PTMN - Portman Ridge: Bear Market Bites The BDC Business

Summary

- Portman Ridge reported a miss in Q2 2022 due to delayed closings.

- The overall decline in the market has affected BDC total returns, but Portman Ridge has performed better than most in the past 6 months.

- With a -26% discount to NAV and a 12.5% yield, Portman Ridge is worth watching, but is a Hold for now.

An asset class that is currently popular with investors due to the high dividend yield they typically offer is the business development company ("BDC") industry. There are about 50 publicly traded BDCs currently in the BDC universe . One that I have covered previously in this article that was published in June is Portman Ridge Finance Corporation ( PTMN ). In that article, I rated PTMN a Buy due to its (at the time) 11% annual yield and trading at a -21% discount to book value.

article summary (Seeking Alpha)

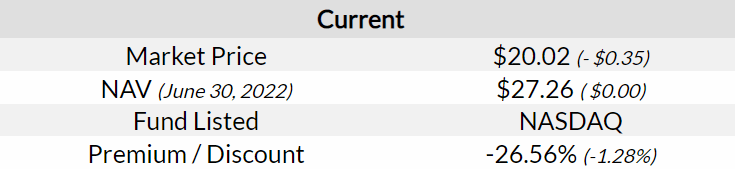

Today, as of October 14, 2022, the price closed at $20.02, and the yield sits at 12.5% with the discount to NAV estimated at -26.5%.

{kind=link}

Since my article in June, the stock has dropped -12.7% despite having just raised the dividend in March and after reporting a miss on earnings in an otherwise respectable Q2 report , considering the state of the market in June:

- Portman Ridge Finance press release : Q2 NII of $0.57 misses by $0.13.

- Total investment income of $15.04M (-30.2% Y/Y) misses by $1.45M.

- Net asset value for the second quarter of 2022 was $261.7 million as compared to $278.3 million in the first quarter of 2022.

- As of June 30, 2022, three of the Company’s debt investments were on non-accrual status compared to six as of March 31, 2022.

During the second quarter, the company repurchased 106,000 shares and refinanced its revolving debt facility. They also declared another $0.63 dividend to be paid on September 2.

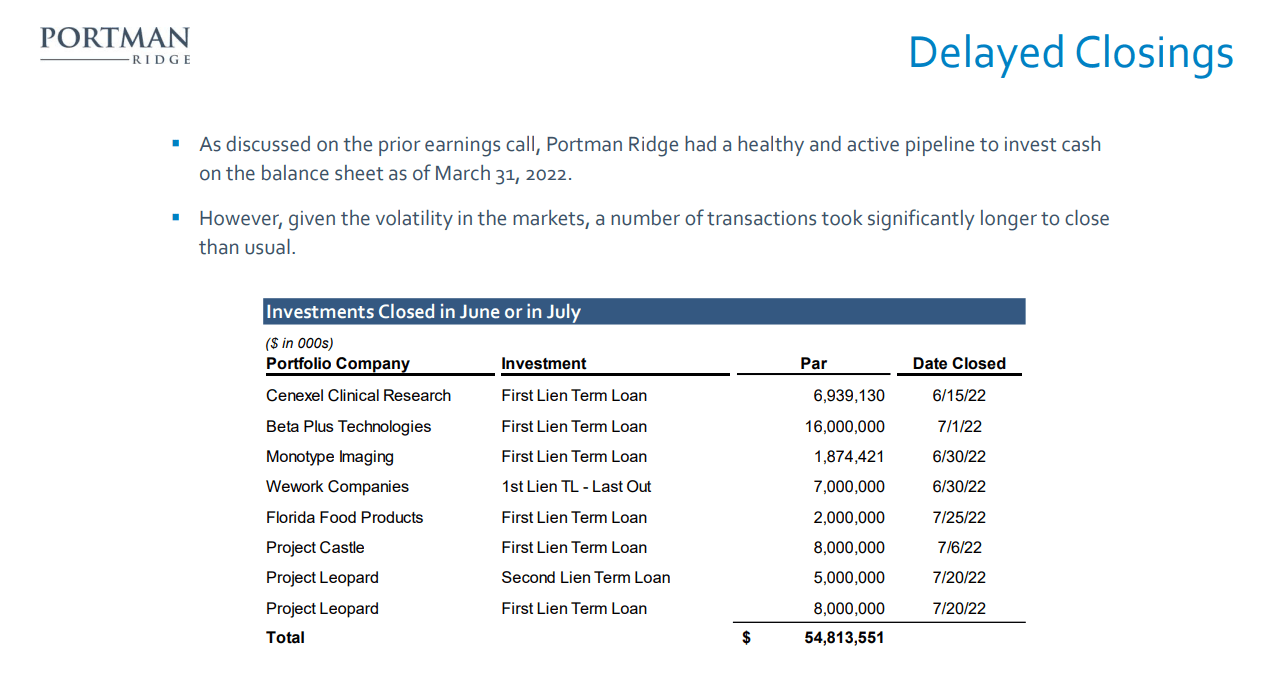

The earnings miss was attributed to a delay on deployment of some new investments that were in the pipeline from Q1.

