DCP - Phillips 66: Blending Barrels Of Cash

2023-03-20 18:03:10 ET

Summary

- Refinery capacity in the U.S. is stressed to serve the market with needed gasoline and jet fuels, leading to high profit margins.

- Following the Phillips 66 acquisition of DCP Midstream, profits and stability are expected to grow.

- Phillips 66 has committed to delivering $8 billion back to shareholders through 2024. I'll show how this is just the tip of the iceberg.

Thesis

Phillips 66 ( PSX ) is traditionally a refining company, taking crude oil and processing them into the usable forms like gasoline, diesel, jet fuel, heating oils, etc. This industry has been underinvested over the last 10 years, and this has resulted in marginal refining capacity left in the United States. This has allowed refiners to capture excellent margins due to a supply and demand imbalance.

Shareholders will find improved stability and returns in the coming years thanks to the acquisition of DCP Midstream, LP. This will provide additional cash flows and stabilize its earning potential, making it less susceptible to the ups and downs of refinery spreads.

The company sees the refinery market as mid-cycle, and thus has committed to returning $10 to $12 billion back to shareholders by the end of 2024. I will show that even if refinery profitability falls by 40%, PSX will still generate $6 billion in cash available to shareholders beyond the $10 billion mark established by management. The current market volatility in oil prices provides attractive entry points for long term shareholders.

Elevated Margins

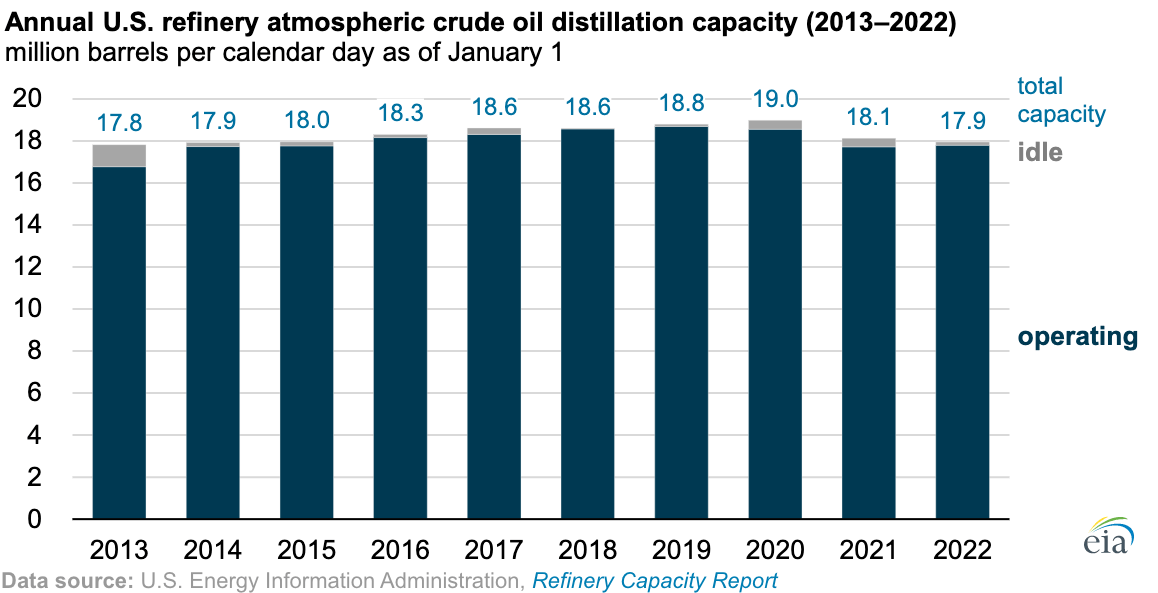

As a whole, the refinery industry has gotten smaller since the pandemic. Total refinery capacity has actually shrunk to 2014 levels as a result of under investment in the industry and closures . We are now entering the hangover period from the pandemic. The sudden shock to the industry resulted in refiners closing up shop, and those who stayed in business put off large maintenance projects to stay afloat. It is now time to pay the piper with longer maintenance outages and little excess refinery capacity.

