PML - PML: We Still Need To Be Careful With Leverage

Summary

- PML is a fund I own and recommended to start off the year. After some modest gains, I believe a more cautious tone is warranted.

- Munis saw an unusually strong January after an awful 2022. I expect the months ahead to be full of ups and downs.

- Funds like PML look attractive on the surface due to their relatively high yields. But this comes from the use of leverage, which remains a headwind as short-term rates rise.

- The premium to NAV is nearing 5%, which suggests being selective with buy-in points is appropriate.

Main Thesis & Background

The purpose of this article is to evaluate the PIMCO Municipal Income Fund II (PML) as an investment option at its current market price. This fund's objective is to invest at least 90% of its net assets in municipal bonds whose interest is exempt from regular federal income taxes and the fund invests at least 80% of its net assets in bonds that at the time of investment are investment grade quality - bonds that are unrated but of similar quality.

When 2023 got underway I was a muni bull and opted to recommend PML (and buy it) for a number of reasons. Over the last month and a half this thesis played out as I hoped with the fund seeing some gains:

Fund Performance (Seeking Alpha)

While this is not a large gain by any means, it was well deserved after seeing the broader muni sector dropped consistently last year. While PML could have plenty of room to run, I think a more cautious outlook is warranted. I would look at these gains not as a momentum play but as a reason to be more selective with any new positions. I see some headwinds on the horizon that tell me a rating downgrade to "hold" makes sense - and I will explain them below.

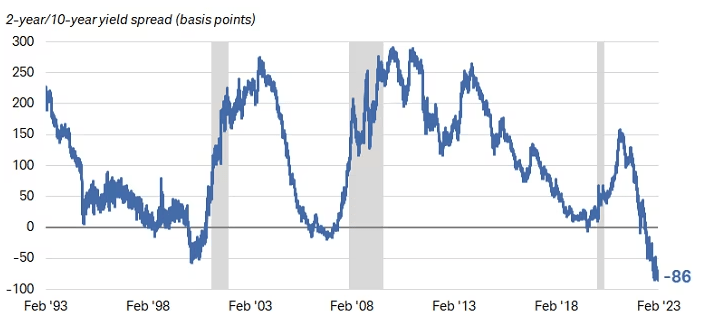

Yield Curve and Leverage - Risk Remains

The first point I need to make when explaining the merit for caution has to do with leverage. Specifically, the cost of having so much of it. PML, and other PIMCO CEFs, use leverage extensively. This can work well in good times and amplify the yield and return. But it can also work to its detriment at times, as 2022 showed us quite clearly. While the new year has started off better, I want to emphasize to stay within a comfortable threshold with respect to this fund and others that use leverage. As the yield curve has inverted even more sharply in recent weeks, this makes the cost of leverage more expensive in relative terms compared to what the fund can earn in the yield "pick-up" on the longer end of the curve:

{kind=link}

2-10 Year Yield Curve (Charles Schwab)

What this means is, the fund's borrowing costs are rising more swiftly than the yield it earns from the securities it is using that leverage to buy.

Now, this is not new, but I am repeating it here because it is easy to overlook this risk now that the market has rebounded and stabilized. This is a good sign overall, but the yield curve inversion is so wide that I am very concerned for what the future is going to hold. With PML's extensive use of leverage, it is difficult to stay too bullish on this option:

{kind=link}

Fund's Leverage (PIMCO)

The a bottom-line here is this is a new year but an old risk is present. So manage your risk accordingly.

Valuation No Longer As Enticing

A second key reason for my downgrade relates to the fund's valuation. This is true both in isolation and in relation to its sister funds, which are the PIMCO Municipal Income Fund ( PMF ) and the PIMCO Municipal Income Fund III ( PMX ). Back in early January, PML was trading just over par value and had a discount compared to the other national muni funds from PIMCO. Today, that story has shifted a bit. PML's premium is not outrageous, but it is getting pricey. Further, it is no longer the cheapest but sits in the middle of the pack:

| Fund |

| January's Premium to NAV |

| Current Premium to NAV |

| PML |

| 0.1% |

| 4.2% |

| PMX |

| 1.5% |

| 0.7% |

| PMF |

| 5.6% |

| 7.5% |

Source: PIMCO

This is not meant to be alarmist but rather to indicate the buy signal I saw in January related to the fund's premium has evaporated to some degree. Will this mean the fund is going to drop like a rock? Of course not. But it does mean to be on the hunt for down days or a stretch where the NAV holds up and the share price declines. This will open up a better value opportunity since currently the story here is mixed.

