CCO - Polen Capital Opportunistic High Yield Q2 2023 Portfolio Manager Commentary

2023-08-19 07:35:00 ET

Summary

- Polen Capital is a high-conviction growth investment manager. We scour the globe in search of the highest quality, sustainable companies to invest in.

- During the second quarter, the Polen Capital U.S. Opportunistic High Yield Composite outperformed the ICE BofA U.S. High Yield Index.

- Leveraged credit markets benefited from easing banking sector concerns, as well as better than expected economic data and earnings.

- Polen Capital did not make any significant changes to portfolio positioning during the quarter.

- We believe current yield levels are very attractive and more than compensate investors for the increased risk.

{kind=link}

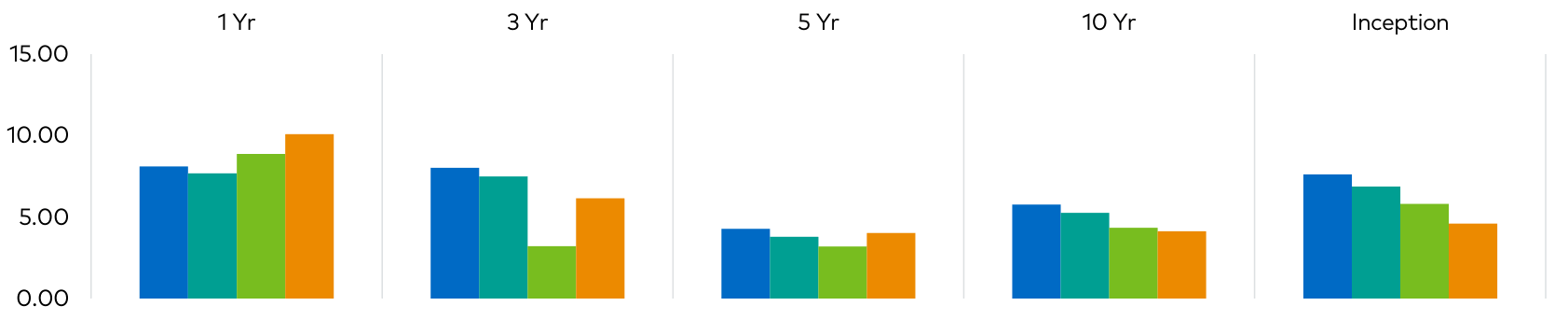

| Polen U.S. Opportunistic High Yield (Gross) |

| 3.60 |

| 7.29 |

| 8.12 |

| 8.03 |

| 4.27 |

| 5.76 |

| 7.62 |

| Polen U.S. Opportunistic High Yield ( NET ) |

| 3.45 |

| 7.03 |

| 7.68 |

| 7.50 |

| 3.79 |

| 5.25 |

| 6.88 |

| ICE BofA U.S. High Yield Index |

| 1.63 |

| 5.42 |

| 8.87 |

| 3.21 |

| 3.19 |

| 4.34 |

| 5.81 |

| Credit Suisse Leveraged Loan Index |

| 3.12 |

| 6.33 |

| 10.10 |

| 6.16 |

| 4.02 |

| 4.13 |

| 4.60 |

| The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Periods over one-year are annualized. Performance figures are presented gross and net of fees and have been calculated after the deduction of all transaction costs and commissions, and include the reinvestment of all income. Please reference the GIPS Report which accompanies this commentary. The commentary is not intended as a guarantee of profitable outcomes. Any forward-looking statements are based on certain expectations and assumptions that are susceptible to changes in circumstances. Opinions and views expressed constitute the judgment of Polen Capital as of the date herein, may involve a number of assumptions and estimates which are not guaranteed, and are subject to change. All company-specific information has been sourced from company financials as of the relevant period discussed. |

Commentary

High yield bonds and leveraged loans produced solid gains in the second quarter. However, performance was lumpy, as gains in April were erased by losses in May, before a strong rally in June. During the quarter leveraged credit markets benefited from easing banking sector concerns, as well as better than expected economic data and earnings. At the same time the market dealt with volatility from the debt-ceiling debate and an ever-shifting Fed narrative. Further, while recession risks remain, those concerns moderated, providing a more favorable environment for lower-rated credits, which meaningfully outperformed in June and in the quarter overall.

