PILBF - Pilbara Minerals: A Growth Story With Upside Potential

2024-01-07 05:54:55 ET

Summary

- Pilbara is a leading producer in Lithium mining, with 8% of the Spodumene market.

- It operates in a stable jurisdiction, Australia, and could benefit from the US IRA framework.

- Given its development CAPEX, its production should reach 1mt per year by 2026, further increasing its market share.

- Meanwhile, its vertical integration downstream to produce Lithium hydroxide battery grade conjointly with POSCO will add value.

- The valuation I modeled exhibits upside potential, even taking into account a conservative Lithium price scenario. The balance sheet is solid, allowing for further cash distribution or opportunistic M&A. To me, it’s a BUY.

My Thesis

Pilbara ( PILBF ) stock price has been quite volatile during the last year, absorbing the impact of a steep decline in the market Lithium price. However, under the surface, Pilbara is on the way to significantly ramp up its production, which should lead to a solid cash-flow generation once the phase of large spending ends. To cope with transitory elevated investment, the firm can count on a solid net cash balance sheet, limiting any liquidity risk. My DCF model indicates a clear upside potential, using conservative hypotheses. To me, it's a BUY.

Investment Overview

I believe the Australian mining company Pilbara is benefiting from an early mover advantage, having started its first annual Spodumene production in 2019 (175kt) combined with a close-to-perfect execution since then. The firm successfully managed to increase the output of its two mines located in the Pilgangoora region (including the Ngungaju mine integrated via the acquisition of Altura in 2021) to 620kt in FY2023 (end June).

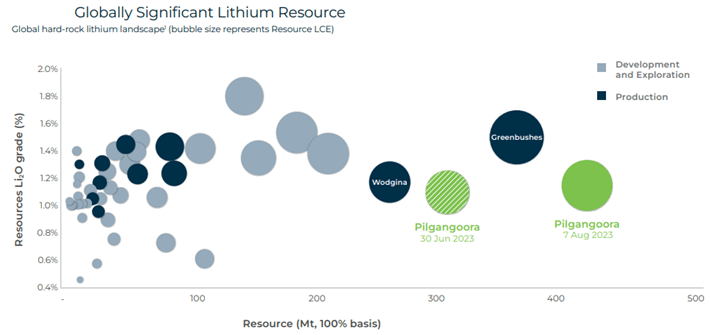

Therefore, a large part of CAPEX has already been spent. Thanks to geological studies, the firm recently increased its estimations of the site's Lithium Ore reserves by 55Mt to 214Mt while Resources outpaced 400Mt, placing itself in the top hard-rock extraction site. It led to an extension of the mine life from nine years to 34 years.

{kind=link}

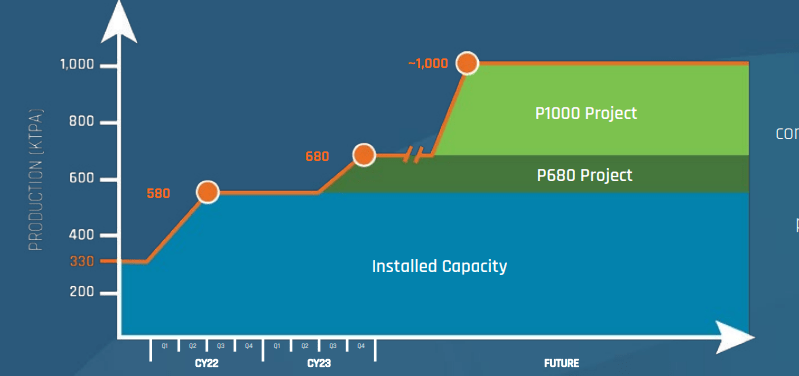

The firm is now engaging capital to develop its P1000 project, with the first ore expected to be mined during the first quarter of 2025 (happening during the second semester of fiscal year (FY) 2026). By calendar year 2026 (FY2027), Pilbara Minerals total production should reach 1mt of Lithium Spodumene (equivalent to approximately 148kt of LCE).

