PILBF - Pilbara Minerals: Ambitious Growth Plans And Strong Finances Make It A Buy

2023-10-30 03:28:51 ET

Summary

- Lithium shortage is driven by new demand for lithium-based batteries.

- Pilbara Minerals is positioned as a leading spodumene producer with ambitious growth plans and strong finances.

- There is a current downturn in the lithium price, creating fear and a buying opportunity.

I have been investigating the lithium space for some time. I have come to believe we are in the middle of a years-long lithium shortage driven by the new demand for lithium-ion batteries. Between 2020 and 2022 the price of lithium carbonate skyrocketed, going from under $8/kg to well over $60/kg . The EV and ESS markets are both growing very rapidly and will create sustained demand for lithium.

Pilbara Minerals ( OTCPK:PILBF ) may be the single best investment opportunity to take advantage of this lithium demand. They are the largest pure-play spodumene producer. In the last year, they sold spodumene for an average price of US$4,447 at a cost of US$687, giving them an 84.5% profit margin.

{kind=link}

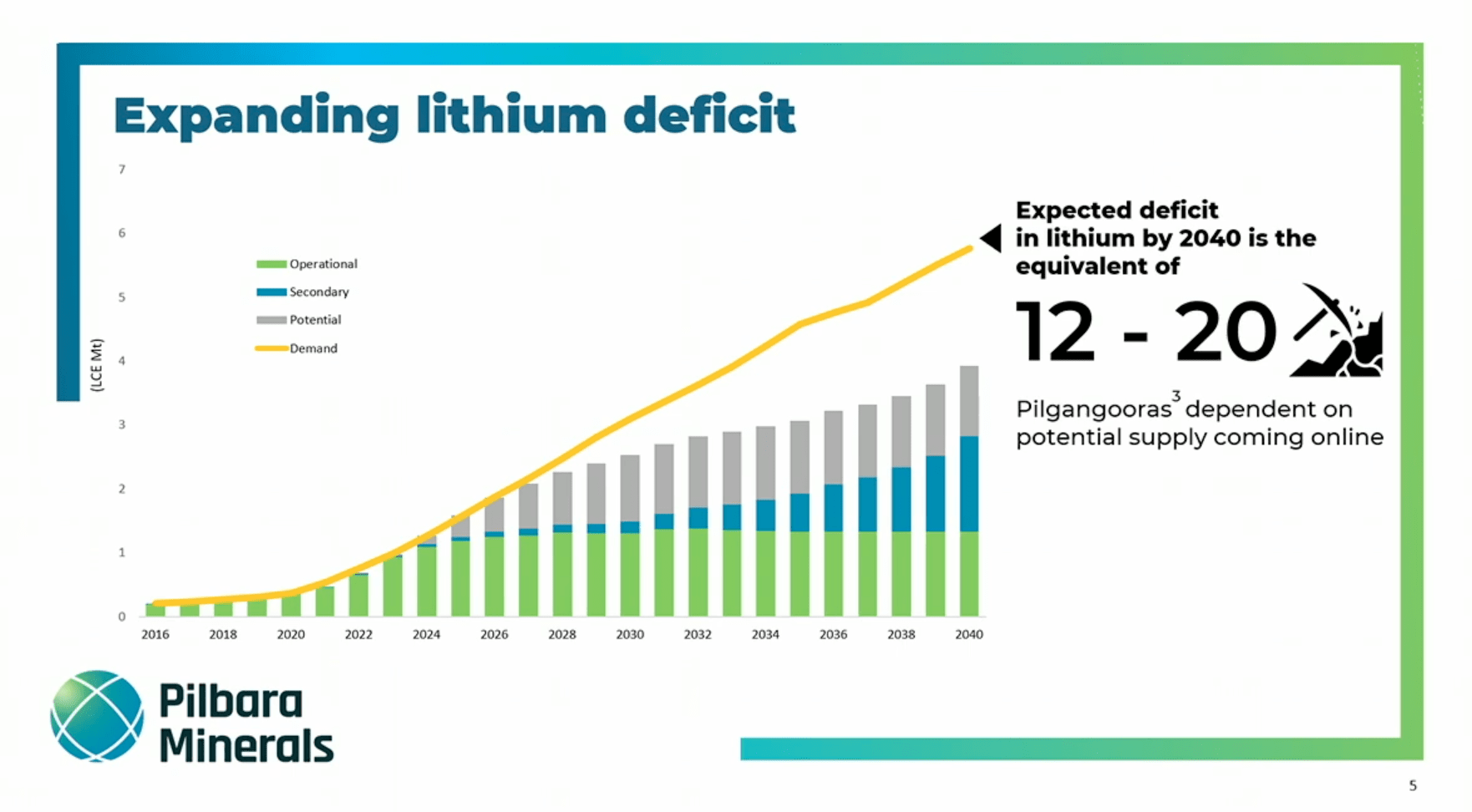

Lithium Supply Deficit (Pilbara Diggers and Dealers Presentation)

If the EV and ESS markets drive a lithium tailwind for the next half-decade, then Pilbara has the best sail to catch this wind. Pilbara is a company that has demonstrated operational strength over time. Furthermore, they are undervalued given some recent fears around the lithium market.

Pilbara Minerals is the Largest Spodumene Pure Play

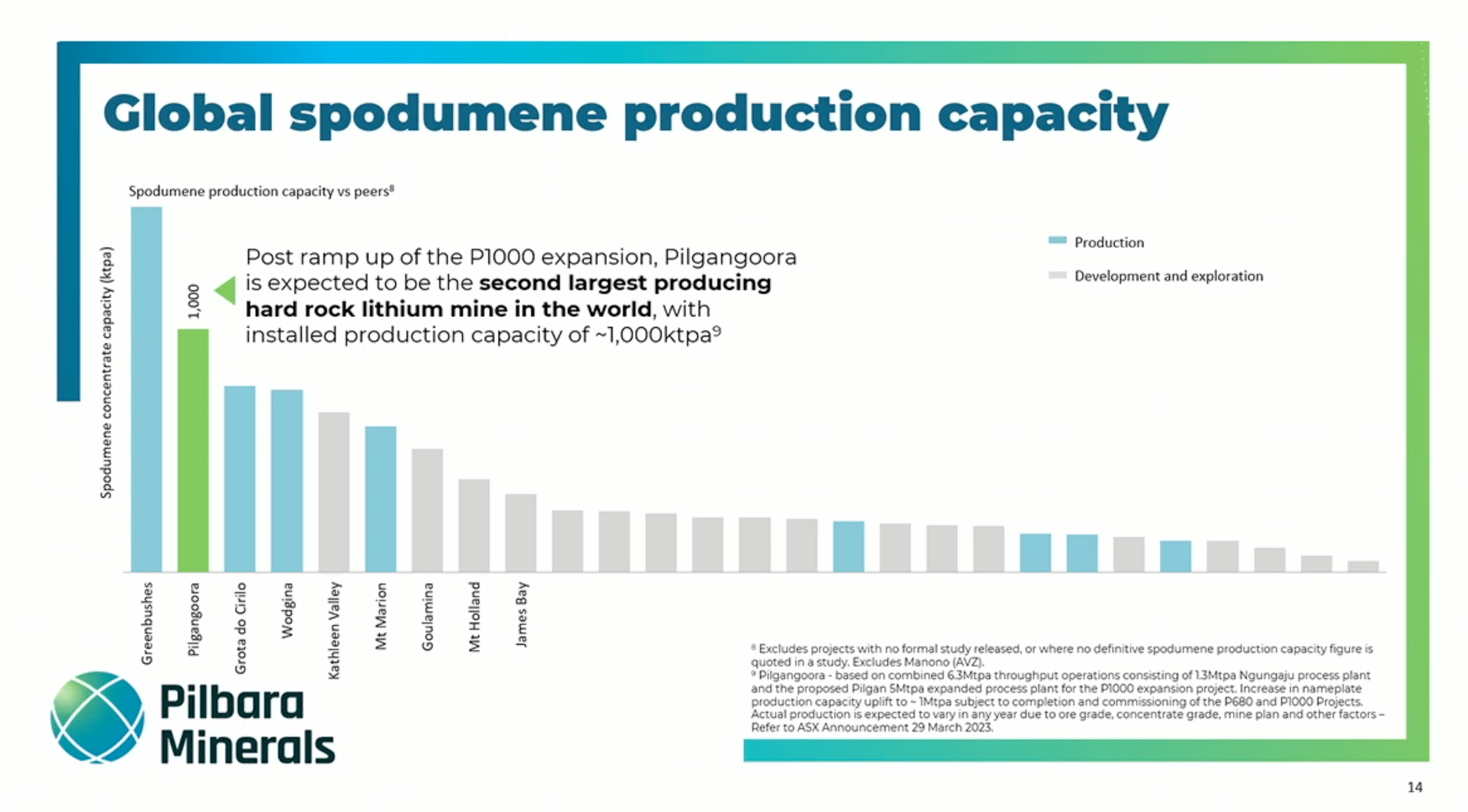

Pilbara Minerals owns and operates the Pilgangoora spodumene mine in Western Australia. This is the second-largest spodumene mine in the world in terms of lithium production, after the Greenbushes mine , and the largest in terms of resource size.

{kind=link}

Largest Spodumene Mines (Pilbara Diggers and Dealers Presentation)

Lithium is primarily mined from two sources: brines and hard rock. Brines are waters that are rich in lithium salts. Albemarle ( ALB ) operations in the Salar de Atacama in Chile are an example of brine mining. There are two hard rock minerals currently being mined: spodumene and lepidolite. Spodumene is the preferred minera l as it has more lithium, is more profitable to mine, and is less environmentally destructive.

So, what makes Pilbara a great opportunity? There are five factors that make Pilbara a great long-term investment.

Pilbara Minerals Has a Great Asset

A great mining company needs a great asset. Pilbara has a fantastic spodumene asset. The deposit is very large. They recently updated their resource size to 413.8Mt grading 1.15% Li2O. This largest spodumene deposit in the world is being mined.