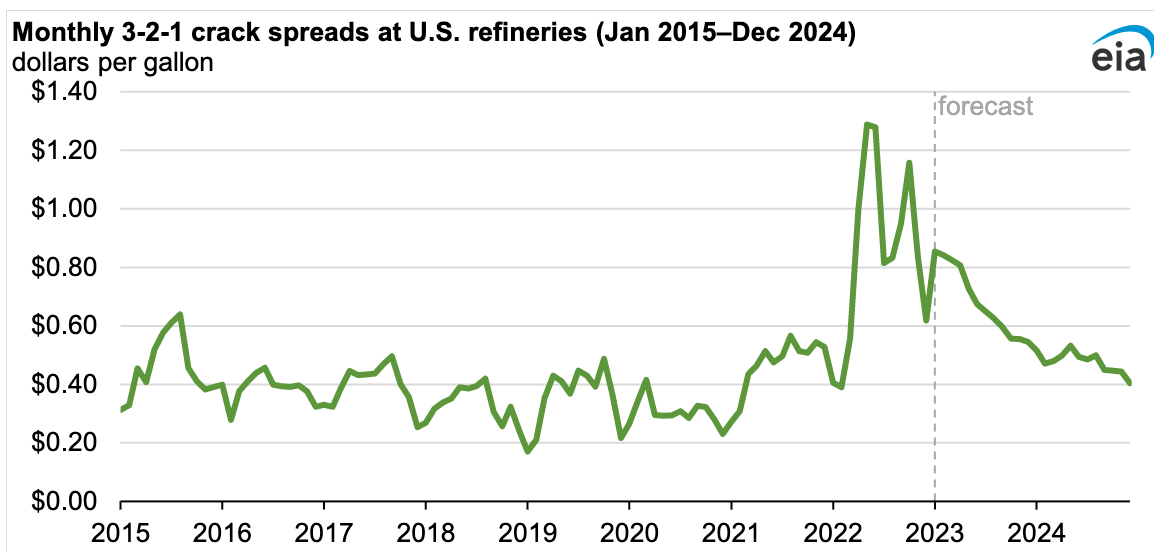

Supply and demand will always find a balance point. As a result of this shrinking supply, refiners' margins have increased. The EIA projects the 3-2-1 crack spread to remain elevated for 2023 before settling back into its normal range by mid-to-end of 2024. As of 3/16/23, crack spreads are trading at $35/barrel or roughly $0.83/gallon, significantly higher than the pre-pandemic levels of $0.30 to $0.40/gallon.

U.S. Refinery Capacity (EIA) 3-2-1 Crack Spreads (EIA)

{kind=link}

{kind=link}

Making PSX Great Again

The company has a target of reducing costs by $500 million annually. This will be accomplished by improving utilization rates and using improved technology to cut costs.

PSX has struggled compared to its peers in terms of mechanical availability and utilization of its refineries. Since 2020, PSX utilization has lagged the industry average by 2-3%. This is clearly an area that PSX has been leaving money on the table. As such, PSX is taking steps to improve the availability of its refineries, pushing toward a goal of 98% available in 2025. This would be a marked improvement from the 90% utilization that was achieved in 2022. While this is a lofty goal, this is not uncharted territory. Utilization rates were 94% before the pandemic, and thus, there is definitely still meat on the bone.

The company is also employing new technology to reduce costs and outage time. Innovations such as rejuvenated catalysts and catalysts that consume less natural gas are being employed to reduce the operating cost structure. PSX is also completing digital monitoring upgrades to ensure equipment failures occur less often and do not cause system disruptions. All of these improvements should translate to the bottom line.

Green offshoots

PSX aims to improving overall production beyond just optimizing the assets that are already in the portfolio. The company expects to capture an additional $700 million through the redevelopment of the Rodeo refinery in California.

