PHT - PHT: Avoid This Amortizing 'Return Of Principal' Fund

2023-11-13 20:00:50 ET

Summary

- Pioneer High Income Fund pays a high distribution yield but has historically earned only modest total returns, leading to principal losses and shrinking distributions.

- PHT's portfolio consists mainly of non-investment grade bonds and convertible securities, with a significant allocation to high-yield corporate bonds.

- While PHT has above-average returns compared to the high-yield bond asset class, its distribution rate may be too high for its earnings power, making it a poor long-term investment.

Readers know I have a personal vendetta against 'return of principal' funds. My critique is that unsuspecting retirees and pensioners are attracted to high yielding funds without considering whether these funds actually 'earn' their distributions.

One prime example is the Pioneer High Income Fund ( PHT ) offered by Amundi Asset Management. At first glance, the PHT fund looks attractive as it pays a 9.7% distribution yield on market price. However, if we dig into the details, we see that the PHT fund has historically only earned 3-4% per year in total returns over the past decade. This means the fund's NAV has shrunk, leading to principal losses and shrinking distributions.

I would personally avoid amortizing 'return of principal' funds like the PHT.

Fund Overview

The Pioneer High Income Fund is a closed-end fund ("CEF") that aims to deliver a high level of current income from a portfolio of non-investment grade bonds and convertible securities.

I have previously made this critique against the Pioneer Floating Rate Fund ( PHD ), but I find Amundi's presentation of their funds' details sorely lacking, as Amundi's website only list links to the various fund's factsheets, annual reports, and semi-annual reports on a minimalist website.

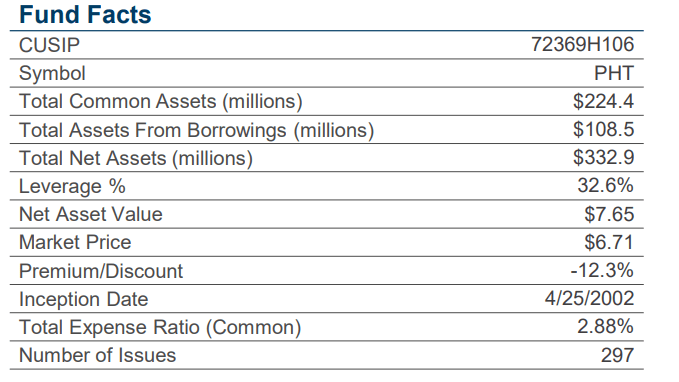

The PHT fund employs leverage to enhance returns. As of September 30, 2023, the PHT fund has $109 million in borrowings against $333 million in gross assets for 33% effective leverage (Figure 1). The PHT fund charged a 2.88% total expense ratio in fiscal 2023.

{kind=link}

Portfolio Holdings As Expected

PHT's portfolio consists of 297 investments with a portfolio duration of 2.8 years (Figure 2).

{kind=link}

Figure 3 shows the PHT fund's sector allocation, with high yield corporate bonds representing 66.9% of the portfolio (domestic 54.5%, international 12.4%). Emerging market bonds are the third largest sector at 9.0%.

{kind=link}

Credit quality is primarily BB-rated (26.0%) and B-rated (39.3%), with a smaller allocation to CCC-rated (14.9%) and BBB-rated (6.8%) securities (Figure 4).

{kind=link}

PHT Has Above Average Returns

The PHT fund has generated modest historical returns with 3/5/10 Yr average annual returns of 4.0%/2.9%/3.2% respectively to October 30, 2023 (Figure 5).

{kind=link}

The PHT fund's historical returns compare favourably to a passive high yield index fund like the iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ), which has only returned 0.2%/2.0%/2.7% respectively in the same time frames (Figure 6).

