PHK - PHK: A Very Good Bond Fund But Very Expensive Given The Risks

2023-09-11 15:09:27 ET

Summary

- The PIMCO High Income Fund offers a high current yield of 11.90%, one of the highest in the market.

- The PHK closed-end fund has not cut its distribution despite the negative impact of rising interest rates on bond prices.

- The fund's portfolio is heavily invested in speculative-grade bonds, but the real risk here is that interest rates will continue to rise.

- This is one of the few fixed-income funds that has been able to cover its distributions over the past year, indicating that the market may be wrong about a potential cut.

- The fund is trading at an incredibly large premium to net asset value, so it might not be worth the risks.

The PIMCO High Income Fun d ( PHK ) is a very popular closed-end fund, or CEF, among those investors who are seeking a high level of income from their portfolios. There are some good reasons for this, as the fund's 11.90% current yield is one of the highest yields available in the market today. This high yield is largely a result of the fund's very disappointing performance in the market. Since the start of 2022, the fund has declined a whopping 22.56% in the market:

{kind=link}

This is not out of line with most other bond funds, though, as the rising interest rate environment has had a substantial negative impact on bond prices. However, the PIMCO High Income Fund has not cut its distribution in response to the weakening in the bond market, which is in sharp contrast to many other funds. This might be one reason why the market seems concerned that it will not be able to sustain its payout going forward. As I pointed out in my last article on this fund, any time an asset achieves a double-digit yield, it is a sign that the market is concerned about the sustainability of its distribution. This fund did actually manage to cover its distribution during the second half of 2022 though, which speaks well to the quality of PIMCO's management team.

The fund recently released its full-year financial report , so we should revisit this fund and determine if its distribution is still sustainable or if it is at risk of a cut. However, even if the distribution does prove to be sustainable, the fund might still might not be the best investment today. In particular, this fund is incredibly expensive right now and is trading at a price that is significantly above the intrinsic value of its shares. As such, most value investors will probably walk away disappointed.

About The Fund

According to the fund's website , the PIMCO High Income Fund has the objective of providing its investors with a high level of current income. This is not surprising considering that this is a fund from PIMCO, which is generally known for its bond funds. This one is certainly no exception to that as the fund's assets are primarily invested in bonds. It does, however, have some allocation to common and preferred stocks:

CEF Connect

We do see a negative allocation to cash here. This comes from the fact that this fund employs leverage in the pursuit of its investment objective, which we will discuss later in this article. The most important thing to consider right now is that the PIMCO High Income Fund is a fixed-income fund, and as the name implies, fixed-income securities deliver the overwhelming majority of their investment return in the form of direct payments to their investors. After all, a bond investor will purchase a bond at face value when it is first issued, receive a regular coupon payment from that bond, and then receive face value again when the bond matures. The coupon payment is the only investment return that these securities deliver over their lifetime. This makes the fund's secondary objective of capital appreciation rather strange because bonds do not deliver any net capital appreciation over their lifetimes as they have no inherent link to the issuing entity.

With that said, it is possible to make some capital gains by exploiting changes in bond prices that come with interest rate swings. I explained this in my previous article on the fund:

"Bond prices are extremely sensitive to interest rates. Basically, when interest rates increase, bond prices decline, and vice versa. The reason for the decline in bond prices comes from the simple fact that newly issued bonds will have a yield that corresponds to the market interest rate at the time of issuance. As interest rates are currently higher than they have been in two decades, we can naturally assume that any brand-new bond will have a higher yield than any of the bonds in the fund's portfolio. Thus, the price of the bonds in the portfolio must decline so that they offer a competitive yield-to-maturity, or nobody will ever purchase them."

This is the reason for the overall decline in the fund's share price that we have seen since the start of 2022. The Federal Reserve's current interest rate tightening regime has been one of the most aggressive in history, which it pretty much has to be because the central bank arguably kept rates far too low for too long following the financial crisis and the COVID-19 stimulus.