Size is important because it allows for scale and longevity. A small resource will be capped in the annual volumes of material it can produce. A large resource can grow, justifying future capital expenditure and expanding capacity. The Pilgangoora resource also has a fantastic grade. 1.15% Li2O is above average. We see mines seeking to go into production with grades lower than 1%. For example, Rock Tech Lithium has a grade of 0.88% Li20. Mining lithium at a grade of less than 1.0% will create challenges in concentrating the spodumene.

Pilbara Minerals is a Great Operator

When comparing a mining company to any other, the fundamental business is about creating output. Pilbara's operational skills stand out in the lithium spodumene space. Their ability to get a mine through construction and into production and consistently scale up their output sets them apart.

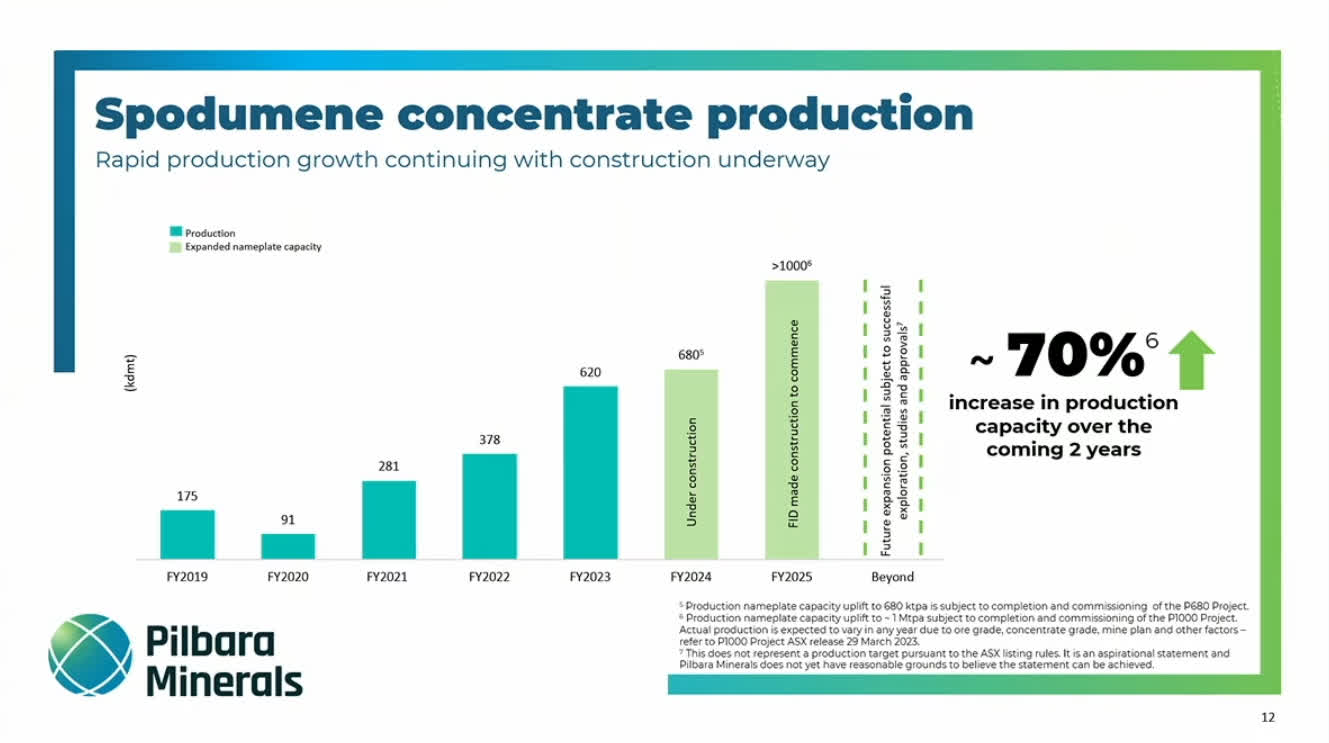

Pilbara came online back in 2019. Since then, they have been steadily increasing their output every year. In FY2023 they grew their output from 378 kt to 620 kt of spodumene concentrate.

{kind=link}

Pilbara Minerals Spodumene Output (Pilbara Minerals Diggers and Dealers Presentation)

Mining is hard. Looking around the lithium space we can see many mining companies facing setbacks and difficulties. Some miners face permitting problems. For example, Critical Elements ( OTCQX:CRECF ) released a PEA study back in 2011 but is not in production yet.

Other miners face jurisdictional risk like Leo Lithium ( OTCPK:LLLAF ) located in Mali. They have faced a number of setbacks in recent months due to the actions of the Mali government. Some other miners face operational problems. For example, Core Lithium ( OTCPK:CXOXF ) came online in Nov 2022 but is struggling with its ramp-up. Similarly, Allkem's ( OTCPK:OROCF ) Mt Cattlin Mine has recently struggled with its operations producing less spodumene than expected.

Again, mining is hard. Spodumene mining requires operating several plants in concert, like crushing, separating, and floatation. Pilbara is one of the few lithium players that has consistently delivered on its operations, producing large quantities of high-quality spodumene concentrate.

Pilbara Minerals Has Great Finances

In FY2023, Pilbara sold spodumene for an average price of USD $4,447/t (SC 5.3) across the year, equating to USD $5,034/t (SC6). All numbers are from their recent annual report . You can see their costs for the last year.

| Year |

| Cost (ex royalties and freight, AUD) |

| Cost (ex royalties and freight, USD) |

| Cost (inc royalties and freight, AUD) |

| Cost (inc royalties and freight, USD) |

| FY2022 |

| $555 |

| $350 |

| $844 |

| $531 |

| FY2023 |

| $613 |

| $386 |

| $1091 |

| $687 |

Their operational costs increased a little because of supply and labor shortages, while their royalty cost increased as their selling price increased. If their real cost/t averaged at $687 that means they had an 84.5% profit margin on their spodumene.

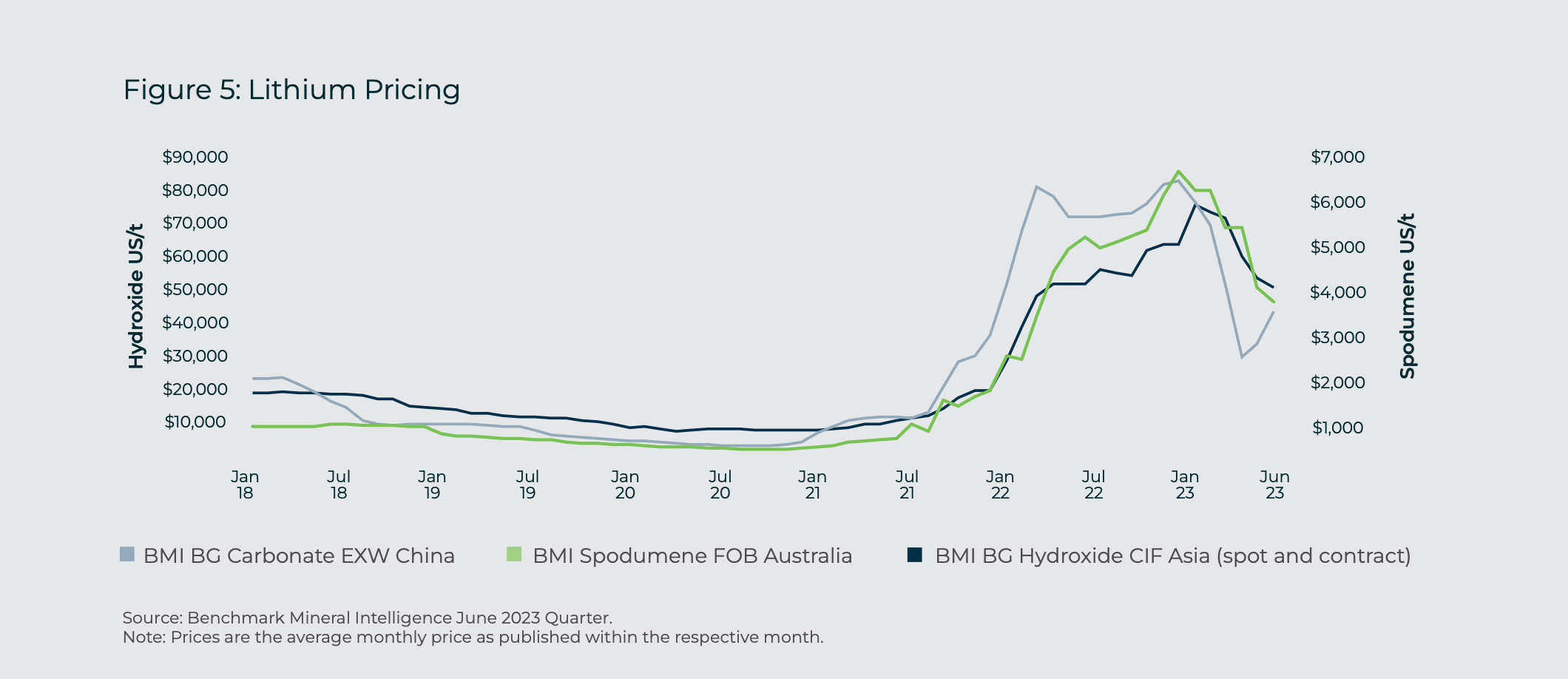

Pilbara is a low-cost producer of spodumene and will continue to make profits as long as the price of spodumene is above $700/t. Benchmark Mineral Intelligence recently published stating that the all-time average market high was $6401/t in Dec 2022, and the price is now around $3,120/t. I expect the lithium spodumene price to be $2000/t as a floor.

