PAXS - PHK: Worth A Switch From PIMCO's Newest CEFs PDO And PAXS

2023-10-17 07:28:41 ET

Summary

- The PIMCO High Income Fund offers a relative value opportunity versus the more recently launched CEFs PDO and PAXS.

- PHK has a lower management fee, longer track record, and higher-quality allocation profile, which should keep its valuation well above the other 2 funds.

- PHK's valuation has compressed recently against PDO and PAXS, offering an opportunity for PDO or PAXS holders to rotate to PHK.

In this article, we take a look at a relative value opportunity within the PIMCO taxable CEF suite. Specifically, we highlight the PIMCO High Income Fund (PHK) which looks significantly more attractive than the pair of PIMCO's most recently launched CEFs - the Dynamic Income Opportunities Fund (PDO) or the Access Income Fund (PAXS).

In this article, we discuss why PHK should enjoy a significantly higher valuation than the other pair of funds and why the recent valuation compression across the three funds offers an opportunity for PDO or PAXS holders to rotate to PHK.

Apart from the valuation consideration, PHK is attractive for more defensive investors given its significantly lower-beta profile due to its sizable swaps book and a low level of leverage.

The Relative Value Case

In the chart below, we can see significant valuation compression across the three funds over the last few weeks.

Systematic Income

This chart shows the trend more clearly. Historically, PHK has tended to trade at a valuation closer to 10% above that of the average of the other two funds and this has now nearly been erased.

Systematic Income

PHK's deserved valuation premium was there historically for several reasons.

First, PHK has a significantly lower management fee of 0.76% to 1.15% and 1.25% for PDO and PAXS, respectively. This may not seem like a big deal but recall that the fee is charged on total assets, which means its impact is magnified as a function of net assets. Assuming 30% leverage, a fee differential of 0.39% translates into a portfolio yield impact of over 0.6%.

Lower fees translate into a lower drag on the fund's net income which should, in turn, translate into a higher valuation. If this is not intuitive, consider an edge case of two funds both holding 5%-yielding Treasuries, with one fund charging a 0.01% management fee and the other fund charging a 1% management fee. The first fund generates a net income yield of 4.99% on NAV while the second generates a 4% yield on NAV.

Investors will obviously avoid the second fund until it trades at a significant discount so that it can generate roughly the same yield on price as the first fund. For example, if the first fund trades at the NAV (i.e. has a discount of zero), the second fund should settle down to trade at a discount of around 20% so that its yield on price is around the same 5% as that of the first fund.

Closer to home, for funds with a portfolio yield of 8%, leverage of 30% and management fees corresponding to those of PHK and PDO, PDO should trade at a discount 7% wider than that of PHK in order to generate the same portfolio yield on price. The three funds don't have the same level of leverage or the exact same portfolio yield, however this aspect does not significantly change the point here.

Systematic Income

The second reason why PHK should trade at a higher valuation is its much longer track record . PHK was launched over 20 years ago while PDO was launched in 2021. PIMCO taxable credit CEFs with longer track records tend to carry significantly higher valuations than PDO or PAXS.

It's not straightforward to isolate the impact of longevity on valuation as the PIMCO funds that were launched earlier tend to also have lower management fees (e.g. 0.65% - 1.10%) than funds that were launched more recently (e.g. 1.15% - 1.35%).

That said, a fund like PDI has a relatively high management fee of 1.10% for a legacy fund (it was lowered slightly when it merged with PKO and PCI). And although the fund's valuation has fallen recently, it remains quite a bit above that of PDO or PAXS.

In our view, a track record, in and of itself, should not necessarily drive a higher valuation. This is because the more recently launched funds like PDO and PAXS have the same managers as the legacy funds like PTY and PCM. However, investors do take some comfort from seeing historic returns, which are relatively strong for the taxable PIMCO CEF suite, which is likely the mechanism that causes earlier-launched funds to enjoy higher valuations.

The third reason for a higher valuation of PHK over PDO and PAXS, which is somewhat weaker in our view than the two above, is the higher-quality allocation profile of PHK. As the sector allocation chart below shows, PHK has a small CMBS allocation - a sector that has been relatively stressed this year. Two, about 16% of its portfolio is in interest-rate swaps (corresponding to the "US Government Related" sector allocation in the chart), which carries no credit risk.

Systematic Income CEF Tool

Three, its leverage is well below that of PDO and PAXS. This not only makes it a lower-beta fund - it also means its net income is much more efficient than that of PDO and PAXS. These two funds generate very little positive net income on their leveraged assets given total expenses north of 7% on their leveraged assets.

Systematic Income

And four, PHK, alongside the other legacy taxable PIMCO CEFs, recently bought back a bunch of their ARPS, reducing its cost of leverage as ARPS featured a higher level of interest expense than repo.

Finally, and this is linked to the allocation point above, PHK has generated a stronger total NAV return versus PDO and PAXS since the inception of these two funds. This is largely due to three factors - higher leverage of the last two funds in a difficult market period for fixed-income assets, their higher CMBS allocation and the lower PHK management fee.

The chart below shows the normalized total NAV return of PHK and PDO since the inception of PDO.

Systematic Income

And this chart shows the same for PAXS.

Systematic Income

Distribution Risk

So, given these reasons, why is PHK trading at a similar discount to PDO? In our view, the culprit is the fear of distribution cuts. In fact, PIMCO is arguably overdue to a distribution cut in their taxable suite.

As the chart below of distribution changes (cuts marked in red, hikes marked in green) shows, PIMCO like to make adjustments roughly once a year. The last two adjustments were hikes for their newer funds about a year ago so we look to be due. Perhaps the cuts across the Muni CEF suite stayed PIMCO's hand on the taxable front, pushing any taxable CEF distribution changes into 2024.

Systematic Income

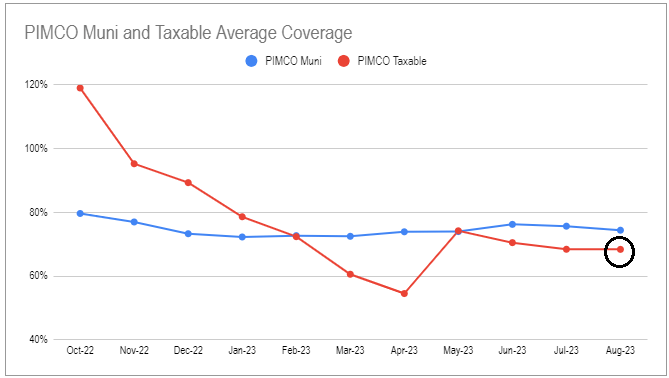

Funds like PDO and PAXS should be at less risk for a cut given their raises over the last couple of years and their relatively low NAV distribution rates. This means that the legacy funds are under a microscope. In our view, funds at risk are PCM, PDI and RCS. The relatively low level of coverage in the taxable CEF suite is a concern for many investors and is likely what's driving the recent valuation compression.

{kind=link}

Overall, investors allocated to PDO and PAXS should consider a rotation to PHK on valuation grounds. This rotation is particularly compelling for more defensive investors given the lower-beta profile of PHK.

For further details see:

PHK: Worth A Switch From PIMCO's Newest CEFs PDO And PAXS