FCT - PHD: Switch From Bonds Into This Floating-Rate Loan Fund

2024-01-05 18:05:51 ET

Summary

- The Pioneer Floating Rate Fund, Inc. offers a high level of current income with a 12.20% current yield, higher than junk bond funds.

- The PHD closed-end fund has underperformed fixed-rate bond indices due to lack of price appreciation, but this may change in the coming weeks.

- The fund invests in floating-rate loans, which provide income and are less affected by changes in interest rates, making it a safer asset to hold.

- The Fed will not cut to the degree that the market expects, which almost certainly will result in this fund outperforming traditional bonds for the near future.

- The fund is fully covering its distribution with NII and trades at a discount on NAV.

The Pioneer Floating Rate Fund, Inc. ( PHD ) is a closed-end fund, or CEF, that specializes in providing its investors with a very high level of current income. Its 12.20% current yield is a testament to its success in this area, as this yield is quite a bit above that of junk bond funds and other funds that invest primarily in high-yield debt securities, although it is reasonably in line with the yields offered by some of the better senior loan closed-end funds that are available in the market:

| Fund |

| Current Yield |

| Pioneer Floating Rate Fund |

| 12.20% |

| Apollo Senior Floating Rate Fund ( AFT ) |

| 12.36% |

| Eaton Vance Floating-Rate Income Fund ( EFT ) |

| 11.26% |

| First Trust Senior Floating Rate Income Fund II ( FCT ) |

| 11.93% |

| Invesco Senior Income Trust ( VVR ) |

| 12.49% |

As just stated, these yields tend to be higher than those of ordinary junk bond funds, despite the fact that the securities are backed by many of the same companies and have similar credit ratings. The big reason for this is that none of these funds really benefited from the very strong price appreciation that we have seen in the market over the past few months.

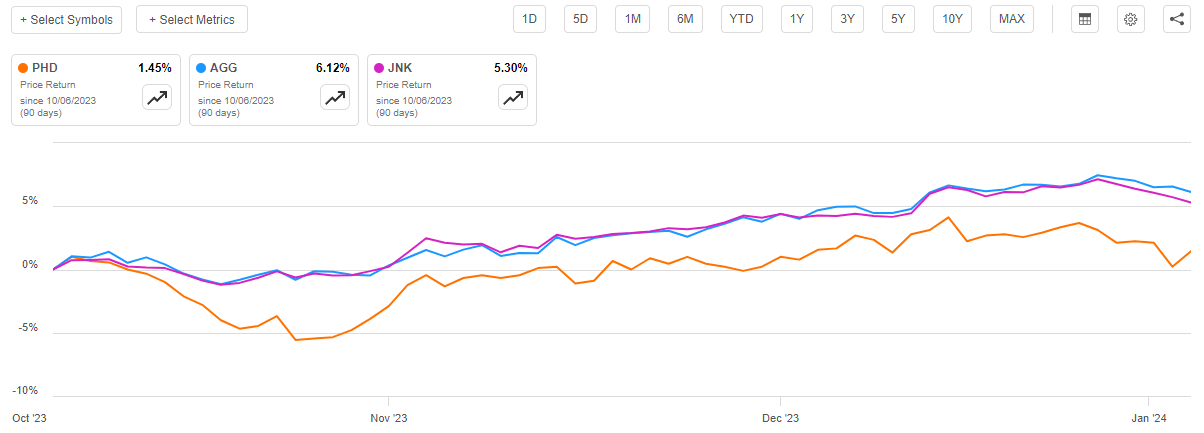

For example, the last time that I discussed the Pioneer Floating Rate Fund was on October 6, 2023. At the time that this article was published, the market was in a pessimistic mood as it believed that the Federal Reserve’s “higher for longer” convictions were going to hold true, so it was generally selling off fixed-rate bonds. However, that changed a week or two later, and investors began to aggressively bid up fixed-coupon bonds in an attempt to front-run the Federal Reserve’s anticipated pivot in 2024. The Pioneer Floating Rate Fund did not benefit from this market sentiment, which has resulted in its share price generally underperforming fixed-rate bonds since the date that my previous article was published.