In Q2 2023, all but one sector of the high yield bond market produced a gain. The top performing sectors were the Retail, Leisure, and Real Estate sectors. Conversely, the biggest laggards were the Banking, Consumer Goods and Utility sectors. Unlike high yield bonds, all sectors in the leveraged loan market produced a gain. The top performing sectors were Consumer Durables, Gaming & Leisure, and Housing. Meanwhile, the Retail, Healthcare and Chemicals sectors were the biggest laggards.

Following the slowdown in Q1, capital market activity for high yield bonds rebounded in Q2 with more than half of the total in BB rated, and more than half was used to refinance existing debt.

Notably, close to 30% of the quarter’s new bonds were used to finance LBOs or acquisitions. Conversely, leveraged loan new issue activity declined from last quarter. As a result, primary market activity for leveraged loans is well behind the total issued during the same period last year. Like high yield bonds, refinancings dominated capital market activity among loans, accounting for close to 75% of the quarter’s total.

In Q2, high yield funds received $3.6bn of inflows, dominated by ETFs. Conversely, leveraged loan funds continued to experience outflows. Leveraged loan mutual funds have seen close to $57bn exit over the past 14 months, including $7.9bn of outflows in Q2 alone. Further, CLO creation slowed, and produced the lowest total since Q3 2020.

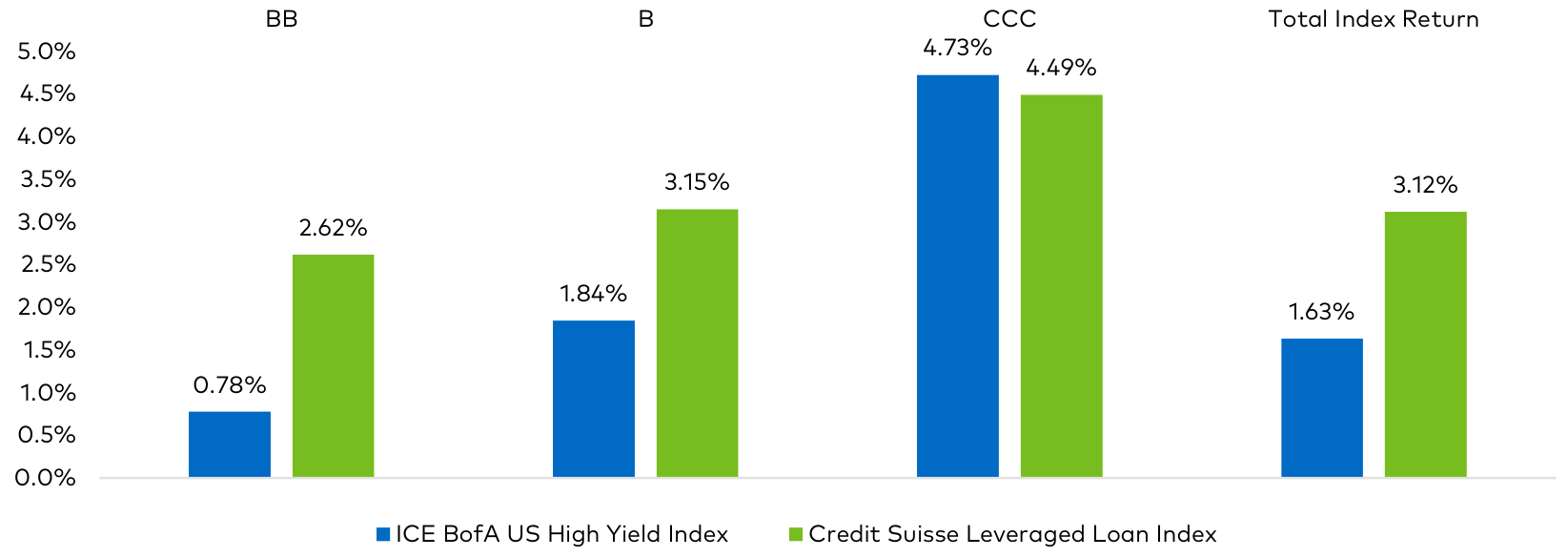

Q2 2023 Total Returns by Quality Rating

{kind=link}

Lastly, as anticipated, default rates continue to rise. In Q2, a total of $22.4bn of high yield bonds and loans defaulted. At the end of Q2, the trailing-twelve-month default rates for high yield bonds and leveraged loans were 1.65% and 2.41%, respectively. Although these rates are well below their historical averages of approximately 3%, both nonetheless represent 2-year highs.