{kind=link}

As a reminder, the Lithium demand should rapidly grow within the current decade, mainly driven by an increasing penetration of electric vehicles. The market leader Albemarle ( ALB ) expects, based on S&P assumptions, that the demand will grow from 800kt LCE to more than 2mt LCE after 2026, with a CAGR close to 30%.

Albemarle

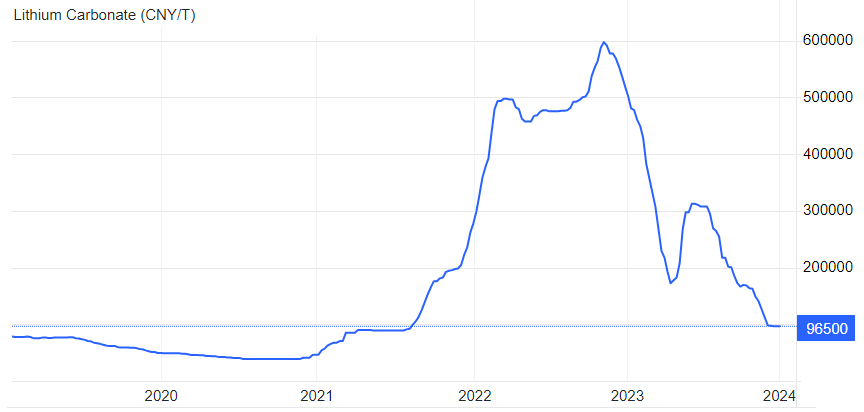

However, the Lithium market has recently suffered a severe correction, as multiple projects came in line while we experienced a weaker EV demand coming from China and lower GDP growth globally, which raised short-term uncertainties.

{kind=link}

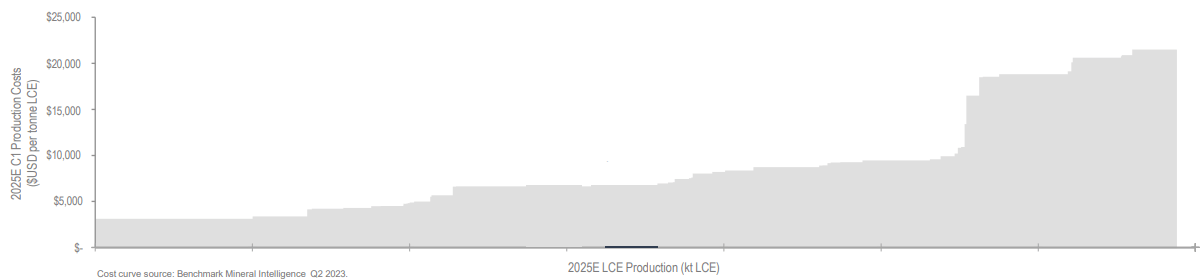

The current All-in sustaining cost curve ((AISC)) indicates high-cost producers are near $20k/t (see below). Meanwhile, Albemarle shows in its most recent presentation that Lithium prices above 20k/t will be required to incentivize miners to operate new sites to fill the expected supply deficit by 2030. I believe such a level could act as a flood, a support. Therefore, further downside could be limited, paving the way for a price rebound in the near term.

{kind=link}

What Valuation Can We Expect?

At first glance, if we look at relative valuation, we see that Pilbara Minerals is not undervalued versus peers on a three-year horizon. However, as most of the production growth will come between 2026 and 2027 (+40% over the period), this is not captured in the available analyst estimates. Thus, I think it is relevant to implement a DCF over the full development cycle.

