PLNT - Planet Fitness: A Fit Stock With Fat Debt

2024-01-10 10:58:12 ET

Summary

- Planet Fitness is a large gym franchise with a successful business model and a focus on providing great value to customers.

- The company has a significant amount of long-term debt maturing in the next five years, which may require taking on more debt to finance the existing obligations.

- The recent stock rally has left current stock prices at what I believe is a fair valuation even considering a positive 12% EPS growth rate for FY24.

- Therefore, I find it impossible to advocate building a position in Planet Fitness from a deep-value or even GARP perspective.

- Hold rating issued.

Investment Thesis

Planet Fitness ( PLNT ) is one of the largest gym franchises in the world. Their massive scale, effective franchise model and great value offering to customers has allowed the firm to grow rapidly while maintaining profitability and cash flows.

However, the firm has a huge portion of long-term debt maturing the next five years which will almost certainly force the firm to take-on more debt to finance these maturities.

When combined with a recent stock rally of almost 70% leaving shares at what is a fair valuation in my opinion considering the firm's expected FY24 EPS, there is simply not enough margin of safety for me to advocate the building of a position in shares from a value perspective.

Therefore, I currently rate Planet Fitness a Hold.

Company Background

Planet Fitness is one of the largest fastest-growing franchisors and operators of fitness centers with more members than any other fitness brand in the world. The firm has more than 18.5 million members across over 2498 owned and franchise locations.

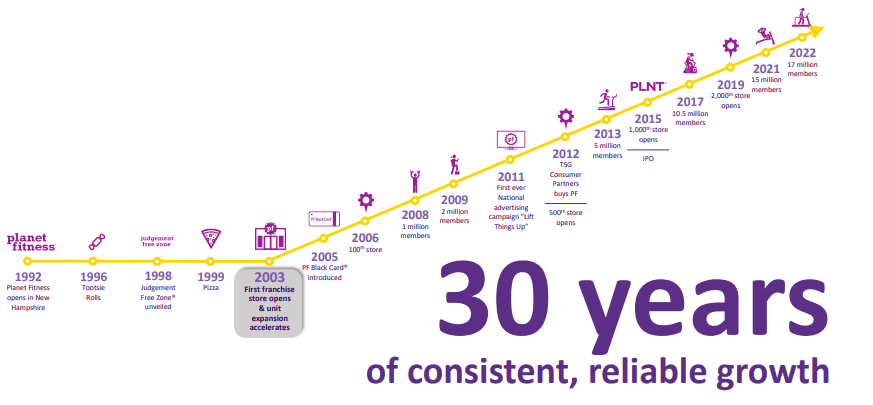

Since the firm’s founding in 1992, Planet Fitness has grown to become a globally renowned fitness powerhouse thanks to a 2003 decision to franchise the gym model. The utilization of a lucrative franchise model much like that employed by McDonald’s (MCD) enabled PF to grow rapidly and expand into new regions of both the United States and beyond.

Today PF operates in the U.S, Puerto Rico, Canada, Panama, Mexico and Australia with the firm priding themselves on the holistic gym experience provided to customers. The brands “Judgment Free Zone” trademark fundamentally underpins Planet Fitness’ ethos which is to create a welcoming and non-intimidating environment for all athletes, regardless of skill or fitness level.

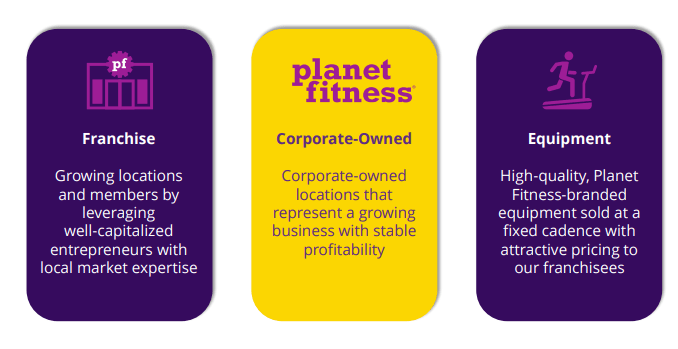

The firm operates three distinct lines of business including the licensing and selling of franchises under the Planet Fitness name, the owning and operating of fitness centers and the selling of fitness-related equipment to franchisee-owned stores.

