MYPS - PlayStudios: Strategic Pivot To Drive Growth

2023-10-18 19:06:14 ET

Summary

- PlayStudios has faced challenges post-IPO but has made strategic shifts towards new growth drivers in its advertising segment.

- The company's core virtual currency segment remains stable, with a focus on higher player spends.

- There is potential for EBITDA margin expansion through cost-saving initiatives and growth in margin accretive portfolio businesses.

Investment Thesis

PlayStudios ( MYPS ) had a rocky debut post the meltdown of SPAC related IPOs and faced severe jolts going forward with tightening platform policy standards along with decline in player spends as a result of tough macro backdrop. However, the company has made significant improvements pivoting strategically towards new growth drivers within its advertising segment while its core virtual currency segment remains stable. We initiate with a Buy rating and ascribe a target price of $3.3 at 5x EV/ Fwd EBITDA driven by 1) stability in its core virtual segment with focus on higher player spends (up 8% in Q2 2023) 2) continued outperformance within its advertising revenue 3) EBITDA margin expansion potential through cost saving initiatives and 4) growth within its margin accretive portfolio businesses.

Company Background

PlayStudios is engaged in operations of social casino and casino games with real life reward programs called playAWARDS. Key games include myVEGAS Slots, myVEGAS Blackjack, Solitaire, Tetris, Sudoku and Mahjong. It boasts a total of 100 million downloads and has about 8 million monthly active users. Revenue is derived primarily from in-app purchases of the virtual currency specifically in its social casino games as well as in-app advertising with bulk of revenue generated revenue primarily from virtual currency (over 90%). The company has dual class of shares with Class A shares holding 1 vote per 1 share while Class B shares holding 20 votes per 1 share which provides the Founder, Andrew Pascal, about 70% of total voting power.

Historical Track Record

MYPS was heavily dependent on its social casino game Pop! Slots which drove the majority of revenue historically. Its social casino portfolio has been on decline as it faces multiple challenges in acquiring customers due to stringent privacy rules making targeting less effective and rising customer acquisition costs due to competitive intensity. While Pop! Slots still contributes bulk of the virtual currency revenue, the company has successfully pivoted to driving its advertising revenues through strategic acquisitions. It acquired Brainium and exclusive rights to Tetris in late 2021 which has been the major growth driver for the company since. In addition, given the advertising games are not required to pay any platform fees, it generally has higher EBITDA margin and both the strategic shifts have been margin accretive as witnessed in the robust margin expansion during 2023.

