SEMHF - Philips Q3 Earnings: Getting More Attractive (Rating Upgrade)

2023-10-25 18:06:52 ET

Summary

- Philips N.V. has been grappling with a significant setback due to the Respironics device recall, which has had widespread consequences both in terms of financial damage and reputation.

- Despite these challenges, Philips demonstrated a strong financial performance in Q3, with robust sales growth and significant margin improvements.

- The company has made substantial progress in addressing supply chain issues and cost-saving initiatives, which contributed to notable improvements in its margins and cash flow.

- The decrease in order intake poses challenges for medium-term growth and raises questions about the company's ability to meet its growth targets.

- For investors with an above-average risk appetite, I believe Philips shares now offer an interesting investment opportunity with the potential for solid double-digit annual returns.

Investment thesis

I move my rating on Koninklijke Philips N.V. ( PHG ) from Hold to Buy, despite the FDA being unsatisfied with Philips’ test results of the foam in its recalled apnea devices. Meanwhile, the company’s Q3 results exceeded expectations but were clouded by another quarter of negative order intake growth.

Philips has been grappling with a significant setback due to the Respironics device recall, which has had widespread consequences both in terms of financial damage and reputation. The recall has already cost the company €1.5 billion, and the risk of further financial losses remains large, with some analysts estimating potential damages of up to €4 billion. The FDA's dissatisfaction with Philips' testing results adds to the uncertainty and financial burden.

Despite these challenges, Philips demonstrated a strong financial performance in Q3, with robust sales growth and significant margin improvements. The company has made substantial progress in addressing supply chain issues and cost-saving initiatives, which contributed to notable improvements in its margins and cash flow.

However, it's important to acknowledge that there are lingering concerns, particularly regarding order growth, which has been persistently negative. The decrease in order intake poses challenges for medium-term growth and raises questions about the company's ability to meet its growth targets. The impact of these challenges appears to be company-specific, as competitors report better order intakes.

In this article, I will take you through my analysis of the company and the underlying industry, as well as the latest developments and financial projections.

The Respironics device recall continues to cause problems for Philips, with the FDA unsatisfied

Let's start with the elephant in the room – the Respironics device recall because of a toxic foam breaking off inside the machines. According to reports, Philips has been aware of the problem since 2015 but only first reported it in 2021. Since then, the FDA has received 98,000 complaints from Philips ventilators and respiratory device users. Some complaints included reports linking the devices to cancer, respiratory problems, pneumonia, chest pain, dizziness, and infections. The FDA even linked 346 deaths to the foam problems.

The recall has caused plenty of headaches for Philips and its shareholders and has already caused significant financial damages, totaling €1.5 billion so far. And yet, the problem is far from resolved, even after an agreement to settle certain legal claims in the U.S. for a little under €500 million (for a full in-depth discussion of the recall, I recommend reading my previous and initial article on Philips ).

Philips has already spent over €1 billion recalling all the apnea devices in question, which amounts to over 5.5 million devices. During the most recent earnings call , management confirmed that 99% of the sleep therapy device registrations that are complete and actionable have been remediated. Furthermore, according to Philips Respironics and third-party experts, the use of the devices and the breaking off of the foam is not expected to result in appreciable harm to the health of patients. If correct, this would protect Philips from the pending lawsuits regarding patient damages.

However, earlier this month, the FDA stated that Philips had not shared sufficient details with the regulator regarding a major recall of its sleep apnea and respiratory care devices. According to the FDA, the foam testing done by Philips is not adequate to fully evaluate the risks posed to users by the recalled devices. This means the FDA requires additional testing by Philips, further increasing costs for Philips linked to the recall. Shares fell as much as 9% in response to the news, which poses another drag on Philips’ financials and means the matter is still far from resolved.

The risk for further financial damages remains large. Some analysts even believe this could run up to a total of €4 billion . As long as the FDA is not satisfied with the testing results and does not acknowledge the results from Philips, the financial risk of personal injury claims remains present. For now, Philips has said it continues to work with the FDA and it has agreed to further testing.

It is no secret that Philips has dealt with the situation poorly by not launching an investigation until 2019 and keeping investors in the dark regarding the financial impact and size of the issue for much of the last two years. It will take the company some time to regain investor trust, and I expect sentiment around the shares to remain negative, especially as bad news keeps emerging.

The management change might contribute to renewed trust in the company’s management. However, new CEO Roy Jacobs previously led the Connected care business, including Respironics, arguably making him one of the people responsible for the whole debacle, highlighting one of Philips’ fundamental problems.

