PLXS - Plexus: Earnings Power Well-Reflected In Current Market Values Rate Hold

2023-09-07 03:53:33 ET

Summary

- Plexus presents with a series of manufacturing wins from its Q3 FY'23.

- But it has done this on flat revenues, tight cash flows, and investors have potentially overpriced its growth potential.

- These may be key risks to the company selling at higher multiples going forward.

- Net-net, I rate PLXS stock a hold.

Investment briefing

Electronic manufacturing players are looking increasingly attractive, on a combination of 1) low earnings/cash flow multiples and 2) superb economic leverage on capital employed. We have been extending our reach beyond complex disease segments in diversified healthcare to this space and found plenty of long-term compounders are very attractive prices.

Plexus ( PLXS ) is one that came on our radar as a function of this thematic. I had looked to the company around April/May as it bounced off its previous lows to catch a strong bid. However, closer inspection reveals a set of economic characteristics that don't quite match up. Here I'll run through all of the moving parts I've uncovered in the name, explaining why I think it is a hold for now. Net-net, I rate PLXS a hold.

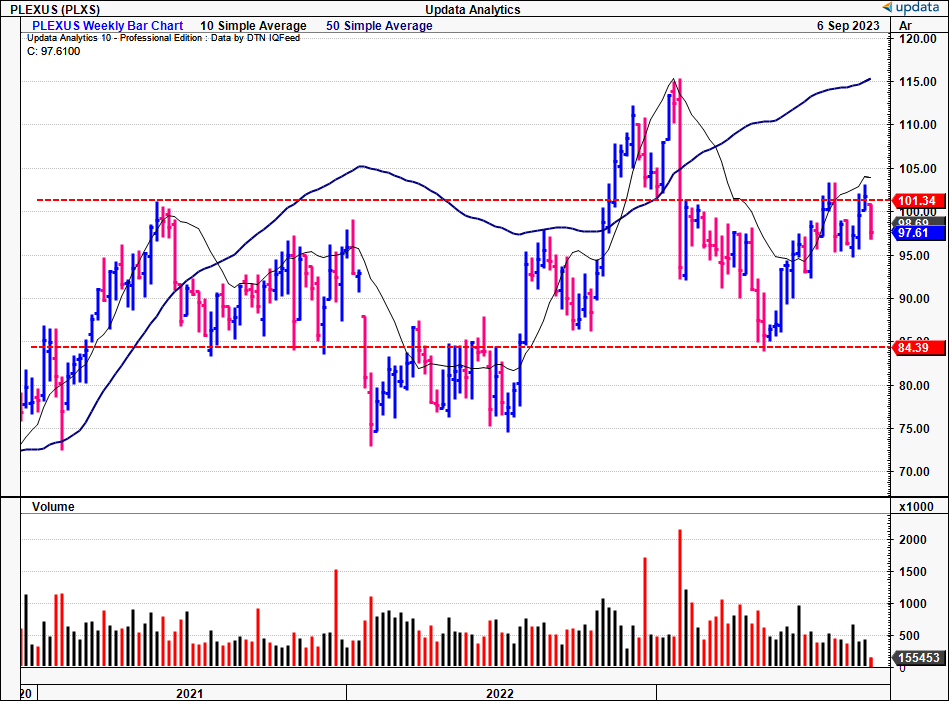

Figure 1. PLXS weekly evolution, trading in congestion within range shown

- Sharp rally off previous lows from May—July

- Double-top leading into September with corresponding reversal

- Trading within short-term congestion

{kind=link}

Critical facts to investment debate

Q3 FY'23 insights—flat revenues, tight cash flows

1. P&L breakdown

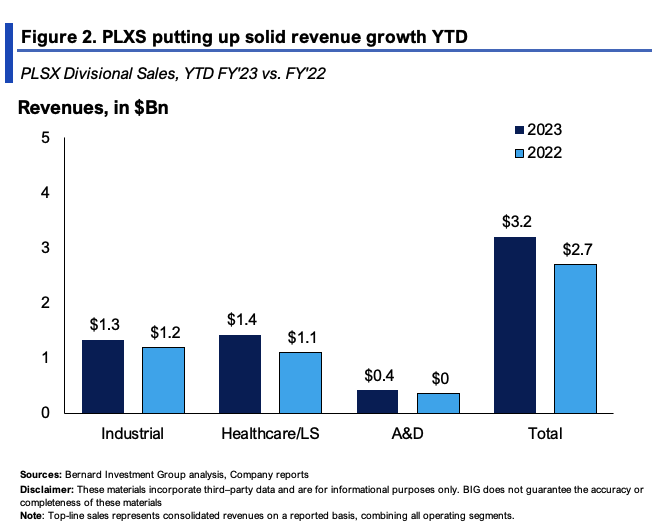

PLXS put up Q3 revenues of $1.02Bn , up 3% YoY and in line with management's guidance. It pulled this to operating income of ~$30mm and a 280ps margin , on earnings of $0.56/share [as a reminder, PLXS reported its Q3 FY'23 numbers, aligning with Q2 CY'23. For consistency and simplicity, I'll be talking in terms of Q3 from here] . PLXS faced headwinds from various market dynamics during the Q3. But these were expected, and align with the broader industry trends of 1) inventory destocking from FY'22 overstock (due to the supply chain headwinds), 2) inventory corrections in its semis markets, and 3) a broad slowdown in aggregate growth in these end markets. The company's divisional breakdown is observed in Figure 2.

{kind=link}

