AGG - PFN: Underperforming Some Of PIMCO's Other CEFs And Trading At A Premium

2023-04-13 17:23:24 ET

Summary

- Investors are desperately in need of income due to the rapidly rising cost of living.

- PIMCO Income Strategy Fund II invests in a portfolio of junk debt and other income-producing securities to deliver a high level of current income.

- The PFN closed-end fund has underperformed some of PIMCO's other offerings like PHK but it is still one of the best bond funds around.

- The 12.12% distribution yield is probably sustainable, which is surprising because yields like this are usually a sign of an impending cut.

- The PFN CEF is trading at a premium to NAV, which is the only real complaint against it.

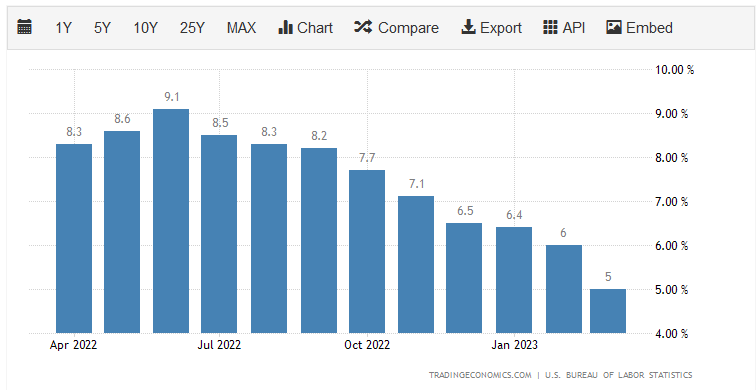

There can be little doubt that one of the biggest problems facing average Americans today is the rapidly rising cost of living. This can be easily seen by looking at the consumer price index, which is the most commonly used measure of inflation. Over the past eighteen months, this index has been at some of the highest levels that we have seen in forty years. In fact, in eleven out of the past twelve months, the consumer price index increased by at least 6% year-over-year:

{kind=link}

This has had a terrible effect on the finances of the average American household. This is especially true of those of lesser means since some of the things that have exhibited the greatest price increases have been necessities such as food and energy. We have seen an increase in the number of Americans taking on second jobs or entering into the gig economy just to make ends meet, while others have been forced to reduce their savings or go into debt just to maintain their standard of living. In short, people are desperate for additional sources of income just to maintain their lifestyles.

Fortunately, as investors, we have other options available to us to obtain an income boost. After all, we can put our money to work for us in order to earn an income. One of the best ways to do this is to purchase shares of a closed-end fund ("CEF") that specializes in income. These funds are unfortunately not very well followed in the financial media and are unfamiliar to many investment professionals, so it can be difficult to obtain information about them. This is a sorry state of affairs, as these funds offer some advantages over the more familiar open-end funds and exchange-traded funds. For example, these funds can employ certain strategies that have the effect of boosting their yields beyond that of the underlying assets or, indeed, pretty much anything else in the market.

In this article, we will discuss the PIMCO Income Strategy Fund II ( PFN ), which is one closed-end fund that can be used for the purposes of earning an income. This fund yields 12.12% as of the time of writing, so it certainly does that job fairly well. However, pretty much anytime something is given a yield that is this high, it is usually a sign that the market expects that the fund will be forced to cut its distribution too. We will need to pay special attention to this as part of our analysis. I have discussed this fund before, but a few months have passed since that time, so naturally, a few things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund's finances. Therefore, let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the PIMCO Income Strategy Fund II has the stated objective of providing its investors with a high level of current income. This is not particularly surprising coming from PIMCO, which has built a reputation as a high-quality bond fund management company. This fund is certainly no exception to PIMCO's focus on bond funds, as is clearly evident by the fact that the fund's portfolio consists almost entirely of bonds, with only a small allocation to common stocks or preferred assets:

CEF Connect

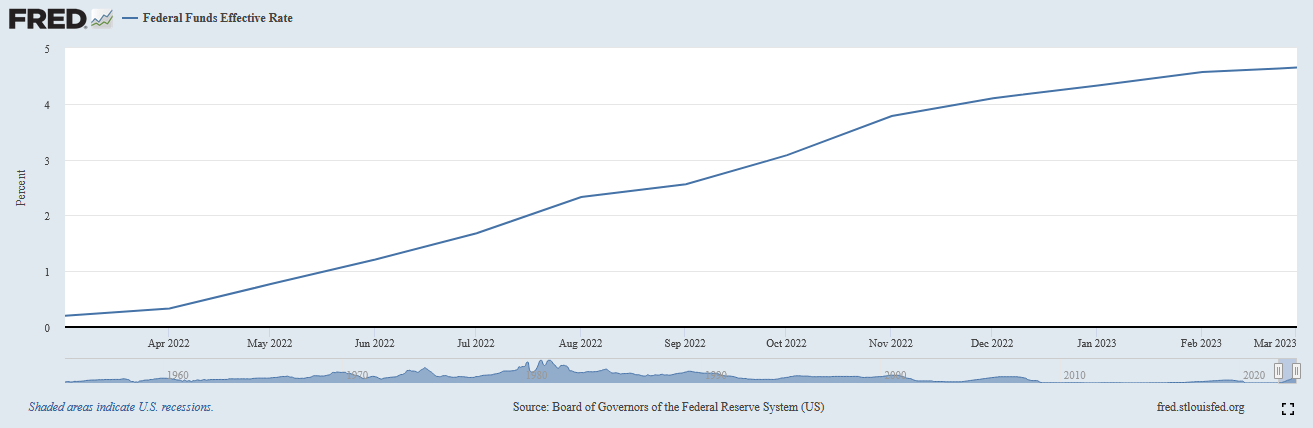

The past year or so has been very challenging for bond funds due to their defining characteristics. In particular, bond prices are especially sensitive to interest rates. This is because most bonds pay out a fixed regular payment to their investors that is based on the market interest rate at the time of issuance. These payments do not typically change with the growth and prosperity of the issuing company, nor do they change when interest rates do. As a result, bond prices decline when interest rates decrease and vice versa. After all, why would anyone buy an existing bond when a brand-new bond with identical characteristics has a higher yield during a rising interest rate regime? As everyone reading this is well aware, the Federal Reserve has been aggressively raising interest rates over the past year. We can quickly see this by looking at the federal funds rate:

{kind=link}

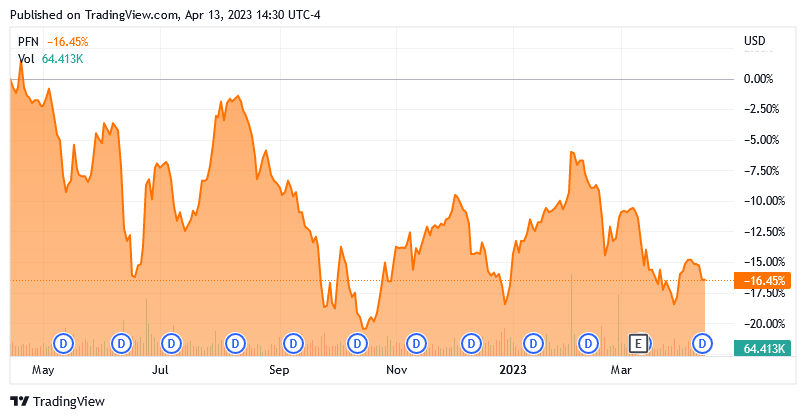

As clearly shown, back in March of 2022, the effective federal funds rate was at 0.20% but today it sits at 4.65%. The current rate is the highest rate that we have seen since 2007 so it is a safe bet that nearly all of the bonds in the fund's portfolio have a stated yield of less than a brand-new bond today. As a result, very few of the bonds in the fund's portfolio will be trading at anything near their face value. Furthermore, it means that the value of the bonds held by the fund will have declined significantly in price over the past year. We can certainly see that by looking at this fund's share price over the trailing twelve-month period:

