SWMAY - Philip Morris Is A 5.1%-Yielding Dividend Aristocrat Retirement Dream Buy

Summary

- After a tough start to 2022, Philip Morris International Inc. is back on track, posting incredible growth in Q4 and 43% 2023 growth guidance that leaves all its peers in the dust.

- 33% of sales are now reduce-risk products, and Philip Morris International is on track to get most of its sales from RRPs by 2025.

- Philip Morris' growth outlook has recovered from the war and now offers the 2nd-best growth in the industry.

- The Swedish Match acquisition gives Philip Morris the distribution capacity to launch iQos in 2023, and it now has exclusive rights to iQos in America.

- Philip Morris International Inc. is a 5.1% yielding dividend king retirement dream stock that offers 13.7% long-term return potential, is 7% undervalued, and is a great Buffett-style "wonderful company at a fair price." It's a potentially good buy for anyone comfortable with its risk profile, and I bought 1,000 shares for my family hedge fund.

A version of this video article was published on Dividend Kings on Tuesday, February 21st, 2023.

---------------------------------------------------------------------------------------

Do you know what my family loves? Generous, safe, and growing dividends. It's not just nice to have during a bear market or recession; we're literally paying medical bills with dividends.

So for my family, safe dividends are literally a matter of life and death. Which is why I'm so happy to recommend Philip Morris International Inc. ( PM ) today.

Let me show you the three reasons that I'm so impressed with this 5.1% yielding retirement dream dividend aristocrat; I bought 1,000 shares for my family's hedge fund.

And even if you can't afford to buy that much, I think you'll agree that this rich retirement dream aristocrat is one that's well worth buying for your diversified and prudently risk-managed portfolio.

Reason One: Philip Morris Is Now The Lowest-Risk Tobacco Company In The World

Investing in tobacco while avoiding dividend cuts and value traps is all about one thing: What is a company's plan to transition to a tobacco-free future, and how well is it executing that plan.

PM was the first tobacco giant to develop reduced-risk products, or RRPs, via its iQos heat sticks.

The reason for that was simple.

- heat sticks can be branded with popular cigarette brands, so PM's brand loyalty would remain intact

- heat sticks offer an experience most similar to traditional cigarettes

- it's the most popular RRP product for older smokers

- younger smokes and nicotine users prefer vaping

- but PM's core customers are older smokers.

PM has spent over $9 billion developing, improving, and launching iQos in steadily more countries. For years, it was losing money on heat sticks, but now it's earning 0.1% higher gross margins on iQos than it does on traditional cigarettes.

Wall Street loves PM and grants it a much higher multiple than either BTI or MO. Why is that? Simple. PM has the world's best cigarette brands and is the global leader in RRPs.

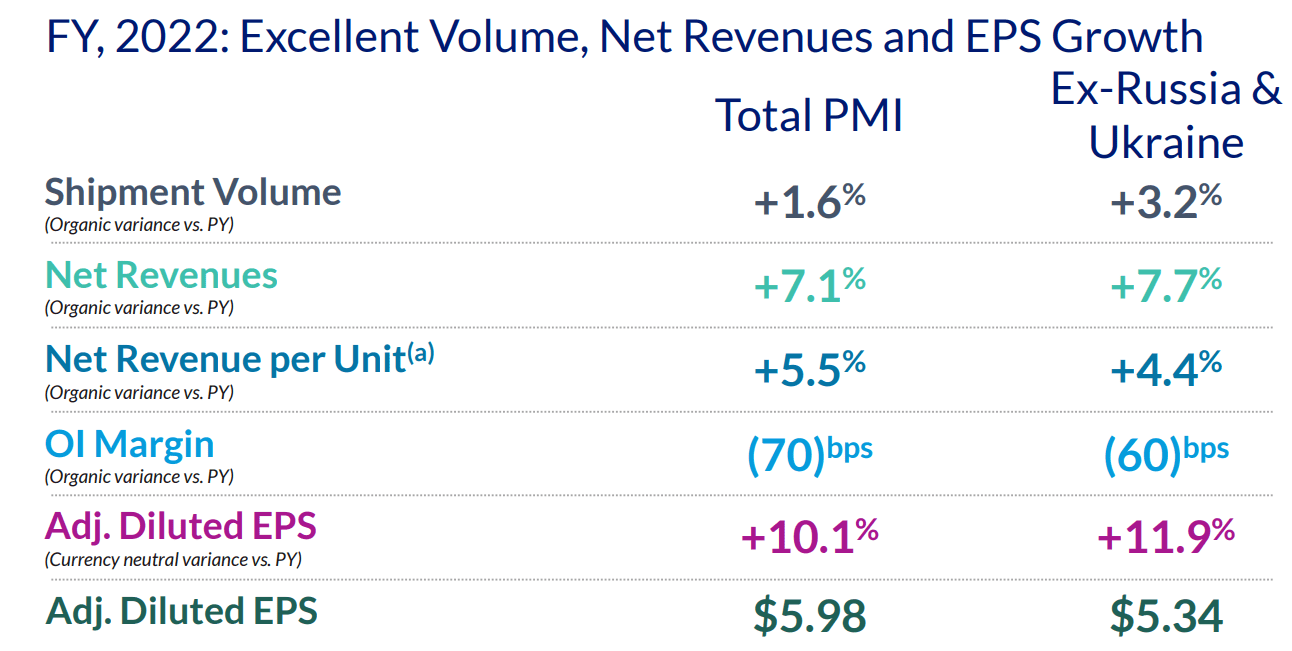

How can we tell? Take a look at PM's cigarette volume declines in 2022.