{kind=link}

Lithium Prices (Pilbara Annual Report)

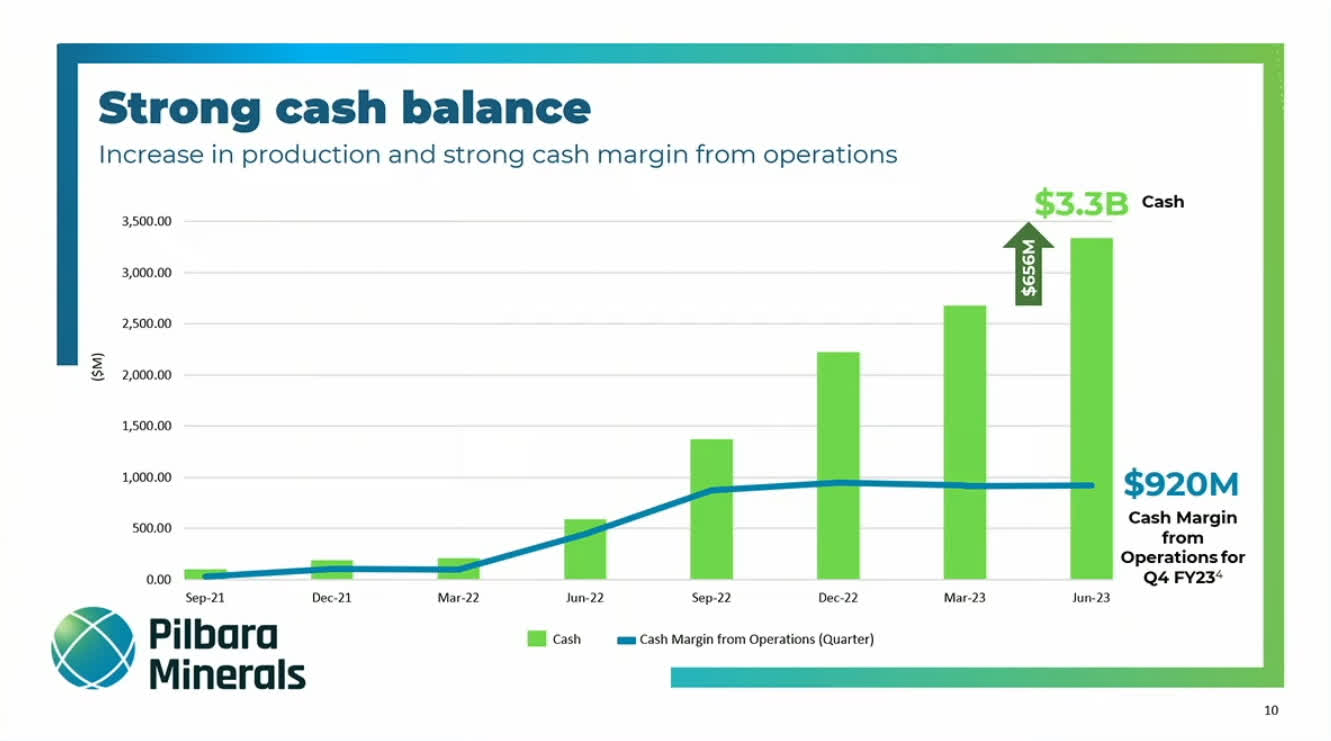

The upshot of this is that Pilbara is in a strong financial position. In just the last quarter they made AUD $920 million in cash and ended with AUD $3.3 billion in cash. They have AUD $272 million in debt.

{kind=link}

Pilbara Cash Margins (Pilbara Diggers and Dealers Conference)

This strong cash position will allow Pilbara to make good capital decisions going forward. Pilbara recently announced a new capital management framework. In this announcement, they initiated the first dividend.

Pilbara Minerals Has Ambitious Growth Plans

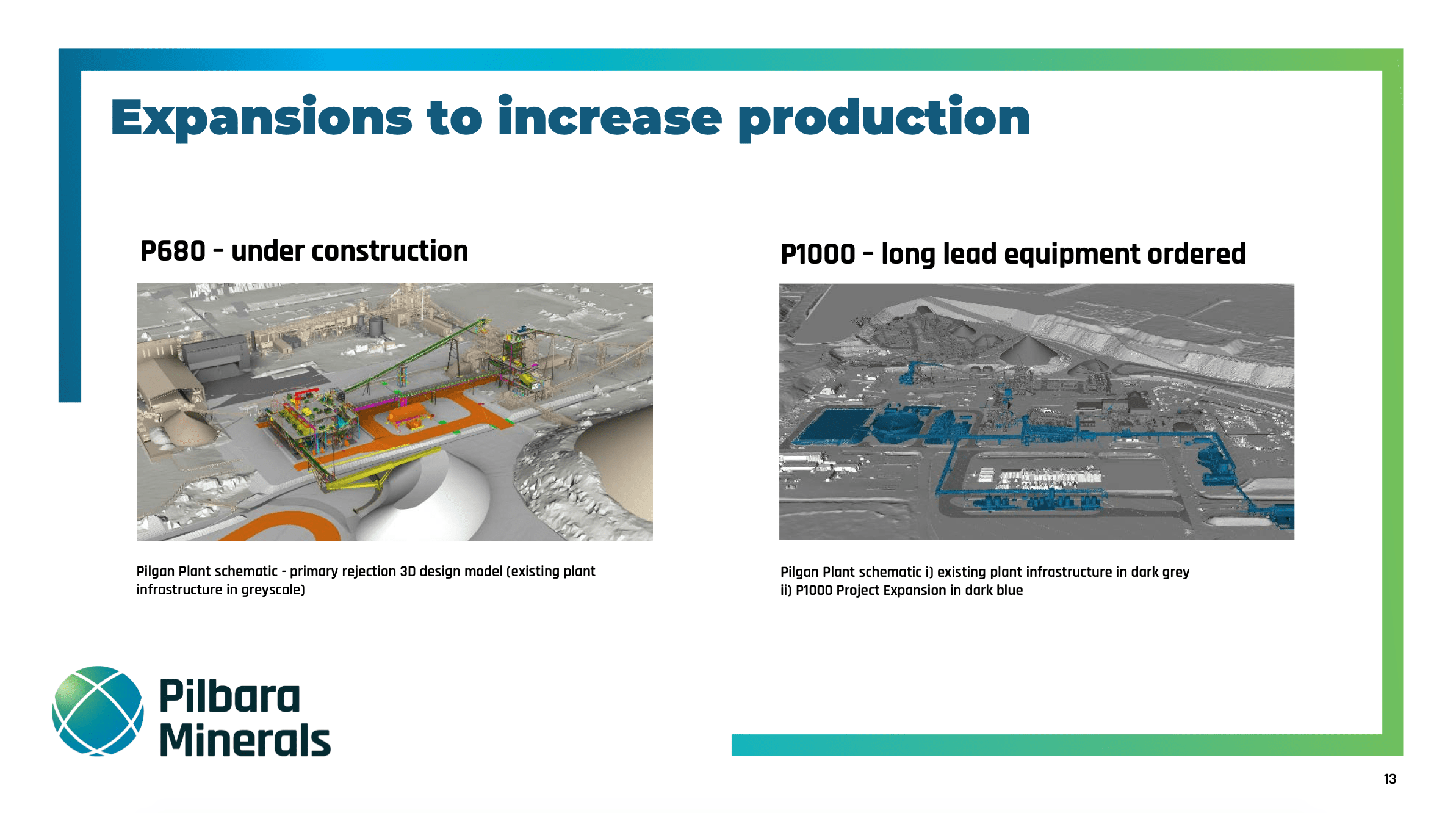

Pilbara has four major ongoing growth projects. First, they are expanding their spodumene processing capacity with the P680 project. This new plant will bring their nameplate capacity to 680,000 t/year. It is under construction and should be complete by Q1 2024. The expected CAPEX was AUD $297.5 million.

{kind=link}

Pilbara Growth Plans (Pilbara Diggers and Dealers Presentation)

The next growth project is P1000, which is another processing plant that will bring Pilbara's nameplate capacity up to 1,000,000 t/year of spodumene concentrate. They declared FID in March 2023 and expect to be operational by March 2025. The estimated CAPEX is AUD $560 million. If spodumene prices are around $3000/t USD then Pilbara should have ~$3 billion USD in revenue, with great margins.

