PM - Philip Morris Earnings: A Clear-Cut Investment Case Doesn't Make It Good Buy

Summary

- 2022 was a landmark year for Philip Morris International Inc.

- The acquisition of Swedish Match and the agreement with Altria will see Philip Morris re-enter the U.S. market - as the strongest player in modified risk products.

- In this article, I summarize the key events of 2022 and outline what investors should look for when PM releases its annual results tomorrow, February 09.

- Moreover, I will provide an updated discounted cash flow sensitivity analysis and historical valuation.

- While the bull case is clear, Philip Morris International Inc. is still not a straight-forward investment.

Introduction

Philip Morris International Inc. (PM) will report full-year results tomorrow, February 9, 2023, at approximately 7 AM ET. I previously reported on the company in July and in October 2022.

In this update, I will discuss recent events and what investors should look for in the upcoming earnings report. After all, Altria Group, Inc. ( MO ), the U.S. business of the original Philip Morris before the 2008 spinoff, recently reported a disproportionate 10% year-over-year decline in smokable product volume, suggesting that the industry as a whole is shrinking faster than previously thought. 2022 was a very important year for Philip Morris, with the company making it clear that it will re-enter the U.S. market primarily through oral tobacco products (market leader ZYN) and at a later date through its IQOS heated tobacco franchise. However, this appears to be just the beginning of a strong growth trajectory.

Analyst Estimates For Philip Morris' Full-Year Earnings

As is widely known, Philip Morris stock trades at a significant premium to U.S.-focused Altria Group and global player British American Tobacco ( BTI , BTAFF ). The reasoning is simple to understand - Philip Morris is a leader in modified risk products (e.g., heated tobacco, oral products, but not vapes), does not suffer from significant concentration risks like Altria (U.S. only) and BTI ( market leader in menthol in the U.S.), is currently less leveraged than BTI, and unlike Altria, has not made any serious management mistakes ( $12.8 billion JUUL transaction ). Personally, I think PM deserves a valuation premium, but I think the current share price of over $100 is a bit expensive, as I will outline in the valuation update at the end of the article. At the same time, I consider the downside rather limited due to the strong bull narrative.