As we can see here, shares of the fund are only up 1.45% since October 6, 2023, compared to a 5.30% gain in the Bloomberg High Yield Very Liquid Index ( JNK ) and a 6.12% gain in the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

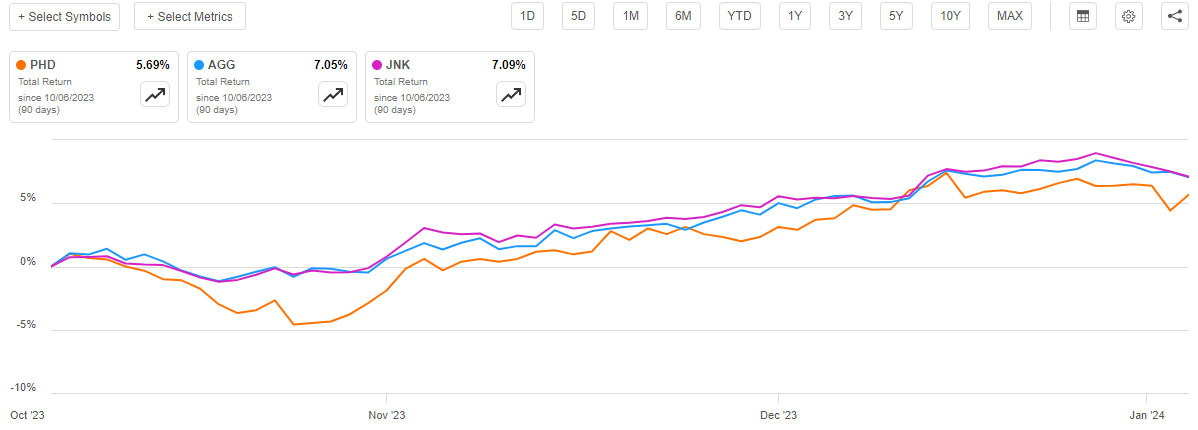

As I have pointed out numerous times in the past, though, closed-end funds such as the Pioneer Floating Rate Fund have a somewhat different business model than exchange-traded index funds. In particular, a closed-end fund will pay out all of its investment profits to the shareholders whereas an exchange-traded fund almost never realizes capital gains and instead just lets its share price fluctuate with the value of the underlying assets. This is one of the reasons why closed-end funds have substantially higher yields than their closed-end cousins. As such, we should always include the distributions that a given fund pays in any analysis of its returns because that is the total return that the fund’s shareholders actually received during a given period. When we do that, we see that the Pioneer Floating Rate Fund still underperformed both of the indices since the date that my previous article was published, although the performance difference is much less stark:

{kind=link}

As we can see, the difference between the fixed-rate indices and the Pioneer Floating Rate Fund was only about 150 basis points over the period. This is still an underperformance though and as such it may be a turn-off for many investors despite the fact that the Pioneer Floating Rate Fund does have a considerably higher yield than the indices.

There could be some reasons to believe that this fund’s fortunes will change though, and it will end up outperforming both of these indices over the coming weeks. As such, it could make sense for investors to take any profits that they may have gotten from the strength in the bond market over the past eight weeks or so and purchase this fund.

About The Fund And Outlining The Thesis

The Pioneer Floating Rate Fund is one of the few closed-end funds that does not have a dedicated website. The fund sponsor simply provides a website that lists all of its funds and provides downloadable literature. As such, we are pretty much going to rely on the fund’s quarterly fact sheet as our primary source of information about the fund itself since that seems to be the closest thing that this fund has to its own website.

According to the fund’s fact sheet, the Pioneer Floating Rate Fund has the primary objective of providing its investors with a very high level of current income. This makes a lot of sense considering that this is a debt fund that invests its assets into floating-rate loans. Floating-rate loans have some similarities with ordinary bonds in terms of how they work. In short, an investor purchases the security at face value, receives a regular coupon payment from the bond’s issuer, and then receives the face value back when the security matures. As such, these securities have no net capital gains over their lifetimes as the only net investment return is the regular coupon payment that the investors receive. These coupon payments act as a source of income for the investor, which naturally means that any fund that invests in floating-rate loans will be targeting income as its primary objective.