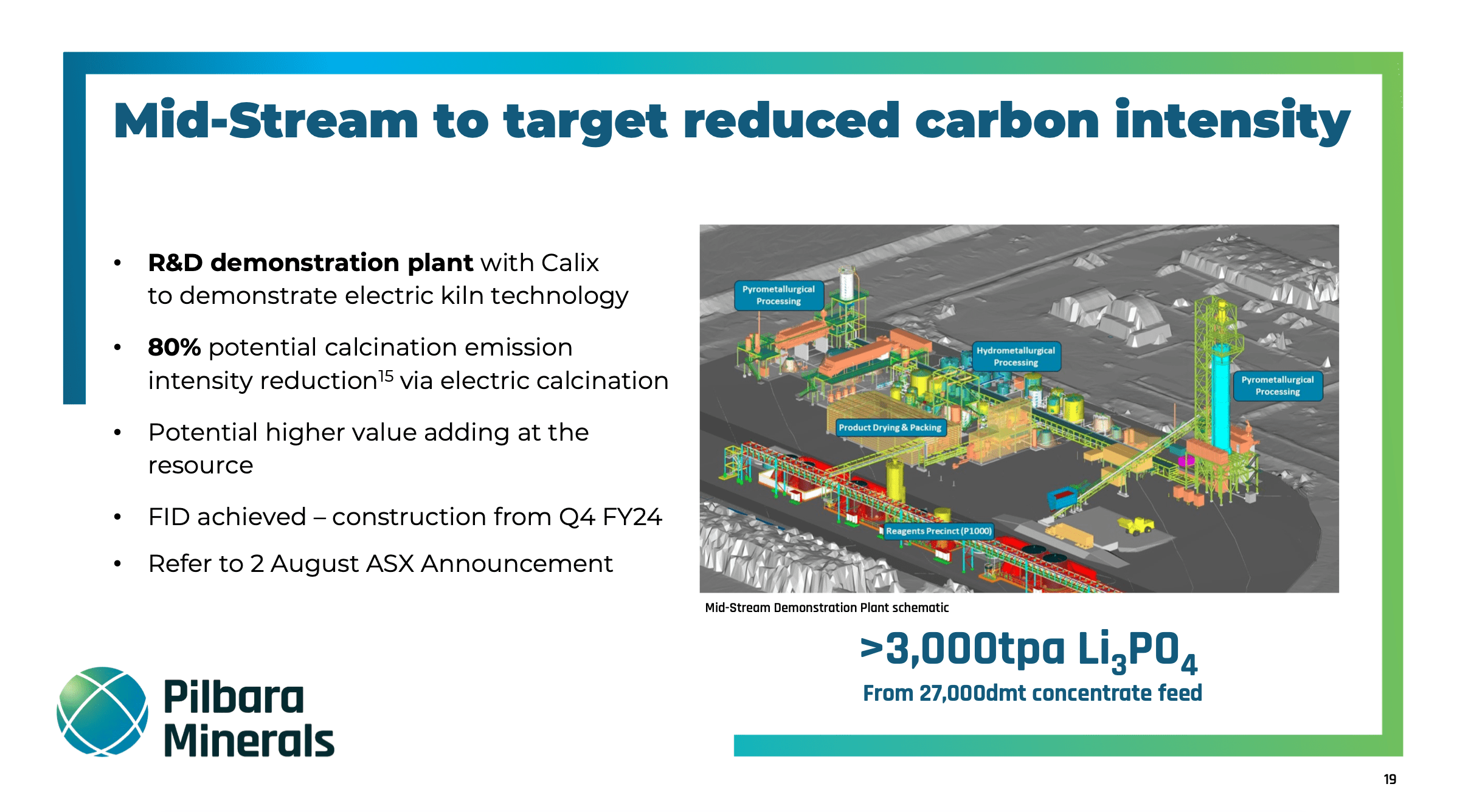

Third, Pilbara is experimenting with midstream processing. They have a joint venture with Calix to process spodumene into lithium phosphate (Li3PO4). Normally converters purchase the SC6 and convert it. The lithium phosphate is a middle step. It is more lithium-dense than SC6 and is easier to convert than SC6, so it should sell at a premium.

{kind=link}

Lithium Phosphate (Pilbara Diggers and Dealers Presentation)

Pilbara declared FID on the demo plant in August 2023. The estimated CAPEX is AUD $104.9 million. The Australian government is funding this project with a $20 million grant. Pilbara will fund $67.4 million of the remaining cost.

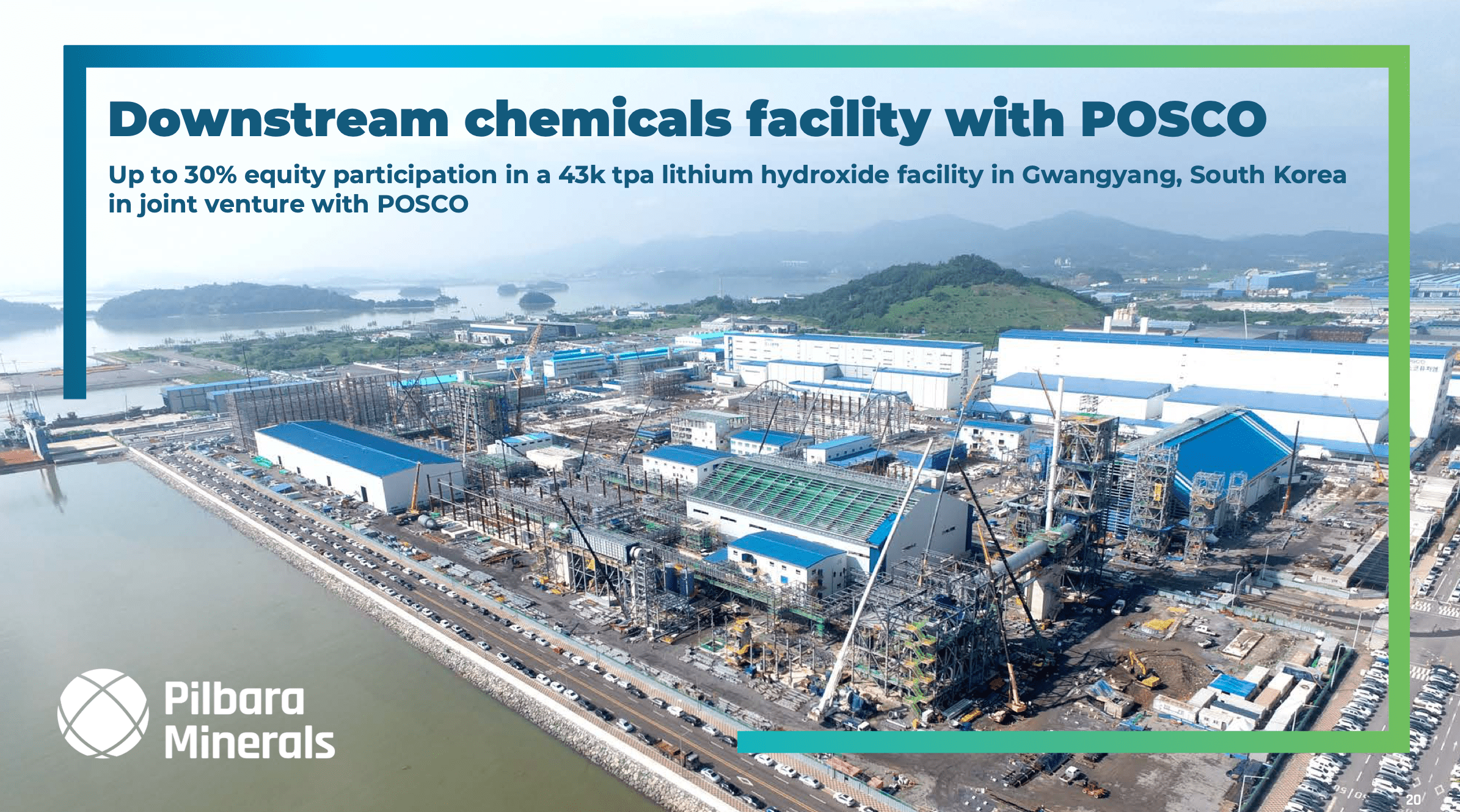

The fourth growth project is a JV with POSCO Holdings ( PKX ) to build a lithium hydroxide facility. POSCO is an experienced chemical producer and has been partners with Pilbara for many years. Pilbara can own 30% of the facility, which will produce 43,000 t/year of LiOH. Currently, they have paid AUD 79.6 million for an 18% ownership stake.

{kind=link}

Hydroxide Capacity (Pilbara Diggers and Dealers Conference)

Putting this all together, Pilbara has plans to aggressively grow its spodumene capacity and create new chemical capacity. They have the ability to grow their capacity further after the P1000 project is complete.

Pilbara Minerals have Great ESG

Pilbara Minerals are part of a new wave of mining companies. In the past, there was a widespread perception that mines are bad for the world. Many of the newer mining companies are seeking to do mining in sustainable and environmentally friendly ways.

{kind=link}

Pilbara's Sustainability Metrics (Pilbara Diggers and Dealers Presentation)

To give a few examples. Pilbara has just completed a large solar farm that will create 6MW of power for their operations. This is expected to replace 3.8 million liters of diesel a year. Pilbara has also been focused on community engagement . They recently installed solar panels and batteries at a local school, saving the school hundreds of thousands of dollars a year.

Discounted Cash Flow Analysis

So, Pilbara is a mining company with great assets and great operations. They have demonstrated they are skilled operators and have ambitious growth plans that will capitalize on the coming demand from lithium.

So, shouldn't they be expensive? It is my opinion that the fears around the lithium market right now are putting Pilbara on sale.

To get a handle on the appropriate price to pay for Pilbara we need to make some assumptions. I will build the model from the ground up here. All the numbers here will be in USD unless otherwise stated.

First, we assume that Pilbara grow its spodumene production to 680,000 t in 2024, then 950,000 t in 2025, slightly under their P1000 target. Then, we assume they will keep growing their capacity to at a rate of 18% CAGR; They have achieved a 28% CAGR between 2019 and 2023.

| Year |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| 2029 |

| 2030 |

| 2031 |

| Spodumene (kt) |

| 680 |

| 950 |

| 1121 |

| 1328 |

| 1561 |

| 1841 |

| 2173 |

| 2565 |

We assume that Pilbara will pay 14% in taxes on their revenue. We also assume they will pay US$350 million in CAPEX in 2024 and then grow it 5% each year. They paid AUD 408 million last year.

We will run our DCF analysis for eight years and discount the cash by 12%.

The key assumption is the spodumene price, and connected to that is the cost of production. Last quarter Pilbara's sale price dropped to $2,240 (SC5.3). The previously cited Benchmark paper had an average price of spodumene (SC6) at $3,120/t. We will take a spodumene of $2900 as the base case, $2000 as the bear case, and $3800 as the bull case. The cost of production will be adjusted a bit for the price. First, the numbers for the base case.

| Year |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| 2029 |

| 2030 |

| 2031 |

| Price (SC5.3) |

| 2900 |

| 2900 |

| 2900 |

| 2900 |

| 2900 |

| 2900 |

| 2900 |

| 2900 |

| Cost/t |

| 640 |

| 670 |

| 700 |

| 730 |

| 750 |

| 770 |

| 790 |

| 810 |

| Profit (US$ billion) |

| 1.53 |

| 2.12 |

| 2.47 |

| 2.87 |

| 3.36 |

| 3.92 |

| 4.59 |

| 5.36 |

| Tax (US$ million) |

| 276 |

| 385 |

| 455 |

| 537 |

| 633 |

| 747 |

| 822 |

| 1041 |

| CAPEX |

| 380 |

| 399 |

| 418 |

| 439 |

| 461 |

| 484 |

| 509 |

| 534 |

| FCF |

| 880 |

| 1333 |

| 1592 |

| 1893 |

| 2260 |

| 2690 |

| 3194 |

| 3784 |

| DCF (12) |

| 786 |

| 1063 |

| 1133 |

| 1203 |

| 1282 |

| 1363 |

| 1444 |

| 1528 |

The net present value of these cash flows is $9.8 billion. They have $2.2 billion of cash and $181 million of debt on their balance sheet. That means it would be reasonable to pay $11.8 billion for Pilbara, or $3.92/share. Currently, they are trading at $2.47.