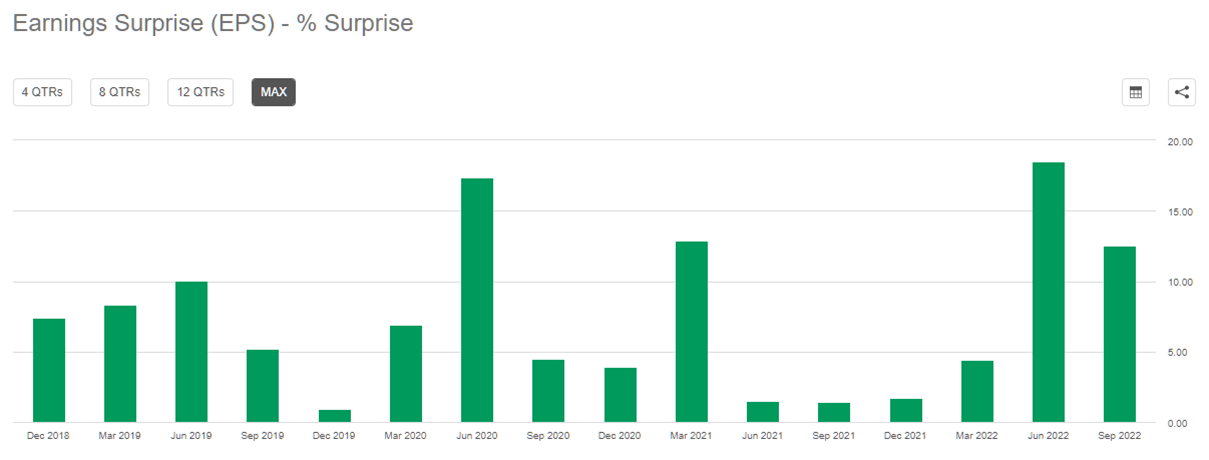

The analyst consensus for annual earnings per share ((EPS)) is $5.67 (or a forward price-to-earnings ratio of 18), which has changed little over the past six months, according to Seeking Alpha . This is hardly surprising, as tobacco companies generally generate very reliable cash flow and PM is no exception to this rule. FAST Graphs shows that analysts have increased their EPS estimates by 6% over the past six months (from $5.52 to $5.87). While I don't think this is significant, it does suggest that - regardless of any unforeseen announcements - there should be no nasty surprise ahead. Quite the contrary, the company has a very solid track record of positive earnings surprises, as shown in Figure 1, which shows quarterly EPS surprises according to Seeking Alpha .

{kind=link}

Figure 1: Philip Morris' [PM] earnings surprises in percent on a quarterly basis (obtained with permission from the Earnings tab of PM's stock quote page on Seeking Alpha)

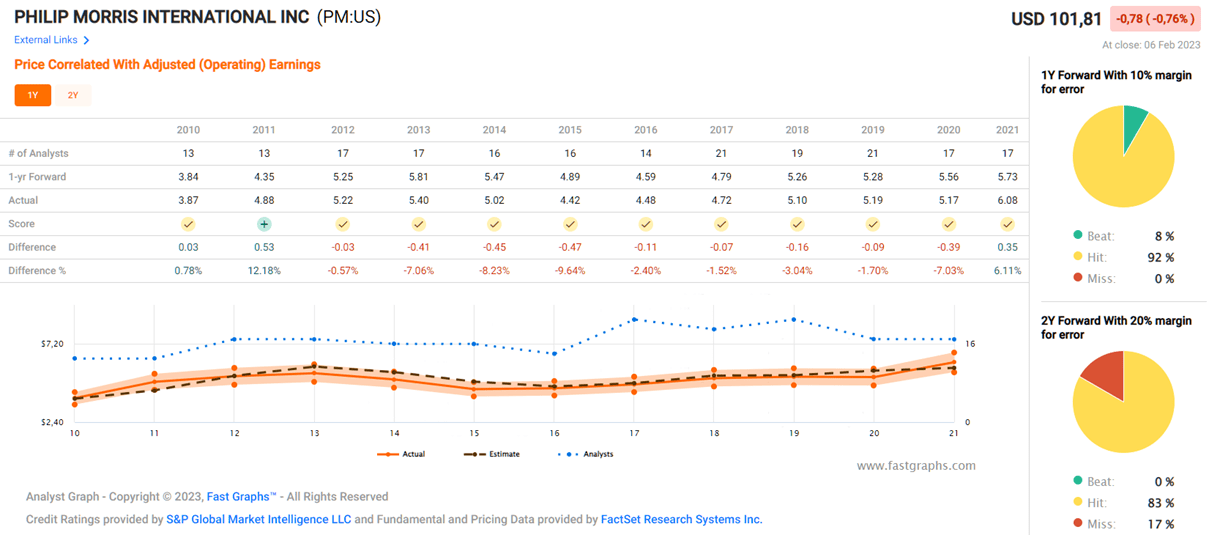

The longer-term picture also looks very good, as the company met analysts' one-year forward expectations 92% of the time, with a margin of error of 10% (Figure 2).

{kind=link}

Figure 2: One-Year-Forward Analyst scorecard for Philip Morris [PM] (obtained with permission from www.fastgraphs.com)

PMI's Combustibles Volumes

In the third quarter of 2022, Philip Morris reported stable volume trends and, as expected due to the inelasticity of the product, solid pricing action. Net sales for the first nine months of 2022 grew by 7.7% on a pro-forma adjusted basis (excluding the businesses in Russia and Ukraine). Total shipment volume grew 3.4% on an adjusted basis, driven by strong growth in heated tobacco units (HTUs) of 15.8% on an adjusted basis and post-pandemic recovery in certain markets. So for the full year, the company can be expected to deliver healthy volume growth, and it is of course very reassuring to see that PM is able to grow not only on an EPS basis, but also in terms of volumes. In this context, of course, Altria's volume decline of almost 10% year-over-year (smokable products segment) is a bit hard to swallow, especially because the company does not currently have a meaningful portfolio of modified risk products (see my earnings review ).

