PZA:CC - Pizza Pizza: 6.5% Yield With Loads Of Pizzazz

2023-11-21 16:18:45 ET

Summary

- Pizza Pizza earns royalty income from two quick service restaurant franchises.

- This royalty play has recovered all the ground that was lost during the pandemic. The dividends are also at an all-time high level.

- We review the recent results and provide an update on our outlook for this company.

All values are in CAD unless noted otherwise.

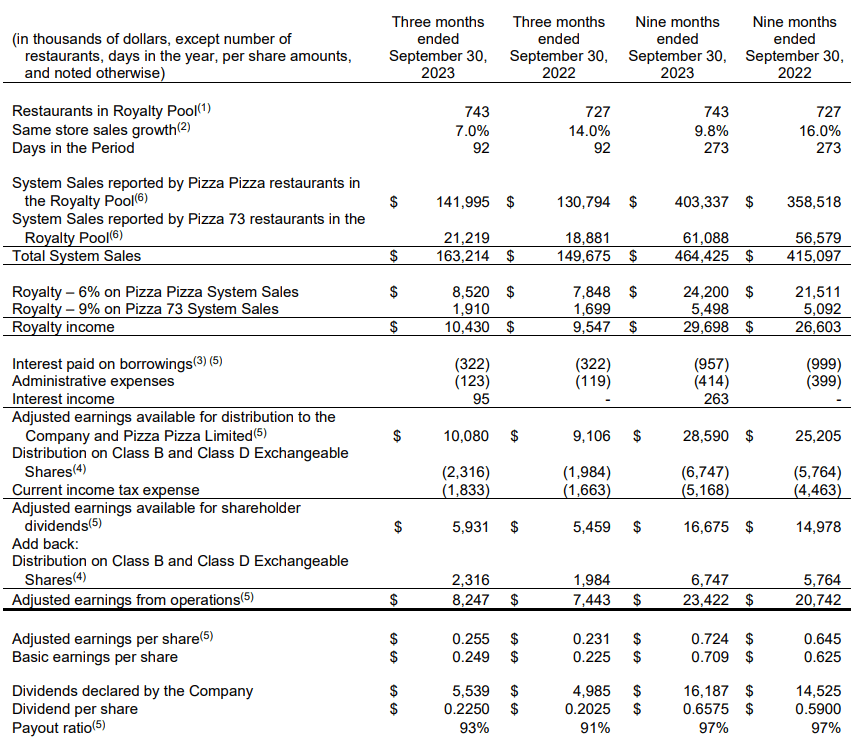

Pizza Pizza Royalty Corp. ( PZRIF ) ( PZA:CA ) earns royalty income from two Canadian quick service restaurants, Pizza Pizza and Pizza 73. It earns 6% on the gross sales from 644 Pizza Pizza restaurants and 9% on gross sales from 99 Pizza 73 restaurants in the royalty pool. This pool is adjusted on January 1 each year, to account for the net new restaurants that opened in the preceding 12 months. As of September 30, 2023, the net number of Pizza Pizza and Pizza 73 locations had increased by 17 and 3, respectively. So we can reasonably assume that the pool will be adjusted to the upside on the 2024 adjustment date. Starting October 2024 , PZRIF will also receive 12.5% in royalties from PZA Pizzeria restaurants in Mexico. Since these do not impact the current financial results, we will only be focusing on the Canadian operations in this piece.

Just like the other royalty plays that we have covered in the past, like A&W Revenue Royalties Income Fund ( AWRRF ) ( AW.UN:CA ) and Diversified Royalty Corp. ( BEVFF ) ( DIV:CA ), this royalty corp also has a streamlined expense structure. The path from royalty income to net profit is short for PZRIF and comprises administration expenses, interest on debt and income taxes. The company maintains a reasonable cash reserve and distributes the balance to its shareholders. The dividend is fully funded by cash flows and the more it makes, the higher is the shareholder payout.

Q3-2023 MD&A

With the recent dividend hike from 7.5 cents to 7.75 cents, the stock now yields 6.46% (current price $14.40). In comparison, A&W yields 6.2%, while Diversified yields close to 9.5%.

Prior Coverage

We were neutral on the royalty corporation back in June of this year. It was trading at 15X forward earnings at the time and that was outside of our comfort zone, given the macro conditions. We were hard pressed to find any cracks in its Q1 results, but with risk-free rates at 5%, downward pressure on PZRIF's price was inevitable in our opinion.

You could overlook this multiple in a zero interest rate era, but with risk-free rates at 5%, we think a lower multiple is almost inevitable. The yield is 5.8% but Pizza Pizza will cut it immediately if earnings decline. They are not going to lever up to appease the dividend groupies. We are hence moving this to a "Hold/Neutral" rating. We would likely move to a "buy" under $13.00 and a "Sell" over $16.00.

Source: Pizza Pizza: The Inflation Hedge Delivers Once Again

The price declined slightly, but the dividends kept its investors afloat since that time.

If you used our buy under price, from the previous article, as the maximum you would pay, well you got a great entry as PZRIF spent exactly one day under that.