The deterioration of Philips over the years has made it perfectly clear the company has not been managed correctly. To then hire an insider from a broken company/system seems like a wrong move, and hiring an outsider with a fresh vision would have made a lot more sense to me. Overall, this gives me little confidence in the company moving forward.

Possibly even more important, the company will also need to work hard on regaining patient trust in its Respironics devices to maintain its market share of above 60% . It is not hard to see that these large worldwide reliability problems of Philips could damage its brand name and the trust users have in its devices. As a result, I am expecting it to impact its market share, at least in the short to medium term, impacting its connected care financial results.

Last quarter, growth in its connected care segment was solid at 10%, but Respironics was only flat YoY, while competitors are reporting growth. On that note, let’s look closer at its Q3 results.

Philips reported solid Q3 results

While the Respironics debacle continues to be a drag on sentiment, the company seems to be doing quite well financially, although not on all fronts.

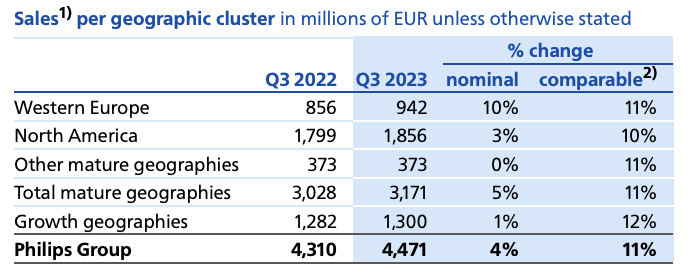

Philips reported strong comparable sales growth in Q3 , up 11% YoY to €4.5 billion. The company had been dealing with significant supply chain problems in the last two years, but these are now largely resolved, allowing the company to play catch up and report strong growth YoY.

Growth was driven by all regions and segments with 14% growth in Diagnosis and Treatment, 10% growth in Connected Care, and 7% in Personal Health. All regions saw sales increase by double digits, between 10% and 12%.

Philips Q3 revenue by region (Philips)

{kind=link}

While I might be quite critical of the company and its management team due to developments in recent years and the lack of successful execution and innovation, factors Philips used to be known for back when it was a global electronics leader, there are definitely also positives to find here. The company is heavily focused on improving its supply chain and improving the operating model by making the company more agile and simplified, which should eventually lead to more stability and margin improvements, which seem to be materializing today.

YTD, Philips has already delivered €685 million in cost savings, driven by productivity initiatives, including the layoff of 7500 workers as part of the plan to lay off 10,000 employees by 2025. These cost savings have resulted in solid margin improvements in Q3 with the group adjusted EBITA margin up 540 basis points YoY to 10.2%, meaning Philips is already close to its 2025 low-teens AEBITA margin target. The YoY increase was driven by 240 basis points from operational leverage (offsetting the 250 basis points increase in wage and component price inflation) and by productivity and pricing actions, which contributed a further 540 basis points.

Philips' growth targets (Philips)

The personal health segment reported the strongest EBITA margin of 18.7%, up 460 basis points YoY, driven by operational leverage, pricing, and productivity measures. The diagnosis and treatment EBITA margin was 12.7%, an increase of 230 basis points, and Connected Care adjusted EBITA margin was 3.7%.

These margin improvements drove a solid increase in operating cash flow to €489 million and allowed the reported net income to turn positive again, from a negative €1.5 billion in the same quarter last year to a positive €90 million last quarter, resulting in €0.33 in EPS.

However, despite these improved cash flows, the balance sheet remains quite leveraged, and considering the lawsuits and costs of further testing hanging over its head, the net debt level and low cash position sit above my comfort level. As of the end of Q3, Philips held total cash of €1.2 billion and total debt of €8.2 billion, resulting in a net debt position of €7 billion.

Luckily, free cash flow turned positive again in Q3, and should further improve in the quarters ahead, which could offer some support here. Q3 FCF was €333 million, driven by higher earnings and improved working capital management. This brings the YTD total to €454 million.

The order intake continues to disappoint

While Q3 results excelled with solid sales growth and significant margin improvements, this was clouded by another quarter of negative order growth, resulting in the share price falling 4% following the release of the earnings report.

The order intake in Q3 was down 9% YoY, bringing the YTD total to a negative 6%. This decrease was driven by healthcare systems in the US and other mature geographies remaining cautious in their buying behavior in the short term as a result of high costs and decreased consumer spending. In addition, China is heavily impacted by government-initiated anti-corruption measures, resulting in significantly lower orders from the country’s healthcare systems.