Previous CEO Chris Rondeau spent over 30 years at Planet Fitness having worked his way up from the front desk to the head of the company. However, after departing from his position at the helm in September, Craig Benson has been appointed as interim CEO.

More information is needed surrounding the dismissal of Rondeau for a thorough understanding to be developed into this issue with the firm’s shareholders. However, for the time being Benson appears like a good fit for the role of CEO given his extensive experience both within Planet Fitness and within the franchising industry as a whole.

Economic Moat – In-Depth Analysis

Planet Fitness has a narrow economic moat within the fitness and gym industry. This moat is built primarily upon their massive scale generating unparalleled market reach and some tangible cost advantages.

At the very center of Planet fitness’ business model is the athlete. The entire PF ethos is centered around providing the customer a great gym-going experience and offering more than their competitors do to create a real value offering.

PF tends to primarily offer two tiers of membership : classic and the PF Black Card. Classic membership enables gym goers to enjoy unlimited access to their local PF “club” (which PF uses as a synonym for gym) along with some partner rewards and discounts, PF app workouts and free in-club fitness training.

planetfitness.com | Memberships

The classic tier is usually priced around the $10 mark and offers customers with no minimum membership term and a very small $49 annual fee intended to cover account setup and organizational costs.

planetfitness.com | Memberships

Planet Fitness’ Black Card allows members to enjoy unlimited access to PF clubs around the world, the ability to bring a guest to the gym anytime, use of auxiliary services such as tanning, massage chairs, total body enhancement and HydroMassage.

Considering that customers pay only $25 a month for the PF Black Tier and the same $49 annual fee, it is clear that PF has built an attractive pricing ladder that presents customers with much greater perceived value for money by signing up for the slightly more expensive Black Tier membership plan.

Regardless of which plan customers go for, Planet Fitness is known in fitness circles for being budget-friendly and almost omnipresent with their 24/7 access touted as a big pro for potential customers.

Planet Fitness also prides themselves on being an incredibly beginner-friendly gym with a significant emphasis being placed on making sure gym goers feel comfortable at their clubs, regardless of fitness level or skill.

{kind=link}

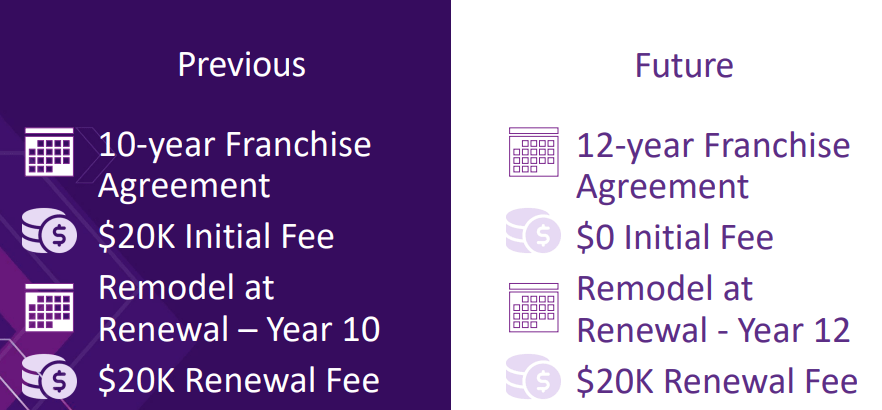

The gyms themselves are traditionally in great shape and very clean. Franchisees have traditionally been offered 10-year franchise agreements with a remodel at agreement renewal (every 10 years). This has recently been agreed to be extended to 12 years to ensure franchisees receive adequate ROI from their clubs.

This upgrade cycle allows Planet Fitness to accurately track how many of their clubs are in what stage of gym equipment lifecycle which enables the firm to accurately predict remodeling rates and costs.

{kind=link}

By franchising the gyms since 2003, Planet Fitness has managed to spread their successful gym formula across North America by quickly and efficiently opening new locations in almost every region of the continent.

