PHD - PHD: Another Amortizing Fund To Avoid

2023-08-02 11:47:58 ET

Summary

- The Pioneer Floating Rate Fund aims to deliver high current income from floating rate loans.

- The PHD fund has generated modest long-term returns of 6.0%/3.1%/3.8%/4.6% over 3/5/10/15-year horizons, but its distribution yield may be too generous and unsustainable.

- Investors should try to avoid amortizing 'return of principal' funds like PHD as they lead to long-term principal losses.

A little while ago, I wrote an article detailing how I go about analyzing investment funds to see if they are amortizing 'return of principal' funds that should be avoided. Let us use the template I laid out in my prior article to analyze the Pioneer Floating Rate Fund, Inc. ( PHD ).

1) Fund Overview

First, we should read an investment fund's marketing literature, to get a sense of the fund's market niche and audience. The PHD fund is offered by Amundi (AMDUF). Unlike other largest asset managers that list out common fund details, Amundi chooses to list only the fund's factsheet, annual report, and semi-annual report in a minimalist website.

From the PHD fund's factsheet, we learn that the fund's goal is to deliver high current income from floating rate loans. Floating rate loans, or otherwise known as leveraged loans , are senior-secured loans extended to companies that are usually rated non-investment grade. They are often quoted as a spread to a floating rate benchmark like the Secured Overnight Financing Rate ("SOFR").

Since these loans are floating rate by nature, the loans have very little duration risk. However, they still have credit risk.

The PHD fund employs leverage to enhance returns. As of June 30, 2023, the PHD fund has $59 million in borrowings against $182 million in gross assets for 32% effective leverage (Figure 1).

{kind=link}

The PHD fund charges a 2.45% net expense ratio, which appears expensive but is roughly similar to other closed-end funds.

2) Portfolio Holdings

Digging into the PHD fund's holdings, we can see that PHD's portfolio currently holds 287 securities with a weighted average term of 4.3 years and 0.2 years duration (Figure 2).

{kind=link}

The fund's low duration is expected as it holds floating rate loans mentioned above.

The top sector allocations for the PHD fund are Consumer (20.1%), Capital Goods (12.6%), Health Care (10.4%), and Technology (10.4%).

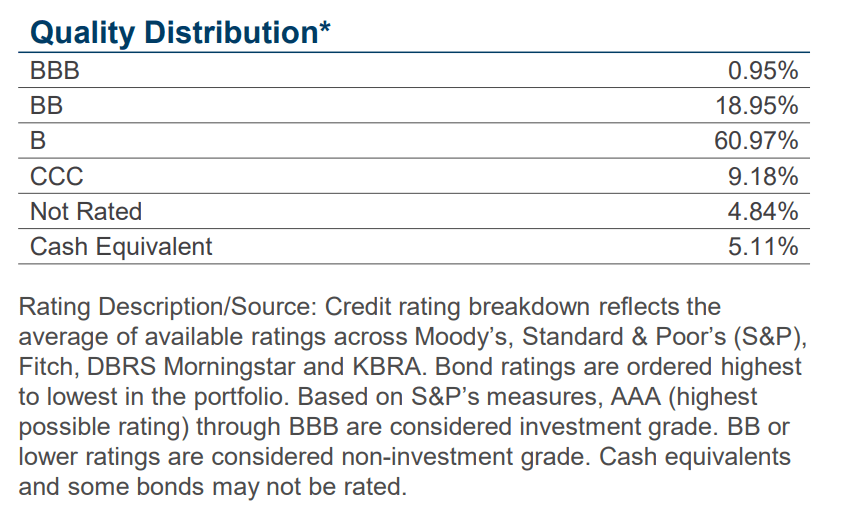

The PHD fund's loans are predominantly non-investment grade, with 19.0% of the portfolio BB-rated, 61.0% of the portfolio B-rated, and 9.2% of the portfolio CCC-rated. The fund also has a 4.8% allocation to unrated securities (Figure 3).