Philip Morris' Swedish Match Transaction And Its Impact

The biggest news of 2022 was PM's bid for Swedish Match ( SWMAY ), maker of the leading oral nicotine pouch brand ZYN. In May, PM offered SEK 106 per share. In October, the offer was increased to SEK 116, according to CEO Olczak primarily due to Swedish Match's cash flows generated in U.S. dollars (which has appreciated considerably since the original offer). While it was initially uncertain whether the transaction would be accepted by enough shareholders, PM said in November that it raised its stake to 93%, allowing it to initiate a forced redemption of the remaining shares, according to Reuters . The transaction was approved by regulators in late October (p. 53, 2022 10-Q3 ).

This transaction will allow PM to re-enter the U.S. market, which I view as an excellent opportunity due to its high margins. In addition to nicotine-containing pouches, snuff, and chewing tobacco (67% of 2021 sales, 74% of operating income), Swedish Match is also active in cigars (26% of 2021 sales, 23% of operating income) and matches (7% of 2021 sales, 4% of operating income). However, the transaction is not only a smart move from the perspective of acquiring the market leader in oral nicotine products, strengthening PM's position as the tobacco company with the leading modified risk portfolio. Importantly, Swedish Match also gives PM access to a very well-developed distribution network, which it can also use to distribute its heated tobacco product IQOS. PM can market IQOS on its own beginning May 2024, when its commercial relationship with Altria Group ends. However, I am confident that it will have a head start in the U.S., as IQOS has already been authorized as a modified risk tobacco product ((MRTP)) in 2020. Things are also looking increasingly good from a regulatory perspective, as PM will circumvent the U.S. International Trade Commission's import ban on IQOS by manufacturing the device domestically.

However, PM is not relying solely on IQOS's MRTP; it also intends to file a Premarket Tobacco Product Application ((PMTA)) for IQOS ILUMA in the second half of 2023. Unlike IQOS, IQOS ILUMA is no longer blade-based, but uses induction technology and therefore no longer conflicts with BTI's patented technology .

The Swedish Match transaction is extremely good news for PM shareholders, as the U.S. also represents the largest smoke-free market in the world. With its strong positioning, PM expects to achieve a 10% volume share of cigarettes and HTUs by 2030. IQOS will be the primary vector for establishing a leadership position in the U.S., but other products in PM's smoke-free portfolio will follow, according to Emmanuel Babeau, the company's CFO. The company also recently announced an agreement with South Korea's KT&G that expands and deepens their collaboration and gives PM exclusive rights to market KT&G's smoke-free devices and consumables worldwide, excluding South Korea. In addition, in late November 2022, the company announced the launch of BONDS, a bladeless, compact, heated tobacco device, in a pilot market in the Philippines.