Rolling into its Q4, management is eyeing revenues ranging from $1Bn to $1.04Bn, on operating margins between 4.7%—5.2%. It eyes EPS of $1.18—$1.36. This would bring it to $4.18Bn at the top in FY'23, calling for 9.8% YoY growth in sales. I'd also point out PLXS' ambitions to hit $5Bn in revenues by FY'25. To get there, it needs to grow sales by ~20% over the coming 2 years. On the $5Bn, is operating margins of 5.5%. Hence, 20% growth in sales for relatively flat margin expansion. I'm not sure what the value creation on this would be, as I'd prefer to see more falling below the top line in PLXS' investment case. Without it, this is a potential flag for me. In fact, I was surprised to see PLXS pull in just $18.8m in OCF on these revenues—and this isn't out of range these past 2 years. More on this as it relates to cash flows a little later.

Additional takeouts for the quarter include:

- Working capital management was something I took note of. PLXS mentioned it reduced gross inventory dollars by an unspecified amount, but this was on a 5% increase in inventory days (thanks to the tighter revenue clip). Customer deposit days increased by 7 days YoY, and tallied >$580mm in customer deposits. This amount covered over 35% of gross inventory at quarter-end per management.

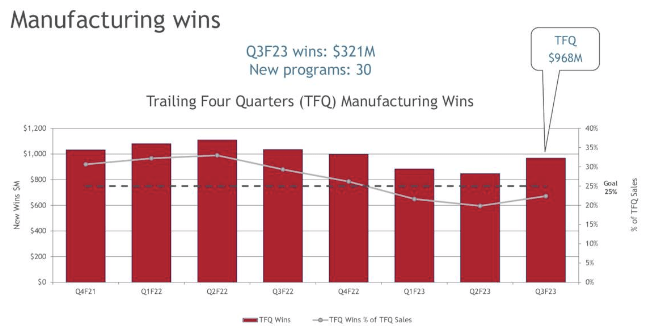

- Perhaps the most compelling takeout was that it brought 30 new manufacturing programs online during the quarter. Critically, these wins are set to generate $321mm in annualized revenue once fully operational. As to the breakdown on this:

- The industrial segment was the headline here, with 18 new program wins, worth ~$193mm.

- Meanwhile, its healthcare and life sciences business brought 7 new programs valued at c.$90mm.

- Its aerospace and defense ("A&D") segment team secured the other 5 wins with a gross value of $38mm.

- Geographically, the Americas performed well, winning ~$200mm in new programs, with its Guadalajara footprint capturing the bulk ($160mm) of these wins. APAC booked $58mm in manufacturing wins—primarily from the industrial sector—while EMEA came in with $64mm in manufacturing wins. For the TTM, PLXS' EMEA operations have clipped >$300mm in manufacturing wins. The entire scope of its manufacturing wins is observed in Figure 3.

- Finally, the funnel of qualified manufacturing opportunities exceeds $4Bn in PLXS' book. The key word here— qualified opportunities. The company also has an early-state funnel that it doesn't share publicly. Management said this was "at a record level right now" on the call.

Figure 3.

{kind=link}

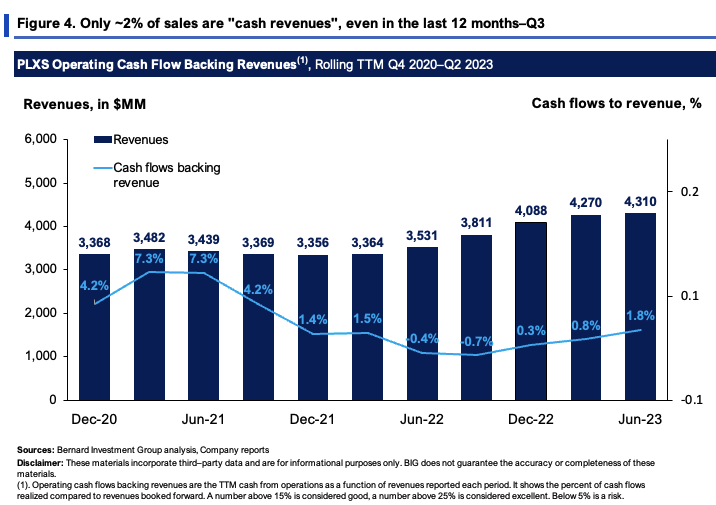

2. Cash flows realized to revenues booked a potential flag

Circling back to the talk on operating margins and cash flows from earlier. The company brought in just $18.8mm in OCF on the $1Bn in revenues booked forward—in line with historical averages. To me, this is troubling.