The revamped refinery will generate renewable diesel and jet fuel to monetize the Inflation Reduction Act while lowering overall emissions. The feedstock for the refinery will use cooking oils, canola, or soybean oils, and thus is entitled to the associated LCFs and RINs that are awarded to a green fuel source. This is expected to be placed into operating in 2024 and is being done in a capital efficient manner by retrofitting the old style refinery, instead of starting from green space.

Midstream Adds Dependability

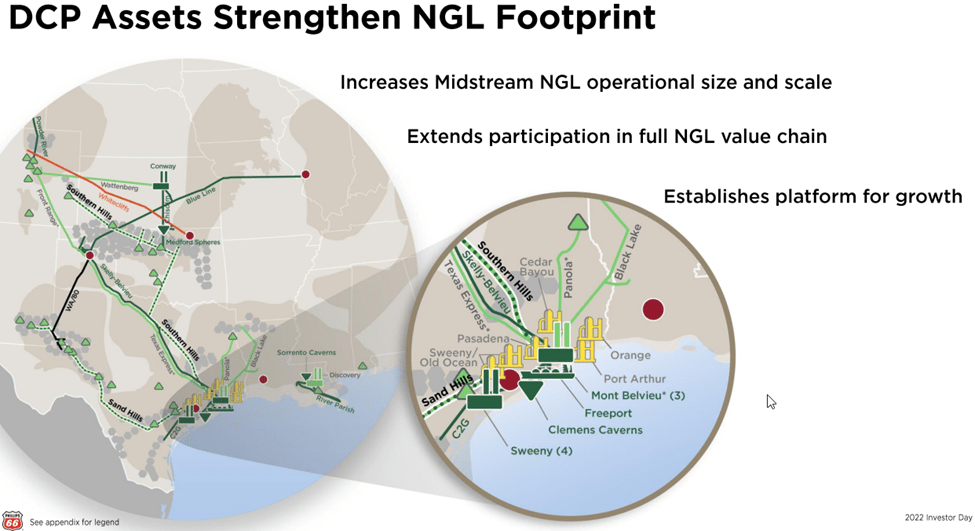

PSX is no longer just a refinery company. Following the DCP acquisition, the company owns or operates 72,000 miles of pipeline to transport products such as crude oil, refined products, NGLs, or Natural Gas to its export terminals. This allows the company to extract profits at every phase of the value chain from the wellhead to the docks, making it ideal for energy producers to transport using the PSX system.

PSX will now be able to transport and process molecules from a multitude of basins to the gulf coast. This will be needed to help meet the export demand to supply the world with cost-advantaged U.S. natural gas and NGLs. The system will directly link the Delaware, DJ, Anadarko, and Haynesville basins to the Sweeny and Mont Belvieu fractionators for export via the Freeport export terminal.

Midstream Operational Map (PSX 2022 Investor Presentation)

{kind=link}

Following the merger, the Midstream segment will operate as the backbone to the company. In general, midstream companies have stable cash flows, thanks to take-or-pay style contracts. Cash flows remain relatively stable even when there are disruptions in the energy market. The newly formed midstream segment generated $4.7 billion or 41.6% of net income in 2022, making it a meaningful contributor to the bottom line moving forward. Management expects a $1.3 billion EBITDA build thanks to commercial and operational synergies.