{kind=link}

But Distribution Rate May Be Too High

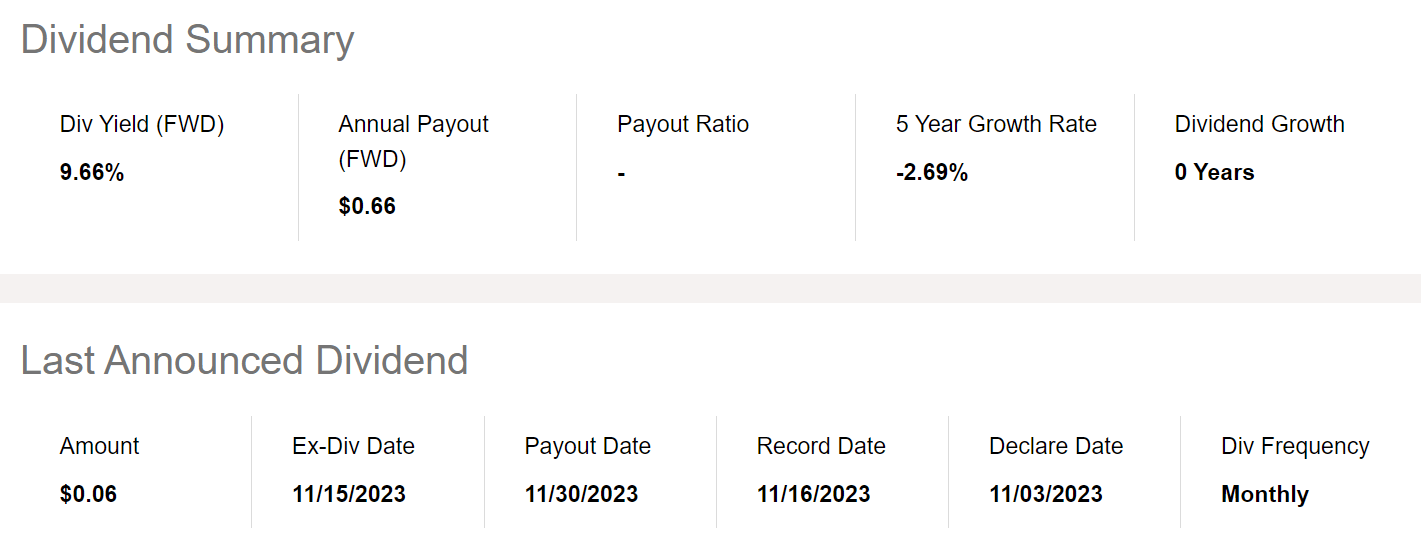

However, the PHT fund's distribution rate may be too high for its earnings power. The PHT fund is currently set to pay $0.055 / month or a forward yield of 9.7% (Figure 7). On NAV, PHT's distribution yield is 8.7%.

{kind=link}

My concern is that the PHT fund is paying an 8.7% of NAV distribution yield but has only earned 3-4% p.a. in total returns for the past decade. Funds that pay more than they earn are called 'return of principal' funds, according to a whitepaper from Eaton Vance.

The simplest way to figure out if a given fund is an amortizing 'return of principal' fund is to look at the NAV history. "Regardless of how distributions are characterized, if a fund’s NAV increases, the fund earned its distribution. If not, the fund did not earn its distribution" .