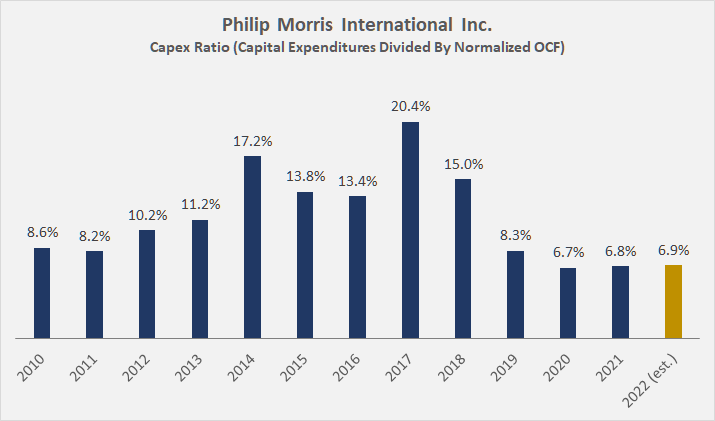

All of this, of course, comes at a significant cost. The Swedish Match deal will cost about $16 billion, excluding net debt of $1.2 billion (SEK 13 billion at the end of 2021). The Altria deal costs PM $2.7 billion plus interest (6% p.a.), of which $1 billion has already been booked by Altria in Q4. PM must pay the remaining $1.7 billion by July 2023, with the option to pay earlier. In addition, as I pointed out in another article , Philip Morris is investing heavily in its business. PM's average capex ratio (capital expenditures divided by normalized operating cash flow, nOCF) is 12% between 2010 and 2021, but after the relative and absolute peak in 2017 ($1.55 billion), reinvestment in the business has declined noticeably (Figure 3). In contrast, Altria has reinvested about 3.7% of its nOCF back into the business (2010 to 2021 average).

{kind=link}

Figure 3: Capex ratio of Philip Morris [PM], capital expenditures divided by operating cash flow, normalized with respect to working capital expenditures and adjusted for stock-based compensation (own work, based on the company's 2010 to 2021 10-Ks, the 2022 10-Q3 and own estimates)

According to the company's 2022 10-Q3 cash flow statement, no material cash outflows were recorded for acquisitions. At the end of Q3 2022, PM's net debt was approximately $22 billion, which represents a notional 2.8 years of debt repayment, assuming PM theoretically suspends its dividends (buybacks are not material at this time). This is hardly a worrying level of debt, especially given the stable cash flow the business throws off. Therefore, I am not irritated by the current shareholders' deficit of $7.4 billion (total assets of $48.1 billion).

To finance the Swedish Match transaction, PM has entered into a one-year unsecured bridge facility ($17 billion, later reduced to $11 billion) and a €5.5 billion term loan agreement. According to Moody's , the acquisition will increase PM's leverage by approximately 36% to 3.0 times EBITDA (2.2 times standalone). Moody's expects the company to be able to bring leverage back down to 2.5 times EBTIDA by the end of 2024.

While the transaction is certainly digestible for PM, dividend increases will continue to be quite modest going forward. After all, PM paid out $7.3 billion in dividends in 2021 and currently generates a little less than $8 billion in normalized free cash flow per year. Still, as a long-term shareholder who is a big fan of the transaction, I don't mind a period of slower dividend growth, and this has been communicated transparently by management.

All in all, I think the transaction is a smart move because of the opportunities it presents. When PM publishes its full-year results tomorrow, I will be very interested to see whether net debt has already moved. Going forward, investors should take a look at the rates at which PM refinances the unsecured bridge facility and the term loan, but this will likely take a while. It is also likely that PM will repay the outstanding $1.7 billion to Altria rather quickly to avoid paying a 6% annual coupon. Even though interest rates have risen, the increased interest burden after the Swedish Match transaction and the final payment to Altria will remain manageable, especially because PM also borrows in euros (still considerably lower rates than in the U.S.) and has a very good standing with rating agencies. For example, Moody's affirmed PM's long-term rating at A2 with a stable outlook in November 2022, recognizing the "strong strategic rationale for PMI's acquisition of Swedish Match, which has a portfolio of smoke-free products and has been growing particularly well in the U.S."

Conclusion - What To Look For In The Earnings Report And When I Would Buy PM Stock

