RAMPF - Polaris Renewable Energy: Intriguing Planet-Friendly Dividend Grower

2023-07-28 15:40:54 ET

Summary

- Polaris Renewables trades at a reasonable valuation and has a low debt to EBITDA ratio at 2.7x.

- Polaris has laid out plans to increase EBITDA by 30% over the coming two years for a reasonable investment.

- The company is continuing to look at other growth opportunities and has good cash on hand to make a sizeable acquisition.

- PIF should increase the dividend over time as cash flow increases meaningfully in 2023 and 2024.

Polaris Renewable Energy ( PIF:CA ) is an intriguing utility stock with a swathe of renewable energy projects in South America and the Caribbean. These countries are in great need of growth in power with renewables making up a larger portion of energy than developed countries. The company has done a good job over the last number of years diversifying its portfolio of power producing properties through different jurisdictions. Polaris pays a robust dividend of 5.74% that should grow over time as the cash flow generation of PIF improves. However, the shares have pulled back significantly with higher interest rates making the yield less attractive. As bond and GIC yields top out around 5 to 5.5%, Polaris has become more attractive at this level of $14 Canadian per share. The company is also an excellent choice for those looking for something focused on the environment that pays a solid yield. The company is a micro-cap at $300 million Canadian and has some risk associated with it due to the small number of revenue generating projects. However, the growth potential is strong and the company has proven itself capable of making smart acquisitions for a solid price in the region.