{kind=link}

Of the royalty plays on our radar, only Boston Pizza Royalties Income Fund ( BPF.UN:CA ) has done better, with the price action actually adding to the total return.

Today we will review PZRIF's Q3 results and provide an update to our outlook from June.

Q3-2023 Results

In a reversal of fortunes, Pizza 73 led Pizza Pizza in same store sales growth this quarter. We can see why this would be a surprise, considering the difference between the two in the 2022 numbers.

{kind=link}

Q3-2023 MD&A

Management explained the resurgence of the Pizza 73 numbers during the conference call.

So I'd say that Pizza 73, for instance, we had a lot of innovation there. I tried to touch on that in my formal remarks. With chicken snacker boxes, curly fries poutine. We have Gourmet Thins out there, which was a real success out of Pizza Pizza. So we bridge that over as well. So there's actually a lot more available and especially in the snacking dayparts there that represent great value out there. And so we think that's resonating.

We also think that the new website and app that we launched a while go back there, they seem to get some pretty quick traction. It's just easier to use. People like ordering that way. And these new items that we introduce are really -- they obviously work very well for delivery. But for pickup, they sort of -- or walk-in sales, they work really well.

Source: Q3-2023 Earnings Call Transcript

While the overall growth lagged 2022, it was a still a solid 7% year over year. Comparing the numbers for the two years is not really akin to comparing a pair of Granny Smith apples, since the growth numbers for 2022 only shone brighter because 2021 still had COVID related restrictions in place. The two pizza brands continued to witness increase in foot traffic (walk in customers/order pickup) and the average amount spent by customers during this quarter. The company also attributes the success in achieving the higher volumes to innovative menu offerings, along with technological and infrastructural improvements for a seamless order placement process. Marketing campaigns that spoke to the inflation weary crowd also worked like a charm.

this summer, unlike some companies who hopped on the popular shrink inflation bandwagon, in other words, shrinking the size of volume of their product, but still selling it for the same price, Pizza Pizza announced its grow inflation campaign to come back to inflation by giving our medium pizza instead of a small pizza for the same small price. This campaign continues to highlight our promotional and value offerings that speak to the pressures Canadian feel related to rising interest rates and price inflation.

Source: Q3-2023 Earnings Call Transcript

We have noticed this shrink-inflation in our dine-ins and dine-outs. Restaurants in general are getting stingy and PZRIF going the other direction will definitely garner goodwill. The Q3 numbers bode well for the holiday-littered Q4, which has traditionally and unsurprisingly been the strongest for this business. Management, while optimistic, was prudent not to get ahead of themselves when asked about their expectations for the last quarter of this year.

And seasonally, this is volume-wise, is always a good quarter for us, but we're certainly aware of strong competition and a value-oriented customer. So we know that we have to be very careful to make sure we stay relevant.

Source: Q3-2023 Earnings Call Transcript

The overall royalty income was higher by 9.2%, led by the increase in the total restaurants in the pool.

{kind=link}

Q3-2023 MD&A

The year over year expenses remained steady, in no small part due to the interest rate on debt being fixed via swaps until April 2025. The rate on the $47 million credit facility is 1.81% plus a credit spread that depends on the debt to EBITDA levels.

Q3-2023 MD&A

The rate was 2.685% for both the current and comparative quarter. While the royalty corp is well set until 2025 vis a vis its interest rate, management anticipated new store openings to slow down in 2024 due to the high cost of financing. They addressed it as a headwind and unlike the 3% plus growth in the year to date royalty pool, the expectation was that this number would come in under 3% in 2024. Coming back to PZRIF, the company is also well set in terms of its working capital at the end of Q3.

{kind=link}

Q3-2023 MD&A

Management chimed in about their comfort levels with the numbers and the payout ratio during the earnings call.

The company targets a payout ratio at/or near 100% on an annualized basis. The company's working capital reserve increased $400,000 during the quarter and was $8 million as of September 30, 2023. With today's dividend increase, the company believes that there is sufficient cash flow to service the obligations as they fall due. And the company will continue to closely monitor sales, royalty income and net income to determine when additional dividend adjustments may be warranted.

Source: Q3-2023 Earnings Call Transcript

PZRIF will start receiving royalties from its Mexico operations in Q4 2024. Perhaps that will stem some of the slowdown that recessionary forces will bring next year.

Valuation and Verdict

PZRIF has held up really well and recovered all the lost ground since the pandemic. We had a buy under price of $13 in our last piece and if you took it (you lucky dawg), we would continue to hold. For a fresh buy, we prefer the beaten down Diversified Royalty at this point. It trades at 9X free cash flow versus around 15X for PZRIF. On a standalone basis too, we get a close to 10% yield from the former versus the 6.5% for PZRIF. The company is well run, but getting in at the right time determines the final outcome of the investment. We continue to stay out.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints. We are long the TSX traded debentures of DIV.

For further details see:

Pizza Pizza: 6.5% Yield With Loads Of Pizzazz