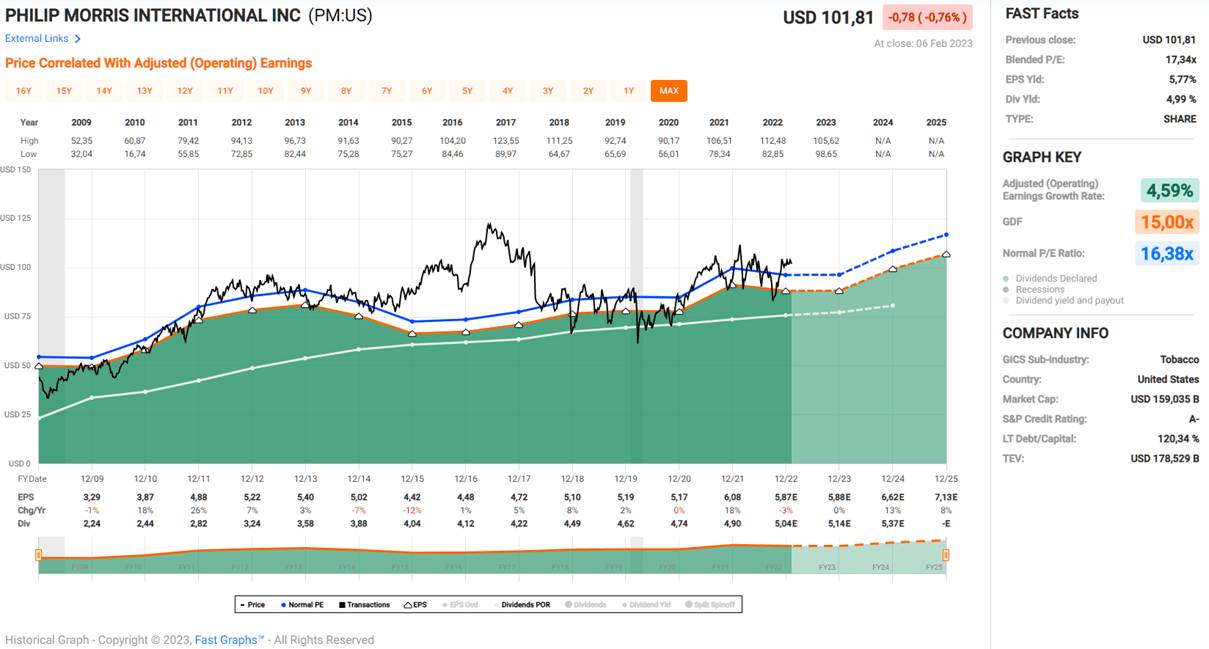

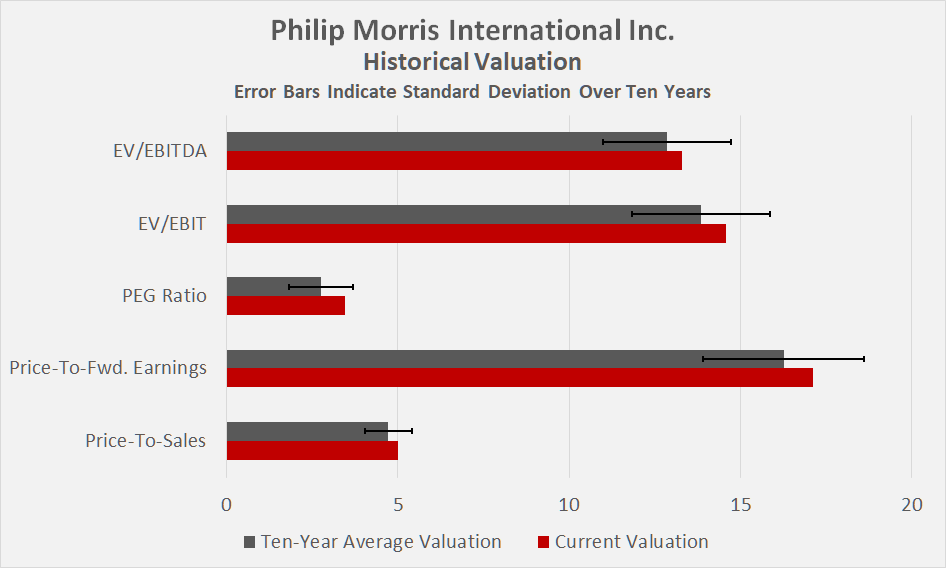

Philip Morris will report its full-year results tomorrow before the stock market opens. At a current price of $102, the stock is trading at a blended price-to-earnings ratio of 17, according to FAST Graphs, which should be considered at least somewhat expensive (Figure 4). The historical valuation, including data since 2013, also suggests the stock is slightly overvalued (Figure 5). Investor service Morningstar currently rates PM with three stars, a fair value estimate of $103 and a medium uncertainty.