{kind=link}

3) Portfolio Returns

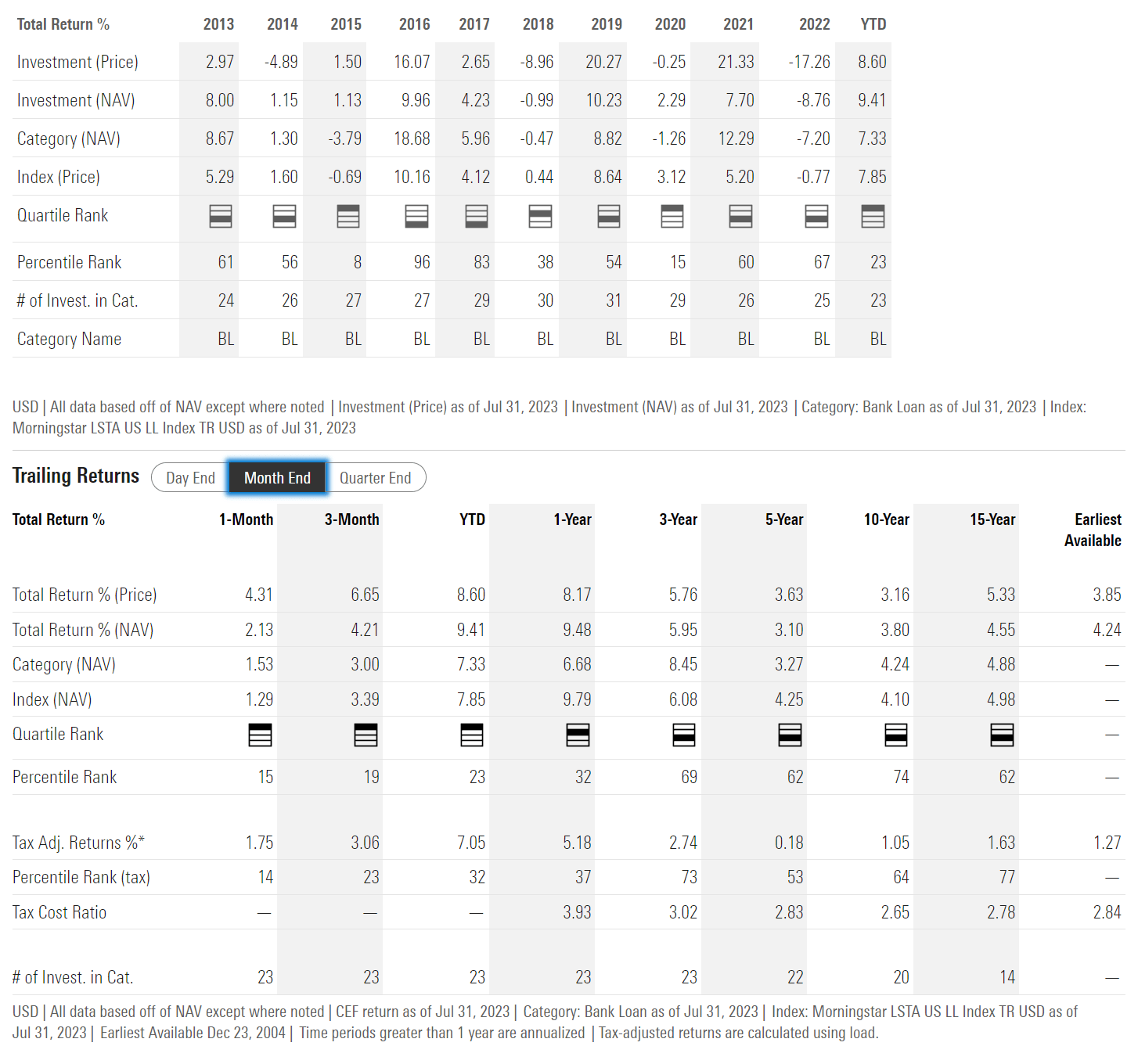

Figure 4 shows the PHD fund's historical returns. The PHD fund has generated modest long-term returns of 6.0%/3.1%/3.8%/4.6% over 3/5/10/15Yr horizons to July 31, 2023.

{kind=link}

PHD's returns are about par for the asset class. Recall, the PHD fund invests in floating rate term loans, so investors can think of PHD's historical returns as that of non-investment grade credit spreads. Over the long-run, high-yield credit spreads have averaged 5.4%, with periods of calm punctuated with occasional panics when credit spreads spike higher (Figure 5).

Figure 5 - High yield credit spreads average 5.4% over a cycle (St. Louis Fed)

Therefore, over a cycle, investors should expect to generate average annual returns of ~5% by investing in the PHD fund, adjusted higher for the fund's effective leverage, but subtracting the fund's expenses.