The difference between the securities that are contained in this fund and traditional bonds is the fact that the coupon payment that investors in floating-rate loans receive varies with interest rates. It is not a fixed amount as is the case with traditional bonds. This causes these securities to react differently to changes in interest rates. As the fact sheet explains:

When interest rates rise, the prices of fixed-income securities in the Fund will generally fall. Conversely, when interest rates fall the prices of fixed income securities in the Fund will generally rise. The floating rate feature of the Fund means that the Fund will not experience capital appreciation in a declining interest rate environment.

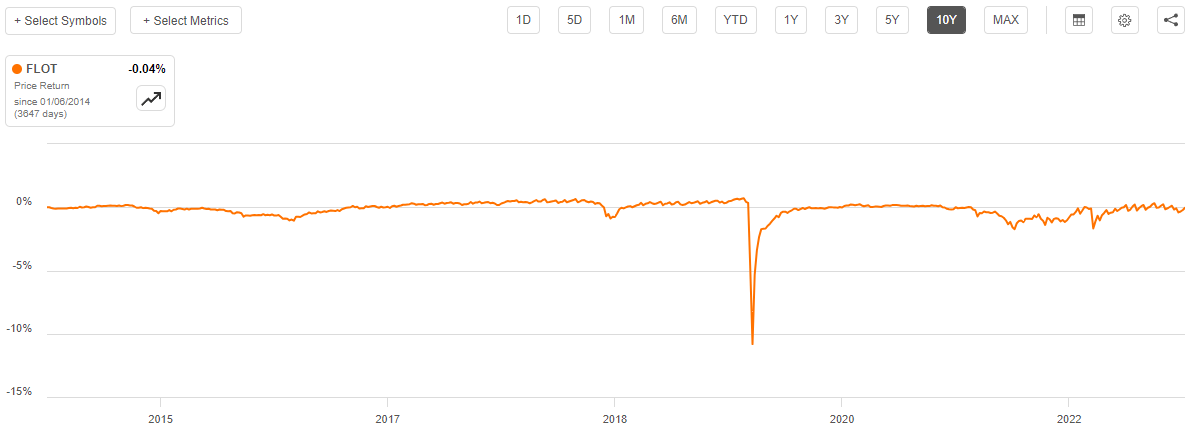

That last sentence is critical because it explains why this fund has not seen share price appreciation over the past eight weeks or so. As I pointed out in my previous article on this fund, floating-rate securities tend to be almost perfectly flat in terms of price. We can see this by looking at the price of the BBG US Floating Rate Notes 5 Yrs. And Less Index ( FLOT ). Here is the index over the past decade:

{kind=link}

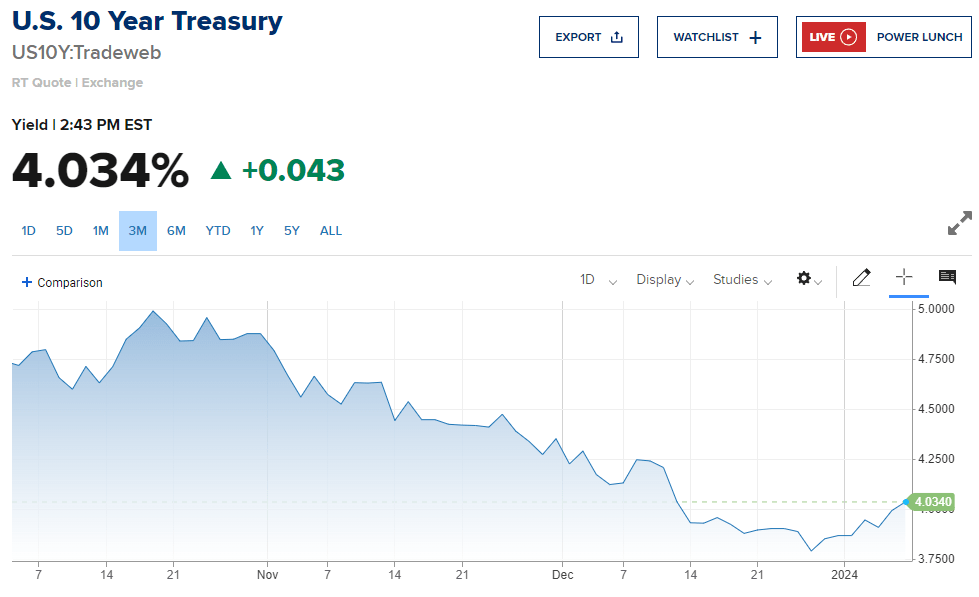

As we can clearly see, with the exception of the pandemic panic, the index has been almost totally flat. It barely reacted at all to the increasing interest rates during the 2018-2019 period or the 2022 to 2023 period. It did not fall, as ordinary bonds did when the Federal Reserve reversed its longstanding “free money” policy in 2022. It also did not benefit from the recent anticipation of interest rate cuts in 2024 that drove up the prices of traditional bonds. As we saw in the introduction, both investment-grade and junk bonds generally saw their prices rise since mid-October as long-term interest rates fell. We can see this fall in long-term interest rates by looking at the yield of the ten-year U.S. Treasury over the past three months:

{kind=link}

The yield of the ten-year U.S. Treasury fell from 4.988% on October 19, 2023, to 3.7890% on December 27, 2023. It has been rising slowly since that date but still remains well below the highs that it reached in October 2023. This is critical to our thesis right now and is the biggest reason why I believe that the Pioneer Floating Rate Fund is a buy today.

In short, the market is overly optimistic about the course of interest rates and has therefore bid bond prices too high. As floating-rate loans have not been bid up and should be relatively unaffected by changes in interest rates (at least as far as prices are concerned), they are a much safer asset to hold. Investors should therefore take the profits that they have already made in traditional fixed-rate bonds and move over to the Pioneer Floating Rate Fund in order to protect their gains and earn a higher yield in the process.

The market is currently anticipating that the Federal Reserve will cut interest rates between five and six times in 2024. We can see this by looking at the federal funds futures market, which currently predicts that the effective federal funds rate will fall by 1.384 percentage points in 2024:

{kind=link}

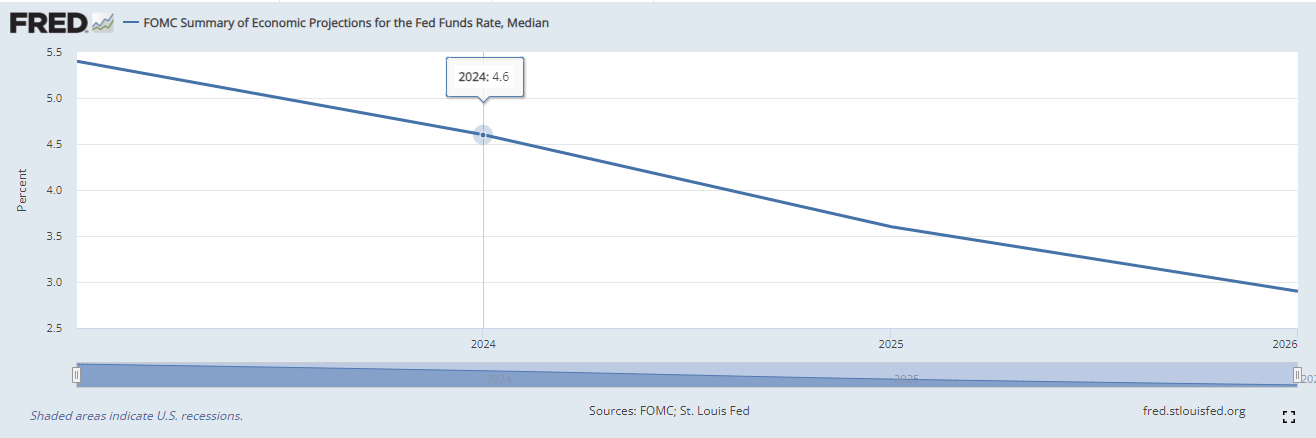

That requires five or six 25-basis point cuts this year. The Federal Open Market Committee does not believe that this is likely to happen. The median projection by the members of the committee is that the effective federal funds rate will be at 4.6% at the end of 2024:

{kind=link}

That suggests that the members of the Federal Open Market Committee believe that three 25 basis points of cuts is the most likely scenario. It is worth noting though that the dot plot, which shows what each of the committee members expects, showed that eight of them said that two or fewer cuts is appropriate and only five said more than three rate cuts. When we also consider the very hawkish tone in the minutes from the December meeting, it seems very likely that the market will be disappointed as the Federal Reserve does not cut rates to the degree that is currently priced into bonds.