Income Metrics Don't Inspire Confidence

Another reason for caution relates to the fund's distribution. This is always important but especially true since PML recently saw a distribution cut (along with other PIMCO muni CEFs). The good news is that even post-cut the fund still sports an attractive income stream, especially on a tax-adjusted basis:

PML's Distribution (Seeking Alpha)

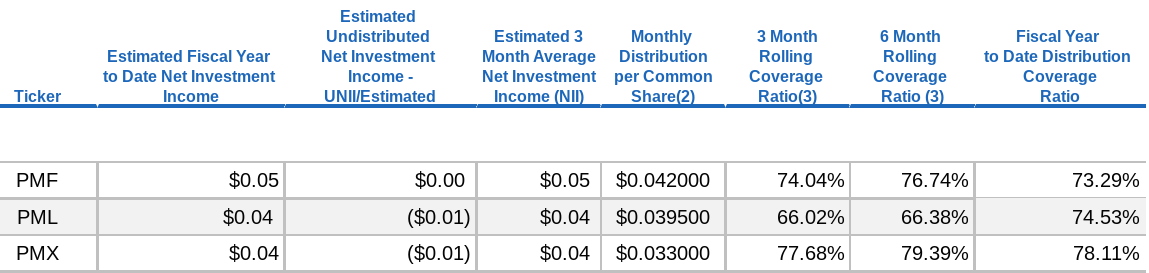

The bad news is we won't know for sure if PIMCO can maintain this level of payout going forward. I already mentioned the leverage headwind and that is a very critical element to maintaining this 5% yield. There are signs we may not be completely out of the woods either, since PIMCO's February UNII report shows all three national muni CEFs are under-earning what they require to keep their distributions steady:

{kind=link}

Income Metrics (PIMCO)

We don't typically see cuts from PIMCO in rapid succession, so this is not an immediate risk in my view. But it does mean if there is another income cut later this year that investors should not be too surprised as they have time to prepare. Income coverage was weak due to higher rates/leverage and that backdrop continues to this day. Whether investors can withstand the volatility that comes from this reality is up for them to decide.

January's Momentum Could Continue

I have displayed a fairly negative tone in this review and I don't want to completely bash this fund. The reasons here are multi-fold. One, I own it and see merit to owning it. The 5% income stream yields me quite a bit after taxes and if the Fed pumps the brakes a bit later this year fixed-income will rally broadly. So I absolutely want to take advantage of that potential by having some muni bond exposure.

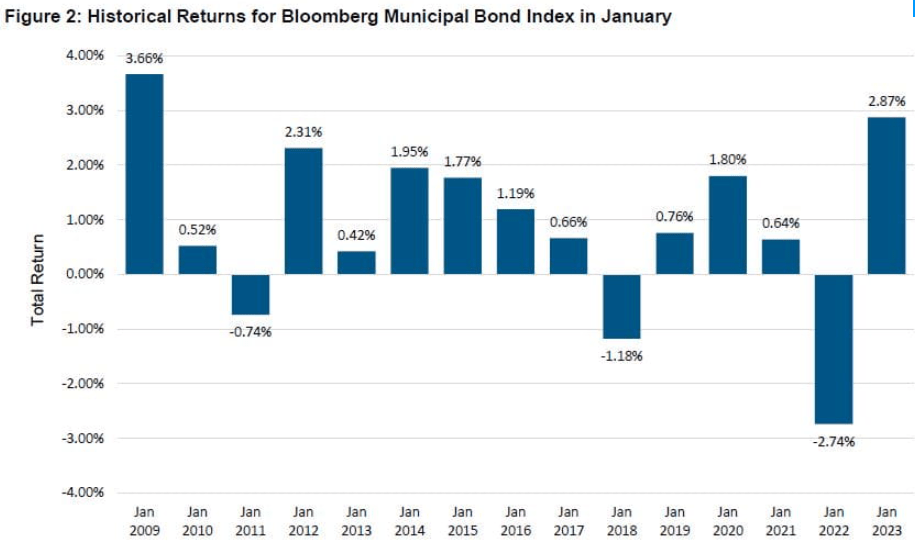

Further, after a horrible 2022, munis saw one of their best Januarys in over a decade. This could signal weakness ahead or it could be the start of a multi-month bull run for the sector:

{kind=link}

January Returns (Muni Sector) (PIMCO)

Where the sector will go from here is anyone's guess. Short-term momentum can signal more gains or a likely breather ahead. What will March and Q2 hold for munis, and PML by extension? I wish I knew for sure. When the outlook is mixed err on the side of caution. That supports my hold rating.

