both fixed-rate and floating-rate debt securities. This is the reason why they were able to deliver such strong performance over the periods, as their management was able to switch from fixed-rate debt to floating-rate debt once interest rates started rising and hurting the prices of fixed-rate debt securities. The management of the PIMCO Income Strategy Fund does not appear to be employing this flexibility with nearly the same skill as the management of either of the other two funds. In addition, the PIMCO Income Strategy Fund II does not state the degree to which the fund is invested in floating-rate as opposed to fixed-rate securities so we cannot be certain of the degree to which investors in this fund are exposed to interest-rate risk. As such, investors should not rely on this fund as an interest-rate neutral income fund as they can with both of the other funds.

A look at this fund’s portfolio does reveal that it is fairly well positioned for a decline in interest rates, though. Here is the fund’s sector allocation:

PIMCO

The overwhelming majority of these assets are going to be traditional fixed-rate bonds. The fund’s annual report does suggest that it had a 34.8% allocation to senior loans earlier in the year, but that is still a minority position, and it appears that the fund may have disposed of those securities as they are not shown among the fund’s current allocation as of November 30, 2023.

With that said, we do generally want to be holding fixed-rate debt securities during periods of falling interest rates. This is because fixed-rate debt prices move inversely to interest rates, so the value of these securities should increase as interest rates decline. The market has been expecting that the Federal Reserve would cut interest rates in 2024, and indeed remarks made by Chairman Powell following Wednesday’s meeting of the Federal Open Market Committee strongly suggested that this is a very possibility. However, some Federal Reserve officials have disputed this. Earlier today, John Williams, President of the New York Federal Reserve, made the following statement on CNBC :

We are not talking about rate cuts right now. We’re very focused on the question in front of us, which as chair Powell said… is, have we gotten monetary policy to sufficiently restrictive stance in order to ensure the inflation comes back down to 2%? That’s the question in front of us.

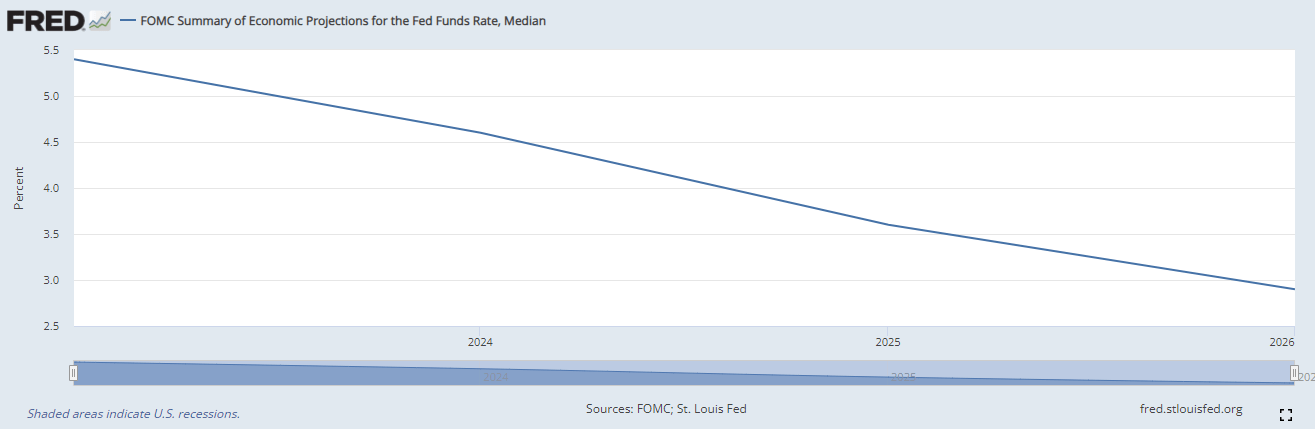

As such, there is no guarantee that the Federal Reserve will be cutting interest rates next year, and the market’s expectation of such could be premature. The market is expecting between five and six 25-basis point cuts next year, with the first one coming in March. The Federal Reserve’s median projection is three 25-basis points cuts:

{kind=link}

That puts a terminal rate of 4.625% at the end of 2024, not the 4% that the market is expecting. If the Federal Reserve delivers on its own projections, this strongly suggests that fixed-rate bonds are overpriced right now. As we have already seen, shares of the PIMCO Income Strategy Fund II have been driven up over the past two months due to the market’s expectations surrounding the 2024 interest rate cuts. As such, buying the shares today could be somewhat risky as the shares could give back some of their recent gains on any signs that the market is wrong about the Federal Reserve’s 2024 policy, as seems likely.