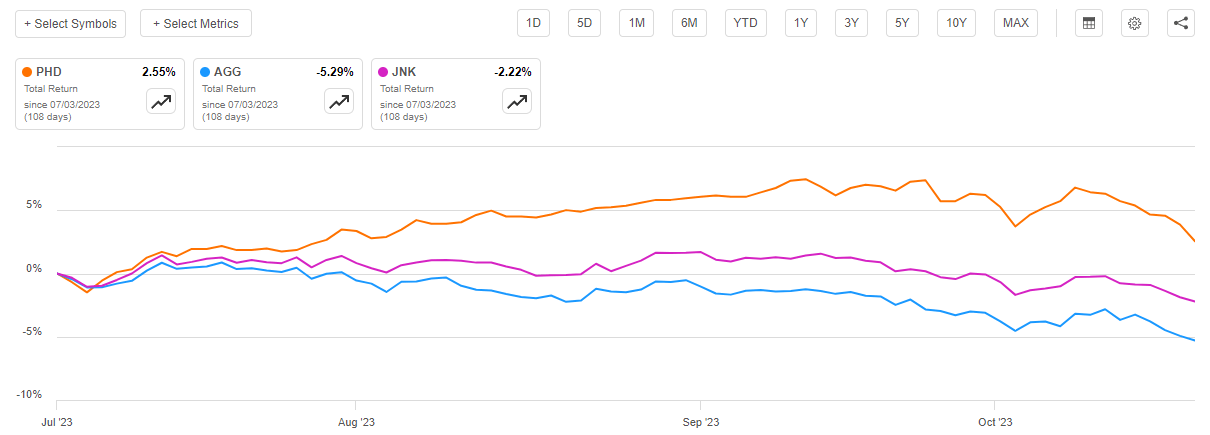

This means that the Pioneer Floating Rate Fund is positioned to outperform the indices over the next few months. This is because this fund should hold up a lot better as bond prices correct as the market begins to adjust to the reality of the current situation. What we will probably see is a situation similar to the one that occurred over the summer of 2023 when the market realized that it was wrong about a September 2023 pivot. As we can see here, the Pioneer Floating Rate Fund significantly outperformed both of the fixed-rate bond indices that we have been using as a comparison over that period:

{kind=link}

It seems likely that a similar situation will occur again, especially if the Federal Reserve does not cut interest rates at its March meeting. After all, if the Federal Open Market Committee does not cut in March, it will have to cut at pretty much every single other meeting over the course of 2024. If it does that, it could risk being accused of playing politics considering the presidential election. It could also be forced into a situation in which it cuts rates in an election year, facing ire from people who accuse it of being political, only to be forced to raise them again in 2025 as inflation takes off. When we combine all of this with the strong headline number in today’s jobs report, it seems highly unlikely that the Federal Reserve will cut interest rates in March. As such, we could even see this thesis start to play out over the next few weeks.

Potential Risks

The Pioneer Floating Rate Fund is certainly not without risks, however. One of the biggest ones comes from the fact that senior loans are typically backed by companies that may not have the strongest balance sheets. This is one of the reasons why the fund is able to sport a double-digit yield despite the fact that Treasuries are only yielding 4% to 5.3%, depending on the maturity date. We can see that the fund’s assets are mostly invested in speculative-grade securities by looking at the credit ratings that have been assigned to the assets in the portfolio. Here they are:

Fund Fact Sheet

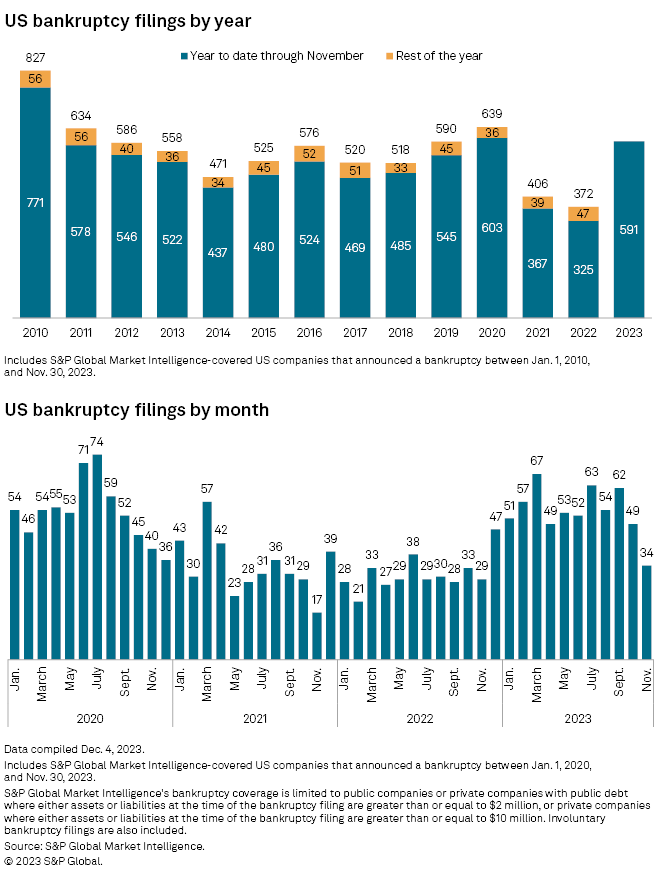

This is somewhat comparable to what we saw the last time that we looked at this fund. However, the fund has moved some of its money from the B-rated securities into BB-rated ones, so it does seem to be reducing its risk a bit. That is something that risk-averse investors should certainly appreciate. This is especially true considering that bankruptcy filings in the United States have been increasing lately. According to S&P Global Market Intelligence , there were 591 corporate bankruptcy filings in the first eleven months of 2023. That was the highest level since 2020 and the second highest level since 2010:

{kind=link}

The reason for this is very obvious. The rapid rise in interest rates since the start of 2022 has caused the interest expenses that companies have to pay to service their debt to increase. There were many zombie companies that arose over the past ten years or so that were able to generate sufficient cash to cover their debt payments but were not particularly profitable. Thus, they had no room in the budgets for a substantially higher interest payment on their debt.

The companies in which this fund is invested may be especially vulnerable to this problem. After all, the fact that the securities in this fund have floating interest rates means that the companies that have borrowed money are immediately seeing the impact of higher interest rates on their budgets. It is not a case where the company can simply keep its interest expenses the same until their bonds mature. This factor combined with the fact that these loans were issued to companies that already had a substantial amount of debt or somewhat weak excess cash flows exacerbates this problem.

Fortunately, the fund has taken some precautionary measures to protect itself from losing much money to defaults. First of all, the largest position in the fund only accounts for 1.63% of its assets. The second-largest position in the fund only accounts for 1.17% of its assets. Thus, a default by any individual company in the portfolio will not have much of an impact on the fund as a whole. Indeed, it seems unlikely that anyone would even notice it because the income from the remaining securities would very quickly erase the loss. In addition, the fact that the fund seems to be increasing the average credit rating reduces the risk of a default in the first place.

Overall, we probably do not need to worry about default losses too much here. It is still something that potential investors should keep in mind though, especially if you expect that economic conditions will deteriorate over the coming months.

Leverage

As is the case with most closed-end funds, the Pioneer Floating Rate Fund employs leverage as a method of increasing the effective yield of the assets in its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase floating-rate debt and similar income-producing securities with variable yields. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will normally be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt because that would expose us to an excessive amount of risk. I do not typically like a fund’s leverage to exceed a third as a percentage of its assets for that reason.

As of the time of writing, the Pioneer Floating Rate Fund has leveraged assets comprising 32.90% of its total assets according to the fund’s fact sheet. Curiously, CEF Connect states that the fund has a 5.25% current leverage ratio. I have a very hard time believing CEF Connect’s figure here, as a 5.25% leverage ratio would not increase the effective yield of floating-rate loans enough to give the fund a yield that is anywhere close to what it currently possesses. The 32.90% figure that is provided by the fact sheet is relatively in line with the leverage that is employed by peer funds that have similar yields, so it seems pretty accurate.

The fund should not have any real trouble carrying its current debt load. The leverage ratio is below the one-third level that we would normally like to see. In addition, floating-rate securities tend to have very limited volatility so there is not really much risk involved in the use of leverage. As such, we should not need to worry too much about the fund’s current leverage.

