PILBF - Pilbara Minerals: The Odds Are In Its Favor

2023-09-25 12:12:45 ET

Summary

- FY2023 has witnessed exponential growth for Pilbara Minerals key operational/financial performance metrics.

- Growth catalysts such as the expected ~70% production growth at Pilgangoora by FY2026, long-term shortfall in global lithium supply support a 'long' investment thesis in PILBF.

- Nevertheless, I believe that the stock's near-term outlook will be impacted by depressed prices of spodumene concentrate having minimum ~6% lithium oxide.

- At present, I see the stock is a 'hold'.

Thesis

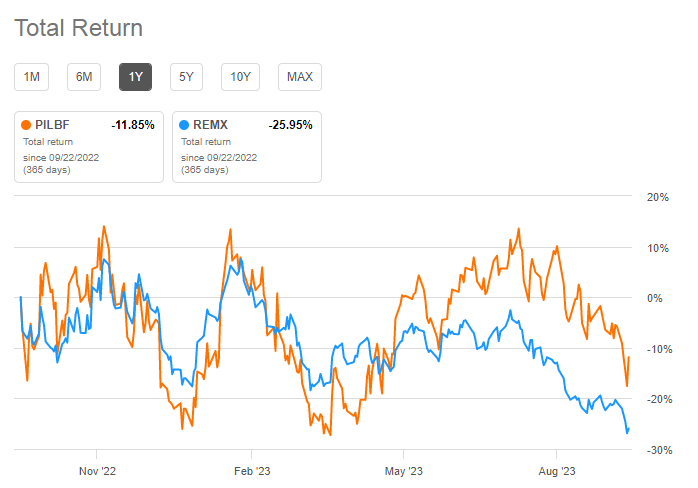

Pilbara Minerals ( PILBF ) is an emerging producer of spodumene concentrate (lithium oxide), operating a single 'producing' asset in Western Australia. The company's recently reported a 35% increase in Pilgangoora's Mineral Reserves, and together with the fact that PILBF is one of the world's largest hard-rock lithium producers, I believe this cements the Pilgangoora mine as a Tier-1 project. PILBF constitutes ~7% of the VanEck Rare Earth/Strategic Metals ETF ( REMX ) and is the 2nd largest holding of its benchmark ETF. Interestingly, the stock outperformed its benchmark ETF in total returns during the past 12 months (PILBF's TR declined by ~12% compared with REMX's TR decline of ~26%).

1-Year Total Returns (Pilbara Minerals v/s Benchmark ETF) - Source: Seeking Alpha Premium

{kind=link}

In this article, we will analyze the mining attractiveness of Western Australia (where the Pilgangoora Project, PILBF's flagship asset, is located), review the company's operational and financial performance during FY2023 (that ended on June 30, 2023), consider the growth potential of the Pilgangoora Project, and also highlight the macro-level headwinds that could impact the stock's near-term performance. We also discuss the expected implications of the above factors on PILBF's FY2024 dividend payouts. This will help us consider an investment case in the company from both perspectives: growth and income. Let's get into the details.

Pilbara Minerals Operates In A Safe Jurisdiction

The Investment Attractiveness Index (or IAI) in the Fraser Institute's Annual Survey of Mining Companies is valuable for assessing a mining jurisdiction's risk environment and mineral potential. The IAI is a composite index of the Policy Perception Index (or PPI) (40% weighting) and the Best Practices Mineral Potential Index (or MPI) (60% weighting). The PPI considers the attractiveness of mining policies in a region based on factors such as the following:

- Uncertainty regarding the interpretation, enforcement, and administration of existing regulations;

- Regulations relating to environmental protection;

- Duplication and inconsistencies in the regulatory framework;

- Taxation policies;

- Uncertainty regarding disputed areas and protected land claims;

- Availability of infrastructure to support mining activities;

- Socioeconomic agreements;

- Politically stable business environment;

- Labor issues and working relationships with labor unions;

- Geological database; and

- Security issues.