Leverage

As is the case with most closed-end funds, the PIMCO Income Strategy Fund II employs leverage as a method of boosting the effective return and yield that it earns from its net assets. I explained how this works in my previous article:

In short, the fund borrows money and then uses that borrowed money to purchase bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. With that said though, the beneficial effects of leverage are nowhere near as strong today with rates at 6% as they were early last year when rates were at 0% so the fund will not be able to boost its yield as much today as it used to be able to do.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since this would expose us to too much risk. I generally like a fund’s leverage to be under a third as a percentage of its assets for this reason.

As of the time of writing, the PIMCO Income Strategy Fund II has leveraged assets comprising 28.00% of its portfolio. This is a very reasonable level of leverage that is quite a bit less than the 29.36% leverage that the fund had the last time that we discussed it. This makes sense, as the fund’s net asset value is up 6.52% since the last time that we discussed it:

{kind=link}

As such, the fund’s leverage as a percentage of the portfolio would have gone down since the portfolio itself has gotten larger. The fund does not appear to be increasing its leverage, which is also a good sign considering the possible risks that the Federal Reserve will not be as loose as the market expects and cause the fund’s assets to give up some of their gains over the next few months.

Overall, it appears that this fund is striking a pretty good balance between risk and reward with respect to its leverage. We should not need to worry too much about its leverage right now.

Distribution Analysis

As mentioned earlier in this article, the primary investment objective of the PIMCO Income Strategy Fund II is to provide its investors with a very high level of current income. In order to accomplish this objective, the fund invests in a variety of bonds that primarily deliver their returns in the form of direct payments to their investors. The fund collects all of the payments that it receives from the bonds that it purchases with the shareholders’ money, and then it borrows more money to allow it to control more securities than it could own with just its equity capital. That has the effect of boosting the income generated by the portfolio and boosting the overall yield. The fund adds any money that it manages to obtain by trading bonds and exploiting price fluctuations to its overall pool of capital and then pays out the investment profits to the shareholders, net of its own expenses. It can be expected that this will give the fund a very high yield, especially considering where bond yields are right now.