Distribution Analysis

As already mentioned, the primary investment objective of the Pioneer Floating Rate Fund is to provide its investors with a very high level of current income. In pursuance of this objective, the fund purchases floating-rate securities that typically have a coupon rate that is a few percentage points higher than the SOFR rate. Thus, the coupon rate on the securities in the fund is probably around 9% to 10% right now. The fund invests its assets into a portfolio of these securities and then applies a bit of leverage to control more securities than it can by relying solely on its own net assets. This allows the fund to collect a higher level of income than would otherwise be possible. The fund collects all of the payments that it receives from the securities in its portfolio and distributes them to its shareholders, net of its own expenses. As the securities themselves have a fairly high yield, we can expect that this strategy will give the fund’s shares a comparably high yield.

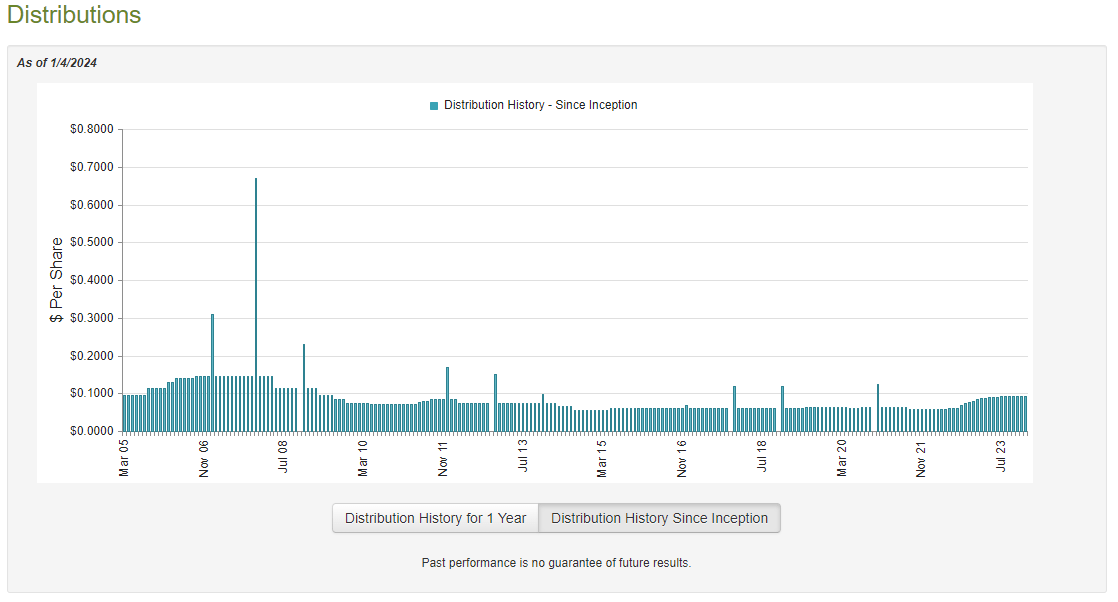

This is certainly the case, as the Pioneer Floating Rate Fund pays a monthly distribution of $0.0925 per share ($1.11 per share annually), which gives it a 12.20% yield at the current price. Unfortunately, the fund has not been especially consistent with respect to its distributions over the years. As we can see here, the fund has both raised and lowered its distributions several times over its lifetime:

{kind=link}

This may prove to be a turn-off for those investors who are seeking to earn a safe and consistent income from the assets in their portfolios. However, it is hardly something that is unexpected considering the nature of the securities that the fund invests in. After all, as we have already seen, floating rate securities are incredibly stable over time and are generally immune to the price changes that would otherwise accompany swings in interest rates. As such, the return that investors will receive is directly dependent on the coupon that these securities pay and that is a function of short-term interest rates. Thus, we can generally expect that this fund’s distributions will increase when the federal funds rate goes up and vice versa. This is one of the reasons why it has raised its distribution three times over the past twelve months, which actually works out well for those investors who need extra money to cover the rising cost of living in today’s inflationary environment.

