KTCIF - Philip Morris: Solid Q4 Multiple Growth Drivers For 2023 Onwards

Summary

- Philip Morris International Inc. finished 2022 with a solid 2022. Despite cost headwinds, Adjusted EPS grew 11.9% excluding currency and Russia/Ukraine.

- Heated Tobacco Unit shipments grew 14.9% in 2022, including 40.1% in the European Union, and cigarette volumes were stable.

- IQOS ILUMA has been a success; PM has broadened its Reduced Risk Products portfolio and is working on expanding in the U.S.

- Philip Morris has a 19x P/E and a 5% Dividend Yield, though we expect no buybacks and only token dividend hikes until 2025.

- With Philip Morris International shares at $102.02, we expect a total return of 47% (15.3% annualized) by 2025 year-end. Buy.

Introduction

Philip Morris International Inc. ( PM ) released Q4 2022 results on Thursday (February 9). PM stock finished the day up 0.7%, and the share price remains 2.9% lower than a year ago:

| PM Share Price (Last 1 Year) Source: Google Finance (10-Feb-23). |

We initiated our Buy rating on PM in June 2019. Since then, shares have gained 53% (including dividends), including since the end of 2020, despite the much stronger dollar and the loss of earnings from Russia since 2022.

Q4 2022 results showed solid progress, with more to come in 2023. Adjusted EPS grew 11.9% in 2022 on a comparable basis, though down 12.9% if we include the impact of currency and Russia/Ukraine. Adjusted EBIT grew 10.3% in Q4 and 6.2% in 2022 organically. Heated Tobacco Units shipments grew 14.9% during the year, including 40.1% in the European Union, while Cigarette volume declines were broadly stable.

The new IQOS ILUMA has been a success, PM has broadened its Reduced Risk Products portfolio and is working on expanding in the U.S. For 2023, PM has guided to an ex-currency Adjusted EPS growth of 7-9%, despite cost headwinds. We expect PM to focus on growth investments and deleveraging in the next few years, with only token dividend increases and no buybacks. PM shares are at 19x 2022 EPS (excluding Russia and not pro forma Swedish Match) and a 5.0% Dividend Yield. Our forecasts indicate a total return of (47% (15.3% annualized) by 2025 year-end. Buy.

Philip Morris Buy Case Recap

PM combines a strong cigarettes business and a broad-based and growing Reduced Risk Products ("RRP") franchise.

We expect PM's cigarettes business to be stable, except where cannibalized by its own RRPs.

We expect PM's IQOS to continue its dominance of the Heated Tobacco category, by far the largest RRP category globally for existing tobacco companies. PM also owns ZYN, the dominant Modern Oral Tobacco product in the U.S., after acquiring Swedish Match ( SWMAY ) in 2022, and has launched its own Vapor products (including disposables).

With its acquisition of Swedish Match PM has re-entered the U.S. market, where it can convert existing smokers to RRPs without cannibalizing its own revenues. PM will regain the U.S. rights to IQOS from Altria ( MO ) after April 2024, and plans to apply for U.S. marketing approval for its VEEV Vapor product in H2 2023.

We believe PM can grow its Adjusted EPS at a CAGR of 9%+. Historically, PM targeted an (ex-currency) Adjusted EPS CAGR of 8-10%. 2021-23 targets, announced at the February 2021 investor day , include a revenue CAGR of at least 5%, an average annual EBIT margin uplift of 150 bps or more, and an EPS CAGR of at least 9% (excluding currency):

| PM 2 021-23 Financial Targets Source: PM investor day presentation (Feb-21). |

With the loss of earnings from Russia and Ukraine following the conflict there, PM now expects to achieve the same 2021-23 growth rates but on rebased earnings that exclude these countries.

New 2023-25 targets may be announced at the next investor day scheduled this September. We expect new medium-term targets to be similar or higher than historic targets. Swedish Match had historically grown its EPS at double-digits, its acquisition is expected to be low-single-digit EPS-accretive in year 1, and re-entering the U.S. market opens up a huge new profit pool for PM. However, there are also short-term costs associated with PM's new plans.

PM also has a Wellness & Healthcare business, consisting primarily of the Vectura and Fertin Pharma businesses it acquired in 2021 (for about $2bn in total). These have long-term potential but are not included in our forecasts.

Q4 2022 results showed operational performance is on track, despite near-term headwinds.

