PDI - PIMCO Update (Quick) | January 2024 | Watch The NAV Momentum Turn

2024-01-17 07:00:00 ET

Summary

- Not much has changed fundamentally in taxable PIMCOs, but there has been a shift in valuations and sentiment.

- The drop in the dollar has put downward pressure on funds with exposure to foreign bonds and currency forwards contracts.

- Leverage is a key consideration for assessing NAV trends, and some funds have reduced leverage significantly in the past month.

- Today, I hold the vast majority of my PIMCO allocation in PCN, PDI, and PDX with a more moderate allocation in PFN.

Not much has changed in the last month or two regarding the fundamentals of the taxable PIMCOs. However, we have seen a shift in valuations and sentiment along with NAV momentum.

Why do I say nothing much has happened fundamentally?

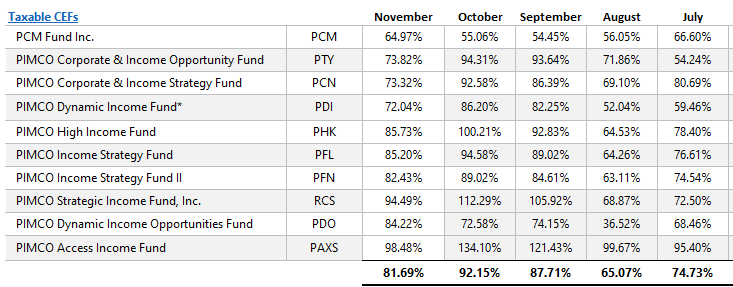

The chart below shows that the average 3-month coverage ratio hasn't moved all that much in the last few months and really since July. Coverage ratios for a few select funds did bounce but then fell back to these 'normalized' ranges.

{kind=link}

We have seen the dollar drop a bit against the euro and the pound, putting downward pressure on those funds with the most exposure to foreign bonds and thus, more currency forward contracts.

The funds with the most EM and non-USD developed exposure are PIMCO Corporate and Income Opportunity Fund (PTY), PIMCO Dynamic Income Fund (PDI), PIMCO Dynamic Income Opportunities Fund (PDO), and PIMCO Access Income Fund (PAXS). No surprise, given the drop in the dollar in November, those are the funds that saw the largest drop in 3-month coverage in November.

ycharts

But what I want to focus on today, now that the January distribution announcement is behind us and no changes were made, is the NAVs and valuation. In other words, where's the opportunity?

