BLDR - Pivot Pending

2023-12-03 09:00:00 ET

Summary

- U.S. equity markets notched a fifth-straight week of gains as benchmark interest rates continued a decisive retreat after economic data and comments from Fed officials fueled bets on a pending pivot.

- Advancing for a fifth-straight week since dipping into "correction territory" at the end of October, the S&P 500 gained another 0.8% on the week, while Mid-Caps and Small-Caps gained 2%.

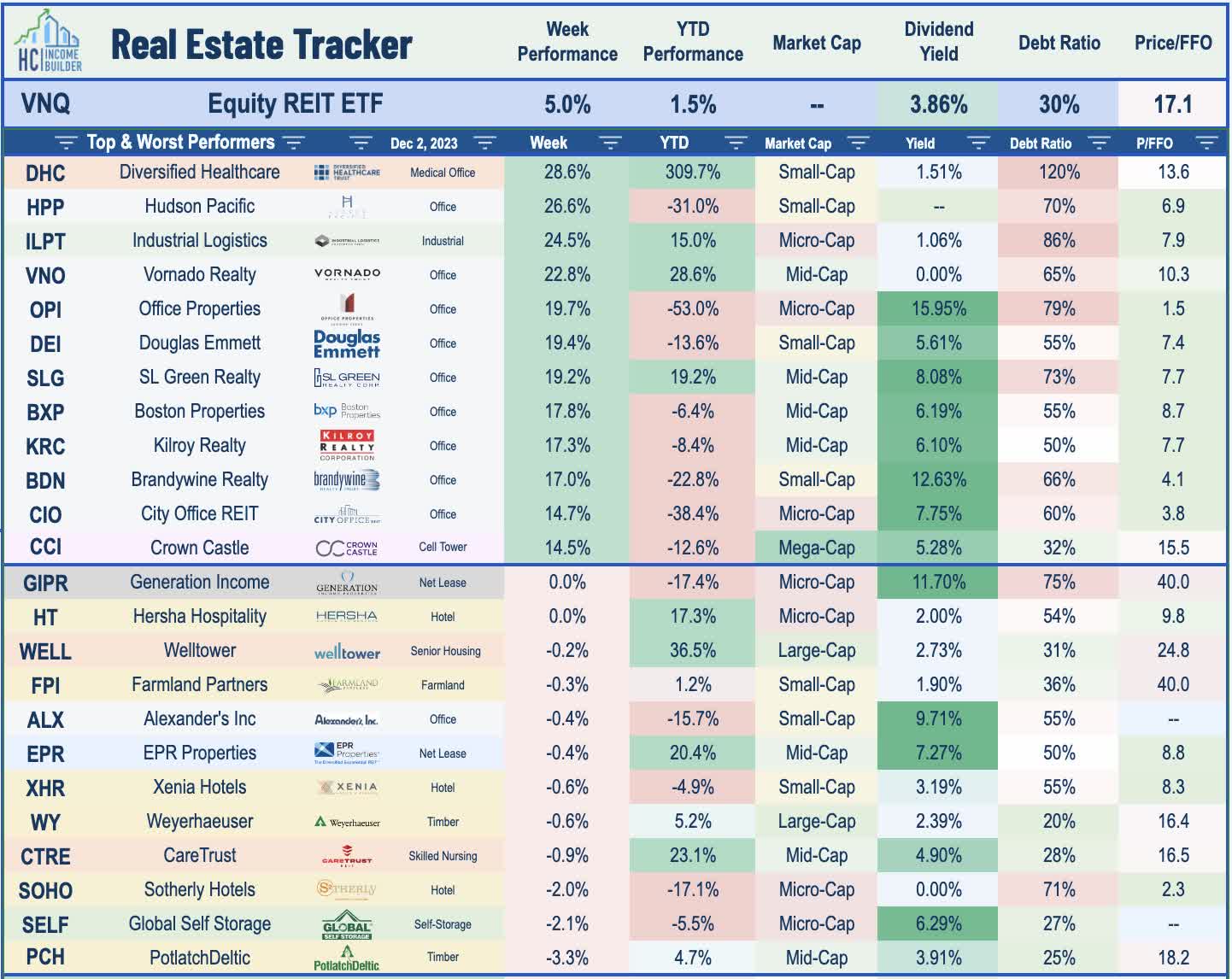

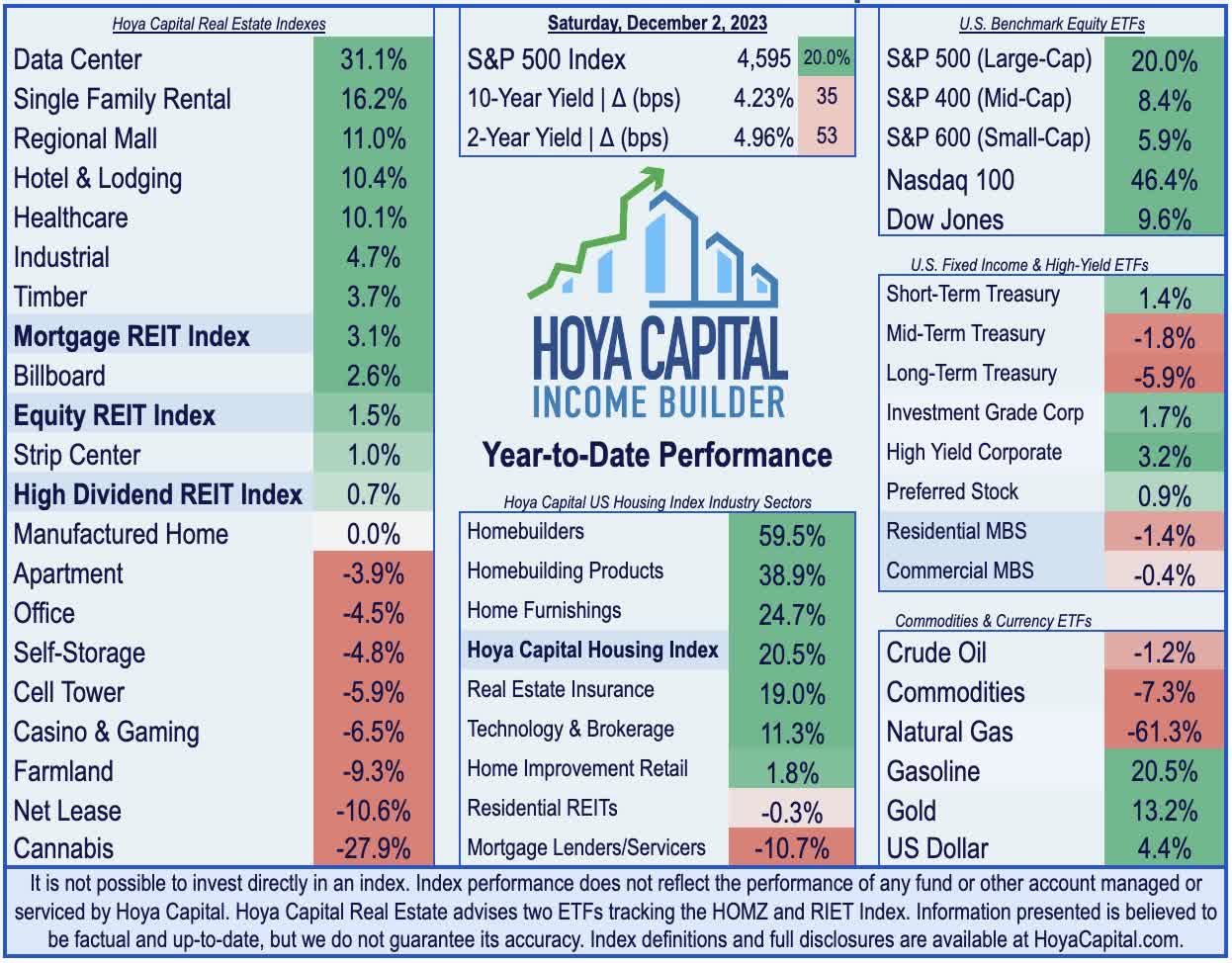

- Lifted by the rate retreat, real estate equities were again the leaders this week. The Equity REIT Index rallied 5.0% this week, extending their rebound since late-October to nearly 20%.

