EMRAF - PNM Resources: No Merger No Thank You

2024-01-12 09:55:38 ET

Summary

- Avangrid's proposed acquisition of PNM Resources falls through after New Mexico utility regulators do not approve the merger.

- PNM Resources returns to being an independent electric utility, with its stock rated as a sell.

- PNM Resources operates in New Mexico and Texas, with a focus on renewable energy sources, but with a poor regulatory environment.

My, my, how fickle Mother Merger can be. On Oct 20, 2020, electric utilities PNM Resources ( PNM ) and Avangrid ( AGR ) announced the proposed acquisition of PNM by AGR. Avangrid is a subsidiary of Spanish mega-utility Iberdrola, S.A. ( IBDRY ). The acquisition terms were $50.30 in cash for each PNM share, or $4.3 billion, plus assumption of $4.0 billion in debt, for a total value of the acquisition of $8.3 billion. All that was needed with an approval by New Mexico utility regulators, but an approval was not on the cards. Regulators did not approve the merger and PNM took the PUC to court. After 39 months of waiting for a positive resolution, on Jan 2, 2024 , AGR threw in the towel and walked away from their offer. PNM Resources returns to being ongoing, independent electric utility, and the stock is rated as a sell.

In the months leading up to the Oct 2020 offer, PNM Resources traded mostly between $37 and $45, jumping up to $50 with the announcement. In 2019 and up to the Covid Crash of 2020, PNM traded as high as $54. In May 2023 shares started to break below $49 as investors were getting impatient, and the tea leaves were not looking favorable for the merger to be consummated. Share prices continue the downward trend and currently trade at $39.50. There are better utility investment alternatives to PNM.

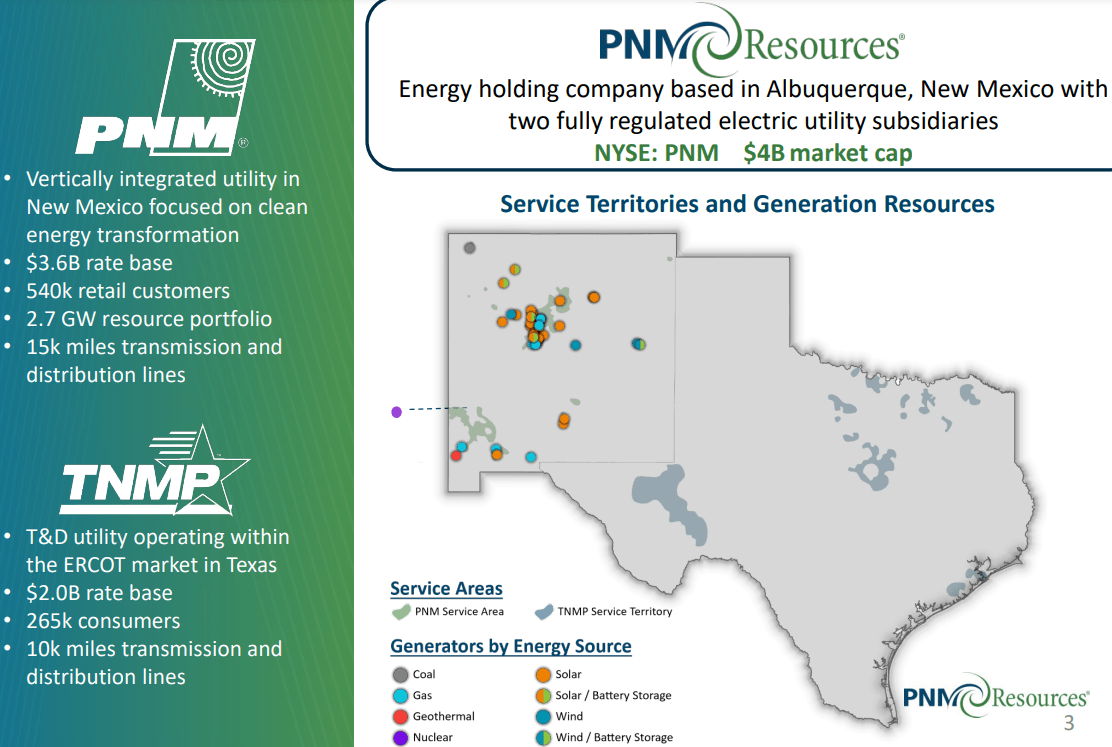

PNM Resources provides electricity through two regulated subsidiaries: Public Service of New Mexico ((PSNM)) and Texas-New Mexico Power ((TNMP)). PSNM serves 544,000 customers in north and central New Mexico, including Albuquerque and Santa Fe while TNMP transmits and distributes power to 268,000 customers in Texas. The slide below from the recent Investors Presentation outlines the service territory in NM and TX.