It's worth noting that with a 2022 PPI score of 86.95 points, Western Australia (where Pilbara's operations are situated) ranks amongst the top 10 regions out of the 62 mining jurisdictions evaluated in Fraser Institute's 2022 Mining Survey . However, the region's score has declined over the last five years, from 96.68 in 2018 to 86.95 points in 2022 (2023 survey results will be released in H1 CY2024). Nevertheless, an overall uptrend in the MPI score during the same period has largely offset the impact of a deteriorating PPI score. This has resulted in an overall IAI score of 88.26 points for Western Australia, placing it 2nd among the 62 mining jurisdictions in the 2022 Mining Survey.

To put that into context, let's look at the company's statement acknowledging government support for its flagship project at the time when it executed an A$250 MM debt facility with the Australian Government and secured a separate US$113 MM debt facility with commercial lenders for Pilgangoora capacity extension/debt refinancing,

Pilbara Minerals would like to acknowledge the significant support provided by the Clean Energy Finance Corporation (or CEFC) over the past five years, from their cornerstone investment in the Nordic Bond which financed the initial construction and development of the Pilgangoora Project back in 2017, to their participation in the 2020 refinancing of the Nordic Bond, which proved invaluable in protecting Pilbara Minerals during challenging market conditions at that time. Pilbara Minerals would like to sincerely thank the CEFC and the Australian Government for its support to date .

FY2023 Results Showed Impeccable Performance

FY 2023 has been a stellar year for Pilbara Minerals. The 2023 results report proves that the company's Pilgangoora Project (in the ramp-up phases) is firing on all cylinders. On that note, FY 2023 production and sales volumes witnessed a YoY increase of 64% (from 377.9 kT to 620.1 kT) and 68% (from 361 kT to 607.5 kT), respectively, augmented by a whopping 87% YoY increase in average estimated realized prices (from US$2,382/ton to US$4,447/ton). Growth in production/sales volumes and average prices resulted in a gigantic 242% YoY increase in revenues (from A$1,189 MM to A$4,064 MM), which helped EBITDA growth by 307% YoY (from A$814.5 MM to A$3,317.2 MM).

On the balance sheet, I see YoY growth in total assets from A$1,978.4 MM to A$5,198.8 MM (or 163% YoY). The strong operational performance at Pilgangoora bolstered PILBF's liquidity, resulting in a phenomenal 464% YoY growth in cash and equivalents (from A$591.7 MM to A$3,338.6 MM). Meanwhile, cash margins from operations also grew by 440% YoY (from A$679.2 MM to A$3,664.3 MM).

Pilbara Minerals FY2023 Financial Highlights - Source: 2023 Results Presentation

I believe these favorable numbers (especially YoY EBITDA growth) also indicate that the Pilgangoora asset is emerging from the initial high-cost production phase, supported by a strong balance sheet.

In addition to the above, PILBF achieved the following significant milestones during FY 2023:

- Released the company's Capital Management Framework , targeting annual dividends between 20-30% of free cash flows.

- Entered into a 55% JV partnership with Calix (a technology development firm) to develop a mid-stream Demonstration Plant at the Pilgangoora project to utilize Calix's calcination technology for low-cost/low-carbon lithium production in the future.

Pilbara Minerals FY2023 Financial Highlights - Source: Results Presentation

Growth - As I See It

Pilbara Minerals produced ~620.1 kT of spodumene concentrate during 2023 (FY 2022: 377.9 kT). The company's FY 2024 guidance estimates spodumene concentrate production between ~660-690 kT at an average SC grade of ~5.2%. If the production guidance is adjusted on a ~5.7% grade, the estimated production will lie within the range of ~600-630 kT.

P680 Project: To sustain production growth, Pilbara is advancing construction on the P680 Project, which will expand the Pilgan Plant's production capacity by ~100 kTpa (read: a thousand tons per annum) from the existing level of ~580 kTpa. Upon completion, the P680 project will enhance the Pilgangoora Project's annual combined nameplate capacity to ~640,000-680,000 dmt (read: dry metric tons) per annum of spodumene concentrate.

