PAXS - PIMCO CEF Update: Getting Ready For PDX

2023-11-22 21:37:01 ET

Summary

- We provide an update for the PIMCO CEF suite.

- PIMCO took advantage of the recent back-up in yields and yield curve disinversion to add assets across the taxable suite.

- Muni CEF coverage continues to decrease, while taxable CEF coverage slightly improved.

- Tax loss-related seasonality may impact certain funds, creating potential entry points for investors.

- We remain bullish on NRGX (i.e. PDX) and PHK.

In this article, we provide an update on the PIMCO CEF suite. Specifically, we discuss the changes in leverage and distribution coverage. We also touch on the transition of the Energy and Tactical Credit Opportunities Fund ( NRGX [PDX]) and tax loss-related seasonality.

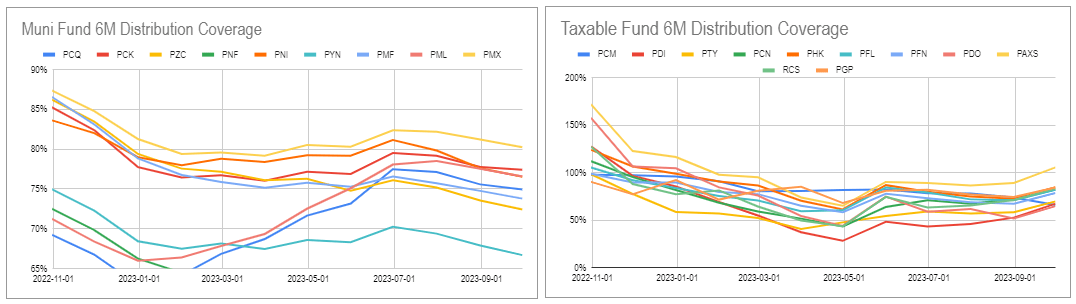

Coverage Update

Muni CEF coverage continued to move lower in September - the most recent month figures we have so far. Recall that these funds made large distribution cuts earlier in the year which increased their distributions. However, the gravity of rising leverage costs is taking its toll and coverage renewed its downward path.

Taxable CEF coverage ticked higher after several months of moving lower, however, it remains at a fairly depressed level.

{kind=link}

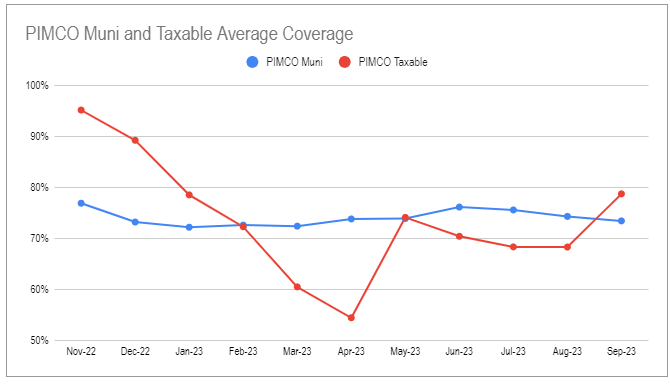

We can see clearer trends in this chart.

{kind=link}

We got some questions about potential special distributions later this year as we saw last year across a number of PIMCO CEFs. Given the stark difference in UNII (mostly negative this year vs. mostly positive last year) specials are fairly unlikely in our view.