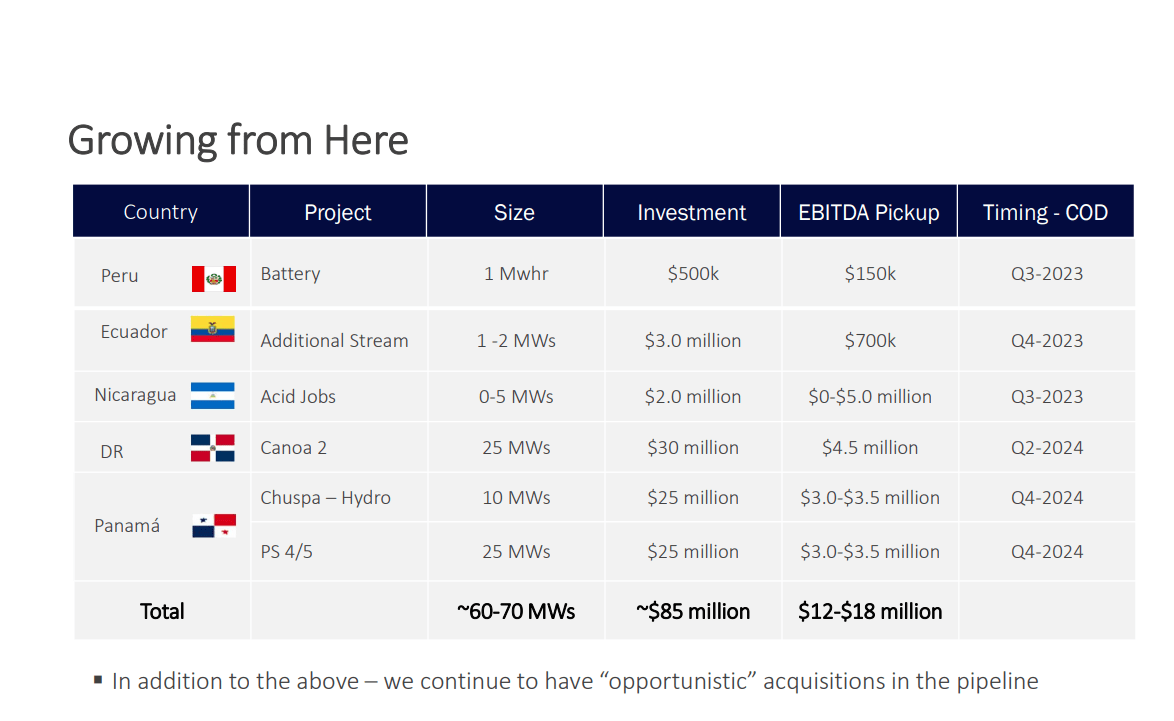

The company has done a good job diversifying itself over the past few years. For many years, the stock had a significant overhang for its largest producing geothermal plant in Nicaragua at San Jacinto. Eventually, some fears proved correct as the company was forced to negotiate a longer term power contract at a lower cost in late 2020. Now the contract is ongoing at a lower rate until January 2039 solidifying that asset and cash flow. All the while they have added a slew of operating and construction projects in Peru, Panama, Dominican Republic and Ecuador. Now the Nicaraguan facility is below 58% of the power generation of PIF and the long term government contract removes uncertainty. Having a foothold in these jurisdictions is also advantageous as the company can add further power capabilities. They are doing this now in the Dominican Republic as they drastically increase solar power generation there through Canoa 2 (part 2 of their solar installation). Canoa 2 will double the power generation in the DR for PIF, from $2 million quarterly to $4 million once completed. Polaris also just completed an acquired solar project in Panama for the cost of $10.7 million. It also means a strong working relationship with the local government and power companies preventing any permitting issues from arising. This was just connected to the grid in April 2023, with no current long term power contract in place yet. As such, the company will just sell into the free spot market and weigh whether they want to make a long term deal to ensure stability in revenues there. Other small improvements to many of the projects are also in the pipeline for 2023 and 2024 adding up to $18m of EBITDA. In 2022 the company had $45m in EBITDA showing these projects could increase EBITDA more than 30% for a reasonable investment of $85m USD.

{kind=link}

June 2023 (PIF presentation)

The balance sheet is strong with $40.6 million US in cash, and a recent export Canada loan facility of $10 million providing additional flexibility from March 2023. Earnings have started increasing again with $4.7 million in Q1 2023, up from $2.5 million in Q1 in 2022 or 22 cents per share. Earnings should continue to increase in the coming year as projects completed in the past year ramp up and investments generate more cash flow. The company is still looking at additional acquisitions outside the below projects, with prices likely coming down and patient management giving a great return on equity. The solid cash position and reasonable debt of $182m US means if a larger transformational deal is possible, PIF could consider it.

Polaris total energy production was up a solid 22.4% to 217,613 megawatt hours in Q1, with revenue following to $20.1m USD. Net debt to EBITDA is a very reasonable 2.7x for a utility company, allowing good runway for growth projects in coming years. The company continues to benefit from carbon credit sales as well, although they are a small portion of overall revenue at $883,000 in 2022, or under 2% of total revenue. They are pure profit for the company, however estimating the value is difficult as the prices vary widely over time. This revenue and profit will be a bonus in the future but not something to base an investment decision in PIF on. As you can see below, the dividend has been stable for several years, but equity has been rising steadily. Revenues for Nicaragua have been reset lower and are stable now for the long term, allowing growth to resume and revenues to head north. The last five quarters have seen revenue growth acceleration and additional projects coming online will assist cash generation. The additional growth projects above in 2023 and 2024 will add a solid chunk of EBITDA. This should allow the dividend to be raised again in early 2024, but growth is clearly the biggest focus for management for the long term. If larger projects become available for a good price, look for management to take those on if the long term return is worth it.

Buy Rated

Polaris Renewables has a good potential growth profile with a reasonable debt load allowing strong shareholder returns. The company has proven it can run multiple projects and upgrade existing projects at a low price to provide additional earnings potential. The company is paying a solid 5.6% dividend and capital appreciation potential is strong at $14 CAD per share today. Being a micro-cap stock in many difficult jurisdictions, the company has a much higher risk profile than your average utility player. Note that the stock is also fairly thinly traded, so positions of size can take some time to build. However, at 5+ years of solid execution, the company has proven it can execute to its longer term goals. I recommend buying shares at these low levels, as the stock should become more interesting over the next year as rates start to drift lower and people look at utilities again.

For further details see:

Polaris Renewable Energy: Intriguing Planet-Friendly Dividend Grower