- Fund flows were a major theme this week as the combination of index rebalancing and a forceful shift in sentiment sparked a double-digit surge this week from many of the most beaten-down REITs. W. P. Carey rallied after S&P announced that it would be added to the Mid-Cap 400.

- Office REITs - the most underweight property sector among active managers and the most heavily-shorted corner of the REIT sector - surged double-digits as the rate retreat has lifted some of the gloom from the beaten-down sector and sparked a short-covering rally.

Real Estate Weekly Outlook

U.S. equity markets notched a fifth-straight week of gains as benchmark interest rates continued a decisive retreat after economic data and comments from Federal Reserve officials fueled bets of a pending pivot toward rate cuts by mid-2024. Fed Chair Powell remarked that policy is “well into restrictive territory,” adopting a more dovish tone than markets expected following a wave of dovish commentary earlier in the week, including remarks from Fed Governor Waller - one of the most hawkish officials - who commented that he’s “increasingly confident" that inflation is trending back towards its 2% policy objective, while highlighting the historic pace of disinflation.

{kind=link}

Advancing for a fifth-straight week since dipping into "correction territory" at the end of October, the S&P 500 gained another 0.8% on the week. The Mid-Cap 400 and Small-Cap 600 - which have underperformed for much of the year until the recent November rebound - gained more than 2% on the week. The tech-heavy Nasdaq 100 traded flat this week, however, as investors shifted into some of the more beaten-down segments of the market. Real estate equities - which were the top-performing GICS equity sector during November - were again the leaders this week, lifted by the continued retreat in benchmark interest rates. The Equity REIT Index rallied another 5.0% this week, with all 18 property sectors in positive territory, while the Mortgage REIT Index advanced 5.3%. Homebuilders were also among the leaders this week as mortgage rates declined for a fifth straight week.

{kind=link}

Bonds continued their impressive November rebound, buoyed by dovish Fed commentary, calming tensions in the Middle East, and economic data generally consistent with a "soft landing" trajectory. Posting its lowest close since early September, the 10-Year Treasury Yield dipped 25 basis points this week to 4.23%, while the policy-sensitive 2-Year Treasury Yield plunged 41 basis points to 4.55% - the lowest level since June. As the Fed enters the "quiet period" ahead of its policy decision on December 13th, swaps market now imply that the likelihood of another rate hike is less than 5%, while there's now an over 60% probability that the Fed will cut rates for the first time by March and imply a year-end policy rate of around 4.0% - down from the current upper-bound of 5.50%. Posting declines in six of the past seven weeks, WTI Crude Oil dipped another 2.2% this week to below $75/barrel - now 25% below the recent peak in late September - despite the announcement of further production cuts from OPEC members.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

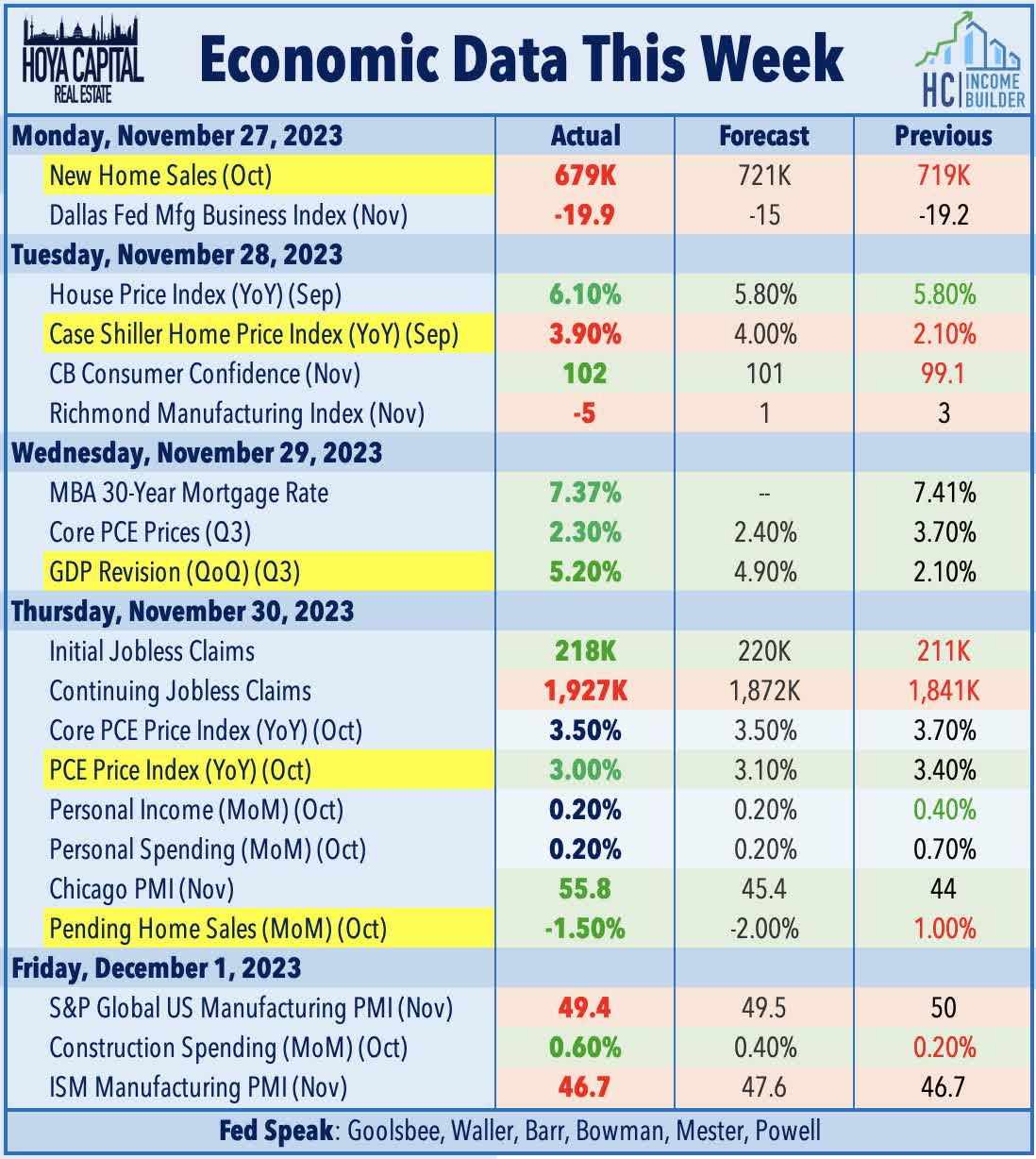

Following cooler-than-expected Consumer and Producer Price Index data earlier this month, PCE Price Index data released this week provided further evidence that price pressures continued to moderate in October. Core PCE - the Fed's preferred gauge of inflation - rose 0.2% in October and 3.5% from last year - slightly cooler than consensus estimates and the lowest annual increase since April 2021. Headline PCE was flat on the month - below estimates of a 0.1% increase - which pulled the year-over-year increase to 3.0%. Goods prices declined 0.3% for the month, driven by a 4.8% dip in energy prices following a late-summer resurgence. Services prices rose 0.2%, an increase that is still being driven largely by the delayed recognition of housing inflation seen 9-18 months ago. The same report showed that Personal Income and Personal Spending each rose 0.2% on the month, which pulled their year-over-year increase to 4.5% and 5.3%, respectively.