{kind=link}

Excluding Russia and Ukraine, PM's total volumes rose 3.2%, and its cigarette volumes fell just 0.5% for the full year. Its constant currency operating EPS grew almost 12%.

For context, BTI had a 5% volume decline in 2022 and MO about 9%.

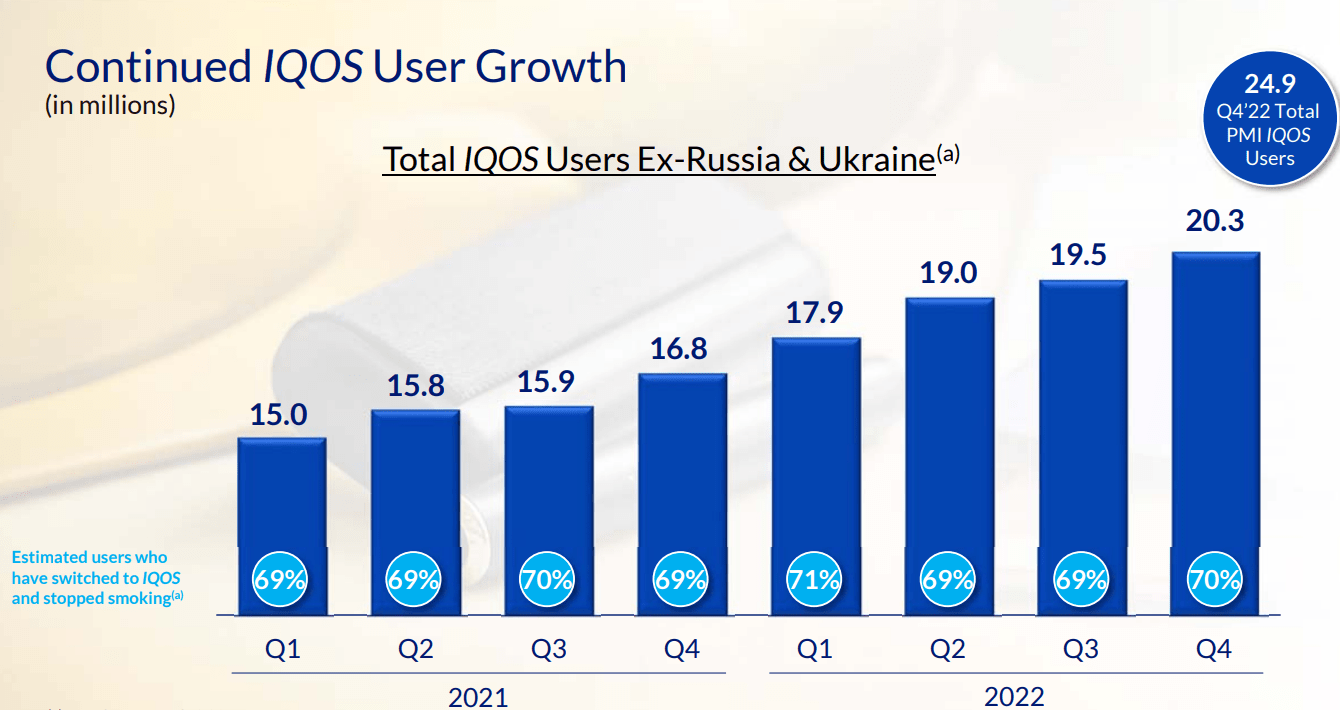

The Russian invasion badly hurt PM's RRP growth rates, but things appear to be getting back on track.