Portfolio Performance & Attribution

The representative account of the Polen Capital U.S. Opportunistic High Yield Composite [1] generated a gross total return of 3.66% during the second quarter and outperformed the ICE BofA U.S. High Yield Index by 203 bps. In Q2, U.S. Treasury yields moved higher. As a result of its shorter duration relative to the benchmark, the duration effect for the quarter was positive. Further, the portfolio’s income advantage relative to the benchmark contributed to the portfolio’s relative performance. Lastly, the portfolio’s aggregate restructured private equity holdings detracted from relative returns.

Focusing on quality attribution, given the outperformance of CCC-rated credits relative to BB-rated credits, the portfolio’s overweight to the former and underweight to the latter, contributed to relative performance during the quarter. Conversely, the portfolio’s aggregate security selection effect by quality rating was negative. Specifically, the portfolio’s B3-rated, CCC1-rated, and CCC2-rated holdings lagged those of the index and detracted from relative performance. However, these negative effects were partially offset by a positive security selection effect generated by the portfolio’s B2-rated and CCC3rated holdings, which outperformed those of the index.

From a sector perspective, attribution shows that the sector allocation effect was positive and contributed to relative performance. This positive effect was driven by the portfolio’s overweight in the Retail, Insurance, and Capital Goods sectors. In addition, the sector security selection effect was positive. The portfolio’s holdings in the Capital Goods, Automotive, Services, and Transportation sectors outperformed those of the index and contributed to relative performance. However, these positive effects were partially offset by the negative effects produced by the portfolio’s holdings in the Leisure and Retail sectors, which lagged those of the index and detracted from relative performance.

Notable issuers that contributed to, or detracted from, the portfolio’s total return for the quarter are set forth below.

Contributors

Tekni-Plex manufactures packaging products used in the healthcare, food, and specialty sectors. Specific products include medical tubing, barrier films used for packaging pharmaceuticals, egg cartons, and protein trays, as well as rubber gaskets and dip tubes used in aerosol containers. During the quarter, Tekni-Plex’s 6.625% Senior Notes due 2025 and 9.25% Senior Notes due 2024 held in the portfolio were repaid with the proceeds of a new $620 million tranche of 12.75% Senior Notes due 2028. As both the 6.625% Senior Notes due 2025 and 9.25% Senior Notes due 2024 were trading below par at the beginning of the quarter, performance benefited from both bonds appreciating to their call price during the quarter. The portfolio also participated in the Company’s new 12.75% Senior Notes due 2028, and the appreciation in the new bonds since issuance also contributed to favorable performance during the quarter. The Company’s leverage is expected Company’s leverage is expected to remain high as Tekni-Plex continues to pursue debt-financed acquisitions and will also face challenging year over year comps for the remainder of 2023. However, Polen Capital views Tekni-Plex as an attractive business and believes the new 12.75% Senior Notes due 2028 offer an attractive yield and are well covered based on the underlying value of the franchise.

ViaSat ( VSAT ) is a global satellite communications service and equipment provider to commercial and government customers. Specifically, the Company provides consumer satellite internet service to rural customers, in-flight broadband for commercial flights / airlines, and connectivity services and equipment for government use. The portfolio’s holdings in the Company’s 5.625% Senior Notes due 2025 and 6.5% Senior Notes due 2028 traded higher during the quarter. In late April, the Company successfully launched the first satellite of the three-satellite constellation (“ViaSat-3”), removing some of the execution risk at the Company as this launch had been delayed a number of times. In addition, ViaSat closed on the $6.1 billion acquisition of Inmarsat in May, which further reduced perceived execution risk at the Company. Polen Capital continues to believe the Senior Notes offer an attractive risk versus reward profile, and as such, maintains these positions in the portfolio.

Detractors

CWT Travel Group Inc. ( CWT ) is a travel management company that manages business travel, meetings, incentives, conferencing, and exhibitions, as well as handles event management. The portfolio’s investment in the Company’s 8.5% First Lien Notes due 2026, preferred equity, and restructured equity underperformed during the period as the Company use of cash accelerated in the face of a slowdown in the velocity of the business travel recovery post COVID. In addition, the Company has also faced some large and public customer losses. Polen Capital continues to hold these positions in the portfolio and is monitoring the situation at the Company closely.

