PAXS - PIMCO CEF Update: PIMCO Trades The October Swoon

2023-12-26 07:32:55 ET

Summary

- We provide a November update for the PIMCO CEF taxable suite.

- Coverage across PIMCO's tax-exempt funds increased slightly in November, while coverage for taxable funds decreased by around 10% on average.

- PIMCO appears to have taken advantage of the swoon in credit prices in September and October.

- We continue to favor PHK and PDX in the taxable suite.

In this article, we provide an update on the PIMCO CEF suite. Specifically, we discuss the changes in leverage and distribution coverage for the month of November. We also highlight PIMCO's tactical moves in the context of the recent drop and subsequent retracement of credit asset prices.

Coverage Update

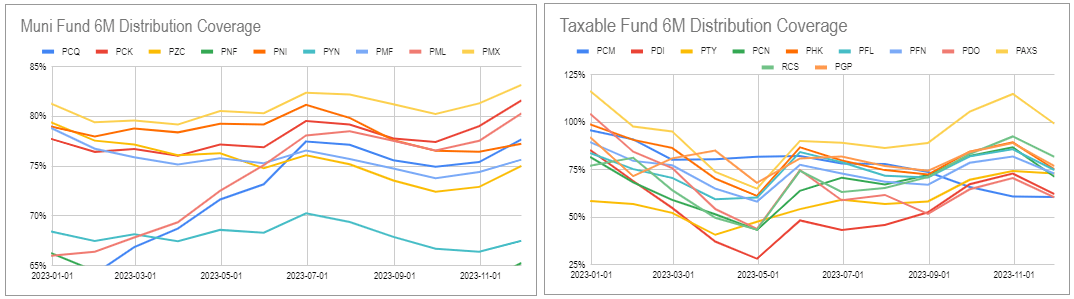

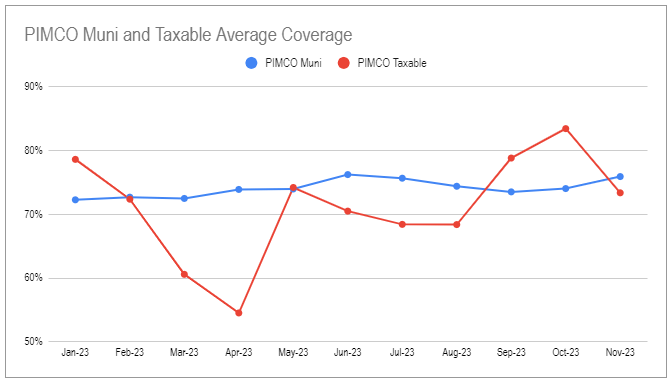

Coverage across tax-exempt funds ticked higher marginally in November, as estimated by the six-month rolling figure. However, taxable fund coverage declined fairly sharply - by around 10% on average.

{kind=link}

If we look at aggregate numbers, we see that Muni coverage has been fairly steady while tax-exempt coverage has whipped around.

{kind=link}

PAXS continued to boast the highest six-month coverage in the taxable suite with PDO, PCM and PDI towards the lower end.

Systematic Income CEF Tool

Interestingly, this stronger level of coverage is not enough to generate interest in the fund. Its discount remains depressed relative to the average PIMCO taxable CEF. This is likely due to the fund's subpar total return since inception - a function of its CMBS overweight.

Systematic Income

Leverage Update

Taxable fund borrowings fell back after spending two prior months at an elevated level.

Systematic Income

The cuts were seen across all funds, suggesting a systemic approach to taking leverage down across the entire suite.

Systematic Income

As a result, the average level of leverage came back down to just north of 30% - fairly low by PIMCO standards.

Systematic Income

Leverage divergence remains fairly wide in the taxable suite, with PCN below 20% and 4 funds having leverage above 40%.

Systematic Income

Now that leverage has come back down, it's worth asking why did PIMCO push leverage up significantly in September and October and take it back down in November?

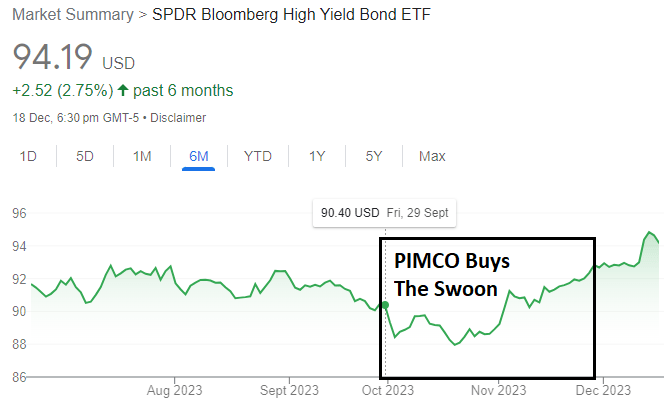

The most obvious answer in our view appears to be the October swoon in credit markets as a result of the perception that the Fed was not yet done with its hiking program. This is illustrated with the help of the price of the high-yield corporate bond ETF ( JNK ) below. We see that credit asset prices started falling in September and fell very sharply in October and started to recover over November.

{kind=link}

It looks like PIMCO bought assets on the dip (during September and October) and then sold them once prices recovered in November. This is a good result for shareholders, and it's what is expected from the more tactical PIMCO managers.

Valuations and Returns

Year-to-date, all taxable PIMCO CEFs are in the green, with RCS leading the way in total price terms and PGP ahead in total NAV terms. PGP has benefited from its equity allocation to finish first, while RCS enjoyed the strongest valuation rerating. PDO and PAXS are at the lower return range, largely due to their CMBS overweight.

Systematic Income

On the tax-exempt side, total NAV returns are fairly comparable, however there is a wide disparity in total price returns. As we highlighted earlier, the higher premium funds have deflated the most as a result of their savage distribution cuts.

This one-two income-return punch is a common hallmark of funds that tend to overdistribute. The overdistribution results in a high distribution rate, attracting demand and pushing their valuation to a high premium. When the distribution cut arrives, the valuation tumbles with it, locking in permanent economic losses for investors.

Systematic Income

The average taxable CEF premium is right around 10%, fairly high relative to the last 2 years but modest relative to the pre-2022 environment. We don't expect valuations to move back to their previous level given the steady cuts the funds have made over the last decade.

Systematic Income

Relative to the rest of the CEF market, taxable PIMCO CEFs are not particularly cheap, with the average PIMCO CEF trading close to a 20% valuation premium, roughly in the middle of the historic range.

Systematic Income

Within the taxable suite, we continue to favor PHK and PDX. PHK is a fairly typical credit PIMCO fund whose valuation has become fairly attractive recently relative to the broader PIMCO suite.

Systematic Income

PDX is more of an energy-focused credit fund. We expect its wide valuation gap of 22% to partly close over the medium term. The key catalyst for this should be its distribution hike as well as a move to monthly distributions.

For further details see:

PIMCO CEF Update: PIMCO Trades The October Swoon