{kind=link}

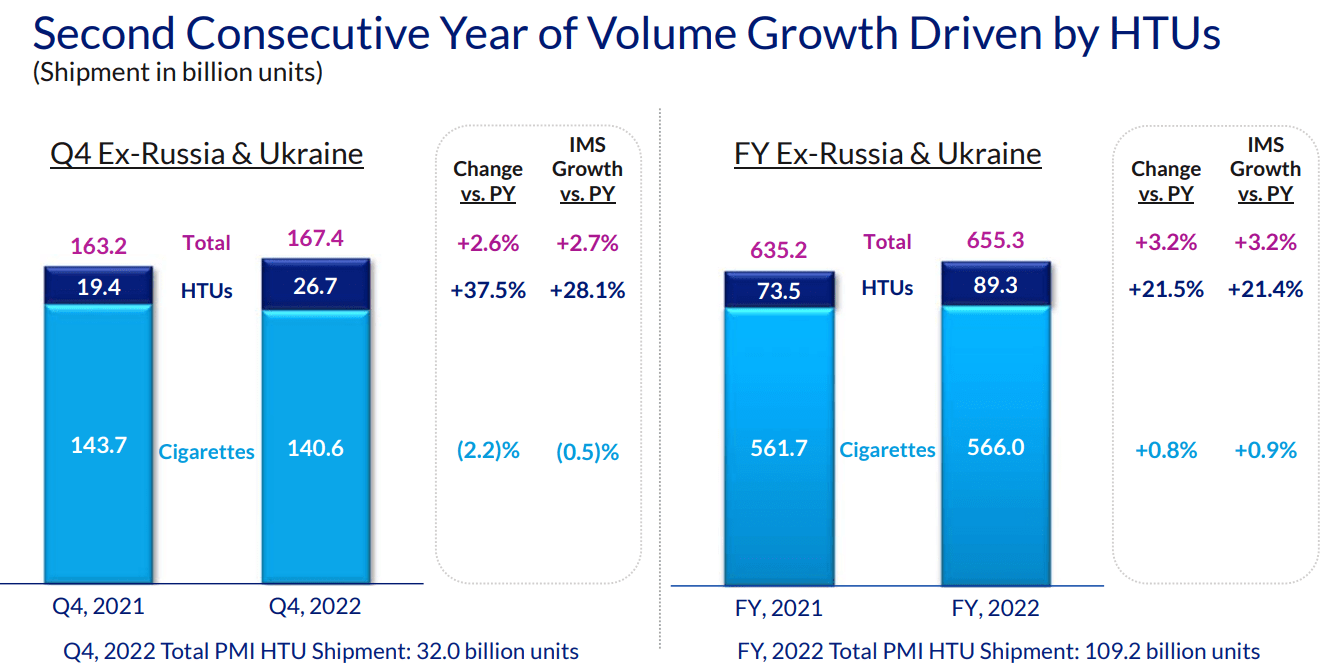

In 2022 heat stick volumes grew 22%, and 38% in Q4. And management is guiding for 43% heat stick growth in 2023.

In 2022 32% of PM's sales were RRPs and that's expected to grow to 39% by 2024.

{kind=link}

Management's goal is to achieve the majority of sales from RRPS by 2025, and it's on track to achieve that goal.

{kind=link}

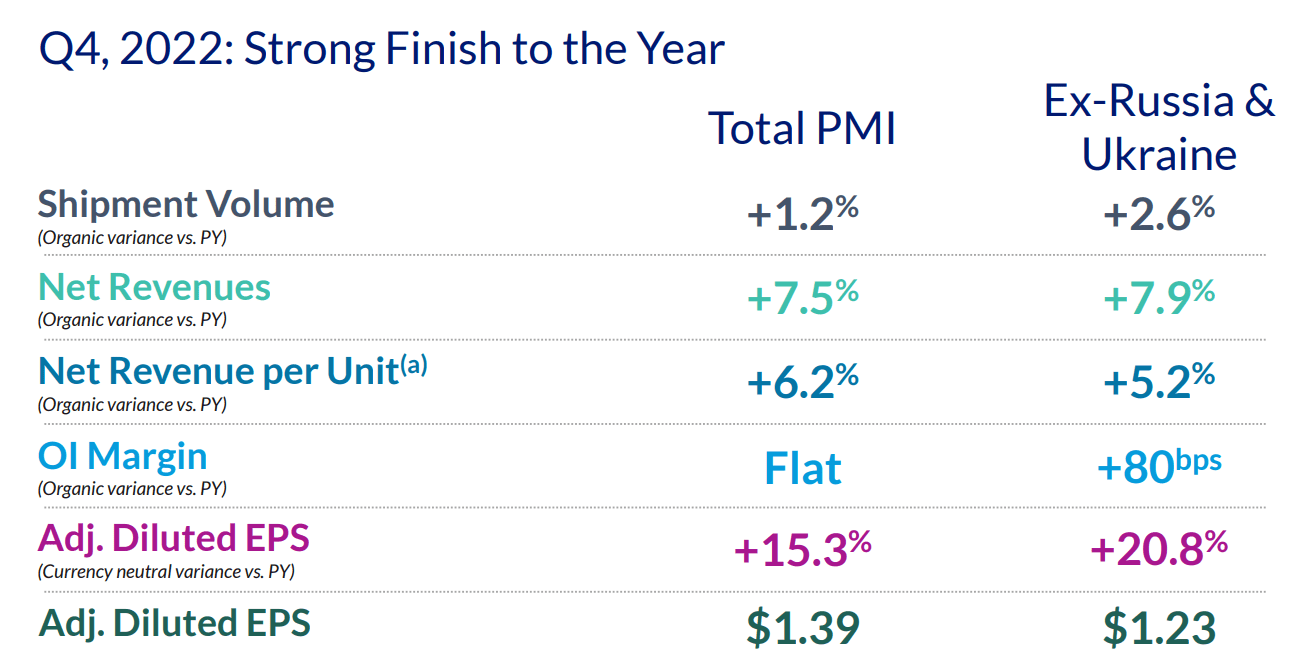

How many tobacco companies delivered 8% sales growth in Q4? Only PM.

How many delivered 21% operating EPS growth? Only PM.

