AGG - PHK: This Otherwise Great Bond CEF Is Insanely Expensive Today

2023-04-13 12:25:41 ET

Summary

- Although inflation has started to cool down, real income growth is still negative, so many people need options to increase the money coming in.

- PIMCO High Income Fund invests in a portfolio consisting mostly of bonds in an attempt to generate a high level of income.

- The PHK closed-end fund has a very good performance track record, as its total return comes pretty close to the index but the yield is a lot higher.

- The fund currently pays out a 12.03% yield and it appears able to sustain this.

- The fund currently trades at a much higher-than-average premium, so it looks very expensive.

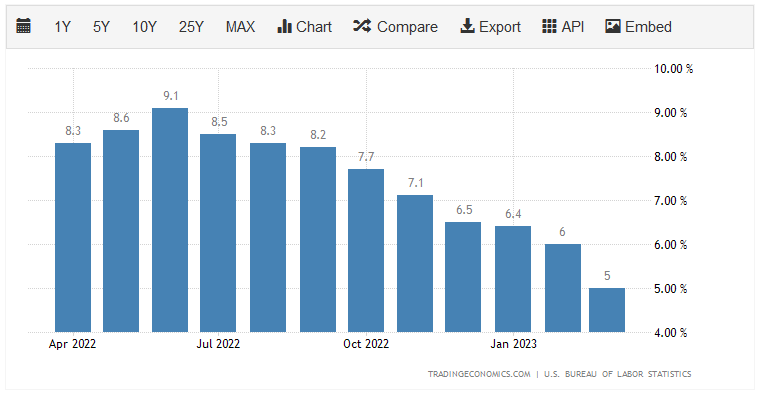

There can be little doubt that the biggest problem facing average Americans today is the incredibly high rate of inflation that is dominating our economy. This is evident in the consumer price index, which has increased by at least 6% year-over-year in eleven of the past twelve months:

{kind=link}

While we did see the index drop to 5% year-over-year in March, that still outpaced wage growth so the average person has now seen 24 straight months of declining real incomes. This has forced a substantial number of people to either take on second jobs, enter the gig economy, or resort to other methods in order to maintain their standard of living. This is not exactly a pleasant environment, which a glance at pretty much any social media site will reveal.

Fortunately, as investors, we have better methods that we can employ in order to earn the extra money that we need to cover our bills or finance our lifestyles. After all, we can put our money to work for us. One of the best ways to do this is by purchasing shares of a closed-end fund, or CEF, that specializes in income. These funds are unfortunately not very well-covered by the investment media and most investment advisors are not especially familiar with them. As such, it can be difficult to find information on these funds. That is unfortunate because they offer a number of advantages over other assets that are available in the market. In particular, these funds offer an easy way to obtain a portfolio of assets and are able to use certain strategies that allow them to earn a higher yield than just about anything else in the market.

In this article, we will discuss the PIMCO High Income Fund ( PHK ), which is one fund that falls into the income-generation category. As the name implies, the fund is managed by PIMCO, which has built something of a reputation as a high-quality fixed-income fund house, so that will likely increase the appeal of this fund in the eyes of many investors. This fund certainly lives up to its name, as its 12.03% current yield is more than sufficient to give investors a very nice boost to their incomes. I have discussed this fund before, but a few months have passed since that time, so naturally a few things have changed. This article will, therefore, specifically focus on these changes as well as provide an updated analysis of the fund’s finances.

About The Fund

According to the fund’s webpage , the PIMCO High Income Fund has the stated objective of providing its investors with a high current income. This is not surprising for a PIMCO fund, as many of the funds from this company are fixed-income funds. This one is no exception to this as the fund’s portfolio consists almost entirely of bonds, although it does have a small allocation to common stocks and preferred equity:

CEF Connect

This fits well with the fund’s description of its strategy as listed on the webpage:

“Using a dynamic asset allocation strategy among multiple fixed income sectors in the credit markets, the fund seeks high current income with capital appreciation as a secondary objective.

Aiming to identify securities that provide high current income and/or capital appreciation, the fund focuses on duration management, credit quality analysis, risk management techniques and broad diversification among issuers, industries and sectors as well as other risk management techniques designed to manage default risk.

The fund may invest any portion of its assets (in none) in below-investment-grade securities, or high-yield bonds (also known as junk bonds). The fund will not invest more than 25% of total assets in non-U.S.-dollar-denominated securities. The fund will not invest more than 40% of total assets in securities of issuers located in emerging market countries. Additionally, the fund will normally maintain an average portfolio duration of between zero and eight years.”