PML Is Well-Diversified

A reason I like and hold PML is because the fund is well rounded. Not only is it a national muni fund (and therefore not beholden to only one individual state), it is also not over-weight any one particular sector. In fact, its largest underlying sector (Hospital-backed revenue bonds) only makes up 16% of the fund. Each other sector has an allocation less than this within the fund:

PML's Sector Exposure (PIMCO)

When we are in a difficult environment like this one, staying diversified is key to my strategy. Still, PML is going to be impacted by the hospital/health care sector, so a look at this area individually is worthwhile for prospective buyers of this fund.

I will start with a discussion on what these bonds even are. The point of distinction here is these are revenue bonds. These differ from General Obligation ((GO)) bonds in that they are not backed by state or local government taxing authority. Rather, they are tied to specific revenue streams. In this case, these are bonds typically issued to finance the construction or expansion of hospitals (i.e. a new building, new wing, etc.). The revenue is then generated from providing health care services - typically coming in the form of reimbursements from insurance companies, the governments, or, in some instances, from patients directly.

There are some opportunities here. I generally view this sector as quite stable. But the Covid-19 pandemic changed that a bit and made the sector look riskier. It is that mindset that offers the opportunity in my opinion. The thought here is that the number of insured Americans has continued to grow and an aging population means more of the citizenry is covered by Medicare and Medicaid. Whether or not this is "good" depends on your perspective, but it is almost certainly good for owners of muni debt backed by hospital revenues. The logic being I trust insurance companies and the government to pay off their policyholder's hospital bills because having a functioning hospital system is central to every community.

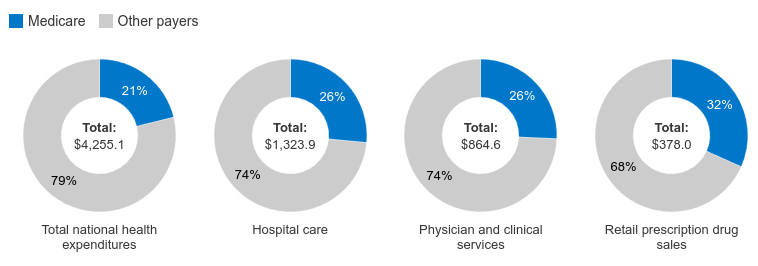

I bring up the Medicare aspect because this is central to hospital revenue. This has been true for years and is only going to be more concentrated in the years to come. As Americans trend older, hospitals will be more reliant on Medicare for reimbursement - but they are already quite reliant on it today:

{kind=link}

Reliance on Medicare (KAISER Foundation)

The conclusion I draw here is that the recent public projections by both Republicans and Democrats in Congress that there will not be cuts to social security or Medicare mean that revenues are going to keep flowing in to hospital systems around the country. This gives me confidence that holding a muni fund with exposure to this sector is not overly concerning.

In addition, I view the fact that the majority of the country is currently insured as a comforting sign. With inflation and corporate layoffs dominating the news, it is starting to look like the consumer environment is going to be challenging. But hospital bills are less at risk of this backdrop since insurance companies (or the government) are responsible for a good chunk of what is billed. With over 90% of the country relying on more than just savings to pay their medical bills, the risk is mitigated:

Insurance Stats (United States) (Congressional Research Service)

What I am getting at is I am good with owning GO muni bonds and revenue bonds from the right sectors. I would note that I would avoid health care related bonds if they are tied to private nursing homes and assisted living facilities. Those have not recovered from the pandemic yet. But traditional hospitals are not in the same boat and PML should see gains from them.

Bottom-line

PML CEF has been a winner of late and that could continue. The muni sector has been ripe for a rebound and the fund's holdings are spread out evenly across a number of areas. However, I do have some concerns. The premium has expanded, the income metrics are weak, and leverage is not always a friend. These competing factors tell me a move to "hold" is the proper decision. Therefore, I suggest readers approach new positions selectively at this time.

For further details see:

PML: We Still Need To Be Careful With Leverage