Philips sees this China headwind as temporary and believes it should not impact fundamental demand from the country. Prior to these measures earlier this year, Philips reported order and revenue growth in the double digits from China and expects demand to remain strong as these short-term headwinds pass.

Furthermore, management pointed out that the order book remains 20% above the Q3 2021 level, although this is in part the result of supply chain issues leading to depressed sales growth in the last two years. While this is promising for its short-term growth, it doesn’t illustrate anything material.

The depressed order intake paints a negative picture for its medium-term growth, meaning that if this persists, Philips will have trouble meeting its medium-term growth targets. Furthermore, while Philips blames this on the macroeconomic environment and tough comparables, competitors are simply reporting a much better order intake, indicating that the problem might be company-specific, making me somewhat more conservative in my growth expectation for Philips in the medium term.

On a more positive note, the order intake is only of importance to 40% of the group sales as the other 60% is derived from recurring revenue streams, such as services and consumables and book-to-bill businesses. So, even if orders remain depressed, the company’s sales should be somewhat resilient as the recurring business offers stability and is much stickier.

Outlook & PHG stock valuation

The better-than-expected Q3 results reported by Philips also allowed management to increase its FY23 guidance for both sales and profitability. Therefore, management now guides for 6% to 7% comparable sales growth and an adjusted EBITA margin between 10% and 11%, up from mid-single digits and a high-single-digit EBITA margin.

However, this guidance still implies a modest performance in Q4 with sales growth decelerating to the low-single-digits and only little YoY margin improvements. This trend will likely persist going into FY24, making me less optimistic about the FY24 sales growth and margin expansion.

Also, based on the current inflow and visibility, the order intake is expected to show a sequential improvement in Q4 but will most likely still be down YoY.

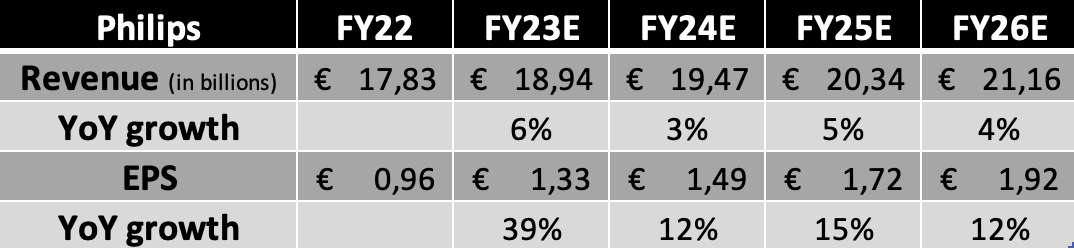

Overall, I slightly adjusted my financial projections, considering the upgraded FY23 guidance and improved margins. Meanwhile, my long-term projections remain largely intact.

Financial projections (Author)

{kind=link}

Following the FDA comments from earlier this month and the disappointing order intake, Philips shares are down another 15% since I last covered the company, meaning shares are now down 50% over the last five years. Furthermore, this means the valuation has also come down further, with shares now valued at a forward P/E of 13x. This sits significantly below its 5-year average P/E of 22x and peers General Electric Healthcare ( GEHC ) and Siemens Healthineers ( SMMNY ), which sit at a P/E of 17x and 23x, respectively.

Of course, the undervaluation itself is not a surprise considering the significantly worse order intake, supply chain problems, and the overhang of further lawsuits regarding the apnea device recall. Philips continues to face significant threats, and the news that the FDA is still not convinced by Philips’ testing results is a negative indication of what is ahead.

Furthermore, its peers are ahead of it in terms of innovation and are seeing stronger demand for their products. Therefore, the discount Philips is trading on is fully justified as the company has a far worse risk profile. So, even as the company should be able to grow EPS at double digits in the medium term, a 13x earnings multiple is the maximum investors should want to pay for these shares today to price in the risks involved.

Based on a 13x earnings multiple and my EPS expectation for next year, I calculate a target price of €19.37 (down from €21). Going with an annual return of 11%, I believe the fair value share price sits around €17, meaning shares are currently trading around fair value.

Therefore, despite my overall negative view of Philips, I upgraded my rating to a buy as I believe the risks involved are now correctly priced into the share price following another 15% decline. For investors with an above-average risk appetite, I believe Philips shares now offer an interesting investment opportunity with the potential for solid double-digit annual returns.

For further details see:

Philips Q3 Earnings: Getting More Attractive (Rating Upgrade)