I won't lay out the charts, but the bear case gives the cash flows a value of $4.7 billion and the bull case gives the cash flows a value of $15.5 billion.

| Case |

| SC5.3 Price |

| NPV (USD billion) |

| Fair Share Price |

| Bull |

| $3800/t |

| $17.5 |

| $5.82 |

| Base |

| $2900/t |

| $11.8 |

| $3.92 |

| Bear |

| $2000/t |

| $6.7 |

| $2.23 |

All this says that if my base case is correct then shares in Pilbara are well undervalued and they stand to make a ~70% return.

Comments on the Price of Lithium

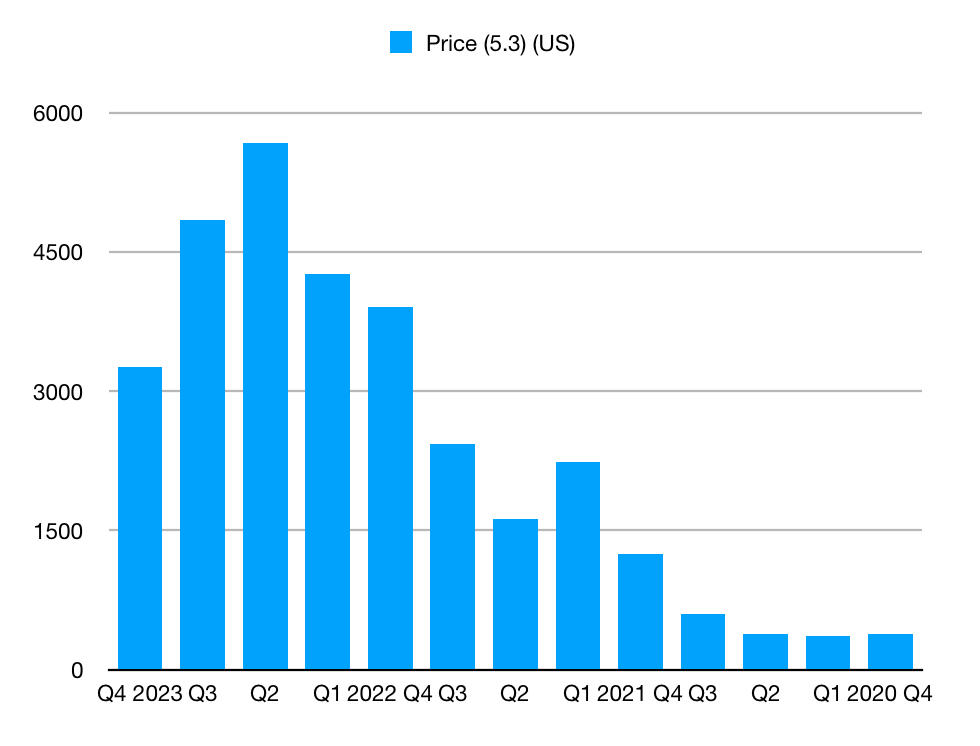

I have made a chart of the Pilbara's quarterly sale price over the last three years, taken from their quarterly reports.

{kind=link}

Pilbara SC5.3 Sale Price (Author)

Clearly, these prices have been very volatile. Back in 2020, Pilbara was selling spodumene for around $400/t, as were most spodumene producers. The price was somewhere below $800/t for a long season before 2021 and Pilbara had a hard time making a profit when they began production in 2019.

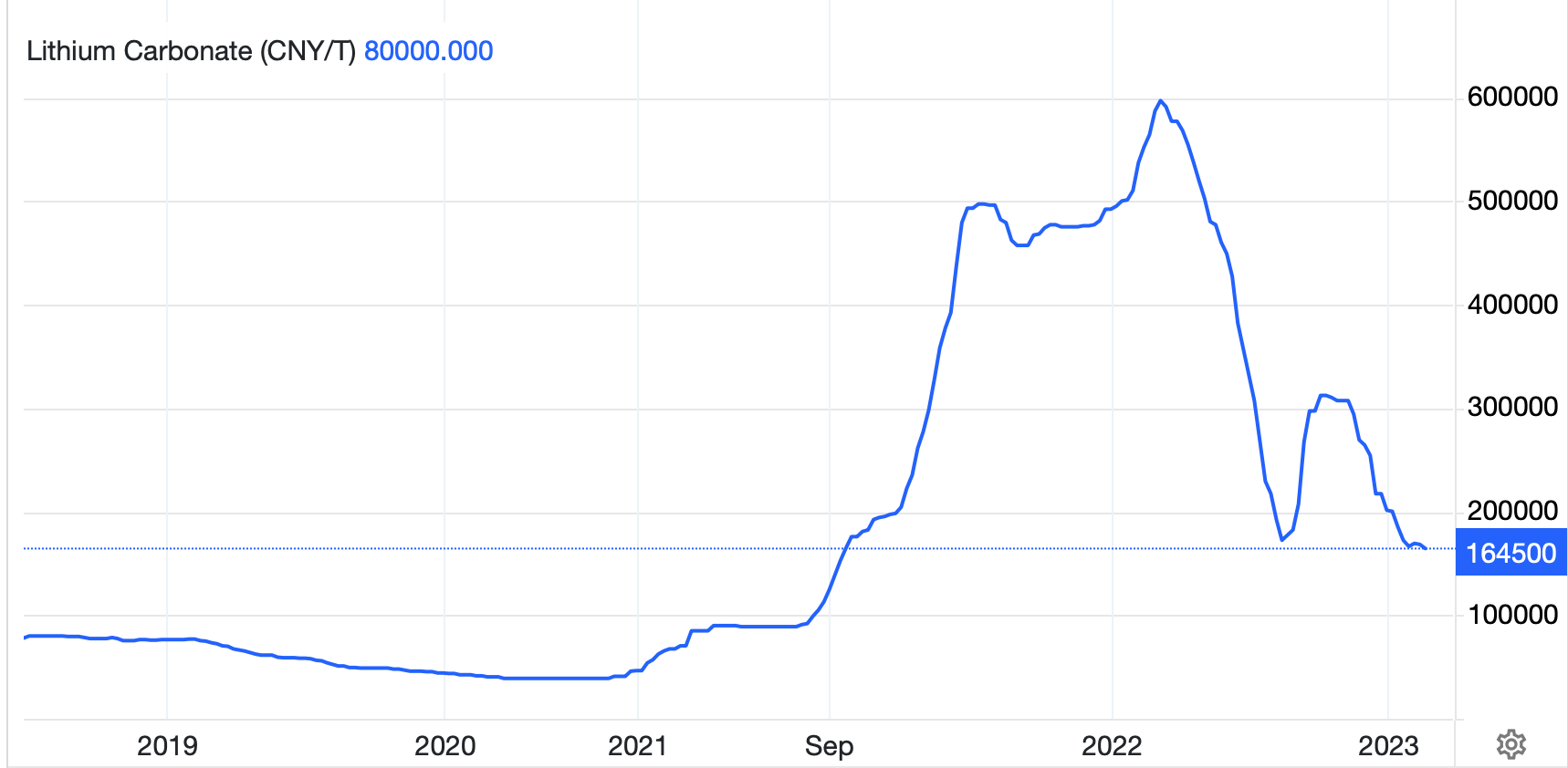

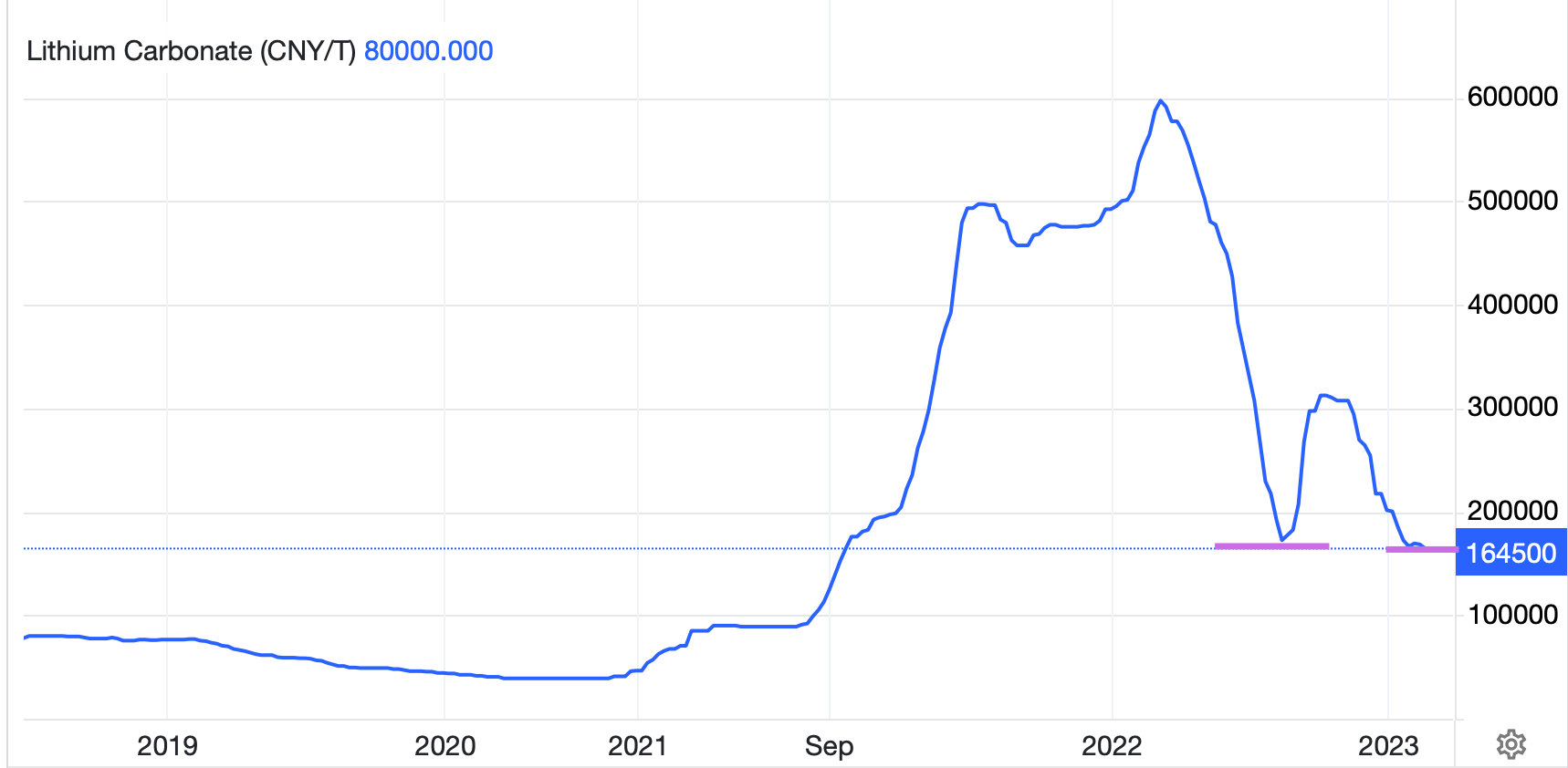

2021 saw a massive spike in demand for lithium, driven primarily by an increase in EV sales. Below you can see the chart from tradingeconmics.com,