{kind=link}

In New Mexico, PSNM operates as a fully integrated electric utility, operating a variety of power generating facilities along with transmission and distribution lines. PSNM also operates a relatively minor network of FERC-regulated high voltage transmission lines. Within the structure of regulated and decentralized Texas utilities, TNMP operates as an intrastate transmission and distribution company. Customer breakdown by revenue is diversified with residential comprising 30%, commercial at 26%, industrial at 5%, and other at 39%. Historically, PSNM has relied on coal as a major power-generating fuel source. Over the past 5 years, PSNM has embraced solar and wind which currently makes up almost half of its generation profile. As of 2023, renewables comprised 47% of power generation, natural gas 32%, nuclear 10%, coal 6%, battery 5%. According to the NREL and reproduced in the Presentation, PNM locale of New Mexico and Texas line up with the sweet spots of both wind and solar power generation, and as shown by the aggressiveness of PNM to replace coal with renewables, PNM could be considered as one of the most integrated utilities when it comes to renewables as a percentage of total power generation.

From a competitive return on equity ROE vantage point, both PSNM and TNMP are approved to earn a slightly below average rate of return. In a recent ruling by New Mexico regulators on Jan 4, 2024, PSNM is authorized to earn 9.26% ROE (down from previous 9.57%) on 50% equity from a $2.6 billion 2023 rate base for state-regulated assets. PSNM is allowed to earn 10.00% ROE on 50% equity from a $0.8 billion rate base for FERC-regulated assets. TNMP is currently authorized to earn up to 9.65% ROE on a 45% equity ratio from a $2.0 billion rate base. While seemingly inconsequential, the difference between the New Mexico 50% equity ratio and the Texas 45% equity ratio could be as much as $0.11 a share in annual earnings differential on a $2.0 billion rate base and a 9.65% ROE. Management is forecasting 10.7% annual growth in its rate base over the next 4 years, rising from $5.6 billion to $8.3 billion by the end of 2027.