Philip Morris 2022 Results Headlines

In 2022, Adjusted EPS grew 11.9% on a comparable basis, as shown in the table below:

| PM Key Volumes & Financials (2022 vs. Prior Year) Source: PM results release (Q4 2022). |

Year-on-year comparisons are distorted by currency, the exclusion of earnings from Russia and Ukraine in 2022 (with the Russian business yet to be divested), and the acquisition of Swedish Match (which contributed 55 days of earnings in 2022). The different columns in the table represent different adjustments for these factors:

- "Actual" figures include currency, Russia/Ukraine and acquisitions

- "Pro Forma" figures exclude Russia/Ukraine from both periods, but include currency and acquisitions

- "Pro Forma ex-FX" figures are "Pro Forma" figures with currency also excluded

- "Organic" figures exclude currency, Russia/Ukraine and acquisitions.

We (and management) prefer the figures highlighted in blue, as they provide the most representative comparisons of operational performance. On these figures, PM total shipments grew 3.2%, Net Revenues grew 7.7%, Adjusted EBIT grew 6.2% and Adjusted EPS grew 11.9% year-on-year.

If we include the negative impact of currency and exiting Russia, then PM's Adjusted EPS fell 12.9% in 2022 (from $6.13 to $5.34), but with nearly all of the decline ($0.77 out of $0.79) due to currency, as the loss of $0.60 of EPS from Russia/Ukraine was nearly entirely offset by growth in the rest of the world.

In Q4 2022, following the same basis of comparison, Adjusted EPS grew by an even stronger 20.8% year-on-year:

| PM Key Volumes & Financials (Q 4 2022 vs. Prior Year) Source: PM results release (Q4 2022). |

Q4 showed a slightly lower volume growth, but much stronger revenue and Adjusted EBIT growth versus the full year, with Heated Tobacco Unit ("HTU") volume growth accelerating and offsetting a slightly larger cigarette volume decline.

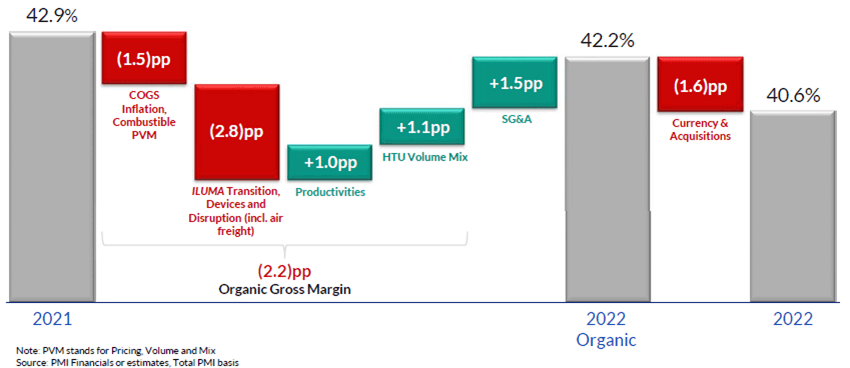

Philip Morris 2022 Cost Headwinds

PM's strong 2022 Adjusted EPS growth was in spite of significant cost headwinds, including currency, cost inflation, supply chain disruption (which necessitates the use of expensive air freight) and the initial dilutive impact from ILUMA:

{kind=link}

Together these mean PM's Gross Margin fell 2.2 ppt and its Adjusted EBIT margin fell 2.3 ppt in 2023.

Strong Heated Tobacco Unit Growth

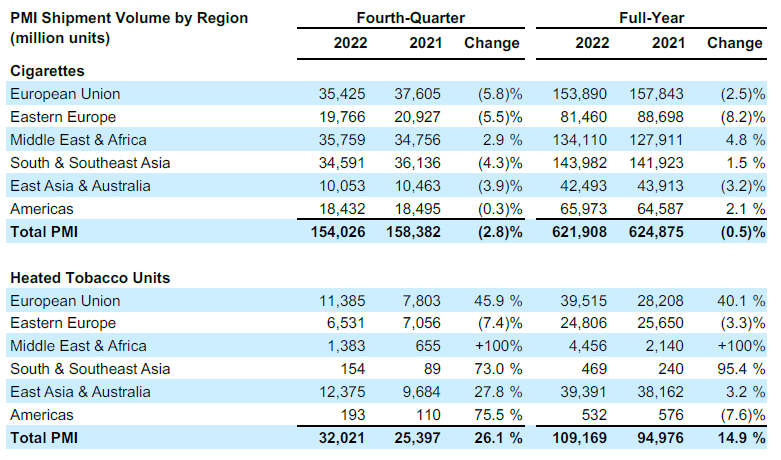

Including Russia and Ukraine, HTU volume grew 14.9% year-on-year in 2022 (including 26.1% in Q4, helped by inventory replenishments); excluding Russia and Ukraine, growth was even higher at 21.5% (including 37.5% in Q4):