{kind=link}

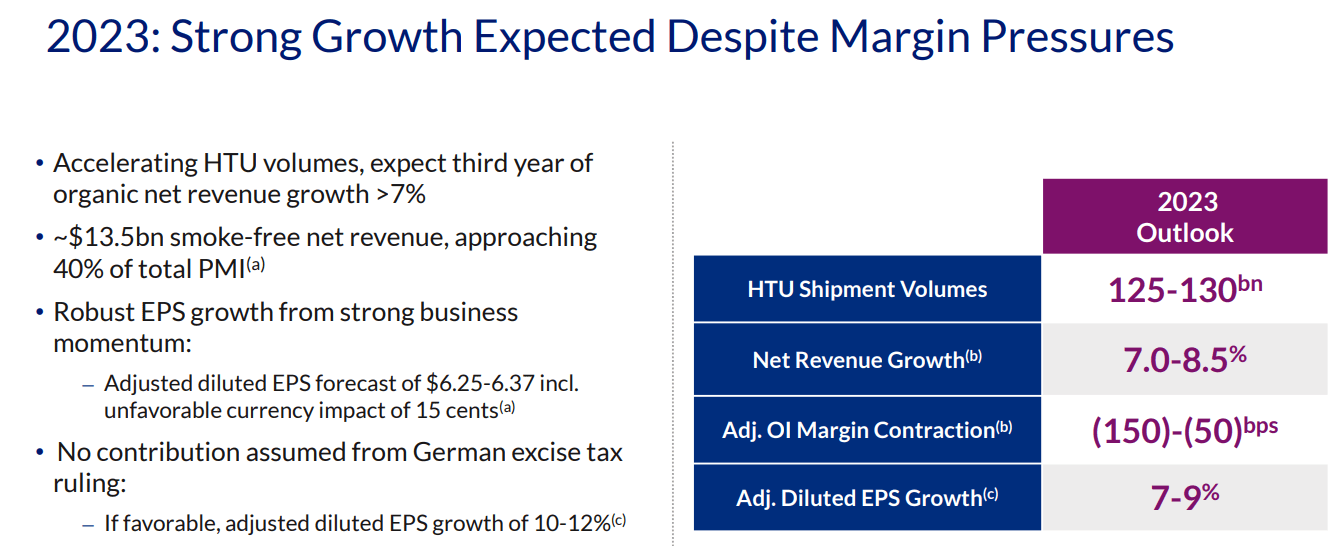

Management expects about a 1% decline in margins in 2023 but still expects to deliver about 8% EPS growth, which is 3% to 4% higher than BTI and MO, respectively.

After a tough year after the invasion, PM appears to be firing on all cylinders, and in 2023 looks to retake the industry's growth crown.

PM expects a tougher economy and continued high inflation to cause consumers to trade down their cigarette brands, which is what hurt Altria Group, Inc. (MO) and British American Tobacco p.l.c. (BTI) in 2022.

But it still expects to post about 0.5% total volume growth while global industry volumes (including RRPs) are expected to decline by 1.5%.

{kind=link}

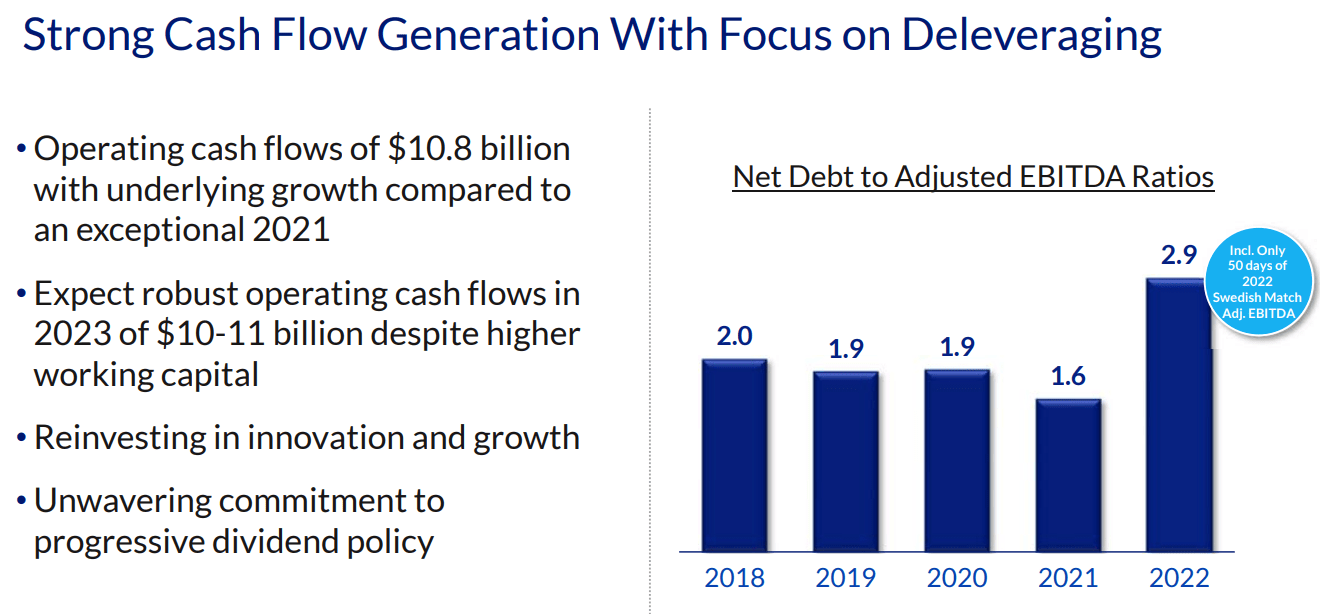

After acquiring Swedish Match AB (SWMAY) in a debt-funded deal, leverage has jumped, but remains below the rating agency safety guideline of 3X net debt/EBITDA.