{kind=link}

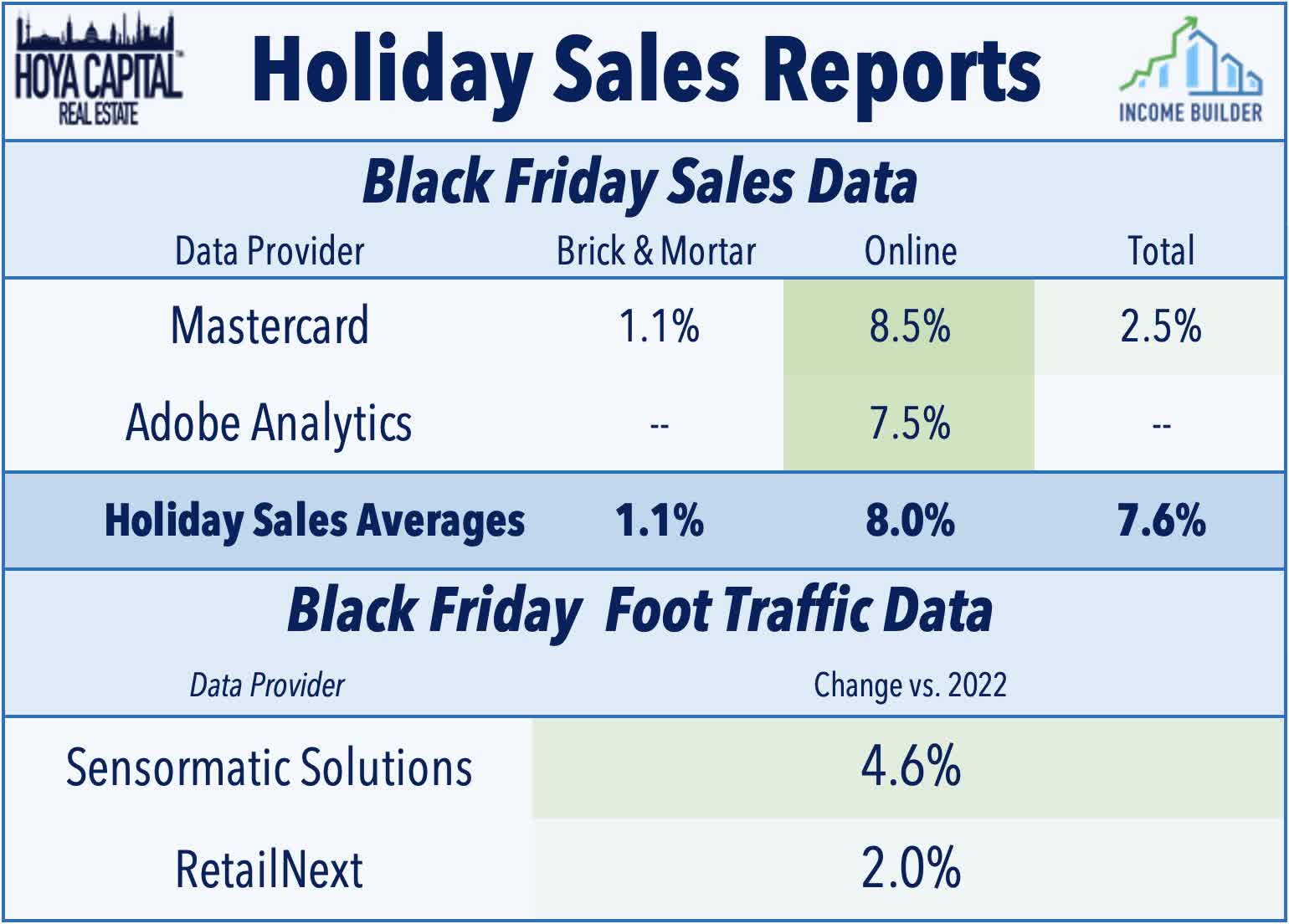

With the critical holiday retail shopping season now in full swing, a handful of firms released sales and foot traffic data from the Black Friday weekend, which generally showed stronger-than-expected trends across both e-commerce and in-store categories. Mastercard's SpendingPulse data showed that total retail sales (excluding auto) on Black Friday were up 2.5% from last year. Online sales rose 8.5%, while in-store sales increased 1.1% from last year. Adobe Analytics reported that e-commerce spending rose 7.5% from last year, noting that electronics categories showed notable strength while home repair underperformed. Sensormatic Solutions reported that shopper foot traffic increased 4.6% from last year - a positive deviation from the overall year-over-year performance in which traffic has been down -2.4% on average throughout 2023 to date. RetailNext data showed that in-store foot traffic was up 2% from last year on Black Friday, an improvement from the recent trend of -2% to -5% over the preceding month. The report showed that foot traffic on Friday and Saturday combined was 1.6% above 2022 levels.

{kind=link}

While the recent pullback in mortgage rates has brightened the outlook for the sluggish housing market, data this week showed the effects of the late-summer surge in mortgage rates to above 8%. New Home Sales slid 6% in October from the prior month to a seasonally adjusted annual rate of 679k - well below consensus estimates of roughly 730k - while sales data in September was revised lower as well. New Home Sales remained higher by nearly 20% from a year earlier, however, as the largest single-family homebuilders have been able to cope with multi-decade-high mortgage rates by leveraging their platform's scale and relatively healthy balance sheet to offer more attractive financing options than what's currently available for prospective homebuyers in the traditional existing home sales market. Supply levels of new construction homes remain low on a historical basis, with newly completed homes being sold within 2.5 months of listing in the latest report - well below the pre-pandemic average of roughly 3.5 months. The median sales price of new houses sold in October 2023 was $409,300, which is 18% below the peak in October 2022, but still 27% above pre-pandemic levels from October 2019. By comparison, CPI has increased by 20% during this time.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