{kind=link}

Figure 4: FAST Graphs chart of Philip Morris stock [PM] (obtained with permission from www.fastgraphs.com)

{kind=link}

Figure 5: Historical valuation of Philip Morris [PM] stock (own work, based on data supplied by Morningstar)

Valuing PM based on its free cash flow, I believe a cost of equity of 8% is appropriate. This is two percentage points less than I am requiring for my investment in Altria (see my recent valuation ) due to the higher risks (U.S. market only, no tangible modified risk products portfolio). A long-term cash flow growth rate of 2% to 3% doesn't seem like an overly aggressive expectation given PM's already strong performance in the modified risk products segment, the Swedish Match transaction, and its re-entry into the highly profitable U.S. market. However, also from this perspective, the shares are currently slightly overvalued, as shown by the sensitivity analysis in Figure 6.

Figure 6: Discounted cash flow sensitivity analysis of Philip Morris [PM] (own work, based on the data found in the 2022 10-Q3 and on own estimates for free cash flow)

It looks like PM will present solid full-year results considering the stable volume trends and good pricing so far in 2022. Even without the business in Russia and Ukraine, PM remains the top player in modified risk products. It is important to understand that the economies underlying heated tobacco products are even more attractive than regular cigarettes in terms of profitability, partly due to more favorable taxation. All in all, the gross margin of HTUs is typically about 10 percentage points higher than that of regular cigarettes.

Since I have no current plans to increase my already significant position, I will simply hold on to my shares. If I were not currently invested in the stock, I would at least consider buying a small initial position before the results are released, since PM oftentimes rallies after the earnings announcement. However, at the same time, and given the trading range of Philip Morris stock, I would be careful to not let the fear of missing out affect my thinking. At over $100, the stock is not cheap, and with no real catalysts in the near term, I don't see any reason to expect much upside in the short term, so I wouldn't be in a hurry to build my position.

In addition, after analyzing the press release, I would try to answer the following questions:

- Are cigarette volumes as robust as previously thought? What about the growth in HTU volumes? Is the 2023 target of 150 billion HTUs (slide 9 of this presentation ) still achievable, even taking into account ex-Ukraine and ex-Russia, former IQOS growth markets? In any case, I would not over-interpret a temporary slowdown, as sales of the "normal" IQOS devices will suffer as consumers learn about the more advanced induction-based IQOS ILUMA system.

- Did management pay the $1.7 billion to Altria? Altria's full-year cash flow statement shows only the initial $1.0 billion payment, but perhaps the transaction was settled after year-end. Paying a 6% coupon is no mean feat, although the $1.7 billion principal is certainly not really significant. In any case, I would like to see the company borrow cheaper to finance this payment or pay it directly from cash on hand.

- How did PM's capital expenditure ratio fare in 2022?

- How did the working capital accounts develop in 2022? As a high-margin business with a very simple product, I doubt the current inflationary environment has a significant impact, same as supply chain disruptions (except for IQOS device shipments). With this in mind, I would not over-interpret a temporary decline in operating margin. Management has already indicated that Q3 operating margin was depressed due to costs associated with the IQOS ILUMA rollout.

- Is the 2023 guidance still in line with previous expectations? Excluding the Russia and Ukraine business, PM still expects annual sales growth of over 5% and adjusted earnings per share of over 9%, but based on rebased earnings.

Thank you very much for taking the time to read my article. How did you like it, my style of presentation, the level of detail? If there is anything you'd like me to improve or expand upon in future articles, do let me know in the comments section below.

For further details see:

Philip Morris Earnings: A Clear-Cut Investment Case Doesn't Make It Good Buy