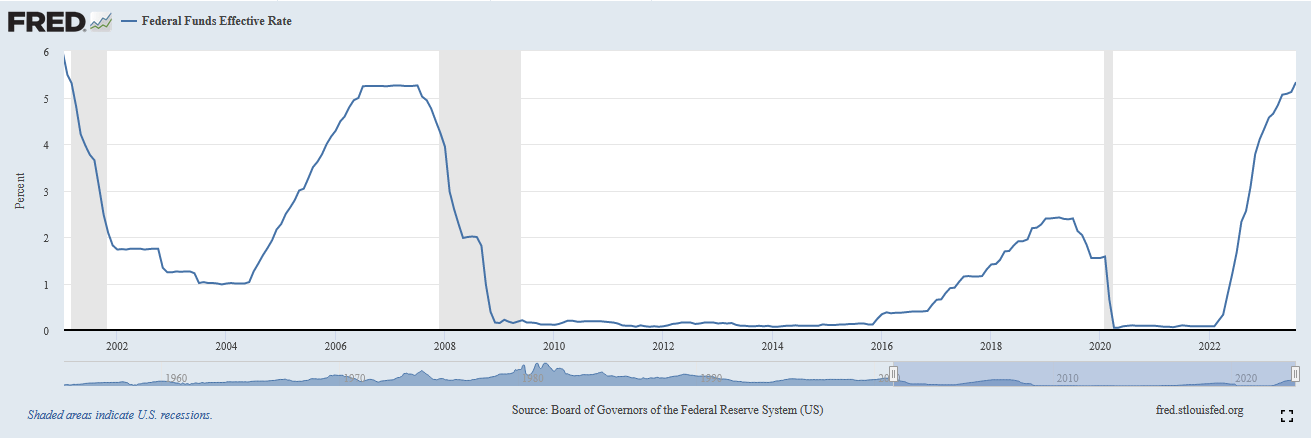

The Federal Reserve has shown no real signs of changing its policy since we last discussed this fund. In fact, it has raised rates further. We last discussed this fund on April 13, 2023, at which time the effective federal funds rate was 4.65%. As of the time of writing, the effective federal funds rate is 5.33%, which is the highest level that has been seen since February 2001. That was right before the start of the recession that followed the bursting of the .com bubble around the turn of the century:

{kind=link}

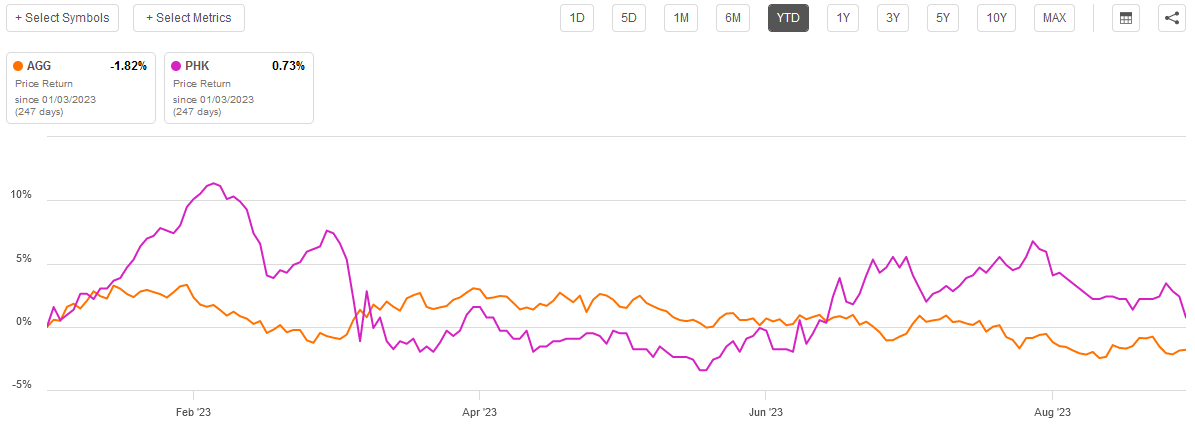

Today's forty-year-olds would have been in high school the last time that interest rates were at today's levels. In other words, we have now had an entire generation of traders get through a good portion of their careers without seeing interest rates so high. That has, understandably, created some unexpected conditions in the bond market. For example, there was a widespread belief that the current interest rate level would be temporary and that rates would begin falling during the final few months of 2023. The bond market even rallied a few times based on that belief. As we can see here, during both January and March, both the PIMCO High Income Fund and the Bloomberg US Aggregate Bond Index ( AGG ) rallied:

{kind=link}

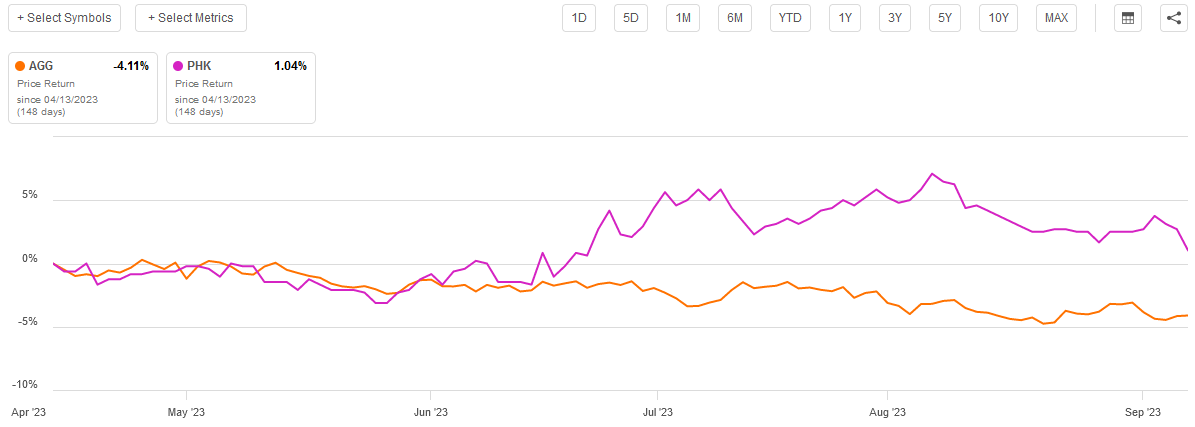

The only explanation for these rallies is that traders expected the Federal Reserve to cut rates and that these rate cuts would push up bond prices. Obviously, that has not happened, and in fact, the Federal Reserve is now stating that more rate hikes are a very realistic possibility. There are no insiders at the nation's central bank that are predicting near-term rate cuts. Despite this, the PIMCO High Income Fund is actually up since the last time that we discussed it even though the bond index is down:

{kind=link}

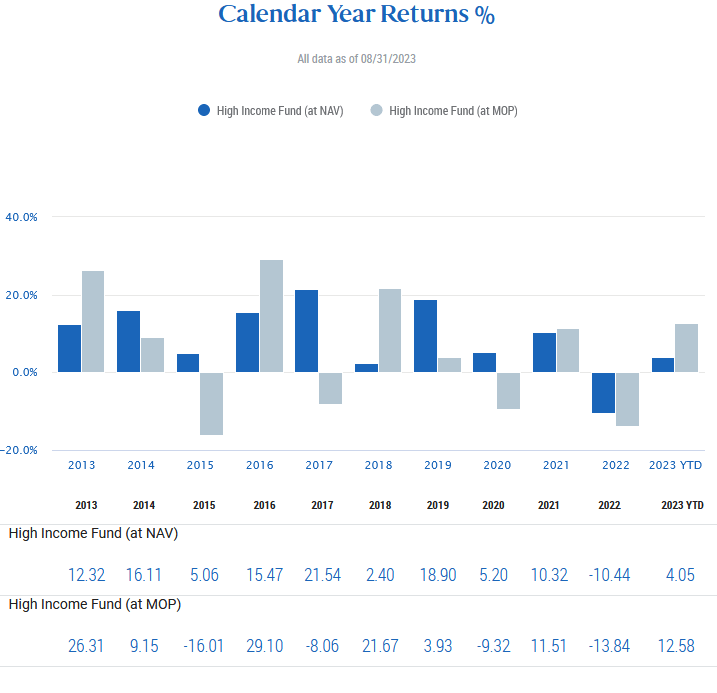

As I have pointed out in numerous previous articles though, closed-end funds do not always trade based on the actual value of their underlying assets. PIMCO itself points out that this fund's market performance has vastly exceeded the actual performance of its portfolio. As of August 31, 2023, PIMCO states that the fund's portfolio only managed to deliver a 4.05% total return year-to-date but the fund's shares delivered a 12.58% total return over the same period:

{kind=link}

Indeed, as we can clearly see, this fund has several years in which its market return differs vastly from the actual return of its assets. This can create buying opportunities for investors at times, such as in 2015 when the fund's portfolio delivered a positive return, but its shares fell substantially. The reverse is true today, as the fund's outsized performance relative to the portfolio itself could be a sign that the shares have gotten ahead of themselves. We will discuss this later in this article.

