PSTX - Poseida: Buying This Rally Playing The Roche CAR-T Collaboration

Summary

- Poseida Therapeutics caught a strong rally last year following its announced collaboration with Roche.

- Worth an accretive $6Bn to PSTX, there's scope for the company to accelerate its CAR-T pipeline.

- As speculators on clinical-stage assets, we are buyers of this rally, eyeing initial price objectives to $10.50–$11.

- Net-net, rate buy.

Investment summary

Advancements in the oncology treatment market have led to tremendous gains for investors over the past 5-years. Not only that, the propensity to create a medical and remedial breakthrough in complex domains of oncology is doubtlessly an immense benefit to society at whole. It is for these reasons that both our values and core investment principles align with companies making headway in this manner.

Here I'll turn to our investment thesis on Poseida Therapeutics, Inc (PSTX) after it received the vote of approval from Swiss pharma giant Roche (RHHBY) to advance its series of Chimeric Antigen Receptor T-cell assets last year. For this, we are looking to play the upside from this deal. This report is aimed at those investors speculating on clinical-stage assets.

The trade thesis is to buy PSTX shares at, either, a limit of $7.70, or an at the market order below $8 over the coming week [from the time of this publication], for an initial price objective of $10.50-$11, seeking an initial ~40% return potential. For those reading this sometime after the fact, I'd suggest any point of entry at or below $8.50 is an attractive mark for this trade, but will look to revise this as the PSTX price structure evolves if/when further upside targets emerge. I anticipate new upside targets could be generated into the coming weeks, thereby extending the time horizon of this trade. For risk management, I don't recommend using a stop, but advocate to exit with a pullback to $6 and clipping the loss at ~20%, as we can always buy it back later with a reversal rally. We are buying 150 shares, potentially sizing this up along the way if the market supports this. If the stock runs to our price objective, this will warrant a reappraisal - either we reallocate, book profits, or think long-term positioning. Note, we run [relatively] equal-weight portfolios, so there's chance we will trim this position back anyway if its weighting overshoots our mandate.

Note: Before reading any further, it's imperative to understand the potential downside risks, and there are a few. The obvious risks to this playing out include a broad market correction. Moreover, any negative news around the company's Roche deal will be a large negative. Additionally, the potential for large PSTX shareholders to close positions, to take profits and allocate elsewhere could drive price action to the downside. Given PSTX's current market cap size, there's chance for wide volatility in the name, should this occur. Moreover, there's additional risk over the medium-term if the company's pipeline assets were to fail to progress or meet trial outcomes. Should this occur, there's immediate risk to this investment thesis, and we could make a loss on this position. Investors must realize these risks before making any investment decisions.

PSTX's CAR-T clinical assets an attractive play

The Roche deal saw PSTX catch a heavy bid over the last 6-8 months. The stock is up 292% off its June lows to the time of writing. With the advancements in oncology, the Roche deal makes sense to us.

For those unaware, chimeric antigen receptor T-cell ("CAR-T") therapy is a breakthrough approach in cancer treatment that entails the genetic engineering of autologous [or allogenic] T-cells. The aim is to manually express a chimeric antigen receptor [the "CAR" component, as mentioned above], targeting a specific antigenic epitope that is expressed on malignant cells. For reference, an epitope is the part of an antigen that is recognized by the immune system, and carcinoma's are thought to have the ability to 'trick' this interplay as an escape mechanism, thereby fuelling their angiogenesis and growth. Consequently, the ability to target the specific epitope results in a highly specific immune effector cell, capable of recognizing and killing cancer cells with high avidity and specificity.

CAR-T therapy has garnered substantial data in the treatment of haematologic malignancies, with early-to-mid-phase trials demonstrating effective response rates and robust remission data. Its efficacy, and therefore attractiveness to both clinicians and patients, stems from the above-mentioned 'reprogramming' of T-cells to selectively eliminate cancer cells, bypassing the need for systemic toxicity and off-target effects related to chemotherapy and radiation therapy - the current standard of care. If it continues along this pathway, CAR-T therapy could mean a paradigm shift in standard of care for cancer treatment. Hence, PSTX's assets, and the Roche deal, are absolutely worth paying attention to.

Market research projects a CAGR of the CAR-T treatment market of ~49% t $10Bn into FY27', with additional data suggesting a c.14% CAGR into FY31', or ~25% CAGR into FY30'. In any sense, double-digit geometric growth is the forecast across these studies. This adds to the tail of potential returns on our trade thesis.