The PIMCO High Income Fund is clearly meeting the requirement outlined by this strategy of maintaining more than 80% of its assets in bonds. Admittedly, there may be some readers that point out that the bond allocation is actually more than 100%. This is possible because this fund employs leverage as a part of its strategy. We will discuss the implications of this later in this article. For now, the important thing to keep in mind is that this is a bond fund.

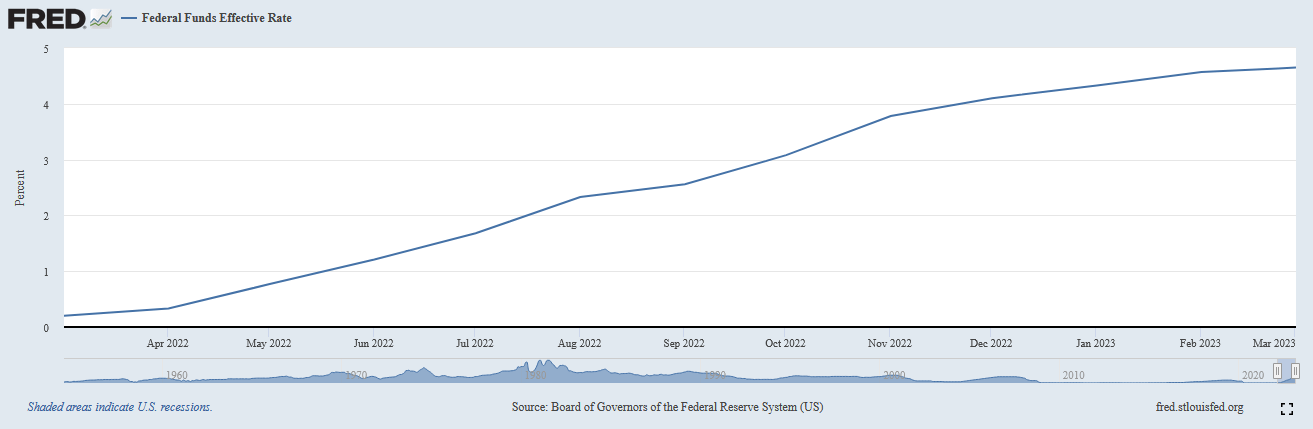

This is important because bond prices are extremely sensitive to interest rates. Basically, when interest rates increase, bond prices decline, and vice versa. Over the past year, the Federal Reserve has been aggressively raising interest rates in an effort to combat the incredibly high inflation that has been dominating the economy. This is easily apparent by looking at the federal funds rate, which is the rate at which the nation’s commercial banks lend money to each other on an overnight basis:

{kind=link}

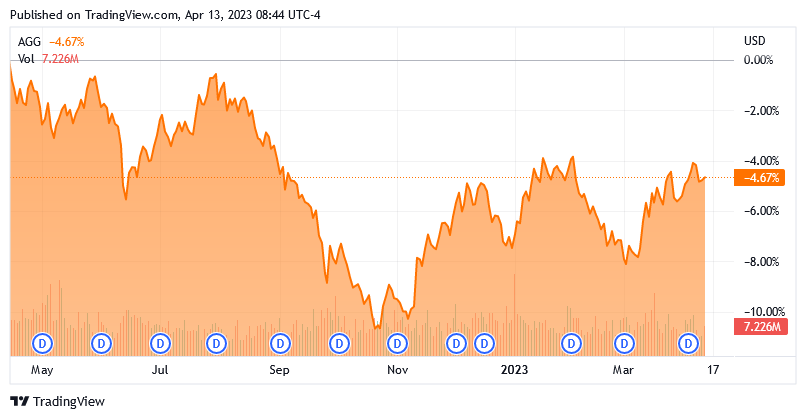

As we can see, the effective federal funds went from 0.20% a year ago to 4.65% today. This has had a devastating effect on bond prices. Over the past year, the Bloomberg US Aggregate Bond Index ( AGG ) is down 4.67%:

{kind=link}

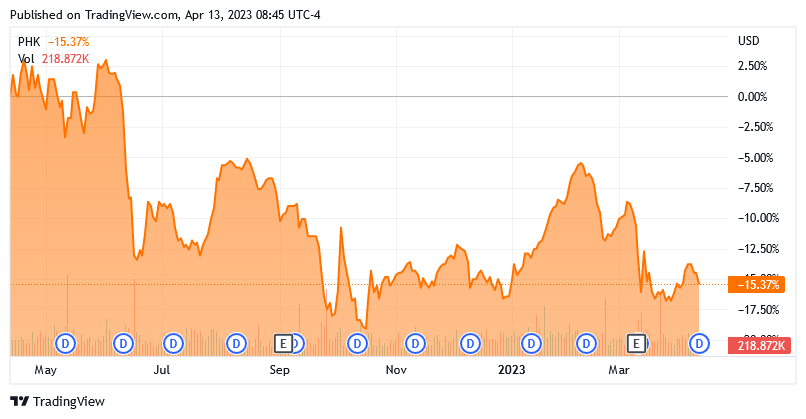

The PIMCO High Income Fund has certainly not held up any better. As of the time of writing, the fund is down 15.37% over the trailing twelve-month period:

{kind=link}

The reason for the decline in bond prices comes from the simple fact that newly issued bonds will have a yield that corresponds to the market interest rate at the time of issuance. As interest rates are currently higher than they have been in a decade, we can naturally assume that any brand-new bond will have a higher yield than any of the bonds in the fund’s portfolio. Thus, the price of the bonds in the portfolio must decline so that they offer a competitive yield-to-maturity, or nobody will ever purchase them.

This is, of course, only a problem if the fund’s management actually sells the bond. A bond will pay its face value at maturity regardless of what the market price does, so unless the issuing company defaults, the fund will not lose any money by buying a bond. However, PIMCO bond funds have a tendency to do a large amount of trading. This one is a bit of an exception to the rule though as the PIMCO High Income Fund only had a 37.00% annual turnover last year, which is not especially high for a bond fund. The reason that this is important is that it costs money to trade bonds or other assets. These expenses are billed directly to the fund’s shareholders, which naturally results in a drag on the portfolio’s performance. This also makes the job of the fund’s managers more difficult as they have to generate a sufficiently large return to cover these extra expenses and still deliver a return that is acceptable to the shareholders. That is a task that few management teams are able to accomplish on a consistent basis and as such, most actively-managed funds end up underperforming the benchmark indices.

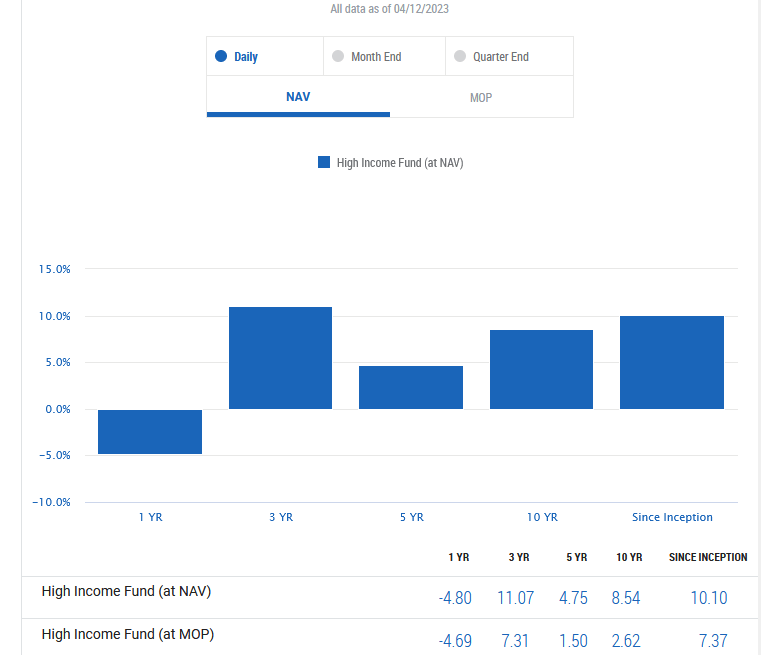

This one has not done as poorly as might be assumed based on the fund’s price action over the past year. There are two reasons for this. The first is that it is not uncommon for the shares of closed-end funds to perform differently than the actual portfolio does. This has been quite noticeable with fixed-income funds over the past year as many of them saw their share prices underperform the actual underlying portfolio. The second reason is that the PIMCO High Income Fund has a substantially higher yield than any of the major bond indices, so its shareholders would have received payments that offset some of the losses that the shares suffered over the period. As of April 12, 2023, the PIMCO High Income Fund’s portfolio delivered a –4.80% total return:

{kind=link}

We also see a pretty strong performance over several of the other periods shown in the chart above. Overall, PIMCO certainly appears to be delivering on its reputation as a top-tier fixed-income fund manager with this fund. Thus, investors that are reinvesting the fund’s distributions seem to be doing much better than the share price performance would indicate.