Leverage Update

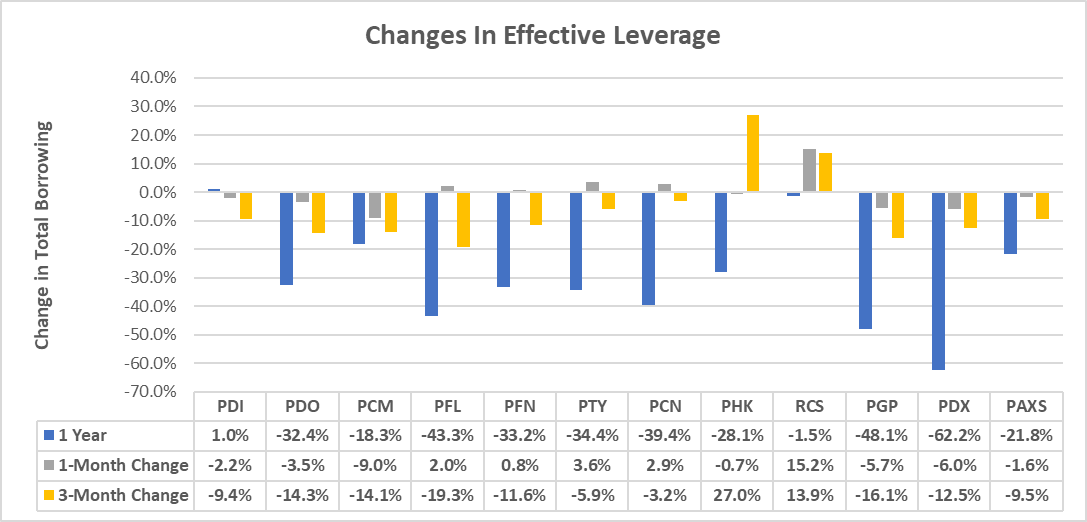

Leverage is a key consideration when assessing NAV trends. The funds with the most capacity to add leverage will be able to use the NAV momentum to their advantage and add opportunistically and generate additional net investment income ("NII"). If they are able to do so, then the NAV growth can 'build on itself', at least until the momentum turns.

What we have seen, historically, is that CEF NAV momentum can last for lengthy periods of time (typically at least several months) before a shift takes place. I attribute this to the laggy nature of bond pricing and the compounding of leverage. Fund flows are also a big driver.

In the last month, we've seen a few funds drop leverage fairly significantly which could put downward pressure on coverage ratios in the near future. However, over longer periods of time, leverage tends to even itself out.

{kind=link}

Leverage for the big three funds: PDI , PDO , and PAXS are lower than they have been over the prior months. This is due to a combination of NAVs rising but also a reduction in the aggregate amount of borrowed funds.

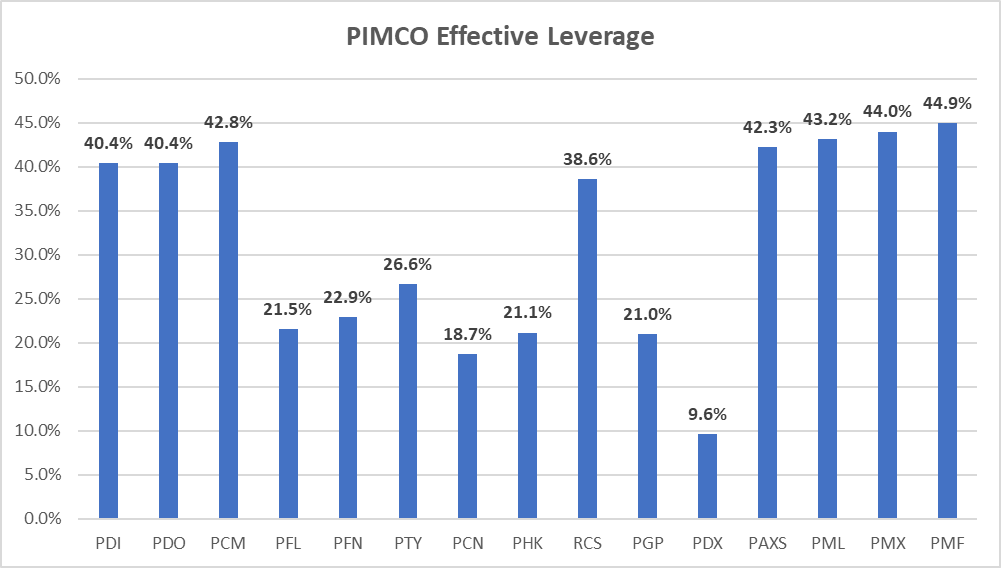

Considering PIMCO typically keeps leverage relatively high- for PDI it has averaged right at 44% the last three years- there is a bit of capacity to add if they have solid buying opportunities.

{kind=link}

NAV Momentum

NAVs were up nicely since the end of October as the risk-on nature of the markets boomed in bond prices. The big three multisector taxables, PDI, PDO, and PAXS saw NAVs rise by 3.75% to 7.25%. Unfortunately, there is a bit of rolling over of that NAV momentum which is causing me to pause.

ycharts

The next cohort has done much better on a NAV TR basis, with all four funds - PTY , PIMCO High Income Fund (PHK) , PIMCO Corporate & Income Strategy Fund (PCN) , PIMCO Income Strategy Fund (PFL) and PIMCO Income Strategy Fund II (PFN) - up around 10% on a NAV total return basis. And they have been able to do that with less leverage relative to the big three above.