{kind=link}

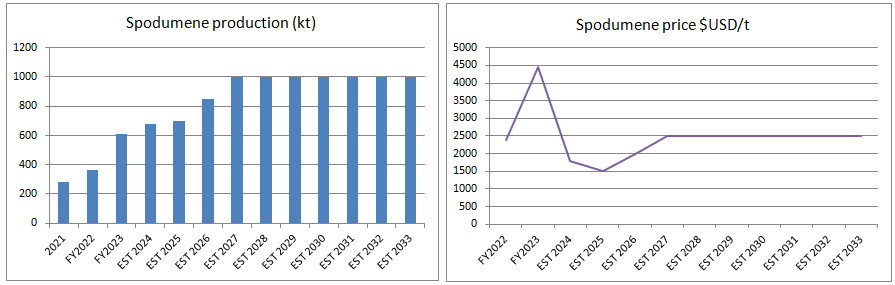

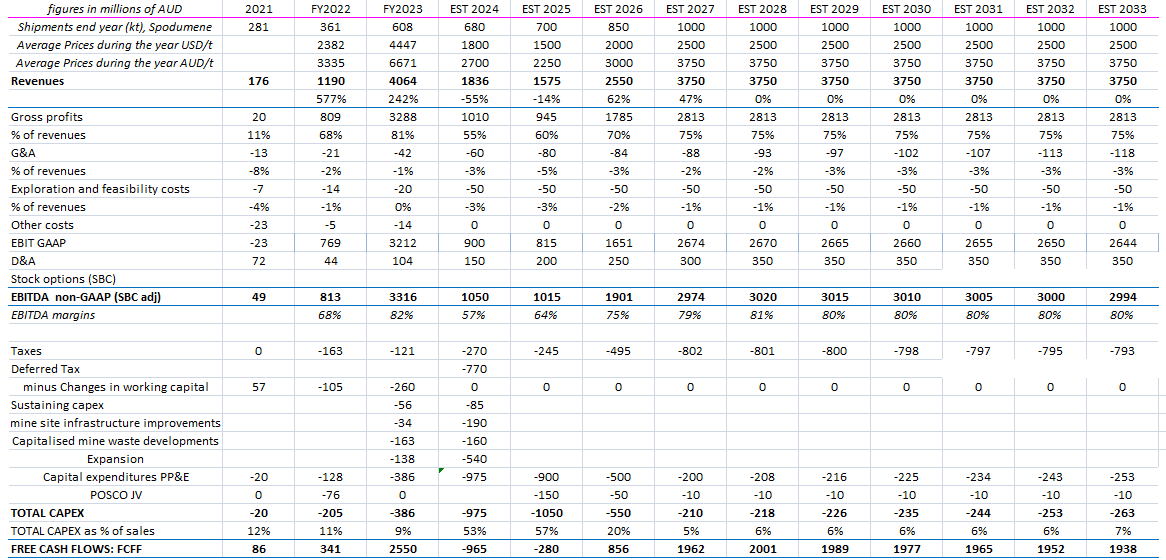

Let's start with the production levels: I modeled a gradual convergence toward the P1000 expansion plan. However, I fixed the full production horizon at FY2027 instead of during FY2025 expected by the management , to be more conservative and to reach some margin of safety. Concerning the commodity pricing: my main scenario (see below) uses low spodumene prices in the near term and a gradual rebound toward 2500$/t, just above the high end of the cost curve (adjusted from future inflation).

{kind=link}

I expect margins to normalize downward and exclude any positive impact from the share of LiOH (hydroxide) produced in the POSCO JV to process Lithium, as details are lacking (but I take into account related CAPEX). Taxes are set at 30% of the EBT (Australian corporate rate) while FY2024 should see a large outflow of AUD773m deferred tax liabilities. CAPEX figures include growth PP&E as expressed by the management: I took the higher range of expenses given the ongoing inflationary cost pressures.

{kind=link}

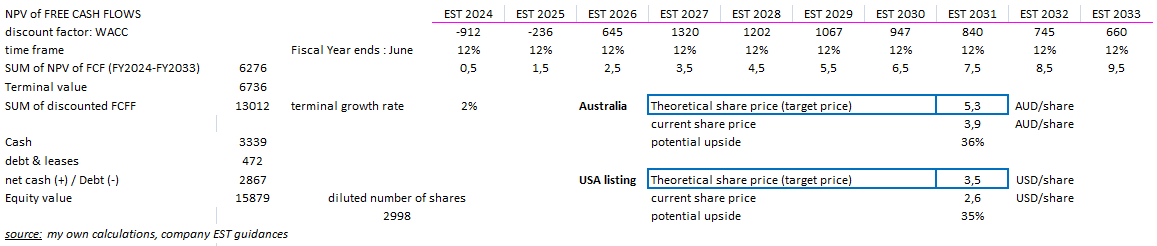

I used a terminal growth rate of +2% and a WACC of 12% to assess the asset concentration risk and P1000 ramp-up risk. I obtain a share price of USD3.5/share, which is 35% above the current USD listed stock price.