On the fund’s webpage, it is specifically stated that the fund may invest in high-yield bonds, which are securities that are colloquially known as junk bonds. It certainly appears to be doing that right now, which is clearly apparent by looking at the credit ratings of the bonds in the fund’s portfolio. Here is a high-level summary:

CEF Connect

A junk bond is anything rated BB or lower. As we can see, that is 64.49% of the portfolio, assuming that the unrated bonds are junk bonds. That is a very reasonable assumption since pretty much any company that has a strong enough balance sheet to merit an investment-grade credit rating will almost certainly pay to obtain one because it greatly decreases its cost of capital. Thus, the majority of the bonds in the fund’s portfolio are probably junk bonds. This is something that may concern those investors that are concerned about the preservation of the principal. After all, we have all heard that junk bonds are issued by companies that have a high risk of defaulting on their debt obligations. However, these risks may be overstated at times. As we can see above, fully 35.19% of the fund’s assets are rated either BB or B by the major rating agencies. These are the two highest ratings available for junk bonds and according to the official bond ratings scale , companies whose securities have these ratings have sufficiently strong finances to carry their debt even through short-term economic shocks.

Thus, the overall risk here should probably not be too great. This conclusion is reinforced by the fact that the PIMCO High Income Fund has 381 positions, so the actual percentage of the portfolio represented by a given issuer is probably not too great. Thus, if any individual issuer were to default, it should have a negligible impact on the portfolio as a whole.

Leverage

As mentioned in the introduction, a closed-end fund like the PIMCO High Income Fund has the ability to employ certain strategies that have the effect of boosting the effective yield of the portfolio. One of these strategies is the fund’s use of leverage, which was hinted at earlier in this article. In short, this fund is borrowing money and then using these borrowed funds to purchase bonds and other income-producing assets. As long as the interest rate that the fund pays on the borrowed money is less than the yield that it receives from the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This could be one reason why this fund’s market price declined so severely compared to the aggregate bond index. As a result of this, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. Fortunately, the PIMCO High Income Fund currently satisfies this requirement as its levered assets only comprise 26.57% of the portfolio. Overall, the fund appears to be striking a reasonable balance between risk and reward.