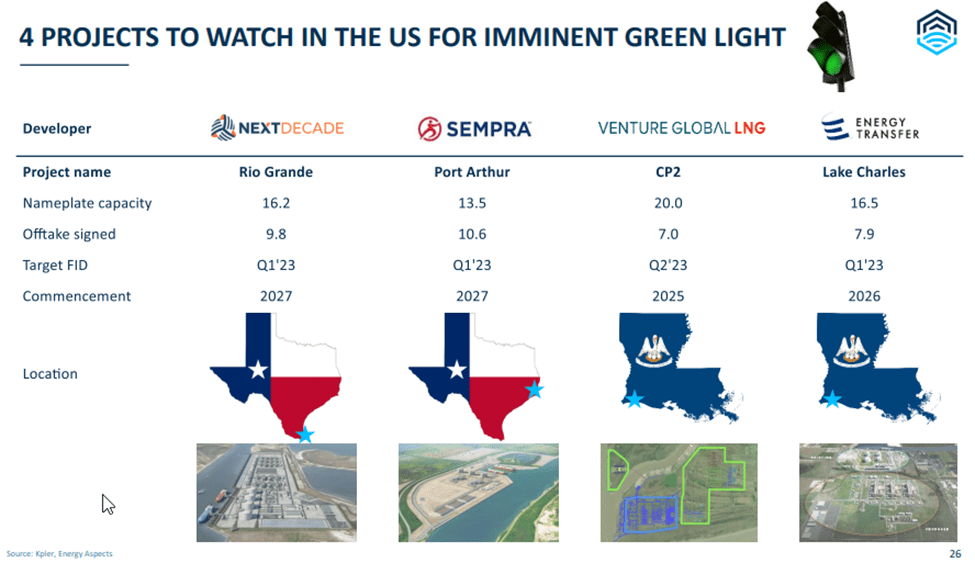

To build on that momentum, these assets have a demand pull starting to develop on the horizon. There are multiple export projects being developed on the gulf coast that will require the ability to process, transport, and separate the molecules in the natural gas product stream. Below is a snapshot of some of the projects under development in the gulf coast area.

LNG export projects (FLEX LNG)

{kind=link}

Midstream Margin Expansion

I detailed in a previous article how the midstream conglomerate, Enterprise Products Partners L.P. ( EPD ), would benefit from this uplift in demand for NGL and natural gas processing. PSX will be no exception after this bolt on deal, as they operate similar assets. The supply and demand fundamentals of the NGL value chain are extremely tight. For example, EPD has 11 operation fractionators, all running at nearly 100% capacity. When demand outstrips supply, margins will expand in this space.

PSX is in the same boat as EPD. The NGL capacity of the former DCP pipeline system is 895 MBBL/d. The volumes transported in 2022 were 705 MBBL/d. The addition of Sweeny Frac 4 (150 MBBL/d capacity) will drive NGL pipeline volumes to roughly 95% capacity while boosting volumes through the entire processing and Natural Gas transportation system.

The $10 Billion (or more) Promise

In November 2022, PSX committed to delivering between $10 billion and $12 billion in shareholder returns between the middle of 2022 and the end of 2024. As of the Q4 conference call , $2.4 billion of that has been complete. For arguments sake, we will assume the final payout is $10 billion, leaving $7.6 billion remaining over the next 24 months.

The company plans to execute this via two mechanisms, dividends and buybacks. As of today, the dividend is a respectable $1.05 per share (4.4% at $95/share). The second arm of the cash return model is currently authorized to buyback more than $6 billion worth of shares (or roughly 13% of the shares outstanding at $95/share)

PSX has been a faithful steward of its dividend. In a recent interview at the Scotia Howard Weil Energy Conference, CEO Mark Lasher spoke music to any dividend investors ears (emphasis added):

And we had a hiatus from share repurchases during COVID. We consistently grew our dividend throughout COVID, so we didn't back off our dividend. We -- that's the promise we make. And we tend to view our dividend as an irrevocable promise. And so we're cautious about increasing that dividend. But at the pace of share repurchases we're making today, we see that incremental dividend cash being fairly consistent. So we'll increase the dividend per share over time. But as we repurchase shares, take those off the table. That will be a consistent amount at about right at $2 billion a year. And so that's the near-term shareholder return commitment that we made

If that doesn't make the dividend investor's heart sing, I don't know what will.

Underpromise, Overdeliver

If we look at the cash flow statements in the 10-K report(page 100) , we get a very good understanding of how cash is generated and deployed for PSX. In 2022, PSX generated $11 billion in net income. Cash reserves went up by $3 billion, so where did it all go?