{kind=link}

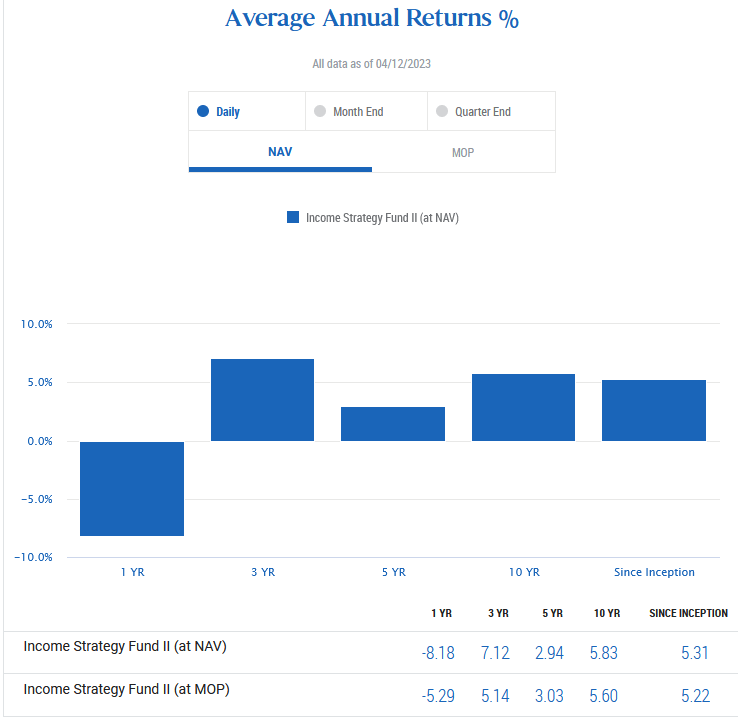

As we can see, the PIMCO Income Strategy Fund II has fallen by 16.45% over the past twelve months. This is much more than the 3.88% decline of the Bloomberg US Aggregate Bond Index ( AGG ) over the same period. However, the closed-end fund has a much higher yield than the index, which helps to even out the total return between the fund and the aggregate bond index. The PIMCO fund did still underperform the index though, which its own website makes clearly apparent:

{kind=link}

The most important thing to look at is the fund's performance at net asset value or NAV. This is the actual total return of the portfolio, not the fund's share price. After all, as I have pointed out in numerous previous articles, a closed-end fund's share price can sometimes exhibit very different performance characteristics than the fund's actual portfolio. In this case, we see that the portfolio itself delivered an -8.18% total return over the past twelve months. That is quite a bit worse than the aggregate bond index and quite a bit worse than funds like the PIMCO High Income Fund ( PHK ), which I discussed in an article that was published earlier today. One reason for this is likely the fact that the PIMCO Income Strategy Fund II employs leverage as part of its investment strategy. We will discuss this later in this article. A second reason might have to do with the fund's strategy of trading bonds extensively.

As is the case with many PIMCO bond funds, the PIMCO Income Strategy Fund II does not simply buy bonds and then hold them to maturity. If it did this, as the index funds do, it could eliminate most to all of its interest rate risk. This is because bonds always pay their face value at maturity, so if you buy the bond with a positive yield-to-maturity, you are guaranteed not to lose money as long as the issuing company does not default on the bonds. However, this fund tries to trade the bonds in order to pocket capital gains. This is evident in its 45.00% annual turnover, which is higher than the average for a fixed-income fund. One reason that this is important is that trading bonds or other assets costs money, which is billed directly to the fund's shareholders. This creates a drag on the portfolio's performance, which makes management's job more difficult. This is because the fund's managers have to generate sufficient excess returns to cover the fund's expenses and still have enough left over to give shareholders an acceptable return. There are very few funds that manage to accomplish this task on a consistent basis, which is one reason why actively-managed funds tend to outperform index funds tracking the same asset class.