P1000 Project: The P680 expansion project includes the construction of a primary rejection heavy media separation circuit together with an integrated crushing and ore facility that can process up to 5 Mtpa (read: a million tons per annum) of ore throughput. The crushing/ore facility will also support the escalation to the P1000 expansion project, which will further expand spodumene concentrate production to the tune of ~1 Mtpa. Interestingly, PILBF's Board made the FID (read: Final Investment Decision) to proceed with the P1000 project in March 2023 . In essence, the P1000 Project entails the following changes to the Pilgan Plant's concentrator, as well as non-process infrastructure:

- Duplication of tertiary crushing by utilizing high-pressure grinding rolls.

- Duplication of existing ball mill.

- Duplication of Floatation circuit.

- Pre-flotation magnetic separation/recovery of secondary tantalum (to enhance by-product credits).

- Heavy Media Separation tailings/split water circuit.

- Dewatering Circuit of the new concentrate; and

- More than 80% of the flotation concentrate is to be designed, such as to be conveyed directly to the concentrate handling pad to reduce manual haulage activities and reduce the cost of production.

- The construction of a 15ML raw water storage dam for the Pilgan Plant.

- The extension of the bore field pumping/piping network for increasing water supply and new bore headworks to incorporate remote telemetry/control, thereby achieving greater capacity and efficiency.

- The addition of 100 new rooms at the Tambrah camp to incorporate the increased workforce employed during the P1000 Project construction and subsequent operations.

The P1000 Project will be executed parallel to the P680 expansion project (already under construction). The first ore production from the P1000 is targeted in the quarter ending March 2025, with full-scale production expected in H1 FY2026. The project will involve capital investments of A$560 MM, with an attractive payback period of only 12 months (assuming first ore production is achieved by Q3 FY2025).

In my view, the completion of these two expansion projects (P680 and P1000) will help increase Pilbara's existing SC production levels by ~70%. The production is expected to peak (above the 1Mtpa threshold) over the next three fiscal years and then stabilize around ~1Mtpa from FY2026 onward. Look at the chart below.

P1000 Expansion - Source: Pilbara's News Update

Declining Lithium Oxide Prices Act As Near-Term Headwind

As discussed above, PILBF is expected to witness organic growth in its operational performance (especially through near-term production growth). However, the prevailing prices of ~6% Li2O (lithium oxide) spodumene concentrate spell trouble for the stock's near-term growth prospects. A closer look at PILBF's 5-year price chart indicates that the stock has gradually built up its upward trajectory since 2019 when the company declared commercial production from the Pilgangoora Project. The share price peaked in November 2022 (at ~$3.70/share) before witnessing multiple oscillations and eventually declining to the current price of ~$2.71/share (at the time of writing).

PILBF 5-Year Price Chart - Source: Seeking Alpha

Meanwhile, the prices of spodumene concentrate containing at least 6% Li2O have remained muted after witnessing a peak at the end of 2022. For reference, note that the prices averaged ~$8,300/ton during November/December 2022 and have tanked to ~$3,350/ton by the end of August 2023.

SC prices at ~6% Li2O - Source: Fast Markets

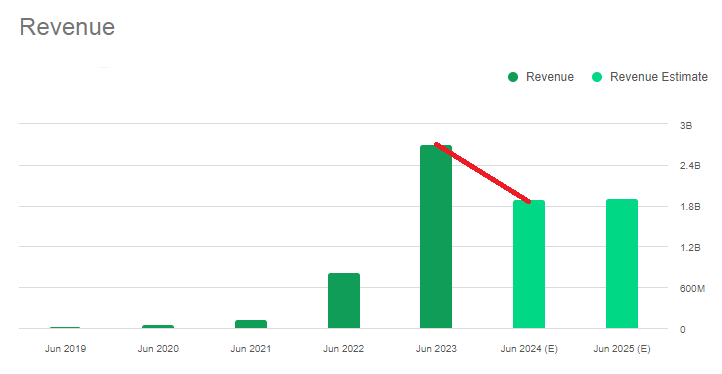

This ~60% decline in ~6% SC prices is likely to have a significant impact on PILBF's FY2024 revenues despite the YoY projected increase in concentrate production stemming from the P680 expansion project. Look at the chart below indicating that PILBF's annual revenues are expected to shrink from ~US$2.71 BB in FY2023 to ~US$1.89BB in FY2024.