Ted Goldthorpe, Chief Executive Officer of Portman Ridge, stated, “As seen by many in our industry, our operations have been affected by the challenging economic environment, rising interest rates and market volatility.... Investment activity was strong, and although originations are still lower than the second half of 2021, during the second quarter, we deployed approximately $32.9 million of our available cash in new investments and an additional $20.6 million in the beginning of the third quarter, all but $7.2 million of which were investments we had in the pipeline since the end of the first quarter.

After the Q2 report, and based on continued market deterioration subsequently in the overall market and the BDC industry specifically, I decided to exit my long position and sit on the sidelines and watch PTMN for a few months. Since the Q2 report on August 9, many BDCs have been struggling to maintain their market value due to worsening economic conditions from ongoing inflation, rising rates (which should actually benefit some BDCs), and volatility in credit markets that is unlike anything we have witnessed in many years.

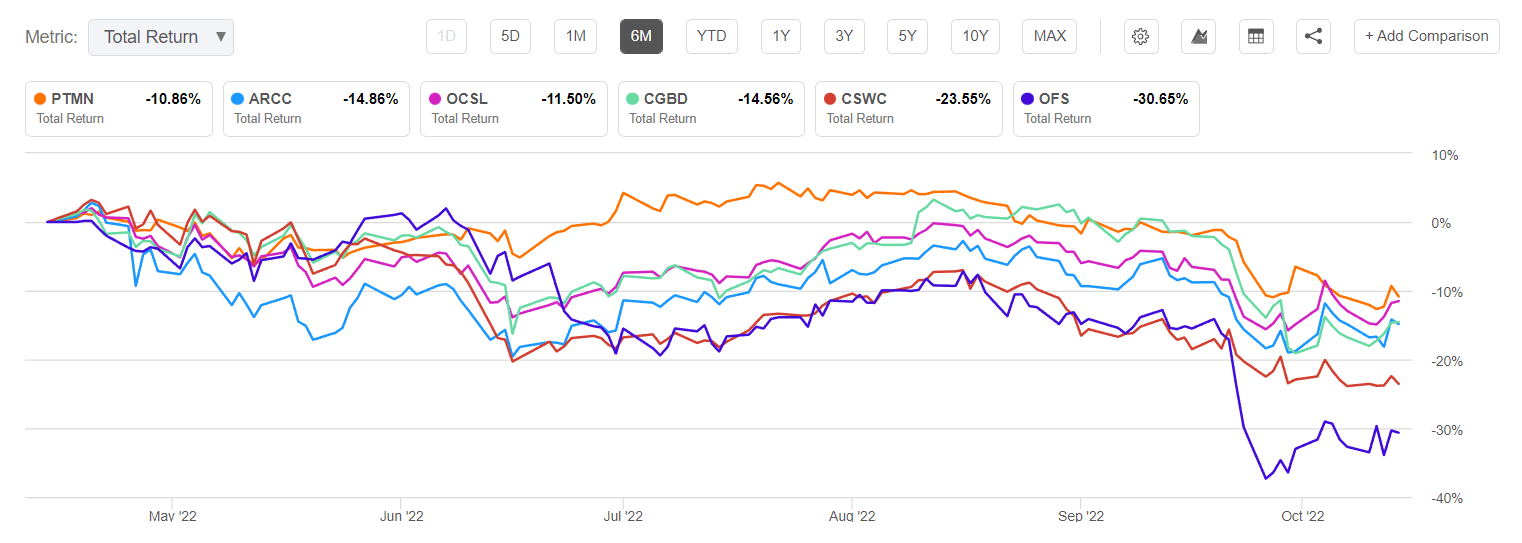

Comparing the total return of PTMN with several similar BDCs that I either own or follow closely, all are struggling to offer a total return better than -10% over the past 6 months. Looking at the total returns of PTMN compared with Ares Capital ( ARCC ), Oaktree Specialty Lending ( OCSL ), OFS Capital ( OFS ), Carlyle Secured Lending ( CGBD ), and Capital Southwest ( CSWC ) shows that PTMN is doing OK relative to the other five.

{kind=link}

As I mentioned at the beginning of the article, there are 50 BDCs, and I am not going to look at all of them here, but the trend is pretty evident from this snapshot. It has been a difficult year, and the past few months have been challenging for just about every asset class other than the energy sector. I remain cautious about any additional investments in BDCs until there is a change in the market trend or a pivot by the Fed on interest rates.