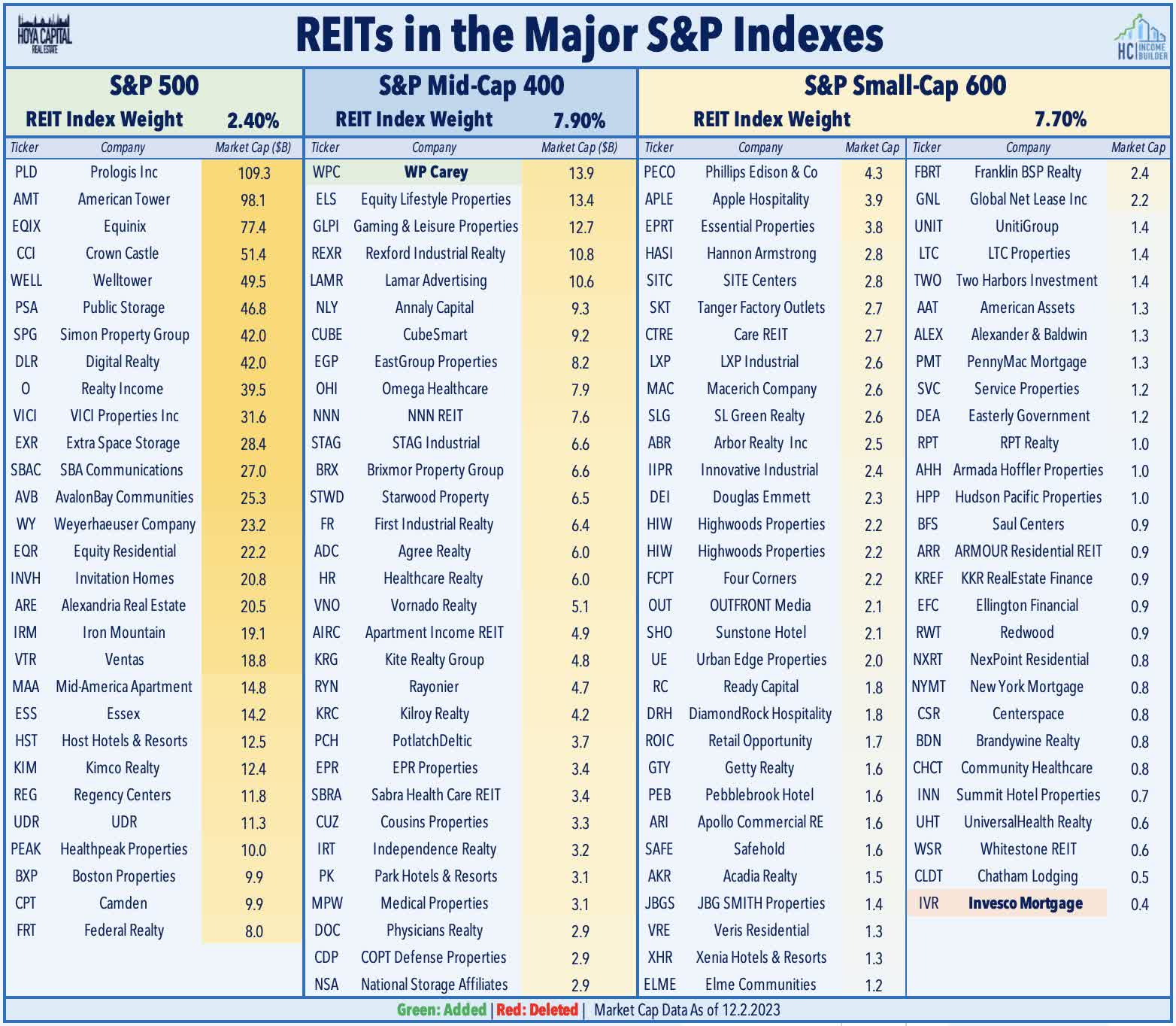

Net Lease : Fund flows were a major theme this week as the combination of index rebalancing and a forceful shift in sentiment sparked a double-digit surge this week from many of the most beaten-down REITs. W. P. Carey ( WPC ) - which we own in the REIT Focused Income Portfolio - rallied nearly 8% this week after S&P announced that it would add WPC to the S&P MidCap 400 index. WPC - which has a market capitalization of $13.6B - had previously been the largest REIT excluded from any of the major indexes. This exclusion was partially a byproduct of its classification as a "diversified" REIT, which WPC has addressed through its "strategic exit" out of the office segment announced earlier this quarter. Later in the week, S&P announced that mortgage REIT Invesco Mortgage ( IVR ) - which was the smallest REIT in any of the major indexes - would be dropped from the S&P 600 . Also of note, Housing 100 Index component Builders FirstSource ( BLDR ) was added to the S&P 500 . REITs comprise only 2.4% of the benchmark S&P 500 , but are better-represented in the mid-cap and small-cap indexes with a 7.9% and 7.7% weighting in the S&P 400 and S&P 600, respectively. Of note, the total value of the U.S. commercial real estate market is roughly $20 trillion, while the total value of the U.S. equity market is roughly $45 trillion.

{kind=link}

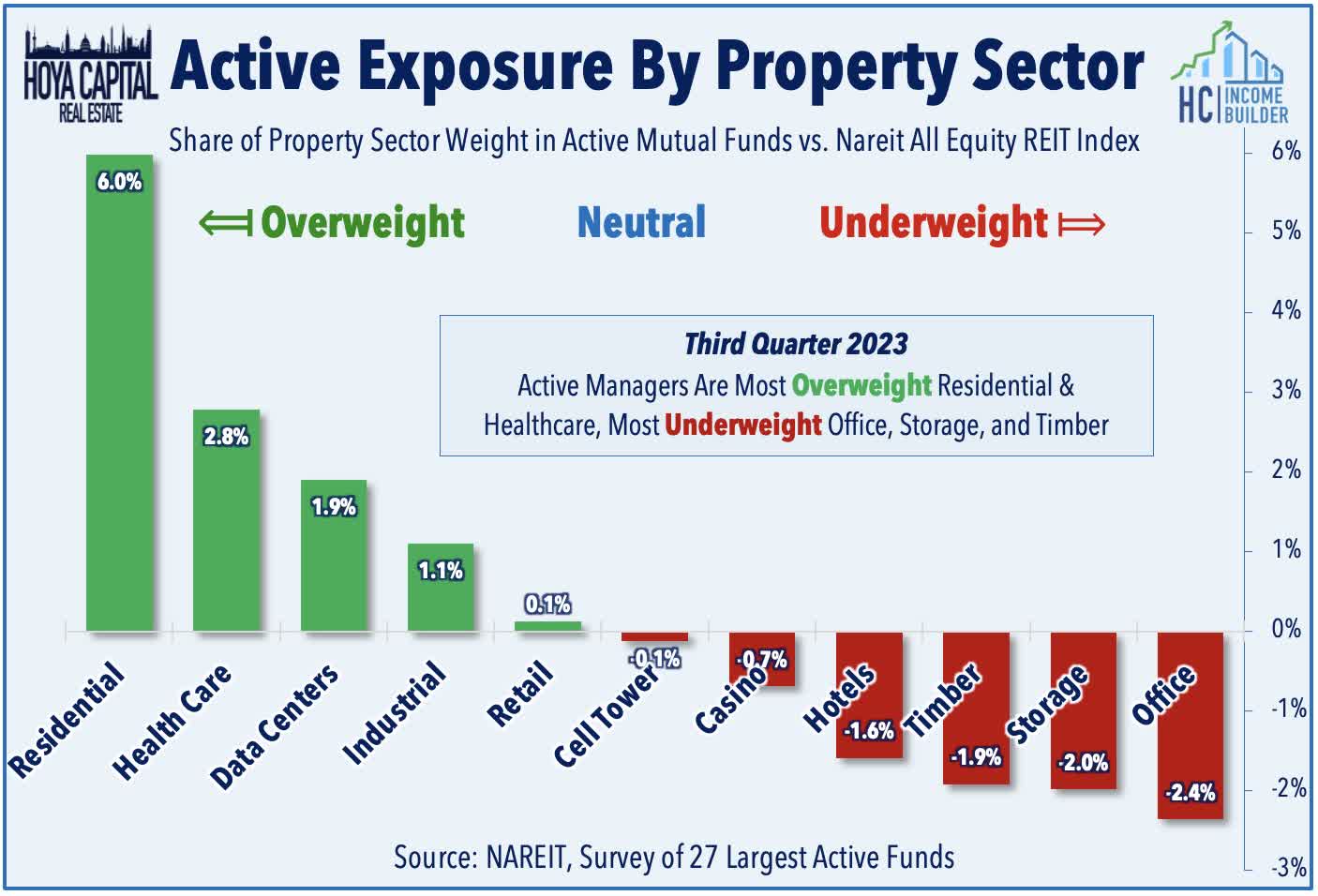

Office : On a related theme, office REITs - the most underweight property sector among active managers and the most heavily-shorted corner of the REIT sector - surged by nearly 15% this week as the sharp retreat in interest rates has lifted some of the gloom from the beaten-down sector and sparked a short-covering rally in recent weeks. Office REITs have become one of the most rate-sensitive property sectors during the Fed rate hiking cycle due, in part, to their relatively highly-leveraged balance sheets and higher use of variable rate debt. NAREIT published a report this week showing that - among the 27 largest active REIT funds - office REITs are the most "unloved" property sector with an average relative underweight of 2.7% compared to the cap-weighted All Equity REIT Index. By comparison, active managers have a 6.0% overweight position in the residential sector and a 2.8% overweight in healthcare REITs. Also of note, data centers REITs have seen the biggest increase year-over-year at 3.9 percentage points, while funds have been selling off self-storage since the fourth quarter of 2022, posting the largest year-over-year decline at 4.5 percentage points.

{kind=link}

Cell Tower : Crown Castle ( CCI ) - one of our three Best Ideas In Real Estate - rallied over 14% this week on reports that activist investor Elliott Investment Management has taken a $2 billion stake in the cell tower REIT after its initial campaign in 2020 was "disregarded... and its recommended changes were neither made nor taken seriously." The investment firm - which had previously disclosed a $1B stake in 2020 - published a new letter calling for board and executive changes and a "re-evaluation" of its strategy around its fiber business, which Elliott blames for its underperformance relative to its cell tower REIT peers, American Tower ( AMT ) and SBA Communications ( SBAC ) over the past several years. Contrary to its peers, Crown Castle has focused exclusively on the U.S. market, and has incrementally invested more heavily in small-cell and fiber networks in recent years, while AMT and SBAC have invested more in traditional macro tower networks in international markets. Elliott remarks that CCI's fiber spending "has pushed CCI's financial profile far away from its stated 7% to 8% dividend growth rate," and calls for "all aspects of the fiber strategy to be re-evaluated."