- By 2025 analysts expect net leverage to fall back to 1.9X.

PM remains committed to its 53-year dividend growth streak (inherited from MO) and expects to generate $9.3 billion in free cash flow in 2023.

- $7.9 billion is the annual dividend cost

- 85% free cash flow payout ratio vs. 85% safety guideline.

{kind=link}

Thanks to 4.6 million new iQos users in Q4, PM has overtaken BTI and retaken the RRP userbase lead.

{kind=link}

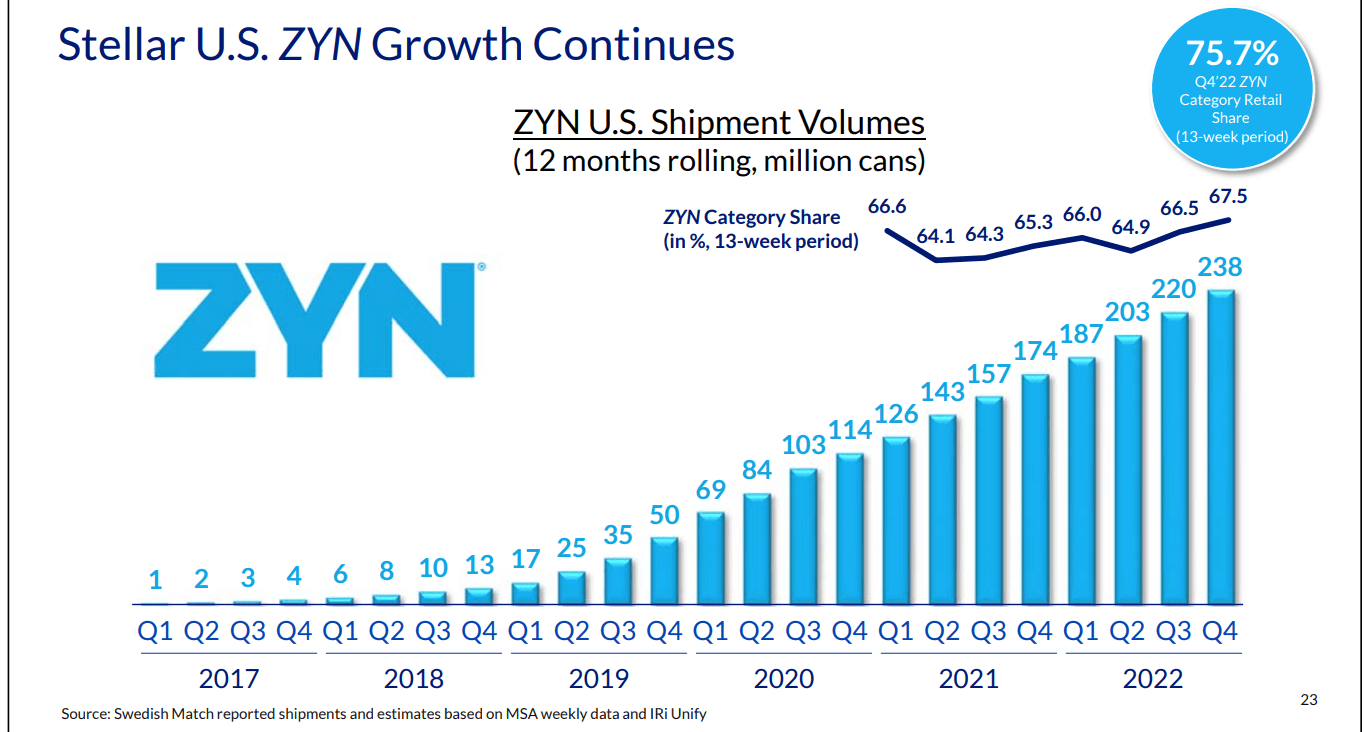

PM is #1 in heat sticks and #1 in oral nicotine in the U.S., with a 76% market share.

Swedish Match Is A Game Changer For PM

The $16 billion Swedish match acquisition closed in late 2022, and is expected to drive 13% sales growth in 2023. But this acquisition is a true game changer because Swedish Match owns Zyn, the #1 nicotine pouch brand in America.

Oral nicotine pouches are still a very small market, representing about 5% of the oral tobacco market. But Zyn is sold almost everywhere cigarettes are, meaning PM bought it for its logistics network.

In late 2022, PM bought the full rights to sell iQos in the U.S. from MO for $2.7 billion.

With Swedish Match, it now has the selling capacity to market iQos in the U.S. and keep 100% of the sales.