{kind=link}

To assess for more scenarios, as the price of a commodity can be unpredictable, I did implement a sensitivity table:

{kind=link}

Balance Sheet Analysis

Pilbara Minerals generated strong cash flow over the last FY23, reaching a net cash position of AUD2.9bn after having paid a dividend of AUD330m. Going forward, I estimate that cash from operations will auto-finance CAPEX and cover the dividend payment (payout of 20-30% of the FCF). Thus, credit risk seems limited.

When large CAPEX is behind and Lithium prices will eventually bottom out, I see FCF increasing sharply leading to excess cash generated which could be used to pay extra dividends, implement buybacks, or decide to acquire new assets given the industry trend to consolidate.

Technicals

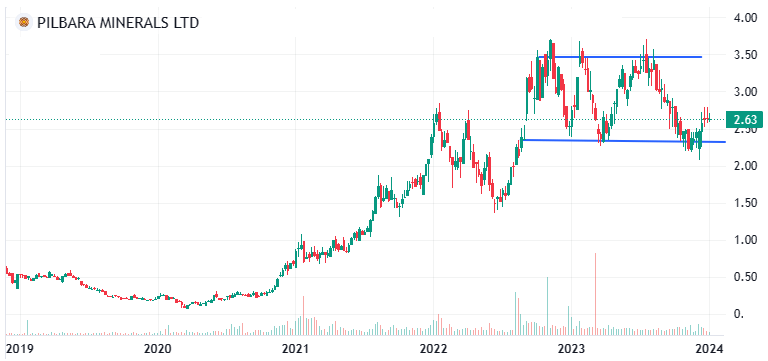

The stock price seems to have bottomed at the $2.2/share support level. This happened in conjunction with the decline of US bond yields: expectations of lower FED rates, lower recession risks, and also better financing conditions for expensive electric cars. The price of Lithium has not yet rebounded, still.

{kind=link}

Risks

The first risk that comes into my mind is company-specific and is related to how the firm will execute. The firm will experience a significant ramp-up of its production in the coming years: any delay or cost inflation could have a severe effect. Moreover, operations are not geographically diversified: all future revenues will be generated by only two mines in one common location.

Let's consider sector-related risks. A slower electric vehicle penetration rate and higher-than-expected production from Lithium producers could create a surplus situation.

Technology developments can also have an adverse effect: first, stronger than expected sales of Sodium batteries (low-density), displacing Li atoms by Na. Second, faster growth of LFP batteries that use less lithium than NCM ones could limit the Li demand. Finally, and this is a longer-term risk, a generalization of DLE (Direct Lithium Extraction) techniques could considerably shorten the production cycle of Lithium from Brines.

Conclusion

I see Lithium as one of the best metals for the current decade, due to the strong demand from electric vehicles but also as the deployment of stationary Li-batteries to stabilize renewable power plants is gaining traction. The Lithium market is controlled by a limited number of producers. Pilbara could place itself among the five largest producers. While the sector has seen a significant price correction translating into pressures on listed equities, I do believe that Pilbara Minerals' strong production roadmap will act as a buffer in the face of current Lithium price uncertainties.

My DCF valuation model indicates the upside potential for a reasonable commodity price trajectory. The balance sheet is very healthy: the net cash position and a rebounding cash-flow generation starting the calendar year 2025 will allow for more cash distribution for shareholders and open options for M&A (to limit the geographical concentration of its assets). To me, it's a Buy.

For further details see:

Pilbara Minerals: A Growth Story With Upside Potential