Fundamentally, Planet Fitness has managed to create a formula for the opening, running and renewal of gyms which resonates with customers all for a relatively low monthly membership fee. This affordable and mostly high-quality product offering is now so prevalent that Planet Fitness is often viewed as the go-to beginner or budget gym.

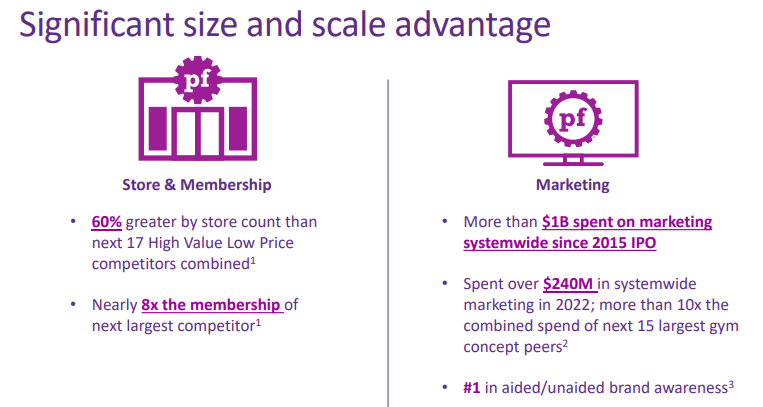

Such a massive market awareness of the Planet Fitness brand combined with a great perceived value offering to customers creates massive networking effects which drives customer referral rates and overall traffic to Planet Fitness gyms.

{kind=link}

The massive scale Planet Fitness has now achieved also enables the firm to significantly reduce the overall costs associated with running each and every franchise which ultimately helps increase both the returns generated by individual franchisees and the company themselves.

{kind=link}

Planet Fitness sells equipment to franchisees too which helps generate further revenues for the firm.

It must be noted that Planet Fitness generates more revenue from their corporate owned stores than they do from franchise locations. Planet Fitness’ propensity to operate stores in-house suggests that the firm is confident both in the quality and profitability of their business model which acts as a great confidence booster for existing franchisees.

Overall, I believe PF has a narrow economic moat that is built upon their scale, reputation and the ensuing cost advantages. The lack of tangible switching costs for consumers limits the firm's ability to create a wide economic moat with competitive pressure from both small-scale gyms and other franchised models still limiting PF’s ultimate pricing power.

Nevertheless, I do believe that PF has a great business which the firm has rapidly expanded through the use of a great franchise model which ultimately generates the narrow economic moat for the firm.

Financial Situation

From an operating performance perspective, Planet Fitness is a mostly healthy and profitable enterprise.

PF has 5Y (FY22-FY18) average ROA, ROE and ROIC of 4.72%, 12.44% and 8.02% respectively. These returns are quite positive indeed with the firm tangibly outpacing inflation with their returns on both equity and invested capital.

PF’s WACC is currently around 6.90% which suggests PF outearns their cost of capital required for investment by around 1.2%. While this margin is not massive, Planet Fitness is still generating excess returns from their invested capital and outearning the cost of said capital too.

The firm also has 5Y average (as measured from FY22-FY18) gross, operating and net margins of 50.88%, 25.77% and 9.40% respectively. PF’s gross margin in particular has remained constant for around 10 years illustrating just how profitable the firm’s core franchise business model really is.

The healthy net margin is also a great example of how effective the business is at generating cash flows even when counting the abnormal impacts, the COVID pandemic had on membership numbers. Without the 2020 earnings, PF’s net margin would average around 13% which is very healthy indeed.