Meanwhile, PTMN issued a shareholder update in their September investor slide deck that is available on their website . In that slide deck, there is reason to be encouraged about the future of PTMN. For example, more than 93% of the floating rate assets are on LIBOR contract. Those contracts take time to reset and remain significantly below 3-month LIBOR rates. Credit quality has been stable, with only 3 investments on non-accrual as of June 30 (compared with 6 in the first quarter).

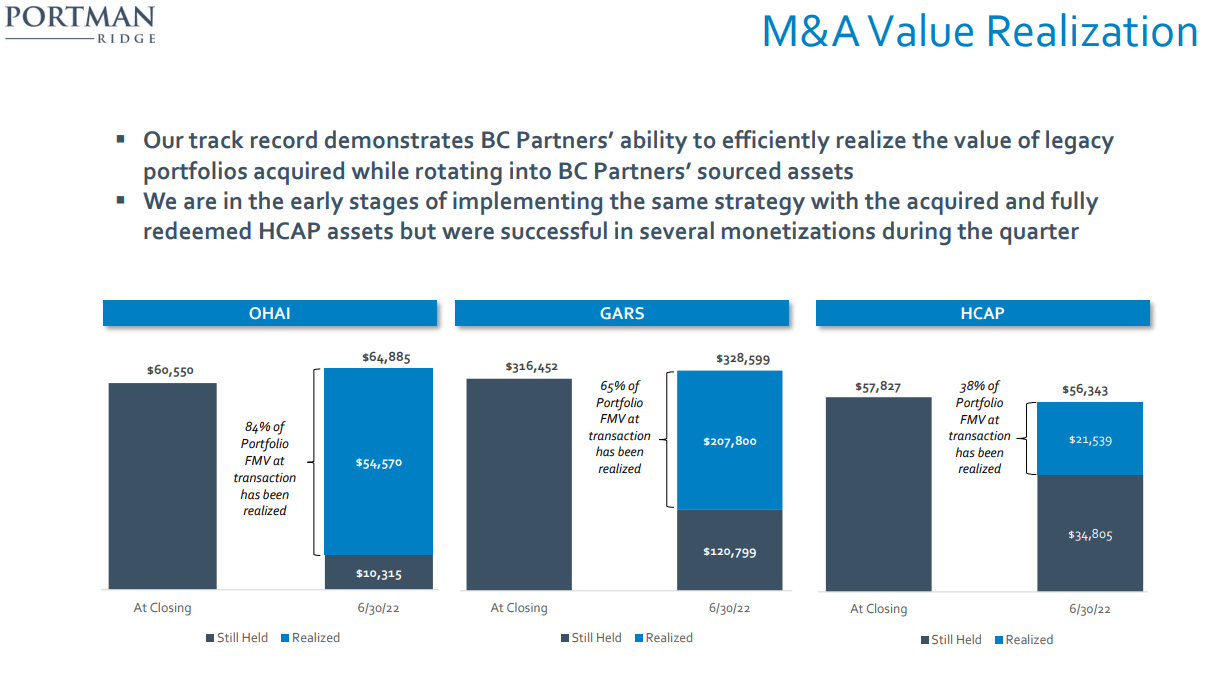

Also, the company is still in the early stages of monetizing the assets from the 3 companies (OHAI, GARS, HCAP) that they acquired from 2019 to 2021.

{kind=link}

As mentioned above, several closings on investments were delayed beyond the end of the second quarter.

{kind=link}

Conclusions And Recommendation

While PTMN has performed better than several of its peers in the BDC industry, the overall market environment remains very bearish with indications that the market trend is unlikely to change until something gives – whether that means the Fed decides not to raise rates by 75 bps as expected in November, or if inflation suddenly shows signs of reversing, or something else causes investor sentiment to turn positive. In the meantime, I am holding off on any new investments in any BDC holdings in my portfolio.

The asset coverage remains steady at about 170% as of June 30 and leverage sits at a reasonable 1.4x debt to equity.

{kind=link}

When the Q3 report comes out in early November I expect to have a better view of what the future might look like for the PTMN portfolio. But, until then, I am watching from the sidelines, and I would advise others to do the same unless you believe that the market has bottomed.

The price for PTMN seems reasonable at -26% discount to NAV, but the risk that NAV has declined substantially since the end of June offsets the value of that discount. I will continue to monitor the situation with cash on hand to take advantage of any positive new developments in the BDC world. Meanwhile, I rate PTMN a Hold.

For further details see:

Portman Ridge: Bear Market Bites The BDC Business