Distribution Analysis

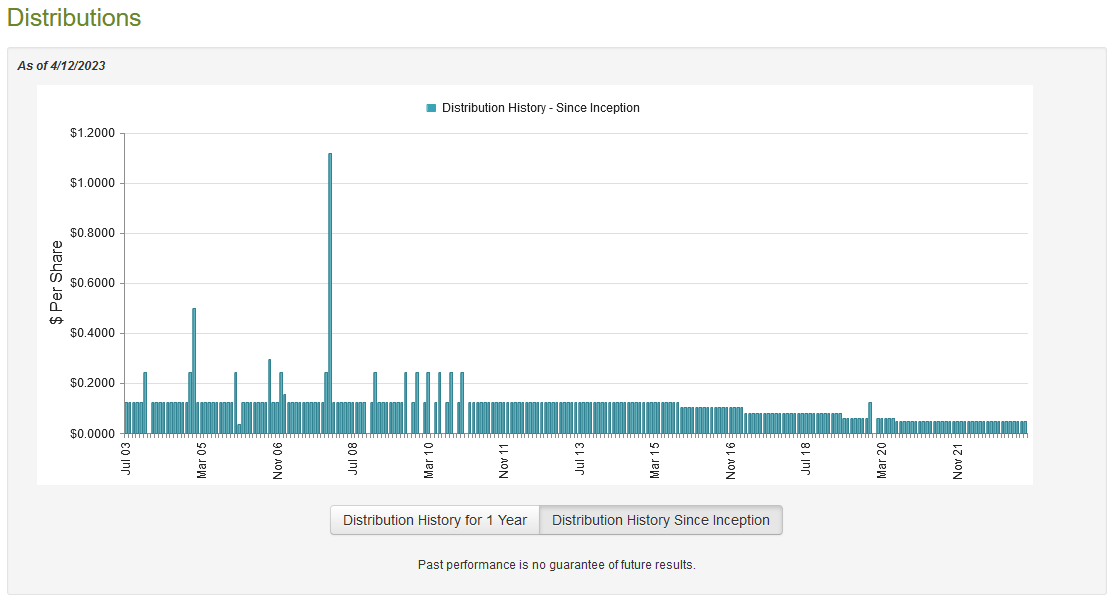

As stated earlier in this article, the primary objective of the PIMCO High Income Fund is to provide its investors with a high level of current income. In order to accomplish that objective, the fund purchases bonds, particularly high-yield bonds, that tend to provide a respectable level of income. The fund then uses leverage to boost the effective yield that it receives from its assets. As such, we might assume that the fund boasts a very high yield itself. This is certainly the case as the PIMCO High Income Fund pays out a monthly distribution of $0.0480 per share ($0.576 per share annually), which gives it a 12.03% yield at the current price. Unfortunately, the fund’s distribution history leaves something to be desired as it has been gradually cutting its distribution over the years. However, it has been stable since 2020:

{kind=link}

The fact that the fund’s income declined gradually over its history may reduce its appeal for those investors that are looking for a safe and secure source of income with which they can pay their bills and otherwise finance their expenses. However, this is one of the only fixed-income funds that did not alter its distribution over the past twelve months in response to the volatility in the bond market, so that is certainly saying something. In addition, as I have noted numerous times in the past, the fund’s history is not necessarily the most important thing for anyone purchasing the fund today. This is because new money will receive the current distribution at the current yield. As such, the most important thing is the fund’s ability to sustain its current distribution.

Fortunately, we do have a very recent document that we can consult for our analysis. The fund’s most recent financial report corresponds to the six-month period that ended on December 31, 2022. This is a much newer report than we had available the last time that we looked at the fund and it should give us a much better idea of how the fund navigated the extremely challenging conditions that existed in the bond market over the course of 2022. During the six-month period, the PIMCO High Income Fund received $41.703 million in interest along with $698,000 in dividends from the assets in its portfolio. This gives the fund a total investment income of $42.401 million over the period. The fund paid its expenses out of this amount, leaving it with $33.968 available for shareholders. This was unfortunately not enough to cover the $39.642 million that the fund actually paid out in distributions during the period, although it did get reasonably close. This is something that could be concerning at first glance due to the fact that the fund’s net investment income is not sufficient to cover its distributions.

Fortunately, the fund does have other methods through which it can obtain the money that it needs to cover its expenses. For example, it might have sufficient capital gains to cover the difference between net investment income and the distribution. As might be expected from the troubles in the bond market over the period, the fund generally failed at this task, although it did not really do that badly. It reported net realized gains of $75.505 million but this was offset by $81.194 million in net unrealized losses. While the fund did fail to grow its assets, the net investment income plus net realized gains were more than sufficient to cover the distributions with a substantial amount of money left over. As already mentioned, unrealized losses are not really a big deal with bonds because the bond will still pay out the face value at maturity so we can probably overlook that. Overall, the fund is probably fine in terms of being able to afford the distribution.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the PIMCO High Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. Unfortunately, that is not the case with this fund today. As of April 12, 2023, the PIMCO High Income Fund had a net asset value of $4.52 per share but the shares actually trade for $4.79 each. This gives the fund’s shares a 5.97% premium to net asset value at the current price. That is a pretty high price to pay for any closed-end fund, despite the fact that this one is a good one. PIMCO funds in general tend to trade at premium valuations though so we can probably not expect to be able to pick this one up at a discount anytime soon. However, the fund has traded at a 4.38% premium on average over the past month, so the current price is a bit expensive. It would probably be best to wait until the price declines a bit before buying shares of the fund.

Conclusion

In conclusion, the inflation rate has come down a bit, but real income growth is still negative, and many consumers are in desperate need of income in order to maintain their lifestyles. The PIMCO High Income Fund provides a way to obtain this income by investing in bonds. The fund has generally performed pretty well for a bond fund over its history and so should prove to be a solid investment for anyone looking for income. The fact that the fund appears to be able to sustain its 12.03% yield only adds to its appeal. The only real downside here is that the fund appears to be very expensive today, so anyone buying will pay through the nose for the good things that come with this PIMCO High Income Fund.

For further details see:

PHK: This Otherwise Great Bond CEF Is Insanely Expensive Today