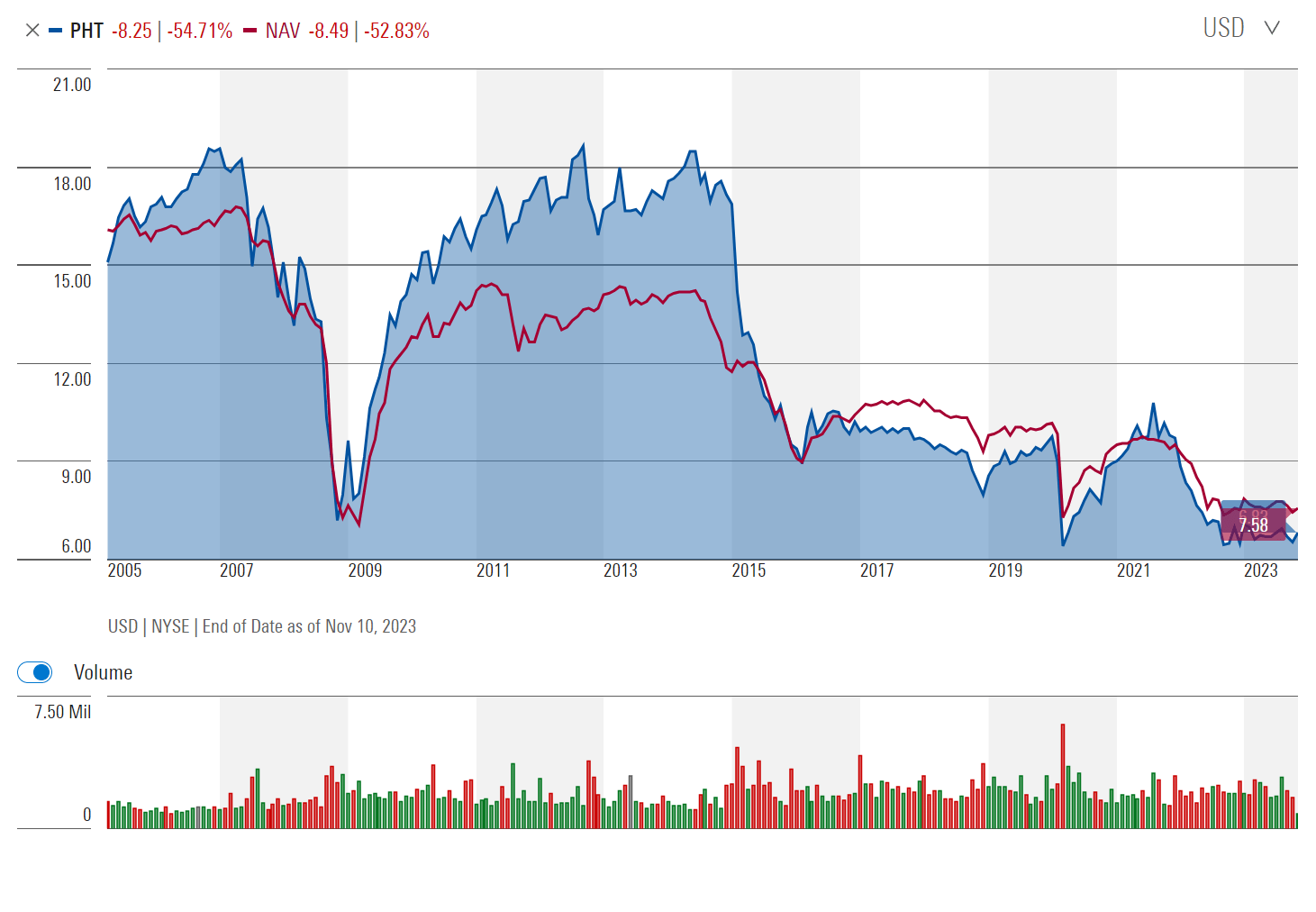

Looking at PHT's NAV history, the PHT fund's NAV has shrunk by ~50% from a peak of over $16 / share prior to the Great Financial Crisis to a recent $7.58 / share (Figure 8). Since fund prices tend to track NAV, long-term investors in the PHT fund would be sitting on massive unrealized losses.