American Tire Distributors the subsidiary of ATD New Holdings ( AHLD ), is the largest replacement tire distributor in North America based on dollar amount of wholesale sales and number of warehouses. The Company distributes close to 40 million tires annually through its collection of 140+ distribution centers in the United States & Canada. The portfolio’s investment in the Company’s common stock, which was received as a result of a Chapter 11 restructuring and resultant reorganization, depreciated in value during the quarter. The Company’s first quarter 2023 results were disappointing with EBITDA falling by approximately $50 million year-over-year due to a combination of weaker volume as well as an absence of certain inventory gains experienced during the same period in 2022. However, the Company was able to take steps to reduce inventory which supported cash flow generation.

Furthermore, the Company is advancing on other strategic initiatives including logistics to mitigate the current tire market softness. Polen Capital continues to hold the Company’s common stock in the portfolio.

Portfolio Positioning

Polen Capital did not make any significant changes to portfolio positioning during the quarter. However, we did execute the credit sale described below. Proceeds from this transaction, combined with other relative value trades, were used to fund the two purchases detailed below. We also increased positions in existing holdings, particularly first lien loans, in which we have a great degree of confidence and find the absolute and relative level of yields attractive for the risks incurred.

Sale - Clear Channel Outdoor 7.75% Senior Notes due 2028 and Clear Channel Outdoor 7.50% Senior Notes due 2029 - Clear Channel Outdoor ( CCO ) is a leading outdoor advertising company in the U.S. and Europe. The Company’s billboards, posters, airport, and transit displays offer advertisers a chance to connect with consumers out of the home. The Company’s U.S. operations recovered strongly out of COVID; however, lags in the European business and wider macro weakness began to pressure results in the beginning of the year. This weakness, coupled with higher interest rates, have reduced the free cash flow outlook, limiting opportunities to organically deleverage. Given that the Company’s capital structure is already highly levered, with a 90%+ loan-to value, the lack to value cash flow generation and growth in 2023 reduces the likelihood the Company will be able to grow into their capital structure. As a result of this concern, along with some recovery in the price of the Senior Notes alongside the broader rally in CCC-rated debt, Polen Capital sold a substantial portion of its holdings during the quarter.

Purchase - Chart Industries 9.5% Senior Notes due 2031 - Chart Industries ( GTLS ) is a leading global provider of specialty highly engineered equipment in the liquification, transportation and storage of gaseous elements. Chart Industries produces customized solutions that touch nearly every step of the energy production process, as well as several other end markets. Additionally, the Company is on the forefront of the energy transition, providing both efficient solutions for existing technologies as well as repurposing and developing new technologies for renewable energy. In the summer of 2022, the Company announced a transformational acquisition of Howden, a leader in specialty compression and air handling systems, which was financed primarily through debt offerings. Howden had nearly 50% of its revenue derived from its high margin and steady aftermarket business, and as a result helps to smooth the overall Chart Industries financial profile away from project-based revenues to a more consistent and repeatable business. While this transaction increased leverage, the Company has made delevering the balance sheet the primary goal for the next several years, publicly stating that there will be no stock buybacks, dividends or otherwise equity-friendly transactions until the balance sheet is below its 2.5x leverage target, making it a natural upgrade candidate. In the months since the transaction closed, the Company has already executed over $100mn in cost/commercial synergies and has divested non-core business lines with proceeds to go towards debt repayment, strengthening the upgrade narrative. Polen Capital believes the Senior Notes offer an attractive risk versus reward profile for exposure to a high margin, low capital intensity growth business.

Purchase - Learning Care Group LIBOR + 3.25% First Lien Term Loan due 2025 - Learning Care Group is an early childhood education provider with over 1,000 locations across the United States that operates under six different banners. Polen Capital has become increasingly positive on the combination of the cyclical and secular tailwinds in the early childhood education sector. Cyclically, the industry is recovering from the COVID related downturn with enrollments and revenues expected to surpass pre-COVID levels in fiscal year 2023. Further, the margin profile of the industry should begin to surpass prior peaks as the combination of higher enrollment and higher pricing is offsetting labor inflation and providing fixed cost leverage. On a secular basis, industry data shows that approximately 20% of the industry closed during the pandemic, and the surviving companies, such as Learning Care Group, now have a strong organic growth profile as they fill the void left by the multiple closures witnessed by the industry. We believe that that combination should enable Learning Care Group to generate EBITDA that surpasses prior peaks, de-leverage the Company, and set the stage for a refinancing in late 2023 or early 2024. Accordingly, Polen Capital believes that the First Lien Term Loan has the potential to provide a strong risk adjusted return.