- $2.5 billion spent on debt repayments

- $1.5 billion spent to repurchase of common stock

- $1.8 billion spent to fund the dividend

- $2.2 billion spent on CAPEX.

Management has been very clear that it plans to repurchase about $2 billion worth of shares a year over the next two years, while also committing to maintaining the annual payout of the dividend at $2 billion.

They also expect profitability to rise over this time period as well. Earnings growth will be generated from the stated cost control measures, as well as increased revenue from the midstream business and the Rodeo renewal project. The table below summarizes the cumulative effect of all of these variables.

| 2023 |

| 2024 |

| Cost Controls |

| $250M |

| $500M |

| Midstream Efficiencies |

| $500M |

| $1000M |

| Rodeo Renewed |

| $0 |

| $500M |

| Changes in refinery margins |

| ($1,560M) |

| ($3,120M) |

| Changes in net income |

| ($810M) |

| ($1,120M) |

For conservatism, I projected an annual 20% decline in refinery margins, so we don't get comfortable with the elevated margins we are seeing now. All due debt maturities were also assumed to be repaid. Using the next table, we can see how this will translate to shareholder returns and net income.

| 2022 |

| 2023 |

| 2024 |

| Net Income |

| $11B |

| $10.2B |

| $9.9B |

| Repayment of Debt |

| ($2.5B) |

| ($0.5B) |

| ($1.1B) |

| Repurchase of Common Stock |

| ($1.5B) |

| ($2.0B) |

| ($2.0B) |

| Dividends paid on Common Stock |

| ($1.8B) |

| ($2.0B) |

| ($2.0B) |

| CAPEX |

| ($2.2B) |

| ($2.0B) |

| ($2.0B) |

| Net Cash |

| $3B* |

| $3.7B |

| $2.8B |

*Will be used to fund the DCP acquisition .

This all means that after returning $8 billion to shareholders over 2023 and 2024, PSX will still have the opportunity to amass over to $6 billion in cash. All of this is accomplished with declining refinery margins by 40%. I also trimmed $250 million from expected returns of the Rodeo Renewal Project.

The company has a general stance of returning 40% of its profits to the shareholders at a minimum. I project that as we move through 2023, PSX will advance the pace of its buybacks, expand the buyback authorization as well as its dividend payout. Given the current market conditions, I feel this is a significant avenue to capture appreciation in the PSX stock price while also collecting a moderate dividend payout.

Risks

The most obvious risk would be a decline in crack spread leading to a rapid decline in refinery profitability. The oil and gas industry is notorious for being cyclical and investors do not want to be caught on the wrong side of the cycle. My analysis baked in an overall 40% reduction in refinery margins and reduced income growth to provide some conservatism. If margins were to fall greater than that, there remains sufficient margin ($6 billion worth) for management to deliver on its shareholder return model.

An additional risk would be an unsuccessful venture with the Rodeo Renewed project. Since this is largely a regulation play, the overall direction of the project could change with the wind. Removal of all profitability expectations for this project still yields excess cash generation of almost $6 billion.

If both of these scenarios pan out simultaneously (say a large scale recession environment), I believe sufficient margin exists to deliver even the high end of $10-$12 billion earmarked for shareholder returns. Too much margin to this number exists to say it is not executable under a wide range of market conditions.

Summary

Phillips 66 has made moves to strengthen its cash generation profile. The acquisition of DCP Midstream improves product diversification as well as cash flow stability. I really like the softening of any potential refinery volatility that the midstream segment provides. It makes PSX less of a boom-and-bust investment and significantly more reliable.

I believe that there is sufficient evidence to conclude that Phillips 66 shareholder returns will exceed $12 billion in a meaningful way by the end of 2024 (possibly as much as $4 to $5 billion if refinery margins drop less than I have projected). The current model provides the opportunity to capitalize on an undersupplied refinery market while also enjoying stability and growth of the NGL market through the midstream segment. I value Phillips 66 as a strong buy under $100/share and a moderate buy under $110/share.

For further details see:

Phillips 66: Blending Barrels Of Cash