{kind=link}

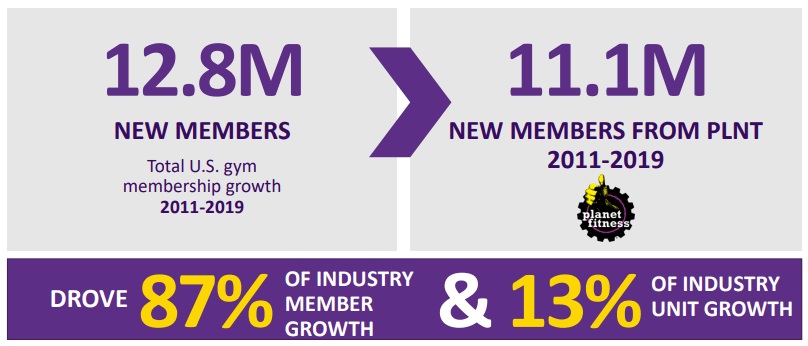

FY 23 has been a mostly profitable year for Planet Fitness with the firm generating significant revenue growth thanks to strong membership figures and an increasing number of new PF clubs. Total revenue for Q3 FY23 was up 13.6% YoY thanks to over 18.5M new members joining the club in the third quarter.

{kind=link}

This massive increase in members accounted for 87% of the total increase in gym memberships in the U.S. which Planet Fitness has attributed to their strategy of going after the 80% of Americans not currently affiliated to any gym.

PF FY23 Q3 Presentation

Planet Fitness saw their franchised store revenues grow 22% YoY while their corporate-owned stores grew revenues by 12%. The massive growth in franchise store revenues was primarily due to significant new location openings and the aforementioned 8% same store increase in net sales.

The sale of equipment to franchisees also increased by 6% YoY thanks to the opening of new locations and the remodeling of existing locations that have reach the 10-year franchise renewal period.

Simultaneously, Planet Fitness increased their same store sales by 8% which illustrates just how well the gym is doing at ensuring existing locations and franchises continue to increase their total membership numbers.

{kind=link}

From a cost control perspective, Planet Fitness is also doing quite well. Total COGS increased just 11% YoY while store operation costs rose just 9%. Compared to the 13.6% increase in total revenue, Planet Fitness has been able to grow their operating margins tangibly.

The firm also managed to keep SGA expenses basically flat YoY which ultimately left the firm with $72.4M in operating income for Q3 FY23, up 17% YoY.

Fundamentally, Planet Fitness has been able to continue growing their business despite consumers universally facing increasingly restricted reserves of disposable income which suggests PF’s product offering is valued highly by their customers.

Q3 FY23 also saw Planet Fitness generate $266.9M in cash from their operating activities up by over 40% YoY thanks to a significant $17M boost in accounts receivables and of course the overall almost $40M boost in net income attributable to Planet Fitness in Q3 FY23.

{kind=link}

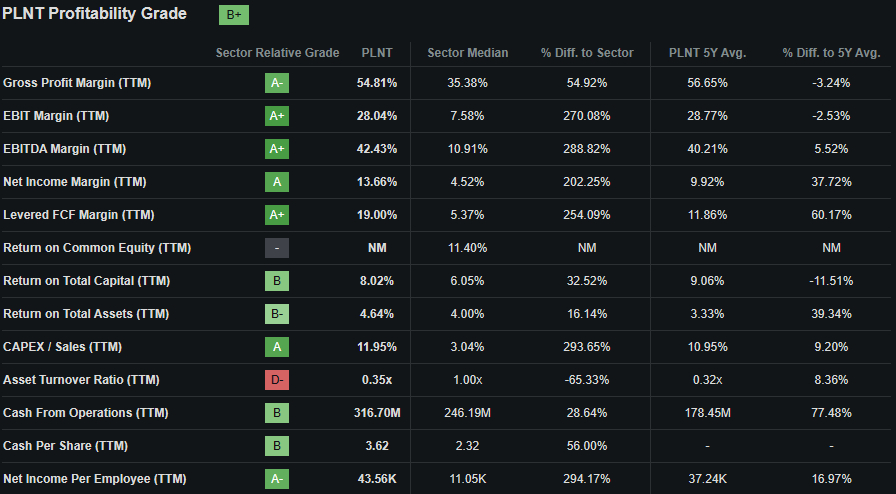

Seeking Alpha’s Quant calculates a “B+” profitability rating for Planet Fitness which I believe to be a mostly accurate relative evaluation of the firm’s current fiscal situation.