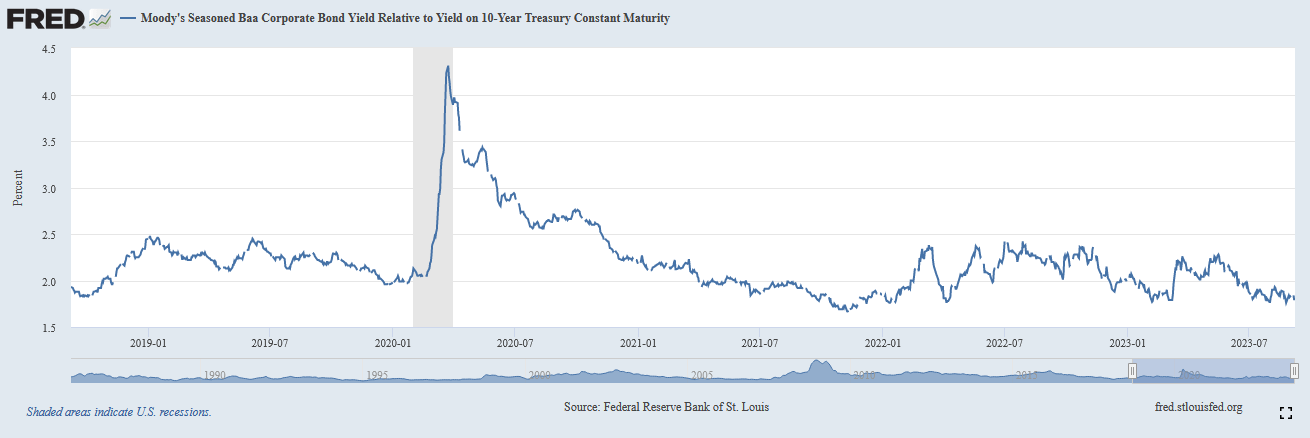

In my previous article on the PIMCO High Income Fund, I pointed out that a sizable portion of the fund's assets are invested in high-yield bonds ("junk bonds"). This is something that many fixed-income funds tend to do as these securities have dramatically higher yields than traditional investment-grade bonds. This has been especially true over most of the past fifteen years or so, as the Federal Reserve's interest rate policy drove the risk-free rate down to basically nothing. Indeed, the ten-year Treasury bond hit an all-time low of 0.54% in March 2020. Over the past decade, investment-grade corporates have traded for about 2.50% to 3.00% above the ten-year Treasury:

{kind=link}

Thus, we can very quickly see that it would be very difficult to achieve an effective portfolio yield of anywhere close to the 10% yield that closed-end funds are famous for by investing in investment-grade corporate securities. Therefore, funds started investing heavily in junk bonds in order to deliver the high yields that income-focused investors like to see. This is something that could concern more risk-averse investors however since we have all heard stories about how risky investing in junk bonds can be. Fortunately, we may be able to derive some comfort from looking at the credit ratings that have been assigned to the securities in the fund's portfolio. Here is a high-level summary:

CEF Connect

An investment-grade security is anything rated BBB or higher. As we can see, those only account for 11.21% of the fund's total assets. Thus, the overwhelming majority of the fund's portfolio consists of speculative-grade securities. This is almost certainly going to be concerning for those investors who simply want a high level of income without needing to take on too much risk. However, we can see that 37% of the fund's assets consist of BB or B-rated bonds, which are the two highest possible ratings for speculative-grade securities. As I pointed out in the past, most companies that are issued one of these ratings should be able to cover their obligations to the debtholders even in the event of a short-term economic shock.