Why is this such a game changer? Because the FDA's proposed nicotine reduction regulations, which aren't expected to take effect until 2028 at the earliest, aren't expected to apply to RRPs like iQos.

They will apply to traditional cigarettes, like what MO sells.

And with PM now having the exclusive rights to market iQos in the U.S., it's possible that within seven years or so, U.S. smokers will be forced to switch from MO's product to PM's.

Cigarette smokers have the highest loyalty to any consumer staples product there is. But if cigarettes don't offer a nicotine fix and heat sticks do? Then it's possible that within a year or two after the regulations take effect, every Marlboro smoker in America could switch over from MO's products to PM.

MO and PM were once a single company.

They split into a U.S.-focused company and a globally-focused one.

PM was spun-off to allow MO investors to decrease their legal and regulatory risk after the Master Settlement.

With the Swedish Match acquisition and the full rights to market iQos in the U.S., PM is now a truly global company operating in every country, including America.

But PM has a diversified regulatory risk profile, unlike MO, which has pure U.S. regulatory risk.

Bottom Line: PM is on track to become the glorious Philip Morris of old in terms of global reach, but with a lot less risk and selling no cigarettes or tobacco within 15 to 20 years.

{kind=link}

PM is also diversifying into wellness and plans to get to $1 billion in non-nicotine sales by 2025.

- about 3% of sales.

While the wellness market it's pursuing is not as large as nicotine (a nearly $500 billion market), it's growing at 11% annually, about 2.5X faster than nicotine.

Reason Two: Excellent Growth Prospects For Decades To Come

What growth do analysts expect from PM in the next few years?

| Metric |

| 2022 Growth Consensus |

| 2023 Growth Consensus (recession) |

| 2024 Growth Consensus |

| 2025 Growth Consensus |

| Sales |

| 1% |

| 13% (Swedish Match) |

| 4% |

| 8% |

| Dividend |

| 2% |

| 2% |

| 4% |

| 5% |

| EPS |

| -2% (Russia/Ukraine/Currency) |

| 6% |

| 9% |

| 11% |

| Operating Cash Flow |

| -9% |

| -3% |

| 9% |

| 10% |

| Free Cash Flow |

| -13% |

| -4% |

| 10% |

| 10% |

| EBITDA |

| -3% |

| 13% |

| 8% |

| 9% |

| EBIT (operating income) |

| -4% |

| 15% |

| 7% |

| 8% |

(Source: FAST Graphs, FactSet.)

After a tough 2022, analysts expect growth to accelerate for several years. And once deleveraging is underway, dividend growth is also expected to accelerate, beginning in 2024.

- 4% dividend growth expected through 2025

- long-term management EPS payout ratio policy is 75%

- so dividends will match the long-term earnings growth rate.

How fast do analysts expect PM to grow now that it has the U.S. iQos market all to itself?

{kind=link}

8.6% long-term growth is second only to BTI (the global vaping leader) and 3% higher than MO's growth outlook.

| Investment Strategy |

| Yield |

| LT Consensus Growth |

| LT Consensus Total Return Potential |

| Long-Term Risk-Adjusted Expected Return |

| ZEUS Income Growth (My family hedge fund) |

| 4.1% |

| 10.2% |

| 14.3% |

| 10.0% |

| Philip Morris International |

| 5.1% |

| 8.6% |

| 13.7% |

| 9.6% |

| Altria |

| 8.0% |

| 5.5% |

| 13.5% |

| 9.5% |

| Vanguard Dividend Appreciation ETF |

| 2.2% |

| 10.0% |

| 12.2% |

| 8.5% |

| Schwab US Dividend Equity ETF |

| 3.6% |

| 8.6% |

| 12.2% |

| 8.5% |

| Nasdaq |

| 0.8% |

| 10.9% |

| 11.7% |

| 8.2% |

| Dividend Aristocrats |

| 1.9% |

| 8.5% |

| 10.4% |

| 7.3% |

| S&P 500 |

| 1.7% |

| 8.5% |

| 10.2% |

| 7.1% |

| REITs |

| 3.9% |

| 6.1% |

| 10.0% |

| 7.0% |

| 60/40 Retirement Portfolio |

| 2.1% |

| 5.1% |

| 7.2% |

| 5.0% |

(Sources: DK Research Terminal, FactSet, Morningstar.)

PM offers the same total return potential as MO, but with lower yield but superior growth prospects.

- MO will now be competing with PM in U.S. heat sticks

- iQos vs. Japan Tobacco's Horizon (MO has 75% revenue share).