Systematic Income CEF Tool

Leverage Update

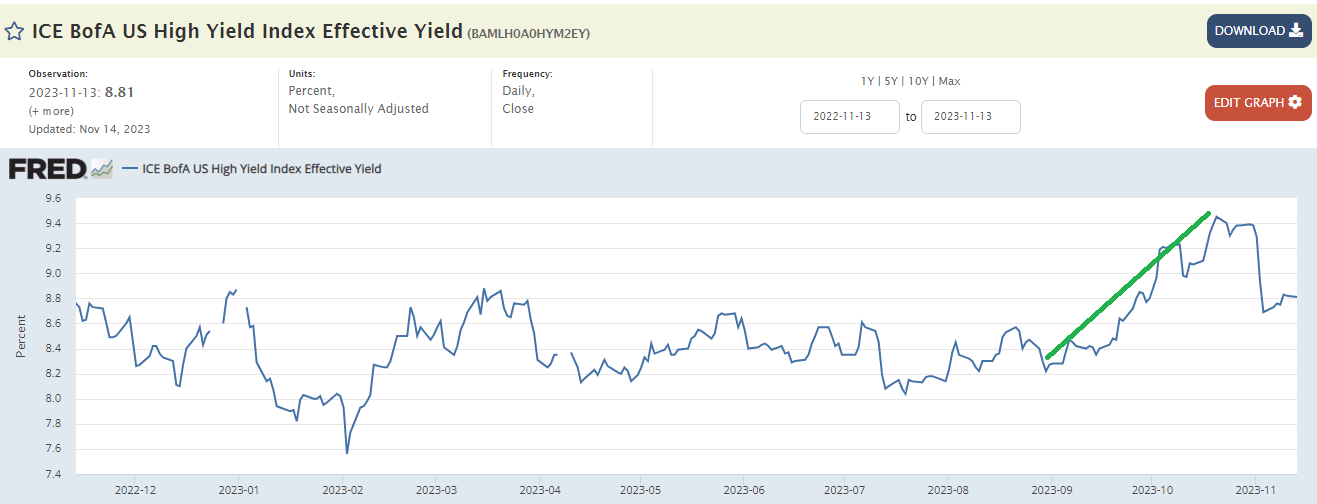

October borrowing levels eased off a bit after a sharp jump in September.

Systematic Income

This makes a lot of sense in our view as yields increased sharply over September, primarily as a result of the rise in Treasury yields. The jump in long-end yields also largely disinverted the yield curve. These two factors meant that credit assets were not just more attractive (because overall yields were higher), but they were now more attractive if financed with leverage (because the yield curve nearly normalized).

{kind=link}

The average leverage level in the taxable suite moved north of 40% in September - a level it hasn't seen in a year.

Systematic Income

Three funds continue to run at leverage levels close to 50%.

Systematic Income

Tax-Loss Seasonality

An important consideration this time of year for CEF investors is tax loss-related seasonality. Funds that have suffered price falls this year may come under more stress as investors lock in tax losses. Unlike in 2022, tax losses are likely to be more immediately useful to offset capital gains as the CEF market overall is actually in the green.

Systematic Income

In the taxable suite, funds that could come under more stress are PDO and PAXS.

Systematic Income

In the tax-exempt suite, California and New York state funds could see more tax-related selling.

Systematic Income

For current shareholders of these funds, there could be more attractive entry points through the rest of the year. However, as we highlighted in the recent CEF Weekly, tax-related selling happens at the same time as the front-running of the Santa Claus rally we often see in January. This is why, on average, December tends to see positive CEF returns and discount tightening.

In short, we don't expect a ton of CEF weakness unless the broader market falls out of bed. For instance, December of last year was quite weak in CEF discount terms. However, that's largely because stocks finished the year on a weak note, dropping through December. On the other hand, stocks are mostly up this year.

Systematic Income

Market Themes

As many PIMCO investors are well aware, NRGX is transitioning to a credit fund this month with 21-Nov as the key date. One view is that 21-Nov is a special date when the discount should move to zero. The view is that on that date the fund has to sit in cash because it must be in compliance with its new mandate i.e. it can’t own the energy assets it currently holds and that the new assets or cash it acquires have to, by definition, be owned at the NAV. For this reason, the fund can’t trade at a discount. In our view, this argument is not very convincing.

First, we won’t know on 21-Nov what the fund is doing - it won’t be holding its current energy assets but we won’t know whether it will be in cash or allocated to its new credit portfolio. It doesn’t take all that much effort for an organization like PIMCO to sell down a bunch of energy assets and acquire credit assets over a day. Even if it can’t do everything in one day, it can quickly buy proxy assets e.g. broad-based credit indices like CDX which it can later exchange for physical assets like corporate bonds and loans over time.

Secondly, and more importantly, there is no difference between assets like cash and traditional credit assets - everything is "owned at the NAV". By this logic, no CEF should trade at a discount because all of the CEF’s assets are "owned at the NAV".

Moreover, imagine a CEF that only held cash - what discount would it trade at? The answer is that it would trade at a discount roughly in line implied by its management fee. In other words, for a typical total fee of 1% a CEF holding cash would trade at a 20% discount. This is for the simple reason that the fund would take around 20% of the total yield that it earned (1% out of about 5% earned on cash). Trading at a 20% discount means the fund would deliver a yield on price of around 5% - the same as investors would get by holding cash assets like T-bills outright.

Net net, we don’t expect an immediate compression of the NRGX discount on 21-Nov. That said, the discount should tighten over time, closer to where other PIMCO taxable CEFs trade. The ticker change on 21-Nov should wake people up to the fact that this is a new PIMCO CEF.

Stance And Takeaways

We recently highlighted PHK as an attractive pick in the taxable suite. Since then the fund has outperformed its peers by more than 2%. In our view, it remains a decent hold in the suite. As the chart below shows, its valuation differential versus the average PIMCO taxable CEF has almost fully closed - an unusual situation historically. PHK has the second lowest management fee in the taxable suite and should, therefore, command a premium valuation.

Systematic Income

We also like NRGX ((PDX)), which we also expect to outperform over the medium term. As mentioned above and discussed in a recent article, it is transforming to a credit-focused CEF and should see its 12% discount tightened to be more in line with the rest of the taxable suite where the widest discount is 4%.

For further details see:

PIMCO CEF Update: Getting Ready For PDX