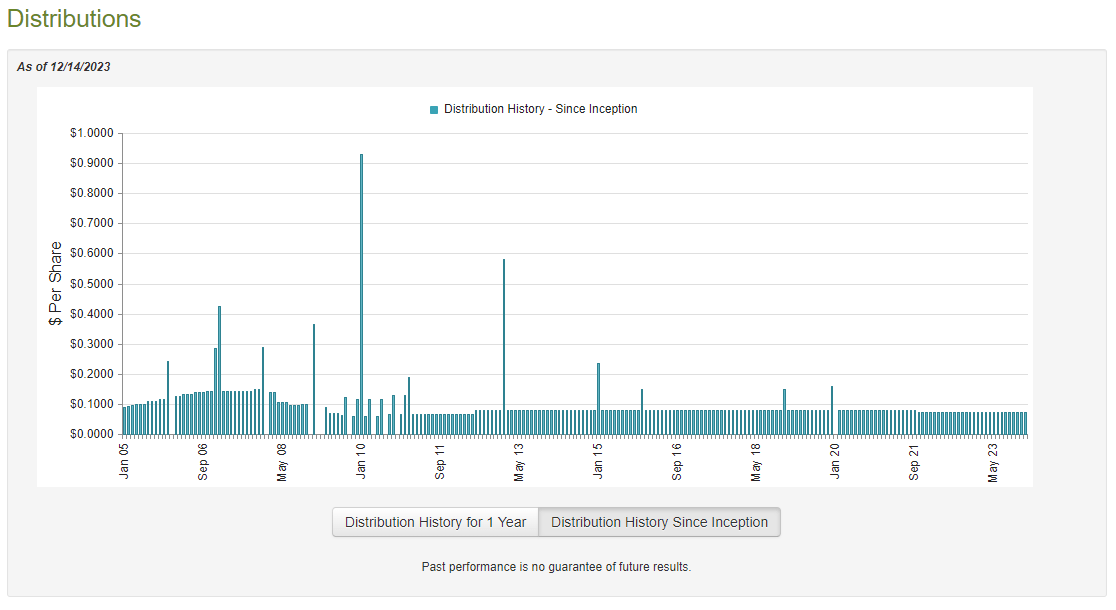

This is certainly the case, as the PIMCO Income Strategy Fund II currently pays a monthly distribution of $0.0718 per share ($0.8616 per share annually), which gives it an attractive 12.15% yield at the current share price. As shown earlier, this is a fairly attractive yield for a fixed-income fund today that compares fairly well with PIMCO’s other funds. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years, but it generally does a better job in this area than most fixed-income funds:

{kind=link}

The majority of fixed-income funds have had to change their distributions quite a bit over the past ten years or so, but this one has been relatively stable, although it did cut the payout back in 2021. For the most part though, this distribution history will probably prove to be reasonably appealing for those investors who are seeking a safe and secure source of income to use to pay their bills and finance their lifestyles. This could explain the fund’s general popularity, although most funds from PIMCO tend to be fairly popular among investors. As is always the case though, we should take a closer look at the fund’s finances, as it seems rather strange that this fund could manage a feat that few other fixed-income funds have managed to accomplish over the past decade or so.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the most recent financial report available for the PIMCO Income Strategy Fund II corresponds to the full-year period that ended on June 30, 2023. This document was linked to earlier in this article. Unfortunately, this report will not include any information about the fund’s performance over the past five months or so, but it should still give us a good idea of how well it managed to take advantage of the generally favorable environment for bonds during the first half of this year.

During the full-year period, the PIMCO Income Strategy Fund received $76.457 million in interest along with $603,000 in dividends from the assets in its portfolio. When we combine this with a small amount of income that was received from other sources, the fund had a total investment income of $77.126 million over the full-year period. It paid its expenses out of this amount, which left it with $62.080 million available to shareholders. This was not enough to cover the $70.331 million that the fund paid out in distributions during the period. At first glance, this is likely to be quite concerning since we typically prefer a fixed-income fund to fully cover its distribution out of net investment income. This one obviously failed to accomplish that.

However, there are some other ways through which the fund can obtain the money that it needs to cover the distribution. For example, it can sell bonds when their prices go up and pocket capital gains that could be distributed to the shareholders. Unfortunately, this fund failed to accomplish this task during the period. It reported net realized losses of $19.897 million and had another $10.669 million net unrealized losses during the full-year period. Overall, the fund’s net assets declined by $4.675 million during the period after accounting for all inflows and outflows.

The decline in net assets would have been much worse than the reported figure, but the fund issued $33.369 million worth of shares to new investors. That money was all lost and then some during the period. Clearly, the fund failed to cover its distribution during the full-year period, which should be quite concerning for those investors who are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles.

Fortunately, it does appear that things have improved somewhat since the close of the period. As we can see here, the fund’s net asset value per share has increased by 2.63% since July 1, 2023.

{kind=link}

This strongly suggests that the fund has managed to cover all of the distributions that it has paid out in the current fiscal year. However, it remains to be seen if it can manage to continue to perform at this level going forward.

Valuation

As of December 14, 2023 (the most recent date for which data is currently available), the PIMCO Income Strategy Fund II has a net asset value of $7.03 per share but the fund’s shares currently trade for $7.18 per share each. This gives the fund’s shares a 0.9% premium on net asset value at the current price. This is worse than the 0.15% premium that the shares have had on average over the past month, but it is still not a large premium for a PIMCO fund. However, it is difficult to justify paying a premium for this fund considering the risks that the Federal Reserve will disappoint the market over the next year.

Conclusion

In conclusion, the PIMCO Income Strategy Fund II appears to be a very reasonable way for investors to take advantage of the expected decline in interest rates over the next year. However, it appears that the market may be far too optimistic about the magnitude of these cuts. The central bank is not guiding to anywhere near the number of cuts that the market is pricing into bonds right now and that could result in the fund giving up some of its recent gains at some point. When we combine this with the fact that the fund’s shares are currently trading at a premium, it could be risky to purchase it right now.

For further details see:

PFN: This Popular Bond Fund May Be Riskier Than Believed