{kind=link}

Healthcare: Lab space operator Alexandria Real Estate ( ARE ) - which we own in the REIT Dividend Growth Portfolio - surged more than 12% this week after providing an operating update at its Investor Day conference in which it affirmed its 2023 FFO guidance and provided its initial 2024 guidance calling for FFO growth of 5.5% and same-store NOI growth of 4.0% at the midpoint of the respective ranges. In a wide-ranging presentation, ARE highlighted the strength of its best-in-class balance sheet - noting that 99% of its debt is fixed rate with a weighted average term remaining of 13 years - and that 92% of its leases are structure as triple-net leases with an average annual escalation of 3%. ARE expects its occupancy rate to end 2024 at 95.1% at the midpoint - flat with its expectations for 2023 - and expects to report cash rent spreads of 9.0%, a moderation from the 14.5% rent spreads expected this year. The lab space segment has been under pressure over the past eighteen months as the combination of a post-pandemic moderation in biotech hiring and significant supply growth has sent average vacancy rates to over 10%, per the latest CBRE report , which is above the 8% pre-pandemic average. CBRE notes, however, that venture capital funding for life sciences firms increased for the second consecutive quarter in Q3 and was on par with the early 2020 average.

{kind=link}

Mall : Tanger ( SKT ) gained 3% this week after it announced a $194M deal to acquire Bridge Street Town Centre - a 825,000 sf open-air lifestyle center in Huntsville, Alabama. The shopping center - which is 93% occupied- features 80 retail stores, restaurants, and entertainment venues. A departure from its traditional outlet center focus, Bridge Street is Tanger's second open-air lifestyle property and is the company's third portfolio addition this quarter following the opening of Tanger Nashville in October and the acquisition of Asheville Outlets in early November. Tanger expects the center to deliver a first-year return "in the mid-eight percent range" and will fund the acquisition using cash on hand and available liquidity. As noted in our Earnings Recap , retail real estate fundamentals are as strong as they've been in at least a decade, which has allowed several REITs with well-capitalized balance sheets to become more aggressive on the M&A front. Tanger reported in Q3 that its comparable occupancy climbed to 98.0% - the highest since 2016 and up 160 basis points from last year - which has driven year-to-date NOI growth of 6.5%. Leasing activity and rent growth has also been impressive in recent quarters following a stretch of nearly three years of negative rent spreads. Tanger reported blended spreads of 14.5% - the strongest since 2016 and the seventh-straight quarter of positive spreads.

{kind=link}

Hotel : Pebblebrook ( PEB ) gained 5% this week after it announced an update on recent operating trends, noting that October operating results were at the high end of expectations as Same-Property RevPAR increased 2.8% versus the prior year period, and Non-room Revenues grew by 4.9% while urban Same-Property RevPAR rose by 4.8%, driven by strength in Boston, Washington DC, San Francisco, and Los Angeles plus Resort Same-Property RevPAR experienced a 3.6% decrease, significantly improved from prior months, as demand and rates begin to stabilize and Operating Expenses overall were well controlled. Apple Hospitality ( APLE ) gained 3% this week announced that it completed the acquisition of the 192-room Embassy Suites by Hilton in Salt Lake City for approximately $36.8M (~$191k/key). The TSA announced this week that the U.S. saw the busiest day for air travel ever during the Thanksgiving weekend with more than 2.9 million people screened at checkpoints. Checkpoint data from the Thanksgiving weekend shows that throughput has climbed to over 105% of 2019 levels during November - the highest since the pandemic - while hotel data provider STR reports that industry-wide Revenue Per Available Room ("RevPAR") was 17% above 2019 levels in October, as a roughly 21% relative increase in Average Daily Room Rates ("ADR") offset a roughly 3% relative drag in average occupancy rates.

{kind=link}

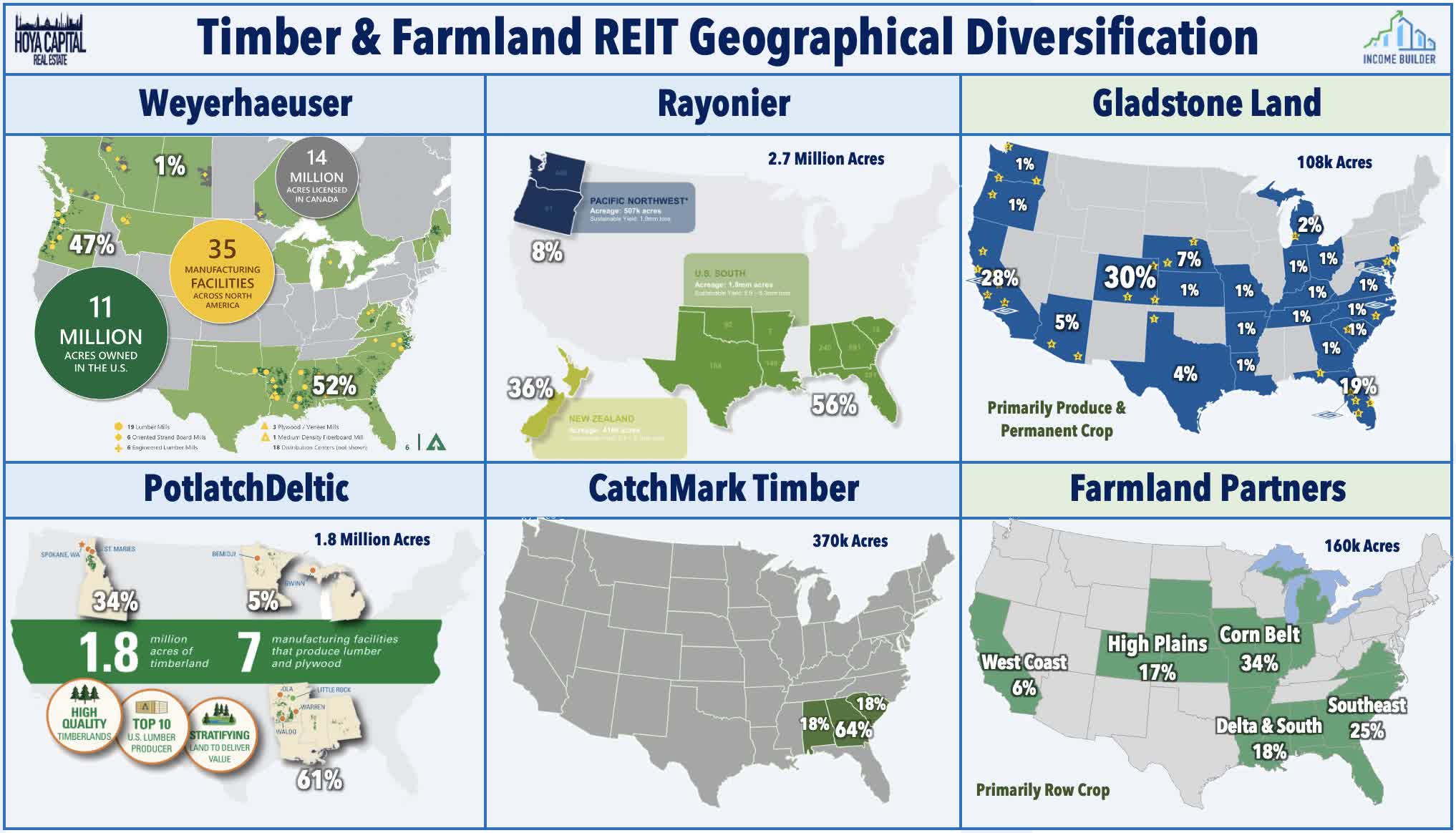

Timber : Weyerhaeuser ( WY ) traded flat this week after it announced it has entered into two distinct agreements with Forest Investment Associates to divest approximately 69,600 acres in South Carolina for $170M and to purchase approximately 60,700 acres of timberlands in North Carolina, South Carolina, and Mississippi for $163M. The land swap is expected to "optimize" WY's Southeast timberland portfolio to be better-located relative to its sawmill and distribution operations. The deal is expected to close by the end of the year. WY owns 870k acres of timberlands in North and South Carolina and approximately 1.2M acres in Mississippi. Roughly half of WY's revenues emanate from its Southern US portfolio, with the other half emanating from the Pacific Northwest. Lumber prices have stabilized this year at around $500 per thousand-foot board ("MBF"), which follows a two-year period of extreme swings during the pandemic in which prices peaked in May 2021 at over $1,500 MBF and bottomed in January 2023 at around $400 MBF.