| PM Heated Tobacco Unit Volumes (Q 4 & FY 2022 vs. Prior Year) Source: PM results release (Q4 2022). NB. Figures include Russia and Ukraine. |

{kind=link}

European Union saw HTU volume grew by 40.1% in 2022, overtaking East Asia & Australia (primarily Japan) as PM's largest HTU market by volume. Q4 also benefited from favorable shipment timing in advance of ILUMA launches.

Eastern Europe HTU volume fell 3.3% in 2022 due to declines in Russia and Ukraine, where PM is still operating but with no new investment and reduced inventory; excluding Russia and Ukraine, volume grew 18.5%.

East Asia & Australia HTU volume grew only 3.2% (and HTU revenues fell 4.6% excluding currency) in 2022, likely due to supply constraints earlier in the year. Growth has picked up in Q4 - management referred to "replenishment of inventories for ILUMA in Japan following lower shipments earlier in the year," and HTU volume grew 27.8% (while HTU revenues grew 10.3% excluding currency) during the quarter.

Broadly Stable Cigarette Volumes

Including Russia and Ukraine, total cigarette volume fell 0.5% year-on-year in 2022 (including 2.8% in Q4); excluding Russia and Ukraine, cigarette volume grew 0.8% in 2022 (but fell 2.2% in Q4):

| PM C igarette Volumes (Q 4 & FY 2022 vs. Prior Year) Source: PM results release (Q4 2022). NB. Figures include Russia and Ukraine. |

{kind=link}

PM cigarette volumes benefited from a continuing recovery in Emerging Markets following the shock from COVID-19. (Cigarette volume decline accelerated from 4.5% in 2019 to 11.1% in 2020, but was a resilient 0.6% in 2021.) Except in Eastern Europe, PM cigarette volumes fell no more than 3.5% or even grew in 2022 in every region.

Eastern Europe cigarette volume fell 8.2% in 2022 largely due to volume declines in Russia and Ukraine. Excluding these two countries, volume grew 0.1%.

ILUMA Driving Heated Tobacco Success

The new IQOS ILUMA has been a success, driving PM's growth in Heated Tobacco.

As CFO Emmanuel Babeau explained on the earnings call :

"ILUMA is driving volume and share growth across its markets … We launched in 8 new markets in Q4, including the Czech Republic, Italy, Portugal, and South Korea, bringing the total to 16. Markets with ILUMA launched now represent more than half of our total HTU volume … NPS scores (for ILUMA) on average increased by more than 10 points across its different market archetypes, and (it has) higher conversion rates compared to IQOS 3 DUO … in both Switzerland and the more recently launched United Arab Emirates, offtake share has almost doubled since launch"

In Japan , when Heated Tobacco found its first success at scale, ILUMA helped PM HTUs increase their share of the total tobacco market from 22.8% in Q1 2022 to 24.5% in Q4 (a much better performance than British American Tobacco's ( BTI ) glo, which finished 2022 with the same 7.5% share it started with):

| PM HTU Share of Tobacco Market & Volume - Japan Source: PM results presentation (Q3 2022). |

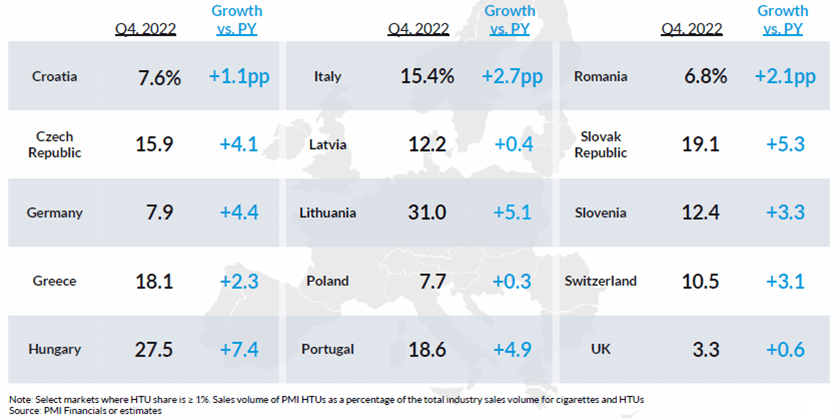

In Europe , PM HTU has continued to gain share in key markets, including in Germany (now 7.9%, up 4.4 ppt year-on-year) and Italy (15.4%, up 2.7 ppt):