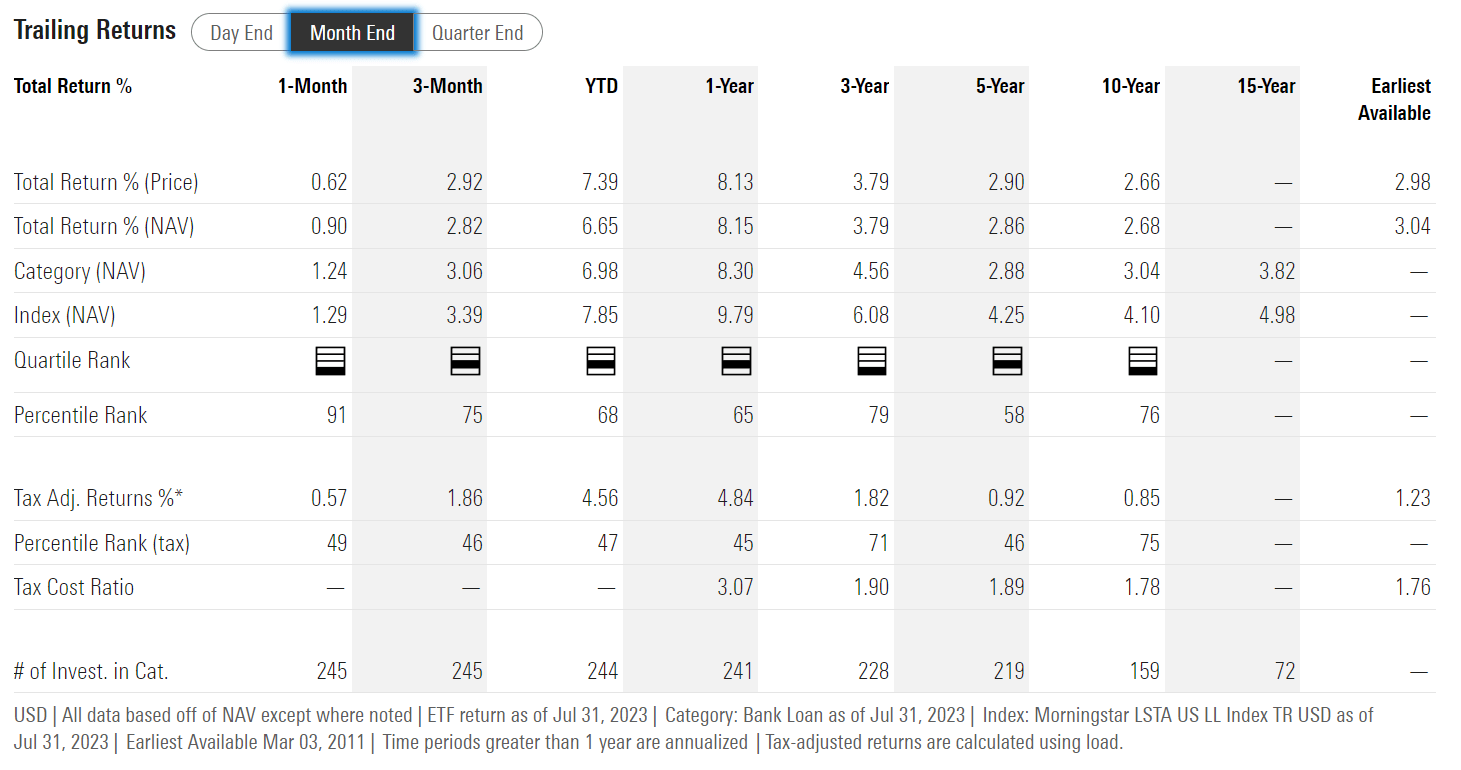

We can also compare the PHD fund against passive ETFs that invest in floating rate loans, like the Invesco Senior Loan ETF ( BKLN ). The BKLN ETF has generated 3.8%/2.9%/2.7% returns over a 3/5/10Yr horizon to July 31, 2023 (Figure 6). Therefore, the PHD fund has outperformed the BKLN ETF. However, investors should note that the PHD fund employs 32% effective leverage, whereas the BKLN ETF is unlevered.

{kind=link}

4) Distribution & Yield

Although the PHD fund earns modest average annual returns of 3.1% over 5 years, it pays a very generous monthly distribution, with trailing 12 month distribution of $0.99/share or 11.0% distribution yield on market price. On the PHD fund's latest NAV of $10.11, the yield is 9.8% (Figure 7).

Figure 7 - PHD pays a very generous distribution yield (Seeking Alpha)

{kind=link}

With the large gap between the fund's average annual total returns (6.0% over 3 years and 3.1% over 5 years) and its distribution yield (9.8% of NAV), I have concerns about the sustainability of the fund's distribution.

The PHD fund has all the hallmarks of being an amortizing ' return of principal ' (an economic concept that is subtly different from the accounting concept 'return of capital') that does not earn its distribution. Over the long run, 'return of principal' funds suffer NAV declines, which can lead to principal loss for investors, since market price tends to track NAV.