{kind=link}

Manufactured Housing : UMH Properties ( UMH ) gained 3% this week after it announced that it expanded its partnership with Nuveen Real Estate through a new joint venture to develop a new manufactured housing community in Honey Brook, PA comprised of 113 MH sites. The development is nearby to two existing UMH communities which have a combined occupancy of 98% with rents averaging $700 per month. UMH will have a 40% stake in the JV and will serve as the managing member, developer, and operating member upon completion. Construction of the community is expected to commence in the next few weeks and should take about 15 months to complete, and UMH will also have the right to purchase the community from the JV after a certain period of time. The deal is the third joint venture between the UMH and Nuveen, having previously partnered to acquire two communities in Florida for a combined purchase price of $37M. UMH Properties now owns and operates 135 MH communities containing approximately 26k developed sites.

{kind=link}

This week, we published our State of the REIT Nation, which noted that two years of persistent rate-driven pressure on residential and commercial real estate markets appears to finally be abating as the worst of pandemic-era inflationary pressures subside. This 'light-at-the-end-of-the-tunnel' comes as commercial property values were approaching the critical 20% drawdown level a level that can result in cascading distress that extends beyond the weakest players. We're not out of the woods, yet, as expectations of "Higher for Longer" are merely shifting to "High for Long" in which benchmark rates will remain materially above pre-pandemic levels into 2025. The 'unwind' is just beginning for the "Zero-Rate Heroes," however, as the business models of many private equity funds and non-traded REITs are contingent on cheap and plentiful debt, which counteracted the drag from higher fees, inefficient structure, and often poor governance. We noted that macroeconomic conditions are aligning in an ideal manner for low-levered entities with access to "nimble" equity capital - conditions that maximize the true competitive advantage of the public REIT model, which these entities have been unable to exploit in the "lower forever" environment.

{kind=link}

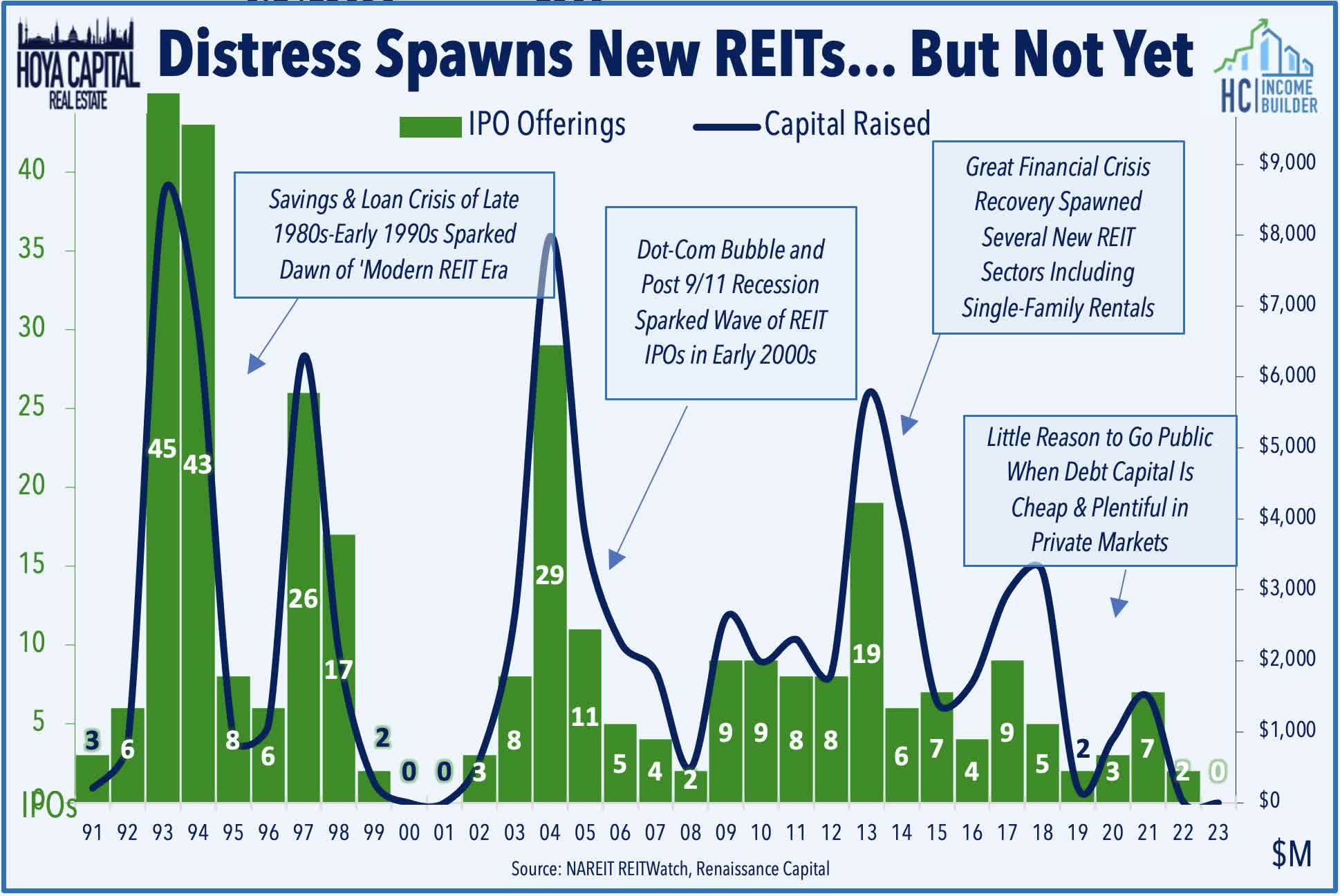

We also noted that while past periods of significant tightening were remembered as those of distress in the broader real estate sector, they can rightfully also be remembered as periods of a significant rebirth that spanned many of the public REITs that exist today. The S&L Crisis of the late 1980s - which resulted in the failure of nearly a third of community banks and resulted in significantly constrained access to debt capital - spawned the dawn of the 'Modern REIT Era.' A second wave of REIT IPOs followed in the aftermath of 9/11 and again after the Great Financial Crisis as the limited access to (and high cost of) debt capital, combined with a lift in equity market valuations of public REITs - pushed highly-levered private portfolios into the public equity markets, a theme that we could very well see repeat over the coming quarters. On cue, Bloomberg reported this week that Lineage Logistics - one of the largest cold-storage logistics property owners - is considering an IPO next year at a valuation of more than $30B. Lineage operators over 400 cold-storage units in North America and Europe, and competes with Americold Realty Trust ( COLD ), which has more than 240 facilities.

{kind=link}

Mortgage REIT Week In Review

Mortgage REITs resumed their powerful rebound as well this week, with the iShares Mortgage REIT ETF ( REM ) surging 5.3%. Since the recent lows on October 27th, the Mortgage REIT Index has rallied 22.5%, outpacing the 17.5% advance on the Equity REIT Index. Mortgage REITs were in focus after Pimco co-founder Bill Gross highlighted two mREITs - Annaly Capital ( NLY ) and AGNC Investment ( AGNC ) - as beneficiaries of the interest rate retreat. Multifamily lender Arbor Realty ( ABR ) led the way this week with double-digit gains after Fitch Ratings affirmed ABR's primary and special servicer ratings with a Positive outlook, pushing back on recent claims in a short report by Viceroy Research earlier this month that ABR's portfolio is more troubled than the company claims. ACRES Commercial ( ACR ) - which has not paid a dividend since 2019 - was among the laggards this week after announcing that it authorized the continued use of its share repurchase program, to repurchase up to $4.1M of common stock previously approved plus an additional $10M of the outstanding shares of both its common and preferred stock.

