VWAPY - Porsche Holding SE: Cheap For Good Reasons

2023-11-13 18:01:44 ET

Summary

- Due to the NAV discount, Porsche Holding SE has been a well-known value investment for a while.

- While at first sight it looks compelling, a rational analysis reveals a lot of risks.

- Ultimately the NAV discount is justified because the final return is simply too unpredictable.

Heisenberg In Action

While I was looking at Porsche Holding SE ( OTCPK:POAHY ) ( OTCPK:POAHF ), it often felt like an example of Heisenberg's "Uncertainty Principle" :

It states that there is a limit to the precision with which certain pairs of physical properties, such as position and momentum, can be simultaneously known. In other words, the more accurately one property is measured, the less accurately the other property can be known.

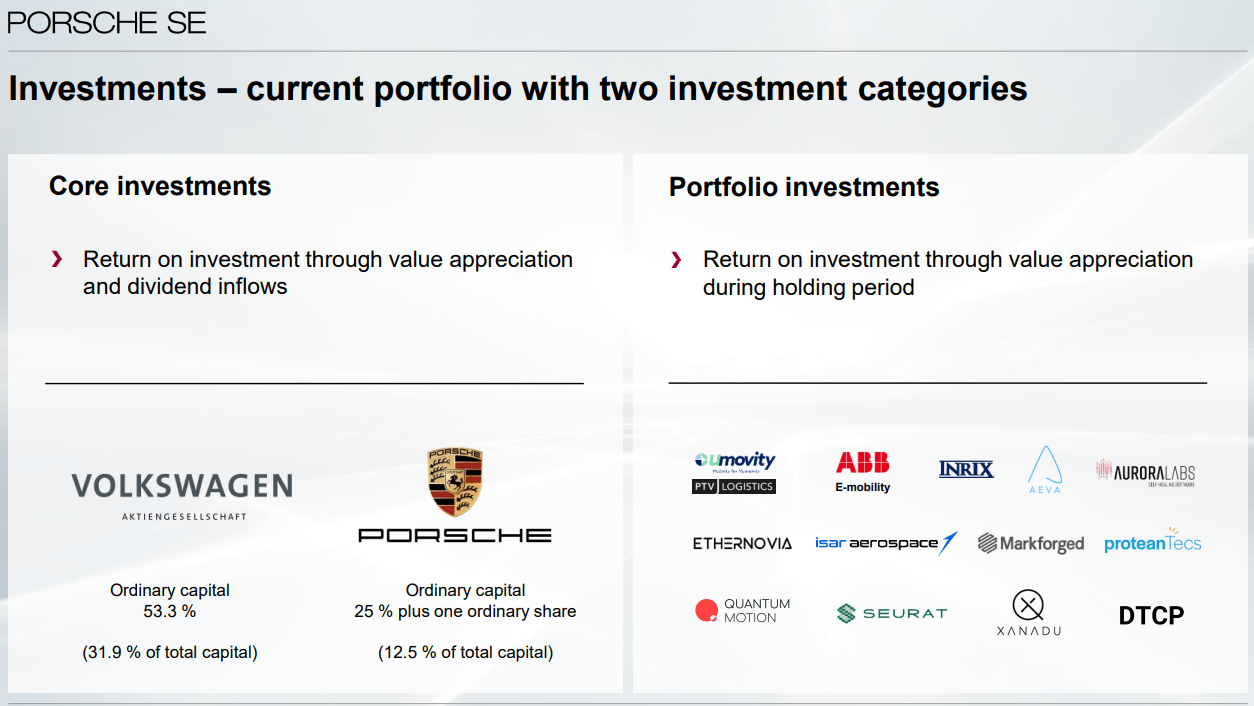

At first sight, the story is (quite) simple: We have two automobile manufacturers, Volkswagen AG ( OTCPK:VWAGY ) ( OTCPK:VWAPY ) ( OTCPK:VLKAF ) and Porsche AG ( OTCPK:DRPRF ), both of which have two classes of shares, ordinary (voting) and non-voting (preferred) shares. The holding company we are examining, Porsche Holding SE, owns a controlling stake in Volkswagen and a blocking minority in Porsche AG.

Porsche Holding SE structure (Porsche Holding SE presentation)

{kind=link}

The total current value of the Holding's properties is:

| Volkswagen, 53.3% of voting stock |

| €18.28B |

| Porsche AG, 25% of voting stock |

| €10.73B |

| Other holdings (estimate) |

| €0.2B |

| Net debt |

| €6.7B |

| NAV |

| €22.51B |

| NAV/share |

| €73.5 |

| Market cap |

| €13.4B |

| Current share price |

| €43.78 |

| Discount to NAV |

| 40% |

Even the holding company has the usual two classes of shares, but only the non-voting shares are quoted, while the voting rights are entirely owned by the Porsche and Piëch families.

Which means in a nutshell:

Porsche/Piëch families control Porsche Holding SE, which controls Volkswagen AG, which controls Porsche AG.

Rather counterintuitively, the Porsche Holding exercises only indirect control over its namesake business. In fact, it owns only a blocking minority in it. - Wait a minute: Why would it need a blocking minority, if it already indirectly controls Porsche AG through the holding company's Volkswagen controlling stake?

This is where Heisenberg kicks in.