{kind=link}

China Lithium Carbonate Spot Price (www.tradingeconomics.com)

The worry about investing in Pilbara is that the lithium price could sink back down to the lows of 2020. If this happened then we would definitely be overpaying. So what's the outlook on the price of lithium?

A Long-term Demand For Lithium

Batteries have several minerals that go into making them like nickel, cobalt, iron, manganese, and lithium. There are different batteries with different chemistries and thus use different elements, but all these batteries use lithium.

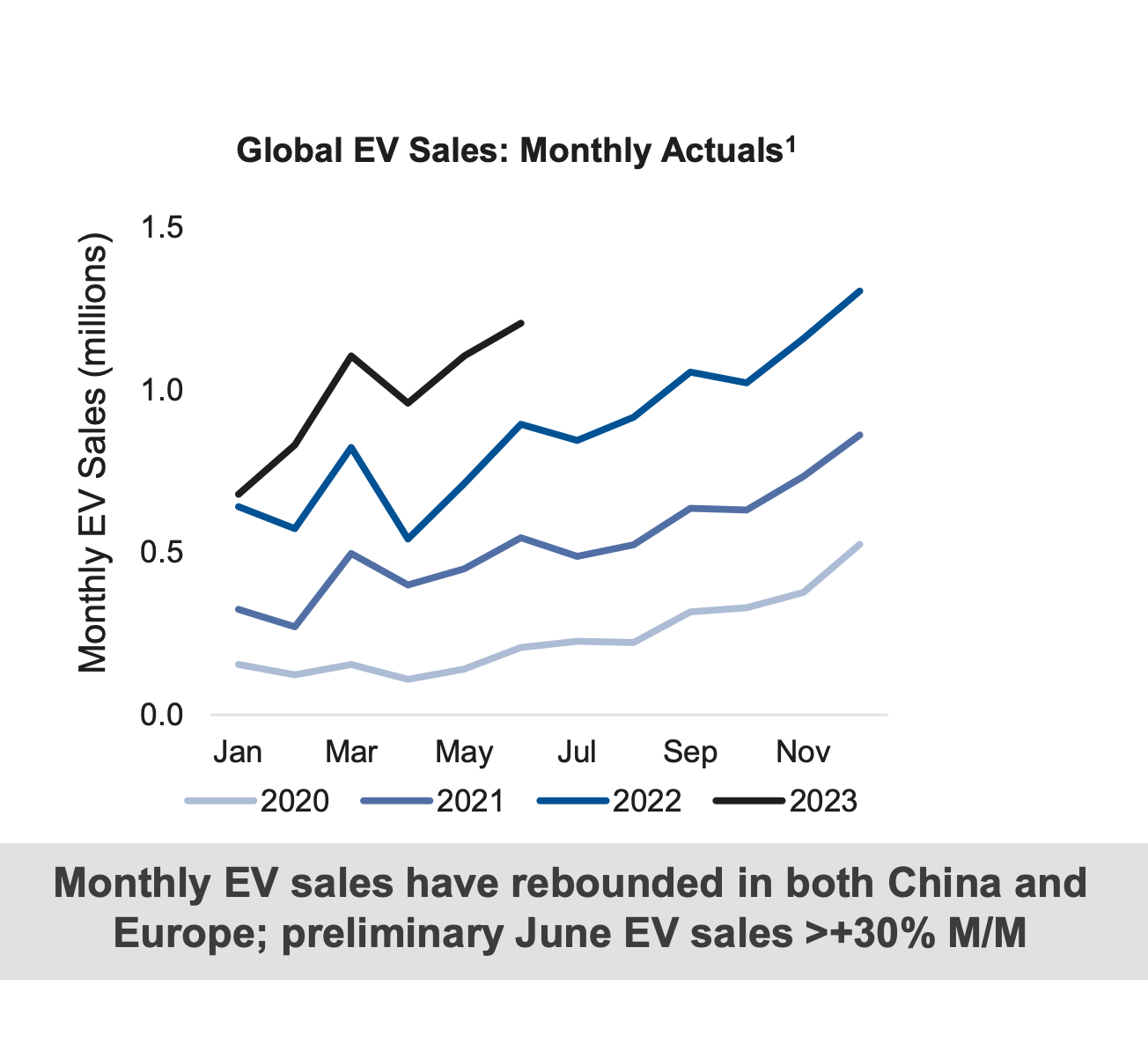

Demand for EVs has been increasing. Despite the recent pullback in both China and the US economies, the demand for EVs is not slowing down. Albemarle publishes EV sales numbers. You can see from the charts below that the monthly sales numbers are still growing ~30% M/M and Y/Y. This demand for EVs translates directly into demand for lithium.

{kind=link}

Global Monthly EV Sales (Albemarle Investor Presentation)

Lithium's Special Role in Batteries

In the making of batteries, lithium is special. For one, all the different chemistries of the various batteries, are lithium-ion batteries. That is, lithium is a major ingredient in all of the batteries being used in commercial EVs.

There are basic reasons for this based on chemistry. Lithium is number three on the periodic table making it the lightest metal and also the most energy-dense.

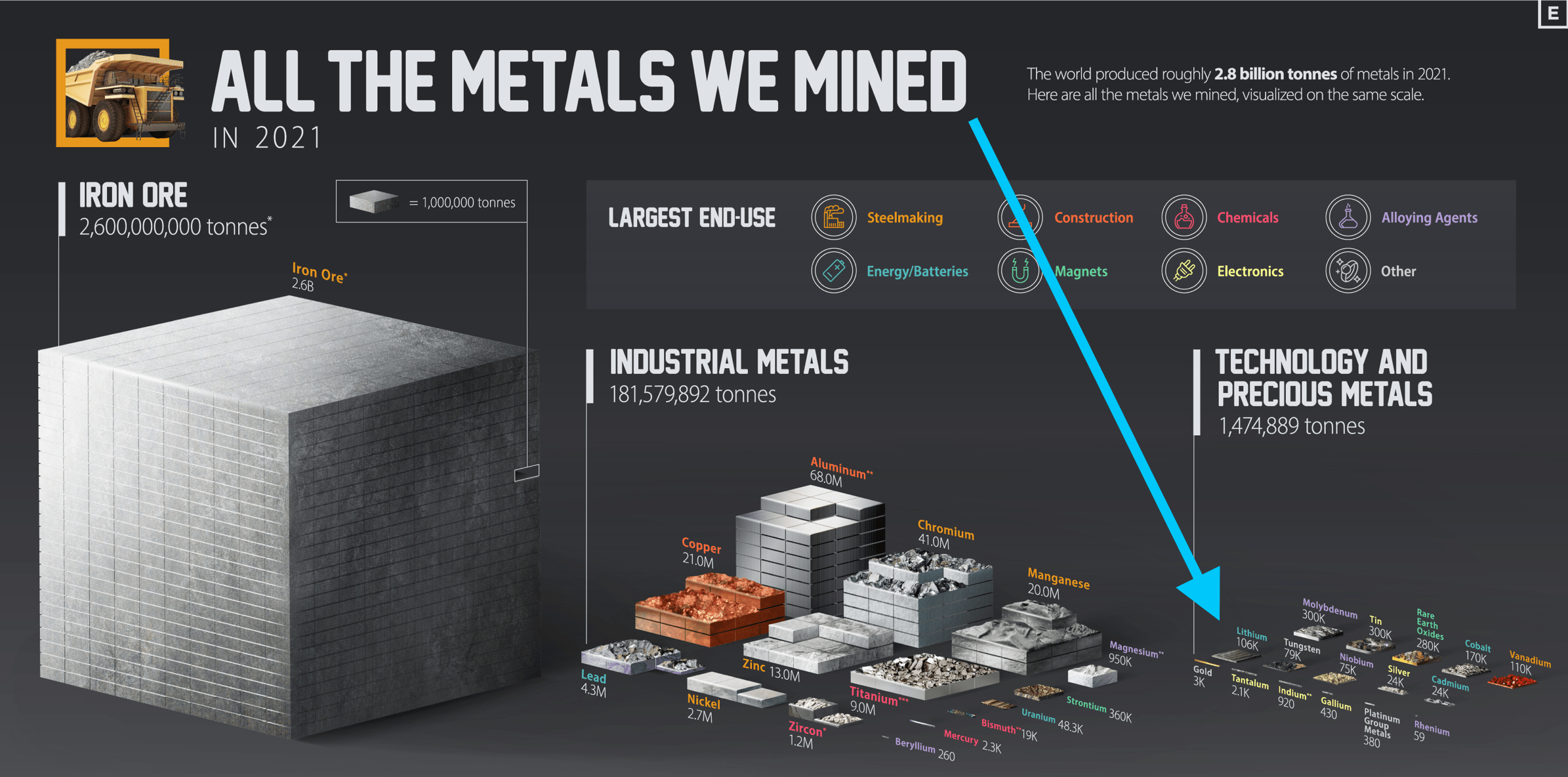

The other special thing about lithium is that relatively speaking, the lithium mining industry is small and immature. There is a nice graphic from Benchmark that shows the relative size of all metals mined in 2021. You can't see the lithium pile because the resolution isn't good enough on Seeking Alpha, so I've added an arrow so you can see where the lithium is. In 2021 103,000 t of lithium were mined, which is not much.