{kind=link}

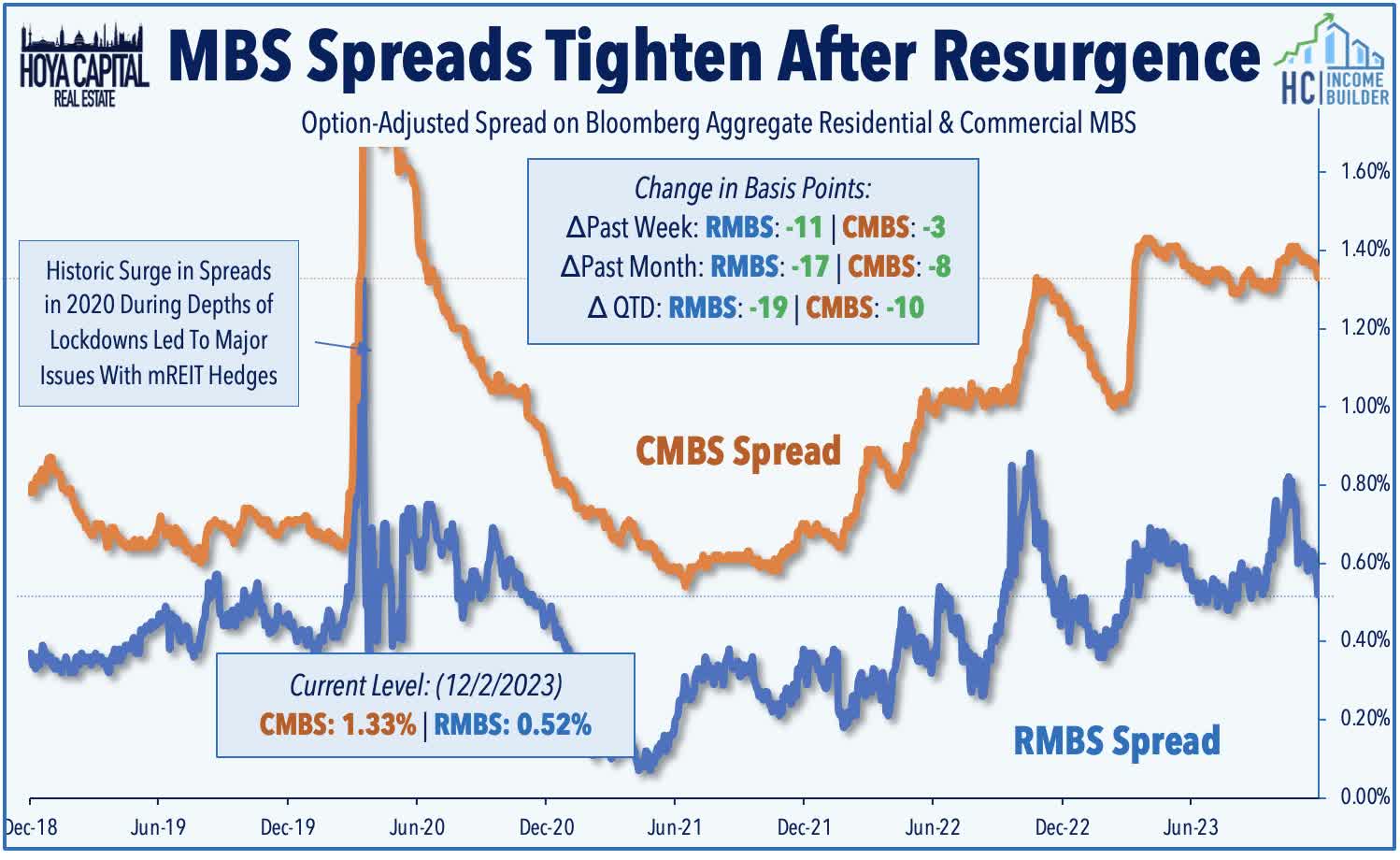

Elsewhere, Ellington Financial ( EFC ) was little changed this week after reporting that its estimated Book Value Per Share ("BVPS") was $14.10 as of Oct. 31, down about 1.5% from $14.33 in September. EFC also declared an interim monthly dividend of $0.06/share to reflect the timing of its pending acquisition of Arlington Asset ( AAIC ), which it expects to close on December 14th. In our Earnings Recap , we noted that the (now largely reversed) surge in interest rates and MBS spread-widening wreaked havoc on residential mortgage REITs during the third quarter, resulting in a significant deterioration in book values for mREITs focused on government-backed ("agency") residential MBS. Agency-focused mREITs reported an average decline in Book Value Per Share ("BVPS") of 13.1% during the quarter, but credit-focused mREITs reported more muted declines in BVPS, averaging around 5%. On the commercial mREIT side, the movement in BVPS was far more muted, with an average decline of about 1% in the third quarter. Residential MBS spreads have compressed by 19 basis points since the start of Q4, while Commercial MBS spreads have tightened by about 10 basis points.