In the case of this fund, the trading activity might also result in the fund realizing losses that it could have avoided had it held the bond for a longer period of time. Of course, the goal is whatever the fund's management purchases with the money from the trade will appreciate enough to offset the loss.

As is the case with many fixed-income closed-end funds, the PIMCO Income Strategy Fund II tends to include fairly high allocations to speculative-grade securities, which are colloquially called "junk bonds." We can see this quite clearly by looking at the credit ratings of the bonds in the fund's portfolio. Here is a high-level summary:

CEF Connect

A junk bond is anything that has a credit rating of BB or lower. As we can see, that is 71.14% of the fund's portfolio, assuming that the unrated securities in the portfolio are junk bonds. It makes sense that most of them probably are as any company that has strong enough finances to get an investment-grade credit rating will probably pay the money to a rating agency to get that rating as it allows the company to save a lot of money in interest over time. The fact that such a high percentage of the bonds in this portfolio are junk bonds is something that may be concerning to many investors. After all, we have all heard about how these bonds tend to have a very high risk of default. However, as we can see above, 35.09% of the bonds in the portfolio are rated either BB or B by the major rating agencies. According to the official bond rating scale , companies that have these ratings have the financial strength to carry their debt and should be able to withstand a short-term economic shock. Thus, we should probably not worry too much here. The fact that this fund has 412 holdings adds to our comfort level here as that should ensure that any individual position only accounts for a very small percentage of the fund's overall portfolio. As a single default will probably not have a noticeable impact, the biggest risk here is interest rate risk.

Leverage

As stated earlier in this article, the PIMCO Income Strategy Fund II employs leverage as a way to improve its returns and provide investors with a higher yield than any of the underlying bonds possess. In short, the fund borrows money and then uses the proceeds to purchase bonds and other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, this strategy works pretty well to boost the yield of the overall portfolio. As this fund is capable of borrowing money at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This therefore could be one reason why the fund fell more than the index over the past year. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for that reason. Fortunately, this fund is fulfilling this requirement. As of the time of writing, the PIMCO Income Strategy Fund II has leveraged assets comprising 28.82% of its portfolio. Thus, it appears that it is currently striking a reasonable balance between risk and reward.