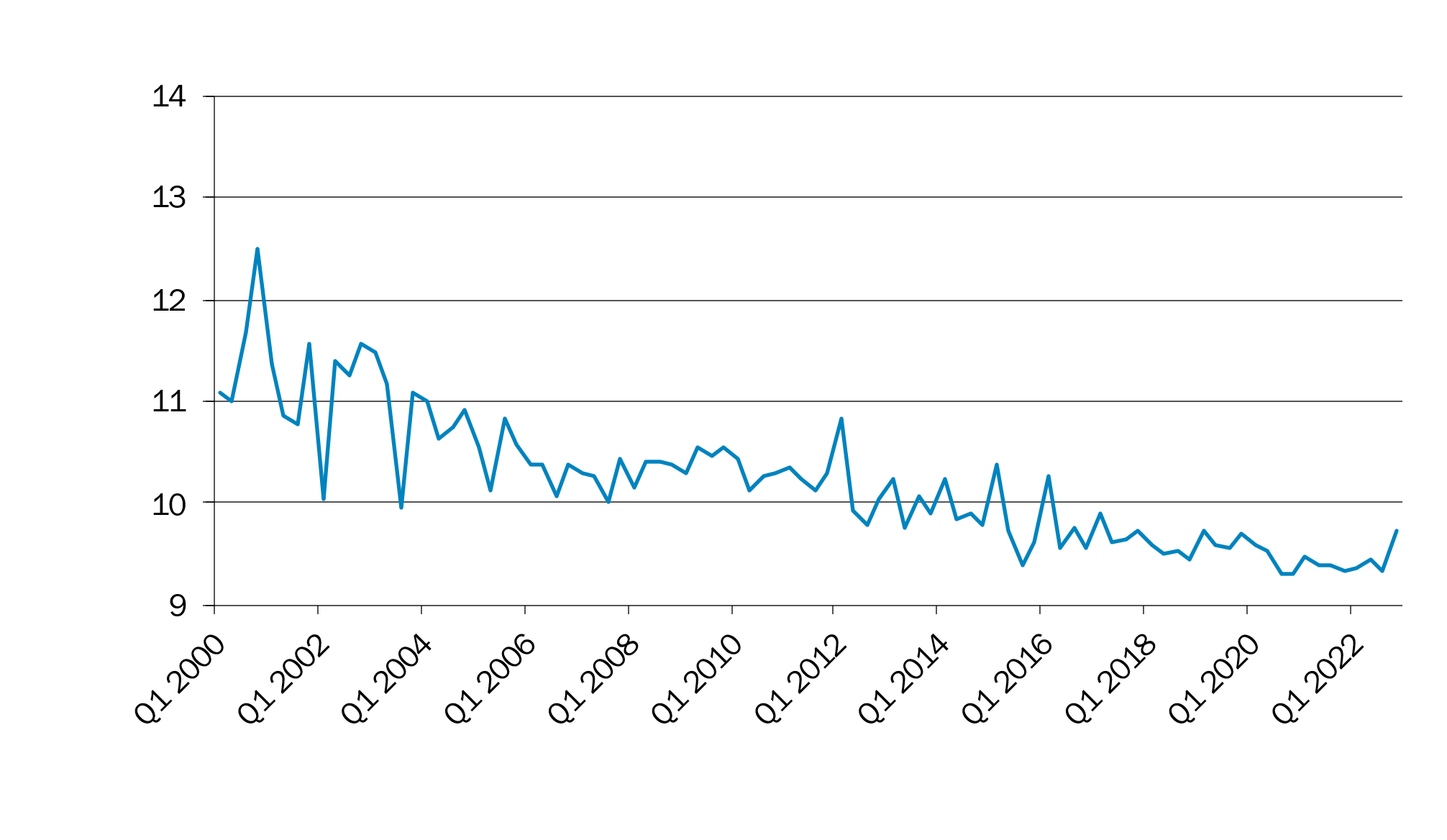

According to S&P Global ( SPGI ), the average ROE authorized for electric utilities was 9.71% for rate cases decided in the first quarter of 2023 (latest data available), up from the 9.54% average for the full year 2022 and about flat with the 9.73% for 4th qtr. 2022. The industry trade organization, Edison Electric Institute EEI, tracks the average quarterly approved ROE and publishes a historical chart, shown below. The electric utility industry is experiencing an uptick in allowed returns, mainly because of inflation-driven higher operating costs and higher financing expenses as a result of increasing interest rates.

{kind=link}

Luckily for investors, PNM utility service territory is a few miles too far from the proposed offshore wind farms to be a viable consideration. Unless the Texas Gulf Coast gets sucked into the same offshore wind frenzy as parts of the East Coast, PNM investors may have narrowly missed the financial albatross of offshore wind power development. However, peeling back a few more layers of PNM due diligence reveal my concerns, especially as it relates to electric utility sector peers. Two major worries are the potential for flattish diluted earnings per share over the next four years and its poor regulatory environment.

From the recent Presentation, management expects to issue $400 million in equity over the next 4 years to finance rate base expansion, for a share dilution of around 12% based on a current market cap of $3.3 billion. Management also projects a 5% annual EPS growth rate over the same period, before the effects of share dilution, from an estimated base of $2.48 for 2023 EPS. It seems earnings growth after dilution will be muted, at best.

The overriding issue with PNM Resources is the poor regulatory environment. FERC-regulated assets offer the best allowed returns but represent only 14.2% of current PNM rate base assets and in 2027 will represent 13.2% of PNM rate base assets. New Mexico and Texas offer below average ROE at 9.26% and 9.65%, respectfully, with the double whammy of Texas only allowing 45% equity on their ROE calculations. The rates for New Mexico and Texas reflect a below average allowed ROE compared to the information tracked by EEI and S&P.

As the ultimate gatekeepers of utility profit, regulatory oversight should be an important factor in utility selection. In a recent SA article supporting my Buy recommendation for American Electric Power ( AEP ) titled AEP: Attractive Transmission Assets , there is a link to the ratings and graphics for the State Regulatory Assessment listing maintained by the Regulatory Research Associates RRA, a service of S&P Global. RRA rates each state's financially support of the utilities under their jurisdiction. Individual states are grouped by three major classifications (Above Average, Average, Below Average) and three minor classifications, with New Mexico and Texas results being undesirable. New Mexico is considered Below Average - Average and Texas PUC is considered Average - Below Average. From the RRA list, there are 34 states with better regulatory ratings than those overseeing PNM Resources. Investors are strongly urged to review the RRA ratings by state.

On a peer basis, I prefer focusing on utilities serving those states identified as having the best regulatory oversight. According to RRA, the best states include Alabama, Florida, Georgia, Pennsylvania, Wisconsin, Iowa, Michigan, Mississippi, North Carolina, and Tennessee. Within the electric utility industry, investors should prefer American Electric Power for its FERC exposure and potential for improving operating profit margins; Southern Company ( SO ) for one of the industry's best overall regulatory environments; Canadian-based Emera ( EMRAF ) for its 50% rate base exposure to Florida regulators; and Duke Energy ( DUK ) for its diversified utility footprint in attractive states. NextEra Energy ( NEE ), WEC Energy ( WEC ), and Alliant Energy ( LNT ) also have preferred regulatory backgrounds over PNM Resources. The table below outlines current valuations, using Enterprise Value divided by trailing 12-month EBITDA as a valuation tool. Investors should keep in mind most utility mergers are consummated at a 12x to 15x valuation.

EV/EBITDA Valuations (Guiding Mast Investments, finance.yahoo.com)

Unfortunately, even a slightly better EV/EBITDA valuation compared to its electric utility peers does not compensate for PNM Resources' poor regulatory environment. Investors are better advised to rely on the best profit gatekeepers, as identified by RRA and S&P.

For further details see:

PNM Resources: No Merger, No Thank You