The most important point from Seeking Alpha’s Quant profitability figures that stands out is Planet Fitness’ performance relative to the sector median. The outperformance of PF compared to other fitness brands supports the thesis that PF has developed a great market presence and enjoys tangible cost advantages compared to their competitors.

PF’s capital allocation is sub-standard in my opinion with the firm sporting a solid balance sheet characterized by excellent short-term liquidity but being weighted-down by a massive pile of long-term debt.

The firm has $540.1M in total current assets while total current liabilities amount to just $272.8M. This leaves PF with an excellent quick ratio of 1.72x and a wonderful current ratio of 1.98x. Such ample short-term liquidity suggests Planet Fitness will face no immediate liquidity issues in the coming 12 months.

However, total assets for Planet Fitness amount to $2.94B with total liabilities coming in at $3.11B.

{kind=link}

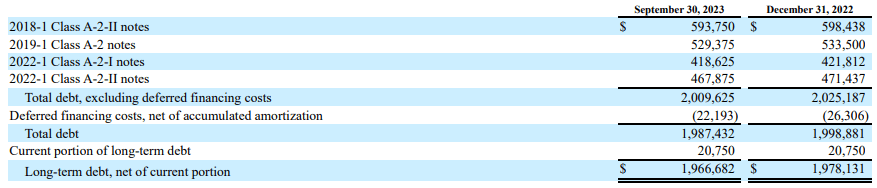

The firm’s total liabilities are buoyed by a pretty massive $1.97B chunk of long-term debt that the company holds. The table above breakdown how PF’s long-term debt is divided with a majority of notes being on fixed interest rates of around 4.008% to 4.666%.

{kind=link}

PF’s long-term debt maturity profile is as follows. While 2024 should be of no issue for the firm, 2025 will already see a pretty sizable $600M in maturities. PF’s unlevered FCF for the TTM is $238.8M which in itself is insufficient to cover these maturing debentures.

I do believe that PF will be able to refinance a portion of these maturing debts to even out their maturity profile. However, it is also quite likely that the firm will take on new LT debt to enable the finance of these maturing notes.

On the one hand, the smart utilization of debt by Planet Fitness has enabled the firm to expand at a rapid rate all the while their current liquidity has remained strong. Nevertheless, the firm must also begin to reign in a portion of this long-term debt in order to ensure the firm does not become reliant on such significant amounts of debt.

The massive debt pile currently facing Planet Fitness was taken aboard in 2018 when PF raised a new $1.225B securitized financing facility to pay off their existing $707.7M senior secured first lien term loan. This move left PF credit negative and increased their debt-EBITDA ratio from 3.8x to 5.8x.

The firm currently has a debt/EBITDA ratio of 5.63x and a debt/FCF ratio of 12.01x which are both quite elevated indeed.

Unfortunately, Planet Fitness does not pay investors a dividend.

Overall, PF is a pretty profitable business with solid gross margins and continued growth characterizing their FY23 so far. However, from a capital allocation perspective the firm must continue reducing their total long-term debt in order to solidify the firm’s footings in an increasingly compromising macroeconomic environment.