Inflation-Adjusted Consensus Return Potential: $1,000 Initial Investment

| Time Frame (Years) |

| 7.9% CAGR Inflation-Adjusted S&P 500 Consensus |

| 11.5% CAGR Inflation-Adjusted PM Consensus |

| Difference Between Inflation-Adjusted PM Consensus And S&P Consensus |

| 5 |

| $1,465.25 |

| $1,720.26 |

| $255.01 |

| 10 |

| $2,146.96 |

| $2,959.31 |

| $812.35 |

| 15 |

| $3,145.84 |

| $5,090.79 |

| $1,944.96 |

| 20 |

| $4,609.44 |

| $8,757.51 |

| $4,148.07 |

| 25 |

| $6,753.99 |

| $15,065.24 |

| $8,311.25 |

| 30 (retirement time frame) |

| $9,896.29 |

| $25,916.19 |

| $16,019.90 |

| 35 |

| $14,500.55 |

| $44,582.70 |

| $30,082.15 |

| 40 |

| $21,246.95 |

| $76,694.03 |

| $55,447.08 |

| 45 |

| $31,132.11 |

| $131,934.00 |

| $100,801.89 |

| 50 |

| $45,616.37 |

| $226,961.37 |

| $181,345.00 |

| 55 |

| $66,839.43 |

| $390,433.55 |

| $323,594.12 |

| 60 (investing lifetime) |

| $97,936.56 |

| $671,648.92 |

| $573,712.37 |

| 100 |

| $2,080,852.87 |

| $51,511,461.50 |

| $49,430,608.64 |

(Sources: DK Research Terminal, FactSet.)

PM offers a very solid 11.5% real return potential that could be a 26X bagger within 30 years.

- Buffett's historical unlevered returns are 12.8%

- PM offers Buffett-beating return potential.

| Time Frame (Years) |

| Ratio Inflation-Adjusted PM Consensus vs. S&P consensus |

| 5 |

| 1.17 |

| 10 |

| 1.38 |

| 15 |

| 1.62 |

| 20 |

| 1.90 |

| 25 |

| 2.23 |

| 30 |

| 2.62 |

| 35 |

| 3.07 |

| 40 |

| 3.61 |

| 45 |

| 4.24 |

| 50 |

| 4.98 |

| 55 |

| 5.84 |

| 60 |

| 6.86 |

| 100 |

| 24.75 |

(Sources: DK Research Terminal, FactSet.)

PM offers 3X the yield of the S&P 500 (SP500) and the potential for 3X better inflation-adjusted returns over the next 30 years.

Reason Three: A Wonderful Company At A Fair Price

FAST Graphs, FactSet FAST Graphs, FactSet

PM's market-determined historical fair value is 16.5X earnings to 17.5X earnings.

| Metric |

| Historical Fair Value Multiples (13-Years) |

| 2021 |

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| 12-Month Forward Fair Value |

| 14-year average yield |

| 4.71% |

| $104.03 |

| $107.01 |

| $107.86 |

| $114.01 |

| NA |

| Earnings |

| 16.97 |

| $103.18 |

| $101.48 |

| $105.55 |

| $114.89 |

| $127.11 |

| Average |

| $103.60 |

| $104.17 |

| $106.69 |

| $114.45 |

| $127.11 |

| $107.89 |

| Current Price |

| $100.24 |

| Discount To Fair Value |

| 3.25% |

| 3.77% |

| 6.05% |

| 12.41% |

| 21.14% |

| 7.09% |

| Upside To Fair Value (Including Dividends) |

| 3.36% |

| 3.92% |

| 6.44% |

| 14.17% |

| 26.80% |

| 12.69% |

| 2023 EPS |

| 2024 EPS |

| 2021 Weighted EPS |

| 2022 Weighted EPS |

| 12-Month Forward EPS |

| 12-Month Average Fair Value Forward PE |

| Current Forward PE |

| $6.22 |

| $6.77 |

| $5.26 |

| $1.04 |

| $6.30 |

| 17.1 |

| 15.9 |

PM's historical fair value is about 17X earnings and now trades from 15.9X.

- A classic Buffett-style "wonderful company at a fair price."

PM offers a 13% upside to fair value over the next year.

| Rating |

| Margin Of Safety For Very Low-Risk 13/13 Ultra SWAN Quality Companies |

| 2023 Fair Value Price |

| 2024 Fair Value Price |

| 12-Month Forward Fair Value |

| Potentially Reasonable Buy |

| 0% |

| $106.69 |

| $114.45 |

| $107.89 |

| Potentially Good Buy |

| 5% |

| $101.36 |

| $108.73 |

| $102.49 |

| Potentially Strong Buy |

| 15% |

| $90.69 |

| $97.28 |

| $91.70 |

| Potentially Very Strong Buy |

| 25% |

| $76.02 |

| $85.84 |

| $80.91 |

| Potentially Ultra-Value Buy |

| 35% |

| $69.35 |

| $74.39 |

| $70.13 |

| Currently |

| $100.24 |

| 6.05% |

| 12.41% |

| 7.09% |

| Upside To Fair Value (Including Dividends) |

| 11.50% |

| 19.24% |

| 12.69% |

PM is a potentially good buy for anyone comfortable with its risk profile.

Risk Profile: Why Philip Morris Isn't Right For Everyone

There are no risk-free companies, and no company is right for everyone. You have to be comfortable with the fundamental risk profile.

PM's Risk Profile Includes

- regulatory risk (globally, including menthol bans, nicotine regulations, RRP tax rates, and plain packaging laws)

- smoke-free transition risk (PM is the industry leader)

- litigation risk (lower than in the U.S. due to lack of class action laws)

- M&A execution risk (Swedish Match is the largest deal PM has ever done)

- supply chain disruption risk

- black swan geopolitical risks (like the Russian invasion)

- labor market risk (tightest job market in 50 years globally)

- currency risk (Swedish Match reduces this).