The Mother of All Short Squeezes

Back in 2008, the investment world's incredulous eyes were watching a series of events that nobody would have been able to predict:

Reports emerged of angry traders raging at what they perceived to be a Blitzkrieg attack by Porsche on the financial system, seemingly allowed by German regulators, which permitted it to secretly accumulate VW stock options without having to declare its hand.

You can read the story of the short squeeze here and get all the details on Wikipedia .

The key issue was that Porsche was effectively piling on debt that would eventually be paid off with VW cash - which, however, was out of reach unless ownership reached 75%.

A report on the story from 2012 minced no words:

Porsche's former CEO, Wendelin Wiedeking, considered almost the Lee Iacocca of the European auto industry, tried to engineer the deal through a complex and shady web of financial maneuvers and investments that came completely unglued and almost bankrupted Porsche. ... Indeed, after Porsche attempted the hostile takeover of VW, it was Volkswagen that came to Porsche's rescue. The deal has been delayed while the companies and the lawyers have been trying to sort out who will be on the hook for a number of shareholder lawsuits should they get decided in the favor of the plaintiffs.

However, the squeeze ultimately resulted in the Porsche and Piëch families losing direct control over their own business, while acquiring (sort of) control over Volkswagen. (Thanks to special statutes, Volkswagen is effectively controlled by the local government.)

Ironically, the same short squeeze which created so much angst among traders almost bankrupted Porsche, as in the process of acquiring a majority holding in Volkswagen AG, Porsche Holding SE had built up a multi-billion burden, aggravated by taxes due on very large paper profits on Volkswagen AG options.

And finally it was Volkswagen itself that came to Porsche's rescue, injecting the necessary capital to pay back the Holding's debt, but acquiring in exchange total control over the families' manufacturing business.

The question that is not addressed by any of these reports is why for heaven's sake Porsche wanted to take over Volkswagen - I mean the real reason, not the official one(s).

They started by saying that they were afraid of a hostile takeover attempt by hedge funds to break up Volkswagen, so Porsche came to the mass market auto builder's rescue (but would not attempt a full takeover).

Later they talked about synergies, so they needed a majority.

But this does not explain why they needed a full takeover, as there was already a very intense cooperation between the historically very closely related two companies.

In addition, as can be read in the linked Wikipedia article, both German regulators and EU courts favored the operation openly or indirectly.

Hence, the more we look, the less we understand.

What We Do Know

The only certainties in this story are:

- The Porsche and Piëch families not only love mechanics, but also financial engineering.

- However, they apparently feel a little too secure in their maneuvers with billions worth of complex options that their dealings can easily backfire.

- They absolutely want to control things, but capital needs to come from elsewhere. This is why we always get dual share structures, why shares are often acquired with borrowed money and why they basically rely on Volkswagen dividends for debt and interest repayment.

- Not only at the corporate level they like debt and OPM : In 2021, right around peak valuations of the Holding, its Deputy Chairman Hans Michel Piëch used 25m Holding shares as collateral for a loan, representing 16% of (unquoted voting) shares outstanding. Since that day, the Holding's non-voting and quoted stock has lost 50% of its value. We can now wonder what the bank on the other side of this trade might do and how such remedies would affect the quoted stock.

Ultimately, it looks like the Holding exists only as a financial engineering vehicle to gain back full control of the families' main business. Its capital is OPM, the families are in control, but a public company is obviously helpful when it comes to accessing the bond market - for even more external financing.

We should expect the controlling families to aggressively pursue the expansion of their empire - which is not limited to the namesake Porsche AG, but might also include total control over Volkswagen (and who knows what else).

What they cannot totally control are the real-world risks of second-, third- and fourth-order effects resulting from too much complexity.

"I now see that we can nothing know", says Goethe's Faust .

For ordinary investors without any control over the Porsche and Piëch families' actions and without solid insights into their intentions this means a lot of uncertainty - which warrants a rather high complexity discount. If holding companies usually trade for at least 10-15% less than their NAV, in this case, I would absolutely apply a higher discount of at least 20%.

Lawsuits

The Holding is still involved in a series of lawsuits related to its actions back in 2008 which could potentially result in very high damage payments.

You can find a complete overview in the H2/23 report from page 8. The most important €5.4B (+ interest) claim concerns alleged market manipulation and insufficient public disclosures in connection to the VW takeover attempt. While Porsche won a first trial, the plaintiffs filed an appeal and the final decision of the Federal Court of Justice is still pending.

Potential damage estimates range from a couple of billion up to 10 billion Euros. Some analysts therefore subtract the average sell-side estimate of potential cash outflows from their NAV calculation, which is around €4B. This reduces the NAV discount by another 13%.

However, things are not that simple. The key issue here is again: What would be the second and third order effects of such cash outflows? Where would the money come from? Which creative deals will the families resort to? Will these deals be mainly in the interest of the families' pursuit of control or will they be structured in the best interest of all shareholders?

So there is additional uncertainty (if not negative certainty). To some extent, the controlling families (and public shareholders with them) already depend on the kindness of strangers; once the Holding needed to come up with billions of cash, strangers might not remain as kind as before.

Conclusion

We started with a NAV discount of 40% and discovered why a total discount of 33% for legal risks and all sorts of uncertainties appears to be reasonable. This leaves us with a meager margin of safety of just 7%, which is too little to pique my interest and I can only rate Porsche Holding SE as a (low-conviction) Hold.

For further details see:

Porsche Holding SE: Cheap For Good Reasons