Valuation

{kind=link}

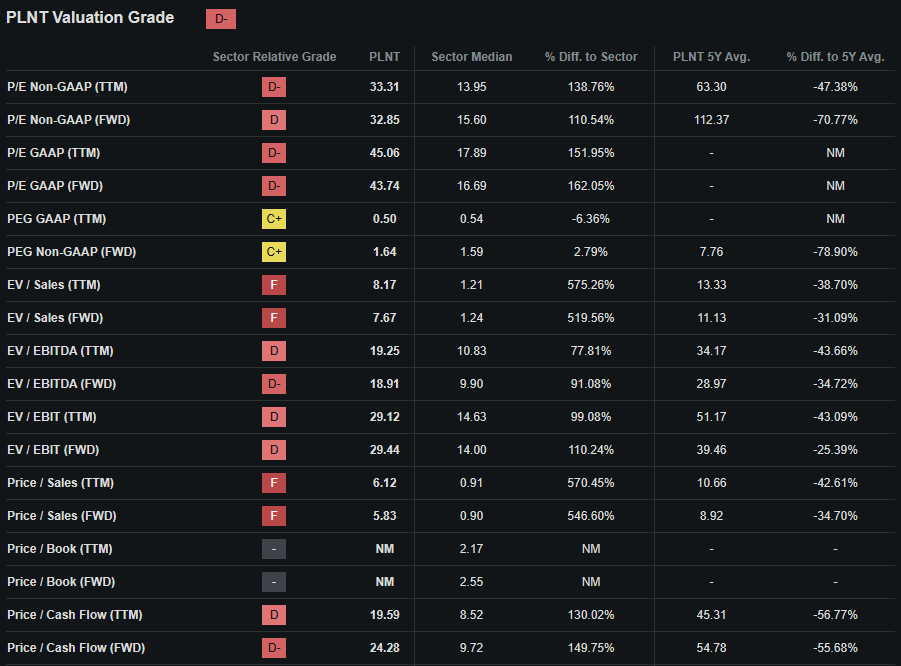

Seeking Alpha’s Quant assigns Planet Fitness with a “ D- ” Valuation grade. I believe this letter grade is excessively pessimistic and suggests a gross overvaluation in Planet Fitness shares.

The firm currently trades at a P/E GAAP TTM ratio of 45.06x which is quite elevated indeed. However, it must be noted that PF is still growing at a rapid rate and therefore warrants this elevated P/E ratio.

PF’s P/CF TTM of 19.59x is reasonable while their TTM EV/EBITDA of 19.25x is also reasonable given the firm’s growth prospects. Both of these metrics are down 56% and 44% respectively relative to PF’s running 5Y average.

The firm’s Price/Sales TTM of 6.12x is quite high but once again down over 43% relative to PF’s running 5Y average.

Considering these basic valuation metrics alone I believe it is difficult to make any meaningful conclusions about the value potentially present in Planet Fitness shares.

{kind=link}

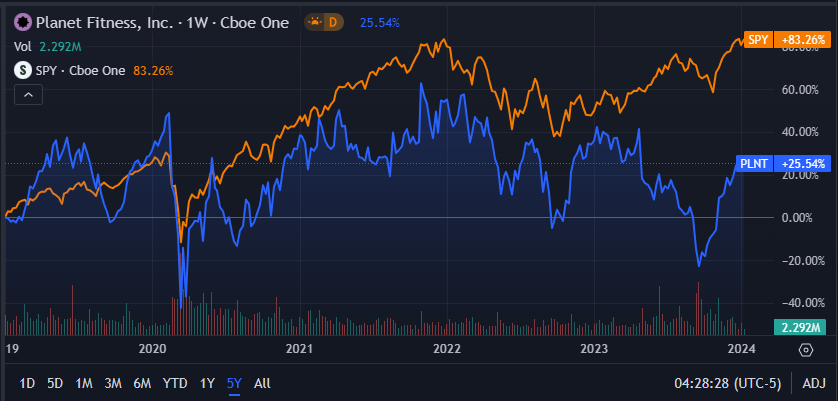

From an absolute perspective, Planet Fitness shares are trading at a slight discount relative to the highs of around $92 seen in February 2022. In September 2023 shares were at a new 52 week low priced at just $43 with a late 2023 rally boosting valuations by almost 70%.

PF shares have also been soundly outperformed by the S&P500 index over the last five years with the popular SPY ETF ( SPY ) outperforming PF by around 50%.

The relative valuation provided by simple metrics and ratios along with the absolute comparison do little in the case of Planet Fitness towards painting an accurate or clear valuation picture. Therefore, a quantitative approach to valuing the stock is essential.

The Value Corner

By utilizing The Value Corner’s specially formulated Intrinsic Valuation Calculation, we can better understand what value exists in the company from a more objective perspective.

Using the firm’s current share price of $73.82, an estimated 2024 EPS of $2.50, a realistic “r” value of 0.14 (14%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 4.74x , I derive a base-case IV of $84.70. This represents a modest 13% undervaluation in shares given current prices.