Outlook

The lack of significant maturities facing the leveraged credit market in the short term has been a positive factor supporting the strong performance this year. Due to the record level of refinancing activity that occurred between 2020-2021, as of this writing, only approximately 12% and 14% of the high yield bond and bank loan markets, respectively, are expected to mature before the end of 2025. Nonetheless, as interest rates have increased, primary market activity has declined. With each passing month, the calendar edges closer to an acceleration in maturities. Accordingly, we believe that investors will sharpen their focus on the maturity profile of the market during the second half of this year.

As maturities increase, the risk of defaults naturally rises as well. To avoid potential defaults and restructurings, issuers will need to address their debt obligations well ahead of maturity. As this process begins to unfold, we anticipate that primary market activity will increase in both the high yield bond and bank loan markets. This issue is most pressing amongst the lower-rated segment of the leveraged credit market (i.e., CCC-rated and below) as this cohort has a disproportionate percentage of debt maturing over the next two years.

While the relatively strong fundamental health of the high yield bond market should aid issuers seeking to refinance their debt, the higher coupon payments they will be required to pay in connection with any refinanced debt will be scrutinized by investors. Many of these issuers locked in fixed rate coupons on their existing bonds before the Fed’s rate hiking cycle began. As a result of much higher interest rates, the coupon payments on newly issued high yield bonds could pressure the cash flow profile of certain companies. Issuers of floating rate debt are already grappling with higher interest costs. For example, the average bank loan issuer’s floating rate coupon payment has increased substantially from just over 4% to almost 9% over the past eighteen months. With inflation double that of the Fed’s preferred 2% target, it is likely that rates and floating coupons will remain higher for a longer period of time.

Furthermore, the outlook for the economy remains uncertain. The negative yield spread, or curve inversion, between 10-year U.S. Treasury Notes and 3-month U.S. Treasury Bills signals a possible recession. However, based on year-to-date performance, the leveraged credit market does not appear overly concerned about an economic contraction in the near term. The high yield bond and bank loan markets have each generated strong returns over this period, as credit spreads have tightened and CCC-rated debt in both markets has outperformed its higher-rated peers. If the economy were to enter a recession as issuers seek to refinance their fixed income obligations, we could see an acceleration in default activity.

While default rates rose during the first half of this year, high yield bond and bank loan default rates are still below long-term averages. Although we expect defaults to continue to increase, most estimates predict average conditions in the coming quarters. At Polen Capital, we are cautiously optimistic that default rates, particularly for high yield bonds, will not rise to levels experienced during past downturns should the economy fall into a recession. In the aggregate, we believe that the fundamental health of the high yield bond market is better than has typically been the case in instances where the economy has begun to slow.

Experience in High Yield Investing

In addition, the maturity profile of the market is still favorable, although issuers will have to begin addressing their upcoming maturities in the near future.

Although each credit cycle is different, it is often the case that an exogenous factor spurs the end of the cycle. In the first quarter of 2023, the mini-banking crisis in the U.S. shook markets. While the Fed took steps to mitigate a repeat of that event, the banking sector is not immune to future shocks and failures. For example, growing concerns about declining Commercial Real Estate (“CRE”) values in the wake of the COVID-19 pandemic could create further pain for banks due to the substantial volume of CRE debt outstanding, a significant amount of which is held by banks. For these banks, a further decline in real estate values could add to their already challenged financial position. Renewed angst about the banking sector or an increase in default activity among CRE borrowers could be the exogenous factor that causes spillover effects into corporate debt markets.

Despite the uncertain environment, we still maintain a constructive view of the market. Although we expect defaults to increase as the maturity schedule shifts, we believe current yield levels are very attractive and more than compensate investors for the increased risk. In addition, the aggregate leveraged credit market has stronger fundamentals relative to pre-pandemic conditions. We continue to identify attractive opportunities amongst issuers across each segment of the leveraged credit market, and we view the current environment as favorable for an active manager like Polen Capital to potentially generate significant alpha for its clients. However, careful credit selection remains paramount as high yield bond and bank loan markets could respond swiftly to an exogenous shock.

Sincerely,

Dave Breazzano, Ben Santonelli, and John Sherman

Footnotes[1] The Composite information provided is based on a representative account of the Polen Capital U.S. Opportunistic High Yield Composite. The representative account is an account within the Polen Capital U.S. Opportunistic High Yield Composite that Polen Capital Credit has deemed the most representative of the Polen Capital Credit-managed accounts pursuing the investment strategy. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Polen Capital Opportunistic High Yield Q2 2023 Portfolio Manager Commentary