Thus, we probably do not need to worry too much about defaults as most economic shocks are not particularly long-term or severe, although it is true that these securities do have a much larger risk of losses due to defaults. The fund's 399 unique holdings help to offset that risk since any individual default should have such a small impact on the portfolio that we should not need to worry about it. In addition, this is an actively managed fund so it is quite possible that the fund's management will sell off a bond if the issuing company's financial situation deteriorates to the point where a default is probable.

As such, the real risk with this fund is that interest rates will continue to rise and push down the value of the bonds contained in its portfolio. That is certainly a possibility that should not be ignored in light of recent statements from the Federal Reserve.

Leverage

As already mentioned, the PIMCO High Income Fund employs leverage as a strategy intended to boost the overall yield and return of its portfolio. I explained how this works in my previous article on the fund:

"In short, this fund is borrowing money and then using these borrowed funds to purchase bonds and other income-producing assets. As long as the interest rate that the fund pays on the borrowed money is less than the yield that it receives from the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As a result of this, we want to be sure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason."

As of the time of writing, the PIMCO High Income Fund has leveraged assets comprising only 17.69% of its portfolio. This is considerably less than the last time that we discussed this fund, which is a good sign. Leverage has been causing problems for some closed-end funds recently, which I pointed out in a recent article . The PIMCO High Income Fund appears to be recognizing this and lowering its leverage in response.

In the case of a bond fund, this could be an especially good thing because rising interest rates have reduced the gap between the rate that the fund can receive from its purchased assets and the rate that it has to pay on the borrowed money. As such, the advantages of using leverage are not as great as they once were so it makes sense that the fund's management does not see the risk-reward tradeoff as being particularly attractive anymore.

Distribution Analysis

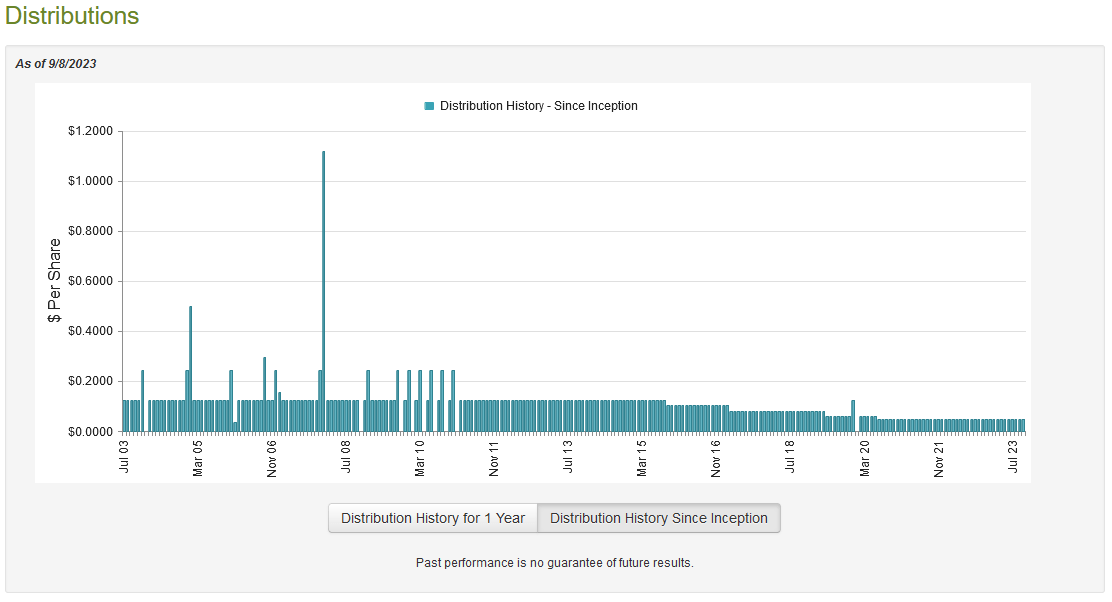

As mentioned earlier in this article, the primary objective of the PIMCO High Income Fund is to provide a high level of current income for its shareholders. In order to achieve this objective, the fund assembled a portfolio of mostly high-yield bonds that deliver the majority of their investment returns in the form of direct payments to the shareholders. The fund then applies a layer of leverage to boost the effective yield of the portfolio. As is the case with most closed-end funds, it then pays out substantially all of its investment returns to the shareholders in the form of distributions. As such, we might assume that this fund has a very high yield itself. That is certainly the case as the PIMCO High Income Fund currently pays a monthly distribution of $0.0480 per share ($0.576 per share annually), which gives it an 11.90% yield at the current price. The fund has unfortunately not been consistent with its distribution and has reduced it several times over its history:

{kind=link}

This is something that will almost certainly be a turn-off for anyone who is seeking a stable and secure source of income to use to pay their bills or finance their lifestyles. However, the fund has proven to be more resistant to the current challenging market conditions than many of its peers. This is one of the few fixed-income funds that has not cut its payout over the past year as tightening conditions have generally reduced bond prices. That could be an attractive characteristic right now, as the recent strong market performance appears to suggest.

As is always the case, it is important that we analyze the fund's ability to carry its current distribution. After all, we do not want to be the victims of a distribution cut as such an event would reduce our incomes and almost certainly cause the fund's share price to decline. The current double-digit yield appears to suggest that the market has some concerns that the fund may have to cut its payout so let us investigate this possibility.

Fortunately, we have a very current document that we can use for our analysis. As of the time of writing, the fund's most recent financial report (linked in the introduction) corresponds to the full-year period that ended on June 30, 2023. This is a much more recent report than the one that we had available to us the last time that we discussed the fund, which is a very good thing as it should give us a good idea of how well the fund handled the first half of this year. We can also see if it managed to make any capital gains by exploiting some of the optimism that the market exhibited with respect to interest rates potentially being reduced.

During the full-year period, the PIMCO High Income Fund received $83.302 million in interest along with $1.433 million in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $84.823 million during the period. It paid its expenses out of this amount, which left it with $67.015 million for shareholders. That was, unfortunately, not nearly enough to cover the $81.236 million that the fund actually paid out in distributions during the period. This is almost certainly concerning since we normally like fixed-income funds to fully cover their distributions out of net investment income and this one obviously failed to accomplish that.

With that said PIMCO funds tend to engage in the trading of bonds in order to exploit changes in bond prices and generate gains. This fund did have some success at accomplishing that task during the period. The PIMCO High Income Fund reported net realized gains totaling $48.873 million, but this was more than offset by $65.222 million in net unrealized losses. Overall, the fund's assets went up by $26.593 million after accounting for all inflows and outflows during the period, but that was only due to a $51.682 million capital raise that was conducted via the issuance of new common stock. The fund's net assets would have declined were it not for this influx of new money. As such, the fund technically failed to cover its distribution during the period.

With that said, the fund's net investment income combined with net realized gains was sufficient to cover all of its distributions. This is the most important thing, since net unrealized losses are not a big deal unless the fund actually sells depreciated securities and realizes the loss. Unrealized losses can always be undone by a bond increase in price, for example. In fact, a bond always pays its face value at maturity so in some cases unrealized losses can be erased by simply holding a security until it matures. Thus, the fact that the fund's assets went down due to unrealized losses is not a big deal. All this fund did was pay out its net investment income and approximately half of its net realized gains to the shareholders.

Valuation

As of September 8, 2023 (the most recent date for which data is currently available), the PIMCO High Income Fund has a net asset value of $4.39 per share. However, the shares currently trade at $4.71 each. That is a 7.29% premium on net asset value at the current price. This is much better than the 11.09% premium that the shares have had on average over the past month, but it is still a premium and generally speaking, paying a premium is overpaying for any fund. While this is probably one of the best fixed-income closed-end funds in the market, the price still seems rather high.

Conclusion

In conclusion, the PIMCO High Income Fund is a very high-yielding bond fund that can be used to earn a high level of income from your portfolios. The fund itself appears to have a good management team that has been able to fairly consistently generate enough net investment income and net realized gains to cover the distribution. That is a better performance than most bond funds have managed over the past year or so.

Unfortunately, there is some risk that interest rates will go up further and push down the value of the PIMCO High Income Fund's holdings. In addition, the price is incredibly high and that could create some risks for investors.

For further details see:

PHK: A Very Good Bond Fund, But Very Expensive Given The Risks