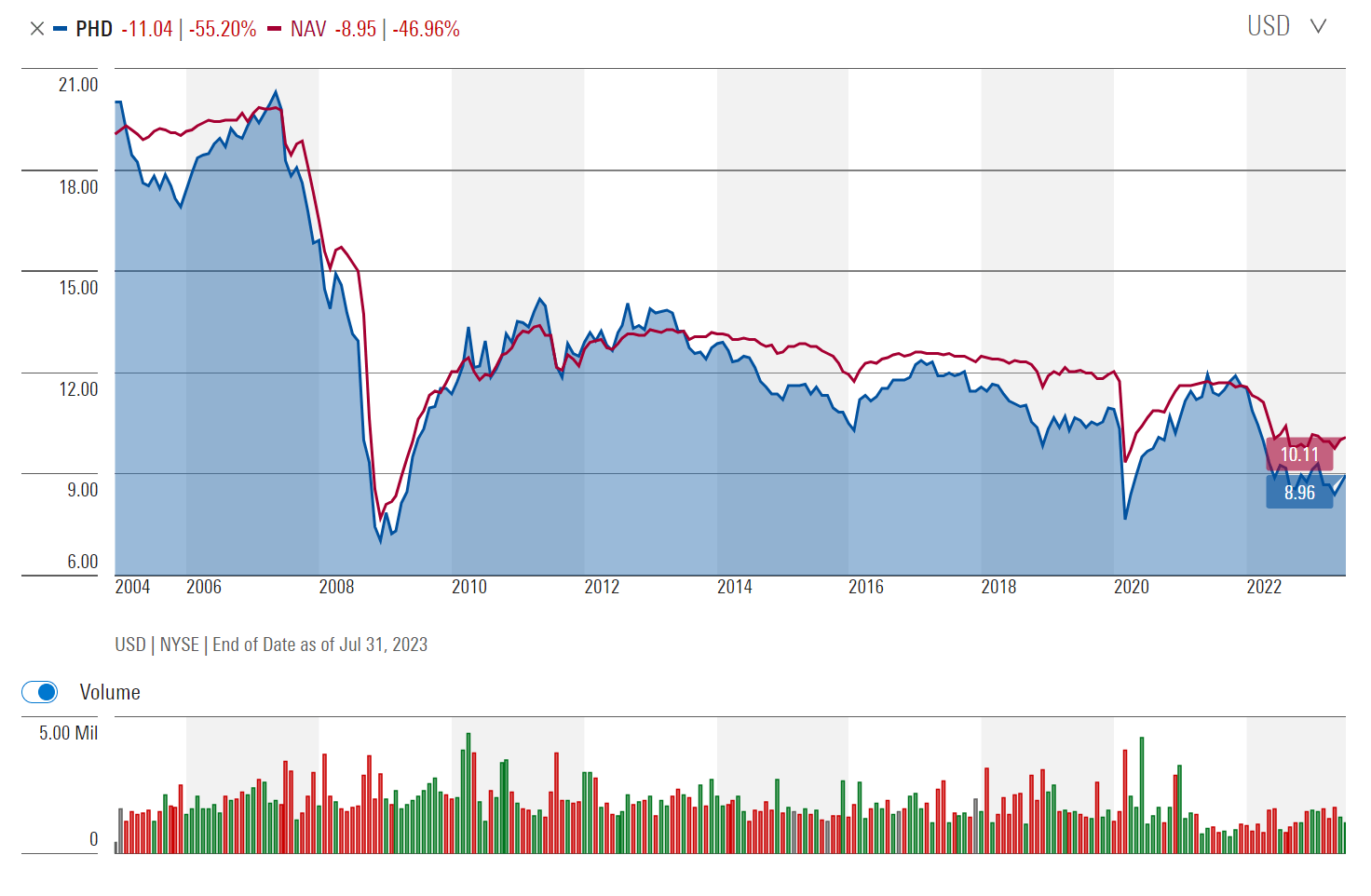

For the PHD fund, a picture is literally worth a thousand words, as we can see the fund's NAV and share price have been in a long-term decline since inception (Figure 8).

Figure 8 - PHD fund's long-term NAV decline (morningstar.com)

{kind=link}

5) Conclusion

While the PHD fund generates modest but respectable total returns of 6.0% p.a. over 3 years and 3.1% p.a. over 5 years, it is currently paying a too-generous 11.0% trailing 12 month distribution yield.

From common sense, we know that when someone spends more than they earn, they eventually go bankrupt. The same principal applies to investment funds as well. Funds that pay more than they earn eventually deplete NAV to zero. Since inception, PHD's share price and NAV have been on a perpetual decline, with both roughly halving.

This result is to be expected, since the floating rate loan asset class only earns ~5% returns over a cycle, yet the fund perennially pays more than that in distribution yield.

The only reason I can see investors consider the PHD fund is to play a short-term credit recovery trade (please see my article on the PIMCO Dynamic Income Fund ( PDI ) for more details). Otherwise, I would recommend investors avoid 'return of principal' funds like the PHD.

For further details see:

PHD: Another Amortizing Fund To Avoid