How do we quantify, monitor, and track such a complex risk profile? By doing what big institutions do.

Long-Term Risk Management Analysis: How Large Institutions Measure Total Risk Management

DK uses S&P Global's global long-term risk-management ratings for our risk rating.

- S&P has spent over 20 years perfecting their risk model

- which is based on over 30 major risk categories, over 130 subcategories, and 1,000 individual metrics

- 50% of metrics are industry specific

- this risk rating has been included in every credit rating for decades.

The DK risk rating is based on the global percentile of how a company's risk management compares to 8,000 S&P-rated companies covering 90% of the world's market cap.

PM Scores 83rd Percentile On Global Long-Term Risk Management

S&P's risk management scores factor in things like:

- supply chain management

- crisis management

- cyber-security

- privacy protection

- efficiency

- R&D efficiency

- innovation management

- labor relations

- talent retention

- worker training/skills improvement

- occupational health & safety

- customer relationship management

- business ethics

- climate strategy adaptation

- sustainable agricultural practices

- corporate governance

- brand management.

PM's Long-Term Risk Management Is The 125th Best Risk Manager In The Master List (75th Percentile In The Master List)

| Classification |

| S&P LT Risk-Management Global Percentile |

| Risk-Management Interpretation |

| Risk-Management Rating |

| BTI, ILMN, SIEGY, SPGI, WM, CI, CSCO, WMB, SAP, CL |

| 100 |

| Exceptional (Top 80 companies in the world) |

| Very Low Risk |

| Strong ESG Stocks |

| 86 |

| Very Good |

| Very Low Risk |

| Philip Morris |

| 83 |

| Very Good |

| Very Low Risk |

| Foreign Dividend Stocks |

| 77 |

| Good, Bordering On Very Good |

| Low Risk |

| Ultra SWANs |

| 74 |

| Good |

| Low Risk |

| Dividend Aristocrats |

| 67 |

| Above-Average (Bordering On Good) |

| Low Risk |

| Low Volatility Stocks |

| 65 |

| Above-Average |

| Low Risk |

| Master List average |

| 61 |

| Above-Average |

| Low Risk |

| Dividend Kings |

| 60 |

| Above-Average |

| Low Risk |

| Hyper-Growth stocks |

| 59 |

| Average, Bordering On Above-Average |

| Medium Risk |

| Dividend Champions |

| 55 |

| Average |

| Medium Risk |

| Monthly Dividend Stocks |

| 41 |

| Average |

| Medium Risk |

(Source: DK Research Terminal.)

PM's risk-management consensus is in the top 25% of the world's best blue-chips, on par with the likes of:

- Visa ( V ): Ultra SWAN

- T. Rowe Price ( TROW ): Ultra SWAN dividend aristocrat

- Lowe's ( LOW ): Ultra SWAN dividend king

- Target ( TGT ): Ultra SWAN dividend king.

The bottom line is that all companies have risks, and PM is very good at managing theirs, according to S&P.

How We Monitor PM's Risk Profile

- 21 analysts

- three credit rating agencies

- 24 experts who collectively know this business better than anyone other than management

- and the bond market for real-time fundamental risk-assessment.

When the facts change, I change my mind. What do you do, sir?" - John Maynard Keynes

There are no sacred cows at iREIT or Dividend Kings. Wherever the fundamentals lead, we always follow. That's the essence of disciplined financial science, the math behind retiring rich, and staying rich in retirement.

Bottom Line: Philip Morris Is A 5.1% Yielding Dividend King Retirement Dream Stock

Let me be clear: I'm NOT calling the bottom in PM (I'm not a market-timer).

13/13 Ultra SWAN quality does NOT mean "can't fall hard and fast in a bear market."

Fundamentals are all that determine safety and quality, and my recommendations.

- over 30+ years, 97% of stock returns are a function of pure fundamentals, not luck

- in the short term; luck is 25X as powerful as fundamentals

- in the long term, fundamentals are 33X as powerful as luck.

While I can't predict the market in the short term, here's what I can tell you about PM.

- The industry leader in reduce-risk products

- the global king of heat sticks

- 53-year dividend growth streak

- relatively safe 5.1% yield (growing at 4% for the next few years)

- 13.7% long-term return potential Vs. 10.2% S&P

- 7% historically undervalued

- 15.9X earnings vs. 16.5 to 17.5 historical

- 13X cash-adjusted earnings

- 87% consensus return potential over the next six years, 12% annually, 50% more than the S&P 500

- 3X more income potential than the S&P

- 33% better risk-adjusted expected returns.

(Source: Dividend Kings Automated Investment Decision Tool)

{kind=link}

If you want to sleep well at night in this looming recession, a high-yield dividend king firing on all cylinders is a great way to do it.

If you want to generate strong and very safe income that grows every year like clockwork, Philip Morris International Inc. is one of the best choices today.

And if you want to retire in safety and splendor, or just pay the bills, Philip Morris International Inc. is one of the best world-beater dividend blue chips you can buy right now.

For further details see:

Philip Morris Is A 5.1%-Yielding Dividend Aristocrat Retirement Dream Buy