{kind=link}

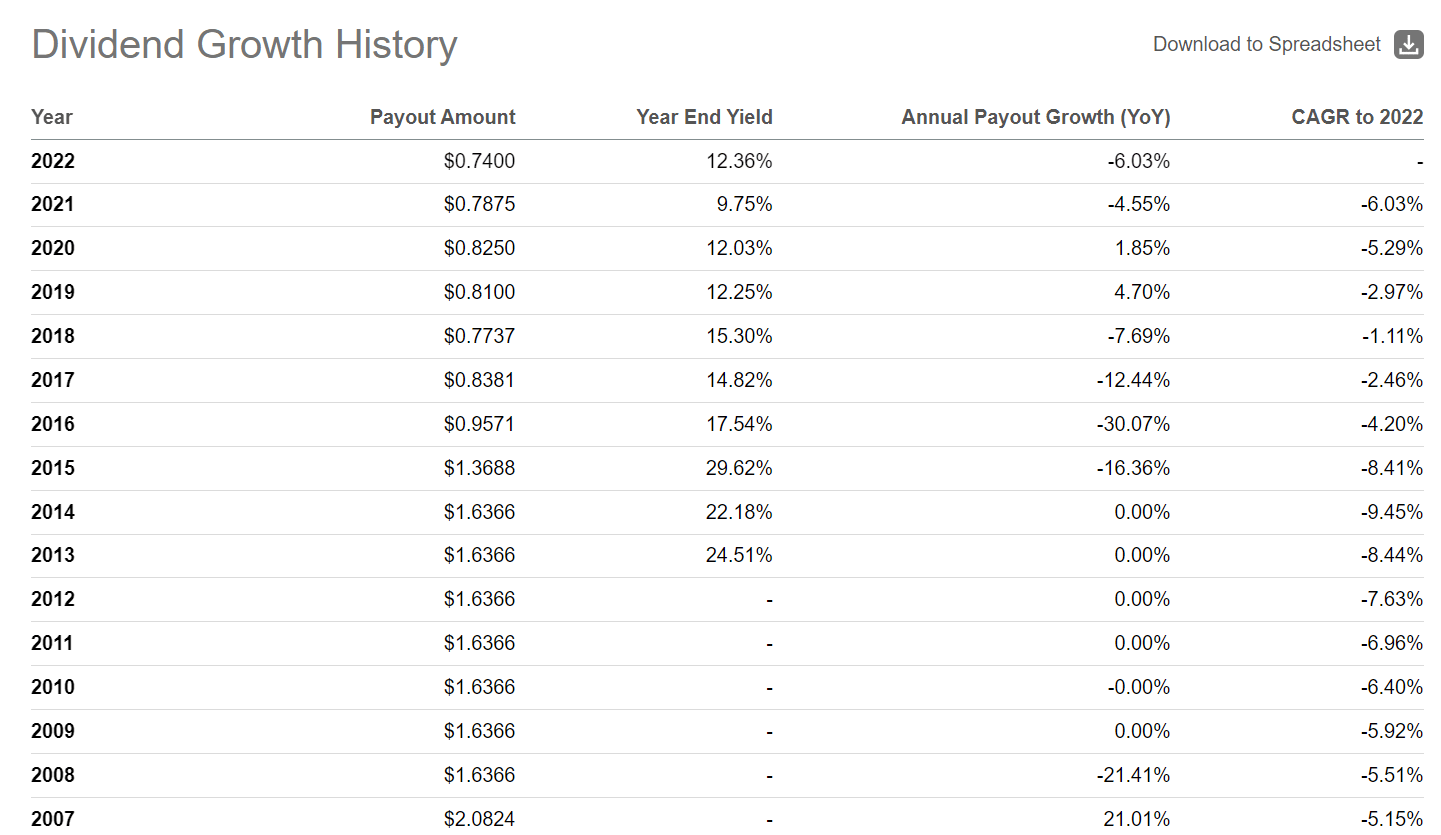

Furthermore, as NAV shrinks, there are less assets to earn income to pay distributions, so distributions also shrink. PHT's annual distribution / share has likewise declined from over $2 / share in 2007 to the recent forward rate of $0.66 or a decline of more than 67% (Figure 9).

{kind=link}

Long term investors would have lost both principal and income from investing in 'return of principal' funds like PHT.

Look Beyond NII And Consider Total Returns

Note, I understand some readers will question my characterization of the PHT fund as a 'return of principal' fund, since if they look at the fund's financial statements, they will see that the distributions have been funded from net investment income ("NII") and there has been no 'return of capital' ("ROC") from an accounting standpoint (Figure 10)

{kind=link}

However, funds can still have an amortizing NAV even if distributions are funded out of NII. This is because the fund may be stretching on the credit quality front by investing in lowly rated credits that carry big yields. For example, B-rate credits have a 1-year 3.2% default rate and CCC-rated credits have a 26.6% 1 year default rate (Figure 11).

Figure 11 - Cumulative default rates by starting rating (S&P Global)

So even though PHT's NII is high, realized, and unrealized losses are also commensurately high, leading to NAV declines over time. In the past 5 fiscal years, the PHT fund had cumulative losses of $2.82 / share in losses.

Conclusion

While the PHT fund has generated respectable total returns of 4.0% over 3 years and 2.9% over 5 years, better than the passive HYG ETF, the fact that the PHT fund demonstrates clear characteristics of being an amortizing 'return of principal' fund makes it a hard pass for me.

Common sense tells us that when someone spends more than they earn, even if they are ultra-high earning professional athletes or investment bankers, they will eventually go bankrupt. The same principal applies for investment funds. Even if a fund like PHT outperforms its asset class, as long as it is set up to pay out more than it earns in total returns, NAV will eventually deplete and distributions will inevitably be cut.

I recommend investors avoid 'return of principal' funds like the PHT.

For further details see:

PHT: Avoid This Amortizing 'Return Of Principal' Fund