As is always the case though, it is important that we ensure that the fund can actually afford the distributions that it pays out. After all, we do not want to be the victims of a distribution cut that destroys the fund’s net asset value.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. As such, it will not include any information about the fund’s performance over the past seven months, which is quite disappointing. After all, we have seen a generally volatile market over that period, as the bond market fell over the summer as participants began to accept that there would be no near-term pivot by the Federal Reserve, but that reversed in October when investors started to get excited about the prospect of 2024 rate cuts. As we saw earlier in this article, these hopes may end up dashed as well. This report will unfortunately provide no insight into how well the fund handled both of these disparate environments. We will have to wait for the full-year report to be released over the next few weeks to have that information.

During the six-month period, the Pioneer Floating Rate Fund received $9,005,464 in interest and $191,436 in dividends from the assets in its portfolio. This gives the fund a total investment income of $9,196,900 over the six-month period. It paid its expenses out of this amount, which left it with $6,685,608 available to shareholders. That was, fortunately, sufficient to cover the $6,434,965 that the fund paid out in distributions over the same period. Thus, it appears that the fund is fully covering its distribution out of its net investment income. This should be somewhat comforting to its shareholders.

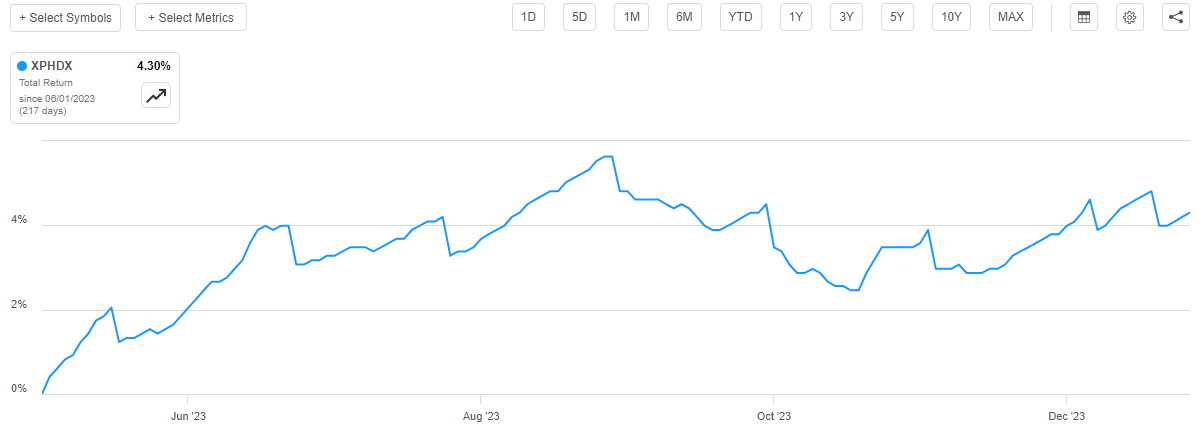

It appears that this continues to be the case. As we can see here, the fund’s net asset value per share is up 4.30% since June 1, 2023:

{kind=link}

This very strongly implies that the fund has fully covered all of the distributions that it has paid out since the closing date of its most recent financial report. As such, we should not need to worry about its distribution being destructive to the net asset value. The big risk here is that a decrease in the federal funds rate will probably decrease the fund’s net investment income, but as already mentioned I doubt that is as big a concern as the market appears to believe.

Valuation

As of January 4, 2023 (the most recent date for which data is currently available), the Pioneer Floating Rate Fund has a net asset value of $10.19 per share but the shares currently trade for $9.14 each. This gives the fund’s shares a 10.30% discount on net asset value at the present price. This is a bit better than the 9.74% discount that the shares have had on average over the past month, so today’s price looks reasonable to buy into the fund.

Conclusion

In conclusion, the Pioneer Floating Rate Fund is looking rather attractive considering that the market is probably wrong about the degree to which the Federal Reserve will cut interest rates over the next year. That situation could lead to a broad selloff of fixed-rate bonds and cause this fund to outperform.

The fact that Pioneer Floating Rate Fund, Inc. currently has a higher yield than most fixed-rate bond funds adds to its appeal somewhat, as income investors are certainly not sacrificing anything by switching their assets into this fund. The PHD distribution appears to be sustainable for the time being as the fund has an attractive valuation, so overall there is a lot to like here.

For further details see:

PHD: Switch From Bonds Into This Floating-Rate Loan Fund