ycharts

Lastly, there are the esoteric funds - PIMCO Global StocksPLUS and Income Fund (PGP), PIMCO Strategic Income Fund (RCS), PIMCO Dynamic Income Strategy Fund (PDX) and PCM Fund (PCM) - with PDX, formerly NRGX, up big due to the exposure to energy.

ycharts

Many may be asking why PDX is up so much when MLPs and other energy stocks (like the XLE, energy select SPDR) are only up modestly. You can see from the one-year chart below that PDX, the blue line, stays largely on top of the orange, the Alerian MLP ETF. In late September, the NAV jumped thanks to the tax treatment of the fund shifting as they changed the investment strategy of the fund to a multisector.

As Landlord Investor wrote on the SA chat back in late September:

This is a total wild guess but if they previously had more than 25% of their portfolio in MLPs then they would be organized as a corporation and carry a large tax liability on their balance sheet. If, as a result of the transition, they have less than 25% in MLPs, then they can re-organize as a RIC and that tax liability is removed from their balance sheet, thus increasing NAV.

Well, that turned out to be accurate as their latest fund card discusses that very thing:

PIMCO ycharts

At this point, PDX is still trading mostly like an MLP fund with a high correlation to those energy-related indices. The fund will likely be curtailing that investment and likely the investment in Venture Global Holdings A, an LNG company as the exposure is nearing one-quarter of the fund's total assets.

I expected the fund to change to a monthly distribution schedule as well as perhaps increase the payout a bit to move it more in line with the other multisector funds. That didn't happen. It appears that the transition is proceeding a bit slower than I thought it would.

Perhaps that is PIMCO thumbing their noses at Saba Capital, who had precipitated the changes. Or perhaps they see the energy/MLP space as a compelling area of exposure for the portfolio.

We should get the December 31st fund card (fact sheet) in the next few weeks which should shed some light on the speed of the transition.

Best Ideas

I remain steadfast in my thought that PCN is my top pick at the moment, especially since PHK has risen back to an 8% premium from the 3% to 4% area in December and even a discount in October and November. Is it time to swap out of it? I would say no as the valuation remains in its long-term band and there are no overly compelling buys on the long side.

If PCN were in the low single digits for premium, I would likely change my tune to swapping PHK for PCN .

PDI is one of the better deals right now at a 5.5% premium. This is still in its fair value range (5% - 7%) but on the lower end while most of the other funds are on the upper end of their ranges. It's all relative!

The market is now equalizing the yields of PAXS and PDO , the newest funds, so their valuations should now always be about ~2% apart (with PDO 2% higher in premium than PAXS ).

This is similar to what the market does with PFN and PFL , the income strategy funds that are largely identical. PFL tends to trade at a 3.0% premium to PFN . Right now, it's a bit over that suggesting a small arbitrage by moving from PFL to PFN .

Lastly, I received a few questions regarding the two high-premium funds, PCM and PTY . These are different funds and should not be compared to each other as 'sister funds'. The only useful characteristic is their excessive valuations.

For example, PTY tends to trade between 16% and 31% premiums, 95% of the time, with a long-term average of 24%. PCM is more volatile, likely because it is smaller and has fewer shares traded (27K vs 568K per day). It trades between 15% and 44%, 95% of the time with a long-term average of 28%.

Today, PCM is just below a 20% premium and PTY is just above 19%. They are both still 'high premium' names but both are well closer to the lower end of their long-term ranges and 4-5% below their averages. Something to watch for the value CEF investor who may want to pick up some shares on the mean reversion trade.

Today, I hold the vast majority of my PIMCO allocation in PCN, PDI, and PDX with a more moderate allocation in PFN.

If you are thinking of adding, I would start slowly and watch those NAVs in case they are indeed, rolling over for a more sustained downturn.

For further details see:

PIMCO Update (Quick) | January 2024 | Watch The NAV Momentum Turn