| Particulars |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| TTM 2023 |

| Virtual Currency |

| 239 |

| 268 |

| 280 |

| 261 |

| 257 |

| Advertising |

| - |

| 2 |

| 7 |

| 22 |

| 42 |

| Other |

| - |

| - |

| - |

| 7 |

| 10 |

| Total Revenues |

| 239 |

| 270 |

| 287 |

| 290 |

| 309 |

| EBITDA |

| 50 |

| 58 |

| 40 |

| 38 |

| 56 |

| EBITDA Margin |

| 20.9% |

| 21.5% |

| 13.8% |

| 13.2% |

| 18.2% |

Strategic Shifts to Drive Growth

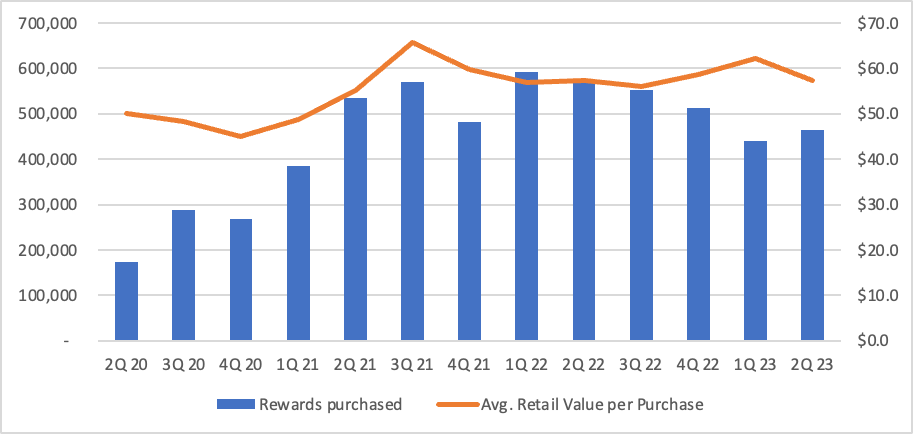

MYPS had been facing the post pandemic reset with a change in player behavior, rising inflation and adverse impact to the user acquisition which led to a decline in revenue for its social casino segment. Management had shifted its focused on maintaining its user base and driving higher payer conversion and spends. Its virtual currency revenue which generates company's core social casino portfolio declined about 7% in 2022 while the performance improved throughout the year. In addition, within H1 2023, virtual currency was down 2.5% YoY implying a sequential acceleration as a result of continued focus on players with higher spends.

{kind=link}

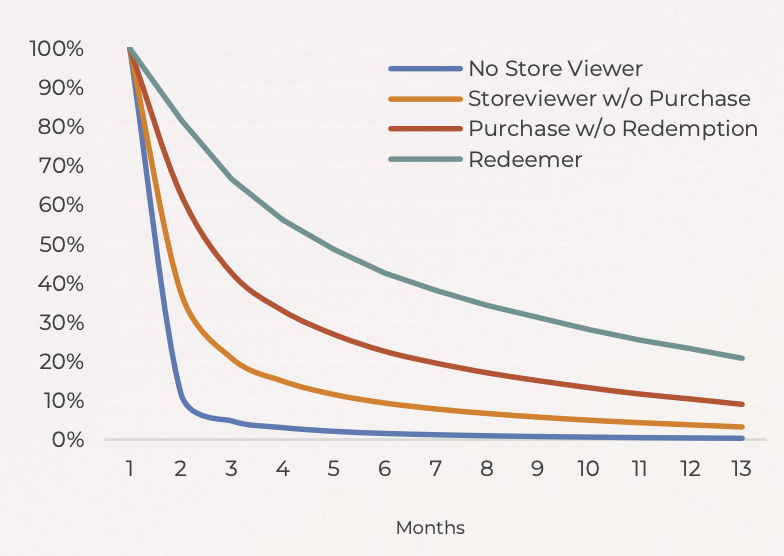

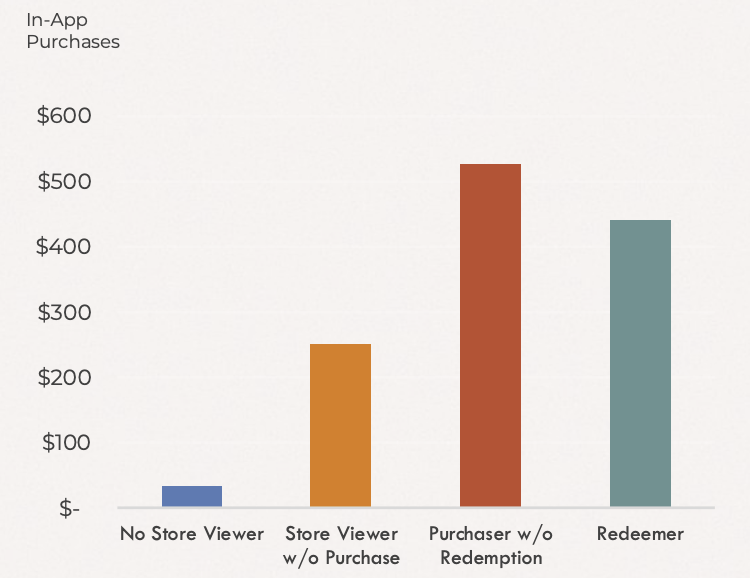

In addition, it initiated a restructuring in Q1'23 focused on cost saving initiatives resulting in consolidation of several studios, reduction of 10% of its total headcount and shifting the development to less expensive locations closer to talent pool. It expects to realise the cost savings starting Q3 and with bulk of savings in Q4. The company has also diversified through strategic M&A within casual games and has started applying playAwards program to games like Tetris and Solitaire which will aid incremental revenue growth. playAwards has been a driver of customer retention with retention rate of 40%+ by month 6 as well as improving player monetization which provides players with real life rewards such as free hotel nights, cruise vacations, restaurant vouchers and other travel and shopping rewards. An average player who is a redeemer of real-life awards on the playAwards store have significantly higher retention than someone who has not yet viewed the playAwards store benefits or who has not purchased virtual currency coins but viewed the store. Similarly, someone who has purchased the virtual currency coins and have redeemed or is yet to redeem the rewards has better monetization compared to others.

playAwards Engagement leading to Higher Retention

{kind=link}

playAwards Engagement leading to improving Monetization

{kind=link}

Its acquisition of Brainium with a significantly higher EBITDA margin is also expected to realise synergies during the year and boost margins.