{kind=link}

The Metals We Mined (Benchmark Material Intelligence)

The Coming Lithium Shortage

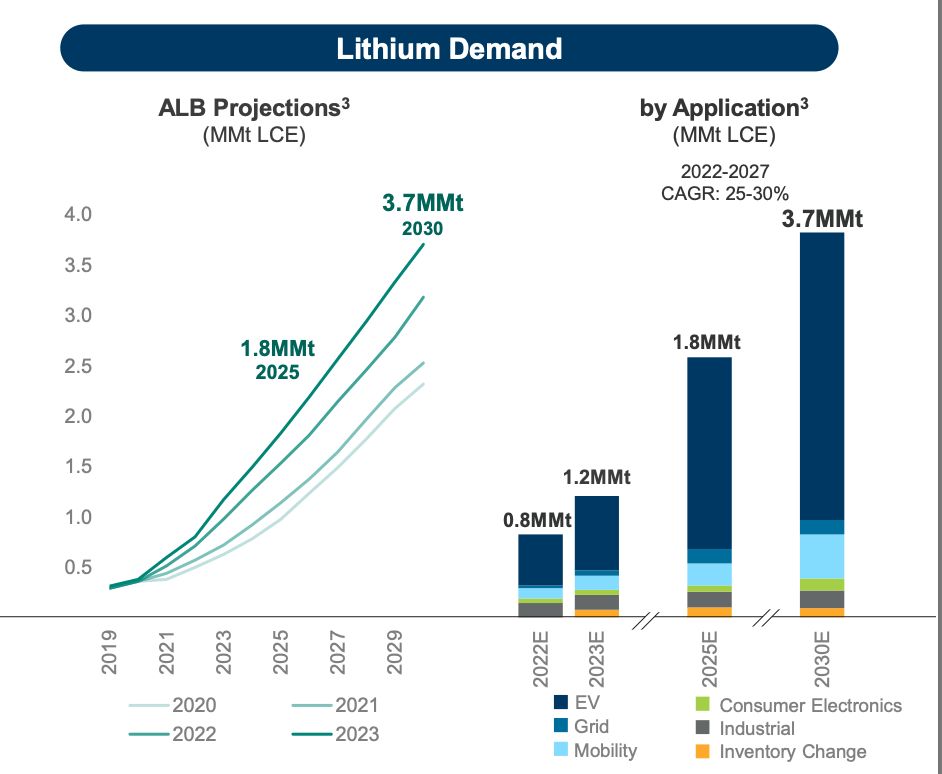

This small lithium industry needs to grow fast. Below is a chart from Albemarle about the amount of lithium produced between 2022 and 2030. They speak in LCE terms, which means lithium carbonate equivalent.

{kind=link}

Albemarle Lithium Demand Projections (Albemarle Investor Presentation)

This chart tells us that in 2022 the global lithium industry produced 0.8MMt of LCE, that is 800,000t of LCE. In 2023 that number should be 1.2MMt. They see lithium demand at 1.8 MMt by 2025 and 3.7 MMt in 2030, meaning a 25–30% CAGR in demand. This demand will be driven by EV and ESS growth.

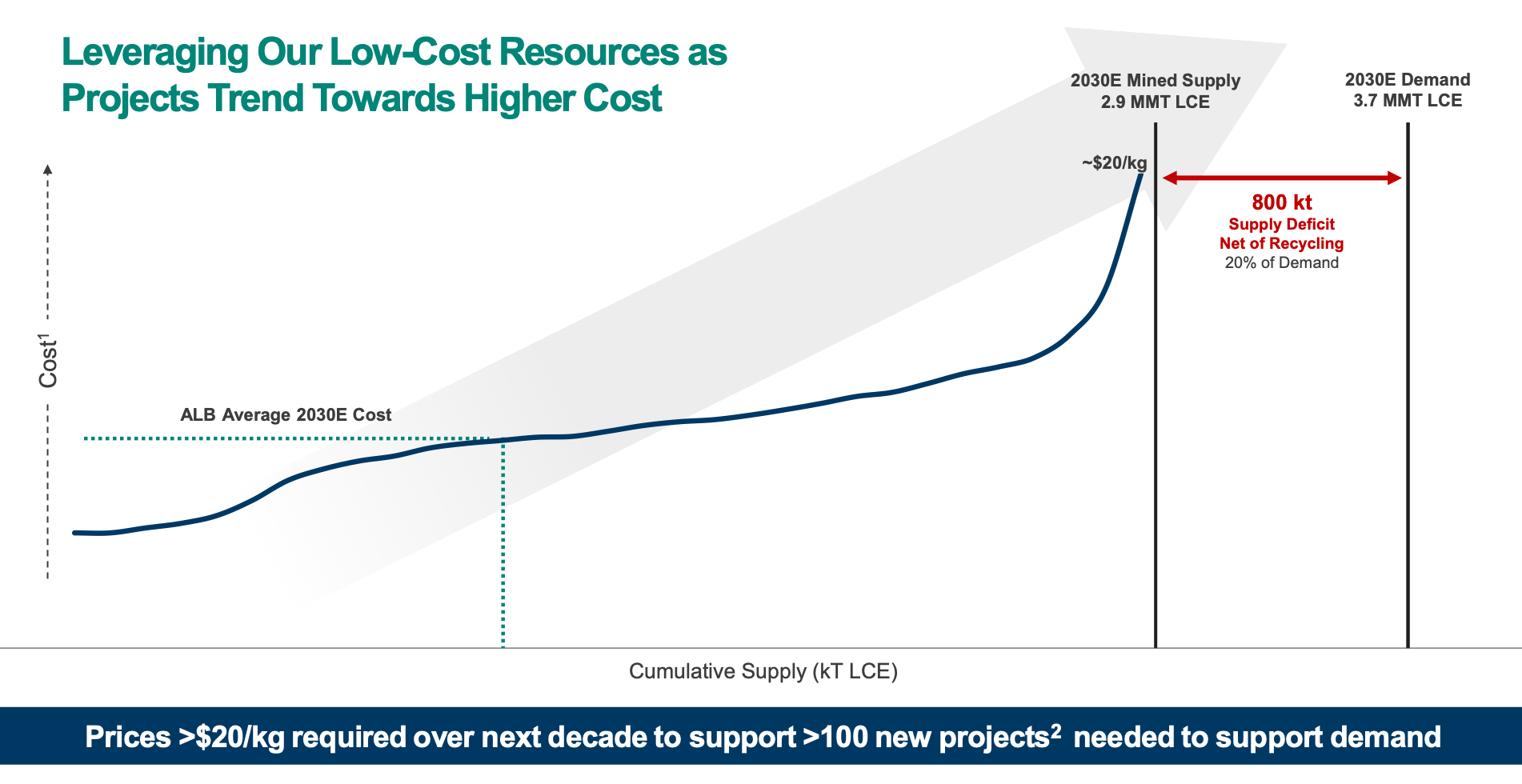

Where does this leave us? Albemarle's prediction is that there will be about 2.9MMt of LCE supply giving an 800,000 t shortfall by 2030. That is, the shortfall could be as large as the entire lithium industry in 2022. The basic reason for this shortfall is that lithium mines take 5–10 years to come online.

{kind=link}

Lithium Supply Gap (Albemarle Investor Presentation)

Their conclusion is that the price of lithium carbonate will be over $20/kg because this is the price required to incentivize more supply. As long as there is a supply gap lithium should be sold at a premium. For reference, this translates to $2200/t for spodumene, over our bear case.