{kind=link}

REIT Capital Raising & REIT Preferreds

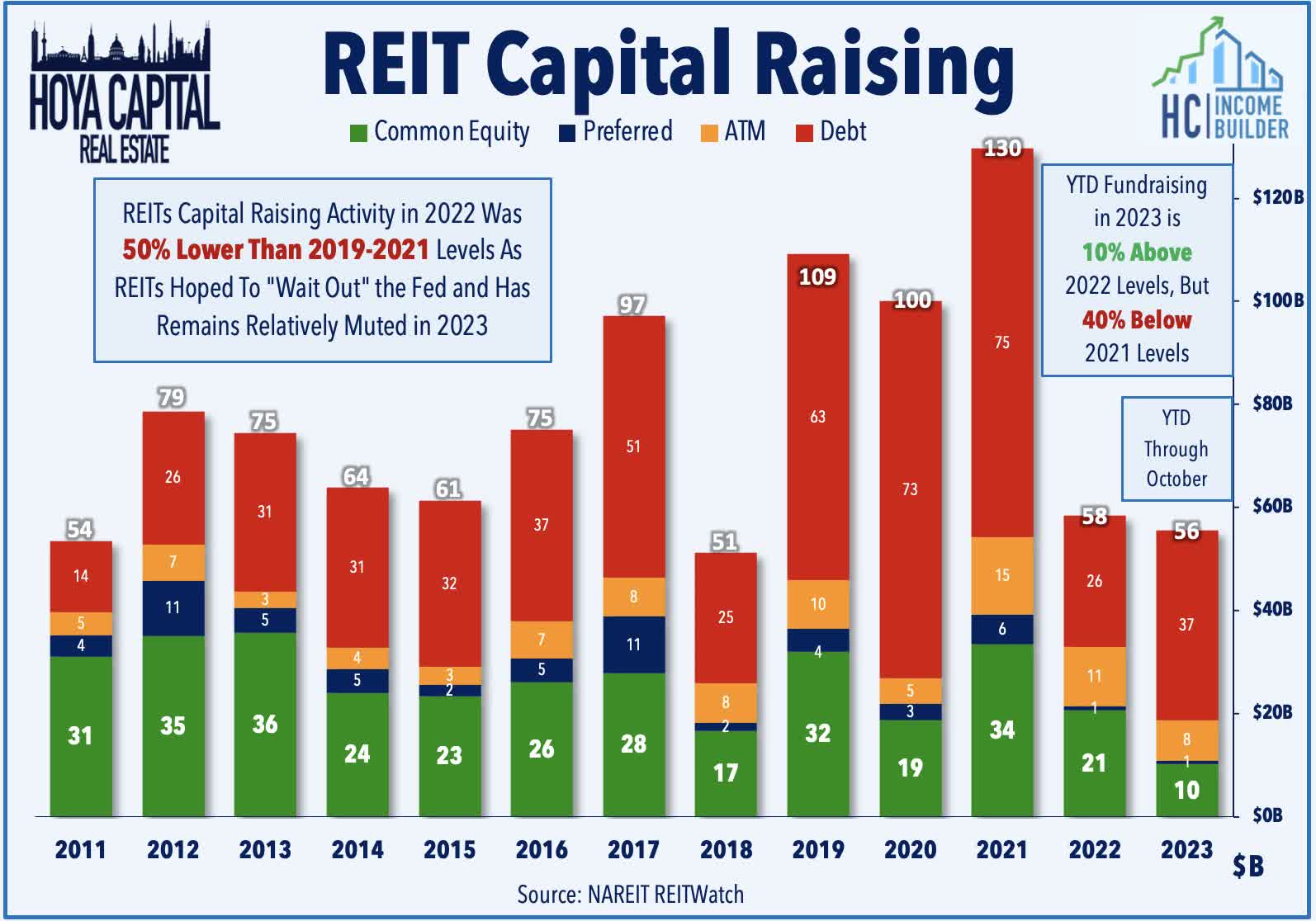

Several REITs were active on the capital-raising front this week, quickly taking advantage of the recent retreat in interest rates. Net lease REIT Realty Income ( O ) raised £750 million - roughly $950M - across two long-term bond offerings: £300M of 8-year senior unsecured bonds priced at 5.75%, and £450M of 16-year senior unsecured bonds at 6.00%. Storage REIT Extra Space ( EXR ) raised $600M through a public offering of an 8-year senior unsecured bond priced at 5.90% S&P reported last week that REIT capital-raising activity is trending at levels that are about 10% above 2022 levels, but still 40% below the record-setting pace from 2021. On the credit rating front, a pair of office REITs received credit rating downgrades this week. S&P Global lowered office REIT Piedmont's ( PDM ) issuer and issue-level ratings on the company to “BBB-“ from “BBB” with a negative outlook, while Moody’s downgraded Office Properties Income 's ( OPI ) corporate credit rating and senior unsecured debt ratings to “Caa1” from “B2” with a negative outlook. Fitch Ratings affirmed the ratings for COPT Defense ( CDP ) including its “BBB-“ Long-Term Issuer Default Ratings with a stable outlook.

{kind=link}

2023 Performance Recap & 2022 Review

With just four weeks left in 2023, the Equity REIT Index is now higher by 1.5% on a price return basis for the year (4.7% on a total return basis), while the Mortgage REIT Index is higher by 3.1% (+13.1% on a total return basis). This compares with the 20.0% gain on the S&P 500 and the 8.4% gain for the S&P Mid-Cap 400 . Within the real estate sector, nine property sectors are now in positive territory on the year, led by Data Center, Single-Family Rental, and Mall REITs, while Net Lease and Farmland REITs have lagged on the downside. At 4.23%, the 10-Year Treasury Yield has climbed 35 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - but down from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index is slightly higher this year, producing total returns of 2.5% thus far. WTI Crude Oil - perhaps the most important "swing" inflation input - is now lower by 1.2% this year, while Natural Gas is lower by over 60% this year.

{kind=link}

Economic Calendar In The Week Ahead

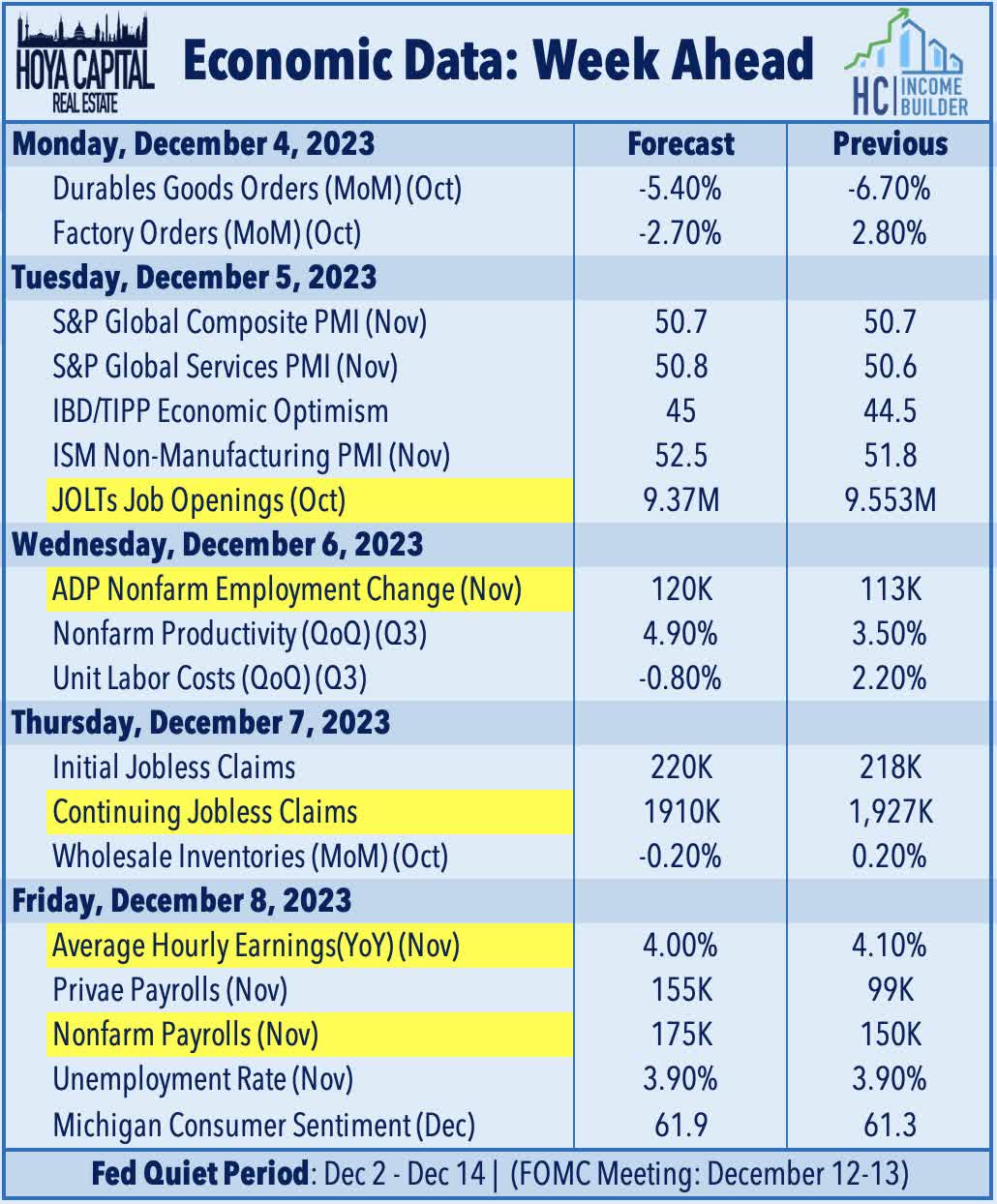

Employment data highlights another critical week of economic data in the week ahead, headlined by the JOLTS report on Tuesday, ADP Payrolls data on Wednesday, Jobless Claims data on Thursday, and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 175k in November, which follows a softer-than-expected October in which the economy added 150k jobs. The closely-watched Average Hourly Earnings series within the payrolls report - which is the first major inflation print for November - is expected to show a cooldown in wage growth to 4.0%. 'Good news is bad news' will likely remain the theme of these reports as several Fed officials have pinned their decisions to pivot away from aggressive monetary tightening on a long-awaited cooldown in labor markets. We'll also be watching the Productivity and Costs report on Wednesday - which includes the Unit Labor Costs metric - along with a busy slate of Purchasing Managers Index ("PMI") data throughout the week. As the Fed enters the "quiet period" ahead of its policy decision on December 13th, swaps market now imply that the likelihood of another rate hike is less than 5%, while there's now an over 60% probability that the Fed will cut rates for the first time by March and imply a year-end policy rate of around 4.0% - down from 5.5% today.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Pivot Pending