| PM HTU Offtake Share in Selected E.U. Countries (Q 4 2022) Source: PM results presentation (Q4 2022). NB. The U.K. is reported in PM's E.U. region. |

{kind=link}

Supply chain issues on ILUMA are expected to "gradually improve" through H1 2023, and PM plans to "progressively" launch the new device in more geographies. PM continues to expect to file a PMTA for ILUMA in H2 2023.

Broadening Reduced Risk Products Portfolio

PM has now broadened its Reduced Risk Products portfolio into lower-income segments and other categories.

In Heated Tobacco , PM has extended its collaboration with KT&G ( KTCIF ) last month, and will continue to be the exclusive seller of the latter's Lil outside South Korea, as a lower-end product that complements its premium IQOS product. (PM Is already selling Lil in more than 30 markets.) Similarly, its BONDS by IQOS line, intended for low- and middle-income countries, has been launched in the Philippines and Columbia in Q4.

In Modern Oral Tobacco , PM has Swedish Match's ZYN as well as its own Shiro product. ZYN continues to dominate the category in the U.S., with a volume share of 67.5% and a value share of 75.7% in Q4. PM "now together have a plan" with Swedish Match to address the European market and will also be launching ZYN in other international markets. (Though Swedish Match, PM is now also selling Traditional Oral Tobacco Products in both the U.S. and the Nordic.)

In Vapour , PM has its VEEV product and VEEBA disposable product, though these are still in early stages. VEEV was last reported to have been launched in 10 markets, including France and Italy, while VEEBA has been launched in Canada, but there has been little data on progress. VEEV was reported by PM as the #2 in the closed category in Italy, with a 20% share, as of Q2 2022; but BTI described the disposable Vapor market in Canada as "immaterial." PM still plans to submit a PMTA for VEEV in 2023.

Active Working on U.S. Expansion

PM is actively working on expanding in the U.S., as CFO Emmanuel Babeau explained on the call :

"A key focus this year will be supporting and further driving strong ZYN growth in the U.S. … In parallel, we will be actively enhancing Swedish Match's U.S. distribution and commercial capabilities for the launch of IQOS in 2024."

We believe ZYN will continue winning in the U.S. in a growing category, IQOS stands a good chance to succeed at scale in 2025 as it has now done in Europe and Japan, while VEEV and VEEBA are more long-term prospects.

Philip Morris 2023 Outlook

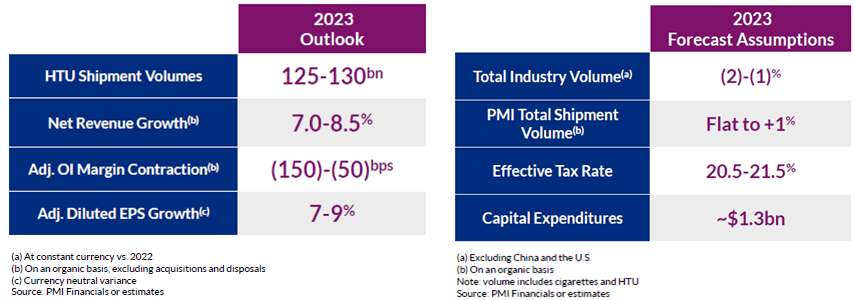

For 2023, PM has provided an outlook that includes, on an ex-currency basis:

- Total Shipment growth of zero to 1%

- Net Revenue growth of 7.0-8.5%

- Adjusted EBIT margin decline of 150-50 bps

- Adjusted EPS growth of 7-9%.

{kind=link}

The 7-9% Adjusted EPS growth includes a low-single-digit benefit from the Swedish Match acquisition, so is in fact lower than PM's historic range due to certain cost headwinds described below.