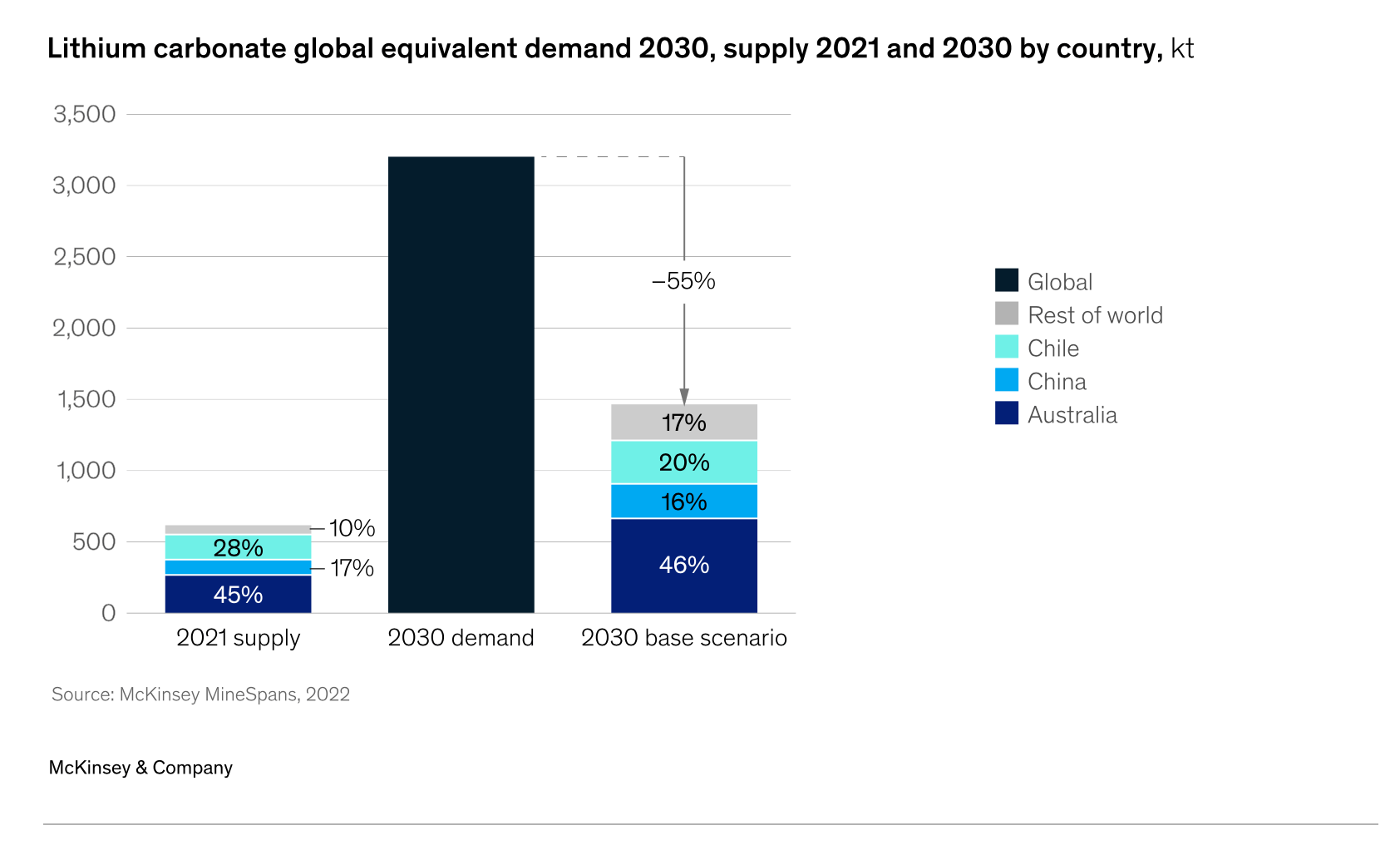

Albemarle is not the only one making predictions like this. McKinsey and Company make similar predictions . They calculate the 2021 LCE supply as 600 kt. By 2030 they predict 3.25 MMt of demand and only 1.4 MMt of supply, giving about 1.8 MMt of shortfall.

{kind=link}

Lithium Shortfall in 2030 (McKinsey Website)

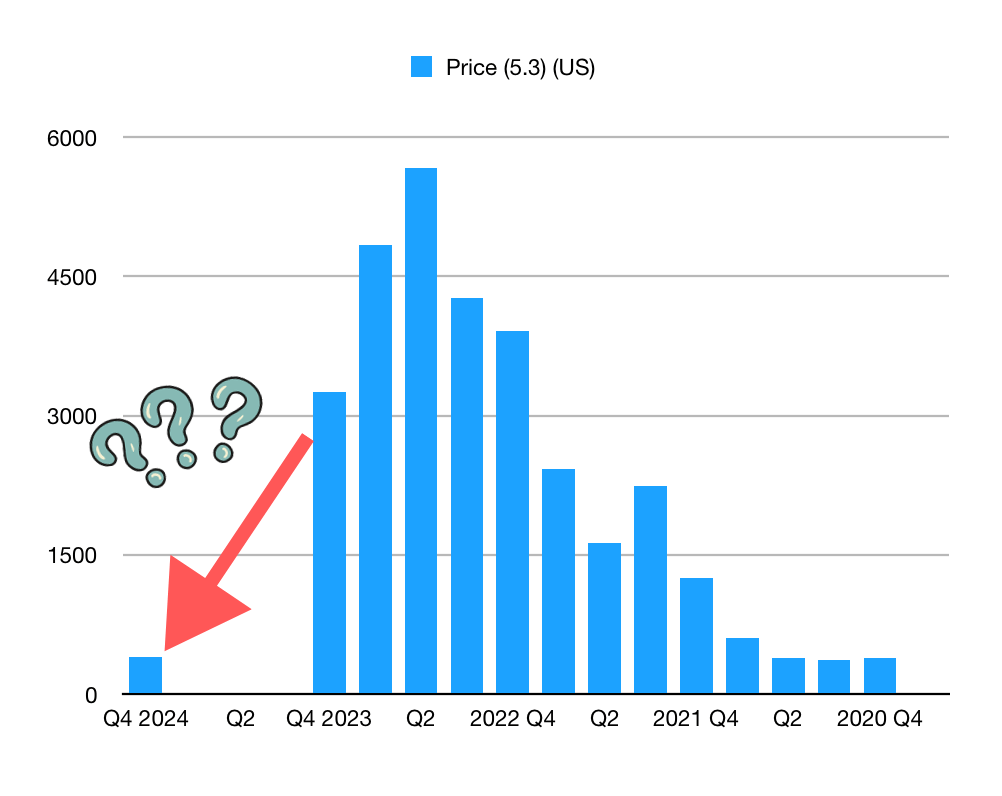

The fear is, that the price of lithium will crash. Pilbara was selling spodumene at $400/t before. If lithium is a commodity, why won't it go back to $400/t?

{kind=link}

Possible Lithium Price Crash (Author)

Lithium prices won't return to $400/t because of the ongoing supply deficit. We are in an era existing where lithium miners will make a lot of money.

This is the long-term picture. There are some short-term market factors that will cause the price to fluctuate. In a recent interview, Pilbara CEO Dale Henderson said that $2000/t is a good number for a floor price of spodumene. Understanding these will help you understand why $2000/t is a good floor number. The current price of $2,240 is a great price, and it's probably the floor. This may not be this high of 2022, but low-cost spodumene producers like Pilbara will be making a great profit.

Short-term Dynamics in the Lithium Market

The question naturally comes up: "If there is long-term demand, then why did the price of lithium crash from $80/kg to $30/kg this year?" Fair question.

{kind=link}

China Lithium Carbonate Spot Price (Training Economics)

The thing to remember is that the lithium market is small and immature compared to many other metals. Undergoing this great surge in demand will create volatility. There are two mechanisms that drive this volatility you should understand.

Marginal Lithium Supply

While the main sources of lithium are spodumene and brine, there are other sources out there. I call these other sources the marginal supply because they are more expensive and more damaging to the environment.

One example of marginal supply is artisanal mining, especially in Africa . This is where people mine ore by hand and ship the ore directly to places like China. Analyst Daniel Jimenez says it is difficult to know how much is happening, but we know that it is happening. Economically, this type of mining is expensive because it requires shipping many tonnes of raw ore. If someone can make a profit from artisanal mining, a low-cost spodumene producer in a tier-one jurisdiction will be making a killing.

Another example of marginal supply is lepidolite. Lepidolite is a lithium-bearing mineral that is mined from rocks like spodumene. The difference is that generally speaking, lepidolite is much lower in lithium content. It usually requires 4-6 tonnage of lepidolite to get the same volume of lithia, so the actual cost comparison on a like-to-like basis means that lepidolite is much more expensive.

The Swing of Marginal Supply

What this means is that when lithium prices are high it will incentivize these marginal sources creating a short-term supply increase. As the price comes down these marginal sources will stop being profitable around the when spodumene prices are $2,000/t or higher.

There are reports that some lepidolite mining has already stopped in some places in China, now that the spodumene price is ~$2500/t. I see that until there is ample high-quality supply, these marginal suppliers will drive volatility in the price of lithium. I see that $2000/t is about the price when these marginal suppliers no longer become profitable, so that is a good floor for our model.

Here is a summary from Joe Lowry , AKA Mr. Lithium:

The ambitious mining of lepidolite in China coupled with an increase in supply of all manner of lithium values from Africa brought the China spot price down to almost a quarter of the peak price. We quickly saw many small lepidolite producers shutdown when spot price went below $40,000/MT.

Inventory Stocking

The second short-term driver of price swings is the stocking and destocking of inventories. Joe Lowry writes:

In my opinion the China lithium carbonate spot price run-up in 2022 to an $80,000/MT equivalent was based on panic buying and irrational behavior by many of the Chinese players. Clearly cathode and cell production in 2022 exceeded even the robust 2022 demand growth leading to a period of de-stocking at the cell, cathode, and lithium raw material level in 2023.

The relative size of the lithium market is small compared to the amount of lithium being sold in batteries. Lithium is held in inventories throughout the value chain. The argument is that as lithium prices crash companies like chemical converters choose to use their lithium stocks rather than purchase lithium on the open market.

Explaining the market cycle of 2020 Fastmarkets commentators wrote this:

In the second half of 2020, lithium demand started to rebound, prices continued to fall until late September as the market destocked, but prices fell to unsustainably low levels, which prompted production cuts – these led to a price rebound as the market switched from destocking to restocking.

Many analysts like Matt Fernley , Daisy Jennings-Grey, and Rodney Hooper cite the destocking argument to explain the recent fall in lithium prices.

Market Summary

The big takeaway here is that despite short-term factors that cause price volatility, there still is a long-term shortage in lithium supply. The reason that the prices have fallen has to do with marginal supply, not long-term supply. As the marginal supplies turn off the price should rebound.

Again, here's what Joe Lowry has to say about the current state of the market.

The battering lithium stocks have taken in the current period of negative sentiment has, in my opinion, created another excellent window to go bargain shopping. This is not investing advice but seems obvious to me. I have added to my favorites this week “because of” not “in spite of” the current metaphorical “blood in the streets.”

Pilbara Summary: A Bad Earnings Call?

Pilbara just posted the quarterly earnings . They had a large drop in Q/Q revenue as they had a drop in their realized spodumene price: $2,240. This is to be expected . The market is afraid that the price will drop even further, but I don't think this is possible. At ~$2.50 price, the shares of Pilbara are a bargain. A great company with a durable competitive advantage is being sold at a great price.

I am calling that this earnings report will be the bottom for Pilbara in terms of the sale price for spodumene. In the next quarter, their realized price should be slightly higher than the current one, meaning that shares are near the bottom now.

For further details see:

Pilbara Minerals: Ambitious Growth Plans And Strong Finances Make It A Buy