Distribution Analysis

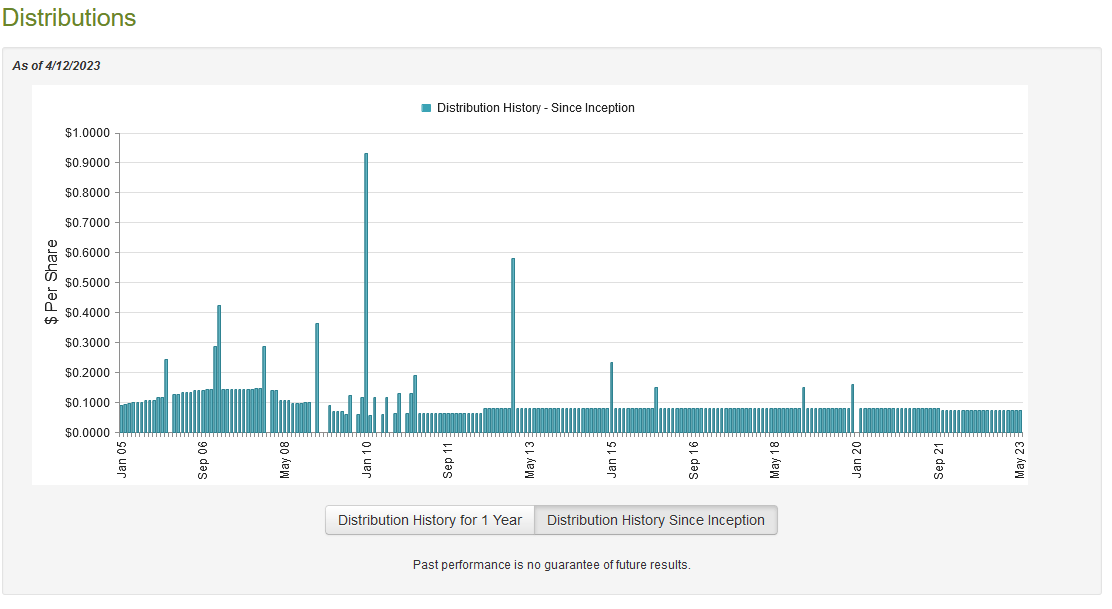

As mentioned earlier in this article, the primary objective of the PIMCO Income Strategy Fund II is to provide its investors with a high level of current income. In order to achieve this, it purchases junk bonds and other high-yielding assets, then applies a layer of leverage in order to boost the effective yield further. As such, we can assume that the fund itself will have a fairly high yield. This is certainly the case as the fund currently pays a monthly distribution of $0.0718 per share ($0.8616 per share annually), which gives the fund a 12.12% yield at the current price. The fund has generally been consistent with its distribution over the years, although it did cut its payout back in 2021:

{kind=link}

For the most part, this distribution history will probably appeal to most investors that are looking for a safe and secure source of income to use to pay their bills or finance their lifestyles. It is obviously not perfect due to the distribution cut back in 2021, but it is as good or better than most fixed-income funds have managed to achieve. Naturally, though, we want to ensure that the fund can continue to pay the current distribution going forward. This is especially important right now since most funds that end up trading with double-digit yields are presumed to be at high risk of making a distribution cut in the near term.

Fortunately, we do have a very recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on December 31, 2022. This is a much more recent report than we had available to us the last time that we analyzed this fund, which is nice because it should be able to provide us with better insight into how well this fund performed in the volatile bond market that dominated 2022. During the six-month period, PIMCO Income Strategy Fund II received $37.304 million in interest net of foreign withholding taxes along with $307,000 in dividends from the investments in its portfolio. This gives the fund a total investment income of $37.611 million over the six-month period. The fund paid its expenses out of this amount, which left it with $30.358 million available for shareholders. This was unfortunately not enough to cover the $34.497 million that the fund paid out in distributions, although it did get pretty close. Nonetheless, this may be concerning at first glance since the fund did not have sufficient net investment income to cover its distributions.

However, the fund does have other methods through which it can obtain the money that is needed to cover the distributions. One of these methods is capital gains. As might be expected from the volatile bond market over the course of 2022, the fund generally failed at this, but it did deliver a reasonable performance given the market conditions. During the six-month period, the fund had net realized gains of $14.371 million but this was offset by $30.746 million in unrealized losses. However, the fund's net investment income combined with its net realized gains were enough to cover the distributions and still leave the fund with money left over. When we consider that the bond market has been reasonably strong so far in 2023, the fund can probably afford to keep its distribution at the current level. We should not really have to worry too much here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the PIMCO Income Strategy Fund II, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of April 12, 2023 (the most recent date for which data is available as of the time of writing), the PIMCO Income Strategy Fund II had a net asset value of $6.84 per share but the shares currently trade for $7.13 each. This gives the shares a 4.24% premium to the net asset value at the current price. That is a bit above the 3.61% average premium that the shares have had over the past month, so unfortunately the price does appear to be a bit higher than we really want. It is incredibly rare for any PIMCO fund to trade at a discount to the net asset value though, so we probably cannot count on getting a better price.

Conclusion

In conclusion, the PIMCO Income Strategy II fund looks like a very good bond fund, just like most of the offerings from this fund house. Unfortunately, the performance has not been quite as good as a few of PIMCO's other funds over the past year, but it has still been much better than many other bond funds have managed. The fund does appear to be able to sustain its remarkably high 12.12% yield going forward, and it is very well diversified to provide protection against anything except for interest rate risk. The biggest problem here is that the fund is trading at a premium, which is a bit expensive for any fund. It might be worth paying the premium for PIMCO Income Strategy Fund II, though, as the manager is one of the best bond managers in the business.

For further details see:

PFN: Underperforming Some Of PIMCO's Other CEFs And Trading At A Premium