EBITDA Margin Expansion Potential

PlayStudios is guiding 2023 EBITDA margin of 18.2% at midpoint, up about 500 bps YoY, from 13.2% in 2022. In H1 2023, the company reported an Adjusted EBITDA margin of 21.6% which implies a sequential deceleration. The strong growth was driven by increasing contribution of advertising games which does not pay fees to mobile platforms. In addition, normalized marketing spends which declined 10% in H1 led to deleverage of ~600 bps as revenue growth outpaced marketing spends. In addition, workforce rationalization and cost saving initiatives is also likely to bear fruit in the coming quarters and through 2024. It recently closed its legacy studios in Austin and Hong Kong and moved its gaming development in Tel Aviv, Israel, with support from Vietnam and South Eastern Europe. Savings related to headcount reduction is likely to drive some upside in H2 2023 with bulk of the margin expansion likely to aid in 2024.

Growth within Brainium Portfolio

Brainium portfolio has been a phenomenal acquisition for the company and has witnessed continued outperformance since the closing. Its expansion of playAwards to the Brainium portfolio would lead to significant improvement in the player spends as well as increase retention would lead to higher growth in a margin accretive (40% EBITDA margin compared to <20% margin for the portfolio) portfolio business of Brainium. This has also been demonstrated within its Tetris portfolio which has seen improved retention post the introduction of the playAwards program.

Valuation

We compare MYPS with other mobile gaming peers and while there are several peers within the console gaming and platform space, we have limited set of peers within the mobile gaming sector strictly. Accordingly, we compare MYPS with Playtika Holding ( PLTK ) and Sciplay Corp ( SCPL ) which have similar focus within mobile gaming. MYPS trades at 4.3x EV/ Fwd EBITDA at a discount to Playtika while at a slight premium to Sciplay Corp.

The discount is driven by relative outperformance of its PLTK in terms of margin performance as well as strong cash generating ability.

{kind=link}

MYPS performance has been gradually improving and trending upwards and has further upside potential for expansion entering into 2023. We believe the company has made several strides in the right direction with continued outperformance within its advertising space and relative stability on its core casino portfolio. We initiate at Buy as we believe current value provides a favorable risk reward driven by its continued ability to drive growth via advertising space and realize better cash conversion ratios. We ascribe a target price of $3.2 at 5x EV/ Fwd EBITDA, a 20% discount to Playtika accounting for the better margin profile, while also ascribing value to MYPS' recovery and growth profile. In addition, the company's flexible balance sheet with ~$210 mn in liquidity and no borrowings enables them to pursue acquisitions, investments in new products and also continued share repurchases with $30 mn remaining under authorization.

Risks to Rating

Risks to rating include

1) Changes in platform privacy rules which makes it harder for publishers to target users and lead to lower revenues and app installs as platforms such as Apple continue to tighten privacy standards

2) Significant deterioration in its virtual currency segment as a result of declining player spends and conversion ratios given the current tough macroeconomic backdrop

3) Cost savings initiatives could be lower than anticipated and may not aid its EBITDA margin expansion

4) FCF conversion can continue to remain muted as the company continues to invest in its products

5) Ad gaming revenue could be hampered as a result of plateauing of its user growth and loyalty members

Final Thoughts

PlayStudios has done remarkably well in recent quarters transitioning from social casino to casual gaming which has led to revenue growth and EBITDA margin expansion despite decline in its core social casino segment. It has embarked upon strategic steps to reduce costs and drive growth within its ad revenue as well as improve its conversion focused on users with higher spends. We believe the current valuation multiple provides favorable risk reward driven by sustainable potential for revenue growth and margin expansion. Initiate at Buy.

For further details see:

PlayStudios: Strategic Pivot To Drive Growth