Growth is expected to be H2-weighted, due to shipment timing, progress on ILUMA, prior-year comparisons, etc. Growth is expected to be the weakest in Q1, with organic revenue growth to be just low-single-digits.

Operating Cash Flows are expected to be $10-11bn in 2023, compared to $10.8bn in 2022.

On the positive side, PM is expecting relatively resilient cigarette industry volumes (down 2% to 1%), strong growth for its HTU volumes (15-19%, from 109.2bn in 2022) and ILUMA supply constraints easing gradually in H1.

On the negative side, PM is expecting significant headwinds on its COGS margin (from ILUMA as before, but also a new factors including leaf, acetate tow, salaries and energy), an additional $150m investment (50/50 split between the U.S. and Wellness & Healthcare), though SG&A margin is expected to stay flat. CapEx is expected to be $0.2bn higher at $1.3bn.

2023 Adjusted EPS is expected to be $6.25-6.37. Russia and Ukraine will be included in 2023 reporting, due to an "increasingly challenging and complex" environment for divestment, so they are included in the 2023 outlook too. However, these countries are now a drag on growth, and EPS growth will be higher without them.

2023 Adjusted EPS excluding Russia and Ukraine, if we assume their $0.64 contribution in 2022 is expected to grow 7% in 2023, is implied to be $5.57-5.69.

The potential benefit of an ongoing court case in Germany, regarding a surcharge on Heated Tobacco, is not included. A favorable outcome would mean an extra 1 ppt in revenue growth, 3 ppt in Adjusted EP growth and Operating Cash Flows moving to the upper half of the guided range.

Valuation: Philip Morris Dividend And P/E

At $102.02, relative to 2022 earnings excluding Russia/Ukraine, PM shares have a 19.1x P/E, which slightly overstates PM's valuation slightly as Swedish Match only contributed 50 days of earnings in 2022; relative to 2023 outlook with Russia/Ukraine adjusted out, PM shares have a 18.1x P/E:

| PM Net Income, Cashflow & Valuation (20 2 1 -2 3 E) Source: PM company filings. |

PM Free Cash Flow ("FCF") Yield is 6.1% on 2022 FCF (overstated by including Russia/Ukraine but understated by not adjusting for Swedish Match) and 5.8% on 2023 guided FCF (overstated by including Russia/Ukraine).

The Dividend Yield is 5.0%, based on a dividend of $1.27 per quarter ($5.08 annualized). The dividend was raised by just 1.6% in September. The implied Payout Ratio, relative to the mid-point of 2022 Pro forma Adjusted EPS, is 95%, but expected to return to PM's 75% target over time as EPS grows.

Share repurchases have been suspended as PM deleverages after borrowing to acquire Swedish Match. Net Debt / EBITDA was 2.89x at 2022 year-end and, when PM last resumed its buybacks at Q2 2021 results, its Net Debt / EBITDA was at 1.74x. PM is unlikely to have deleveraged sufficiently to resume buybacks until after 2025:

| PM I llustrative Net Debt / EBITDA Calculations (2022-25E) Source: Librarian Capital estimates. |

We expect PM to focus on growth investments and deleveraging in the next few years, with only token dividend increases and no buybacks.

Philip Morris Stock Forecasts

With IQOS still growing strongly and Swedish Match now part of PM, we update our forecasts to include a higher growth rate and a higher exit multiple, but removed buybacks to allow deleveraging. Our new assumptions now include:

- 2023 EPS to be mid-point of new outlook (excluding Russia/Ukraine)

- Net Income to grow at 8% in 2024 (was 7%)

- Net Income to grow at 9% in 2024 (was 7%)

- Share count to be flat (was falling 2% annually)

- Dividends to grow at 2% annually (no change)

- P/E at 17.0x at 2025 year-end.

Our new 2025 EPS is 3.6% lower than before ($6.87), with the higher Net Income growth assumption offset by a lower starting EPS in 2023 and the removal of buybacks:

| Illustrative PM Return Forecasts Source: Librarian Capital estimates. |

With shares at $102.02, we expect an exit price of $132 and a total return of 47% (15.3% annualized) by 2025 year-end.

Is Philip Morris Stock A Buy? Conclusion

We reiterate our Buy rating for Philip Morris International Inc. stock.

For further details see:

Philip Morris: Solid Q4, Multiple Growth Drivers For 2023 Onwards