When using a more pessimistic CAGR value for r of 0.05 (5%) to reflect a scenario where a globally spanning recession causes PF’s revenue growth rate to remain depressed while COGS remain roughly constant, shares are valued at around $42.90 suggesting a massive 70% overvaluation in shares.

Considering the valuation metrics, absolute valuation and intrinsic value calculation, I believe that significant uncertainty surrounds Planet Fitness with their relatively growth reliant future resulting in a massive variance between base and bear cases.

In the short term (3-12 months), I find it difficult to say exactly what may happen to the firm’s valuation. Any acute recession in the U.S. or sudden shock to the economy could see shares tumble as the growth the firm is almost entirely reliant on could be compromised.

In the long-term (2-10 years), I believe Planet Fitness will most likely remain at the forefront of the gym industry if their growth prospect materializes.

However, should a decade long depression occur in the U.S. and global economies, there is a real risk that Planet Fitness will struggle to generate enough FCF to finance their business with a potentially significant drop in valuations accompanying this outcome.

Risks Facing Planet Fitness

Planet Fitness faces some real threats arising primarily from their exposure to a cyclical business environment and from what I believe is a compromised asset allocation strategy.

A recessionary macroeconomic environment could result in limited growth opportunities for Planet Fitness as the firm would have to grapple with an increasingly income strained consumer and faltering demand for new enterprise.

Such a scenario could result in a slowdown in new location openings which ultimately would leave revenue growth flatlined at best or declining at worst.

While PF is already a budget-oriented gym offering, the absolute necessity of a gym membership is debatable. I suspect many of the so called “beginners” PF targets with their gyms may be quick to sacrifice a monthly payment of $10 or $28 dollars in order to save cash during a recessionary environment.

Furthermore, I believe PF’s massive long-term debt pile could cause a real headache for the firm in the coming years. The securitized finance facility adopted by the firm in 2018 has left PF with a poorly managed debt maturity profile which could place massive strain on profitability in the coming four years.

It appears that PF will almost certainly be forced to take on more debt in order to finance the current maturities as their FCF will simply be unable to cover the massive obligations coming in the next few years.

In a recessionary environment, PF may be able to obtain some cheap debt which they can use to finance these maturities. However, should interest rates remain elevated as the economy fails to cool as predicted, PF could be faced with a high interest debt which would be problematic for the firm.

From an ESG perspective, Planet Fitness faces little tangible threats. The firm has made it clear in their ESG report that the company as a whole is committed towards ensuring diversity, inclusivity and responsibility underpin the firm’s governing ethos.

PF has 50% gender and racial diversity in their Board of Directors and has achieved a 13% reduction in GHG emissions and an 18% decrease in normalized corporate club water usage in FY22.

The overall lack of any major environmental, societal or governance concerns suggest to me that Planet Fitness may be a good choice for the more ESG conscious investor.

Of course, opinions may vary with regards to ESG material and I implore you to conduct your own ESG and sustainability research before investing in PF if these matters are of concern to you.

Summary

Planet Fitness appears to be a profitable and successful enterprise with significant future growth prospects on the horizon. The firm continues to generate good amounts of FCF relative to their total revenues with a solid gross margin and great short-term liquidity supporting their immediate business objectives.

However, the firm has a significant amount of long-term debt with maturities that will place some pressure on their profitability in the coming years. While Planet Fitness may pay these maturities by taking on new debt, the firm must in my opinion aim to reduce their leverage ratios in order to stabilize their long-term prospects.

Since the rally that began in September 2023, share prices have risen by almost 70% in just a couple of months. Given the current stock price of around $73.82, this leaves shares at a fair valuation relative to FY24 cash flows. I believe there is insufficient margin of safety present to advocate the building of a position from a deep-value perspective.

Considering everything I have discussed, I currently rate Planet Fitness a Hold. A return of share prices to around $43 would create enough margin of safety to enable a rational investment case to be made, even despite the significant debt overhang present at the firm.

However, at present time I do not believe Planet Fitness makes for an attractive investment opportunity.

For further details see:

Planet Fitness: A Fit Stock With Fat Debt