PILBF's Revenue Expectations 2024/25 - Source: Seeking Alpha

{kind=link}

Dividends - As I See Them

It's commendable that Pilbara Minerals announced its first (or inaugural) dividend (to the tune of A$0.25/share) within five years of declaring commercial production at the Pilgangoora Project. As noted above, the company's Capital Management Framework approved by its Board targets an annual dividend payout between 20-30% of free cash flows (with the possibility to enhance investor returns through special dividends, share buy-backs, or a combination of both).

However, I expect that the following factors will significantly impact PILBF's FY2024 free cash flows and, consequently, its annual dividend payout:

1) Operating cash flows will be adversely impacted by lower Li2O prices, partially offset by a ~20% YoY increase in concentrate production volume (assuming that the production volumes are matched by the sales volumes, with a minimum increase in inventory levels).

2) Pilbara has planned to undertake significant CAPEX investments in FY2024, including expected growth CAPEX between ~A$490-540 MM, mine development CAPEX between ~A$140-160 MM, sustaining CAPEX between ~A$75-85 MM, and CAPEX related to project enhancement between ~A$170-190 MM.

3) The expected payment of pending tax liability to the tune of ~A$773 MM will also put pressure on Pilbara's FY2024 operating cash flows.

Market Outlook and Investor Takeaway

The preceding discussion highlights that PILBF's pipeline expansion projects (P680 and P1000) at the Pilgangoora mine target production growth of ~20% in FY2024, leading to ~70% cumulative production growth by the end of CY2025. Nonetheless, a 60% decline in the price of ~6% Li2O spodumene concentrate has hurt the share price badly.

PILBF currently trades slightly below the mid-point (at ~$2.985/share) of its 52-week range (between $2.26-3.71) and promises suitable share price growth over the medium-to-long-term investment horizon (say, 3-5 years) based on the following catalysts:

1) Production growth from the Pilgangoora Project over the next two years to ~1Mtpa.

2) Diversification across the battery materials supply chain through the company's 18% equity stake (with the option to increase shareholding to 30%) in POSCO Pilbara Lithium Solutions Ltd. to develop a ~43 kTpa lithium hydroxide conversion facility in South Korea. In 2023, PILBF announced that the POSCO JV secured a US$460 MM debt facility to fund remaining plant development CAPEX (with expected plant ramp-up to nameplate capacity in FY2024).

POSCO JV Plant Timeline - Source: Pilbara's News Announcements

3) Expected shortfall in global lithium supply (from FY2026 onward) stemming from long-term demand growth of battery-grade lithium raw materials from PEVs (Plug-In Electric Vehicles). According to London-based Benchmark Mineral Intelligence, the global PEV penetration ratio will significantly enhance from ~27% in 2026 to ~76% by 2040. Of course, short-term lithium price volatility cannot be ruled out due to a challenging macroeconomic environment, global inflationary pressures resulting from the Russia-Ukraine conflict, the prevailing volatility in oil prices, and the impact of central banks' monetary policy on economic activities.

Forecasted Lithium Demand Growth - Source: PILBF's Results Presentation

Nonetheless, I think the stock's near-term growth potential will continue to be impacted by the turbulence in spodumene concentrate prices, the impending tax liability worth ~A$773 MM (burdening PILBF's cash flows), and significant CAPEX investments during FY2024.

In my view, the stock is a suitable 'long' investment, but due to the factors mentioned above, I see the stock as a 'hold' for the near term (say, the next 12 months).

For further details see:

Pilbara Minerals: The Odds Are In Its Favor