Figure 4 depicts the company's OCFs as a percentage of revenue on a rolling TTM basis since 2020. All sources of operating cash are included, as are the company's entire revenues.

What shows is PLXS hasn't booked more than 7.5% of revenues as cash flows over this period. In fact, just 1.8% of TTM sales were "cash revenues", a red flag for me. I'd be looking to >15% at the minimum to suggest the company can internally finance any growth operations going forward. At just ~2%, it would appear PLXS may have to turn to the capital markets to finance its growth. Not surprisingly, therefore, it issued another $219mm in debt last quarter, $807mm in the last 12 months to Q3.

{kind=link}

Valuation

The stock sells at 17.6x forward earnings and 13.7x forward EBIT at the time of writing. These are both 25% discounts to the sector, respectively. Although, to pay $13 for every future $1 in pre-tax income, on operating margins of just 5.5%, is that an attractive proposition?

There are two points relevant to the discussion here.

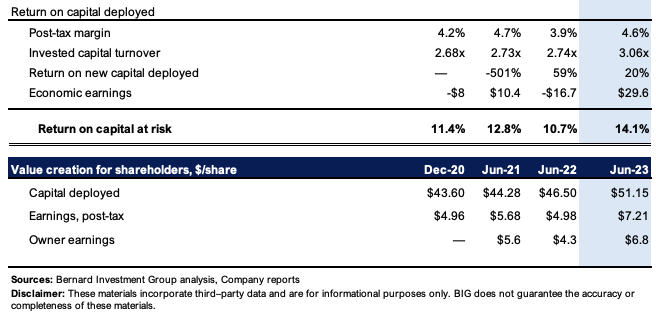

One, most of the cash PLXS puts to work as business capital is tied up in inventories. Of the $2.8n in its current asset account, more than $1.6Bn—57% to be exact—is booked as inventories. Hence, after adjusting net working capital, it has more in inventories than net capital deployed and at risk in the business. Point it, it must turn over this capital (mainly inventories) at high rates to bring in any sort of meaningful income.

As shown in Figure 5, it has done this over the last few years. Its post-tax margins are very thin (single-digits), but its capital turns are ~2.7–3x on average since 2020. That is, every $1 in capital brings in ~$2.7-$3.00 in sales revenue. This is a positive point, and returned 14% on the firm's 'investments' last quarter (TTM values).

Figure 5.

{kind=link}

Second is to understand how much of its growth potential is already priced in, based on these economics. PLXS did 14% trailing ROIC last period. It sells at an EV of $2.97Bn. Looking at ROIC and EV as a function of 1) the cost of capital, and 2) total invested capital is helpful.

Both ratios are shown in Figure 6, with the hurdle rate is 12%, the required rate of return for all our equity holdings. Both ratios show returns produced on the firm's capital—business returns, and market returns created by the investments. Market values are a discounted set of expectations, so comparing the 2 is insightful as to what's priced in and not.

Based on the calculus, it would appear that investors have well and truly priced in the company's earnings power at a $2.97Bn EV. You'd be looking for a number below 100% to imply it hasn't. Alas, paying $13 for each $1 in future EBIT, does not appear worth it in my opinion, not at these starting valuations.

BIG Insights

Takeaways

PLXS was one that came on our radar given the compressed market multiples and that it sells at a c.25% discount to peers. However, on closer inspection, even at these market values, PLXS' growth may be well priced in, in my opinion. The firm booked a number of manufacturing wins this YTD, but future aspirations call for it to hit just 5.5% operating margins by FY'25 on $5Bn in sales. It is also clipping just 2% in OCF on its revenues booked forward. Even though it turns over capital at 3x of sales, the broader set of economics aren't necessarily attractive in my opinion. There may be more selective opportunities elsewhere, that have 1) a longer reinvestment runway to grow the business, and 2) much higher pre-tax earnings growth to produce than PLXS. In that vein, I rate PLXS a hold.

For further details see:

Plexus: Earnings Power Well-Reflected In Current Market Values, Rate Hold