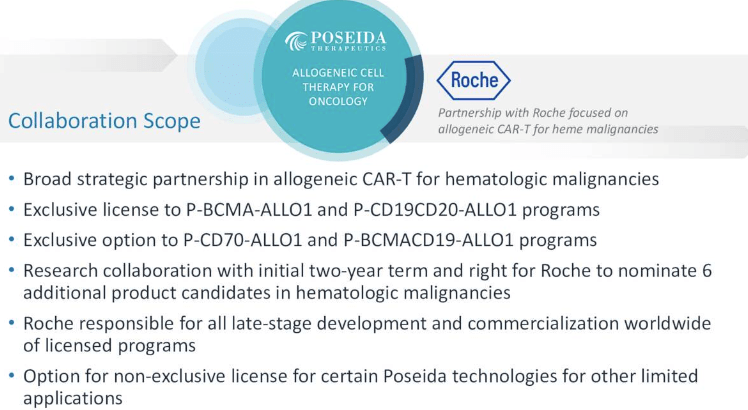

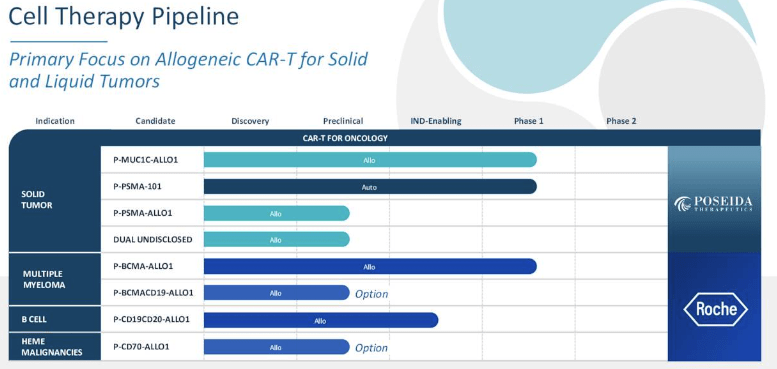

Switching to the deal itself , under the MOU, Roche has optionality to acquire either, exclusive proprietorship, or ability to cultivate and commercialize the various allogenic CAR-T pipelines within PSTX's repertoire. It is particularly focused on compounds acting on haematologic malignancies, including P-BCMA-ALLO1 [for multiple myeloma], and P-CD19CD20-ALLO1, for B-cell malignancies [see: Exhibit 2].

Both parties will concurrently embark on a joint research program ("JRP") to create and develop additional allogenic CAR-T therapies, to address existing and emerging haematologic targets. For the portion of PSTX's clinical programs licensed/optioned to Roche, the company will conduct the early-stage trials and produce relevant clinical materials, aiming to transition these into clinical programs for Roche to develop, and eventually commercialize. This makes sense for both parties, by estimation, as it reduces the pipeline risk for Roche, and the execution risk for PSTX.

Exhibit 1. PSTX/Roche collaboration scope

Data: PSTX Q3 Investor Presentation

{kind=link}

Exhibit 2. PSTX CAR-T pipeline

Data: PSTX Q3 Investor Presentation

{kind=link}

It's the financials that are most attractive to investors, however. Under the terms, PSTX is set to receive $110mm in upfront payments and an additional $110mm in near-term milestone payments. Overall, including all of the research, development and launch milestones, the deal has an accretive value of $6Bn to PSTX over the coming years, in addition to a tiered royalty structure tied to net sales [said to be in the single digits] across its various programs. This is a tremendous bump for PSTX and a vote of confidence in validating its particular clinical pathways, as mentioned earlier. Backing the company, and presuming it can achieve these milestones, this values PSTX at a high multiple by estimation.

PSTX market generated data

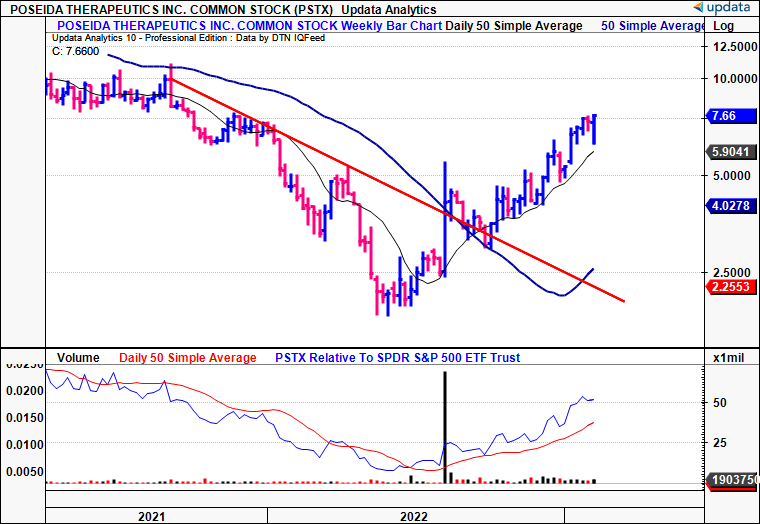

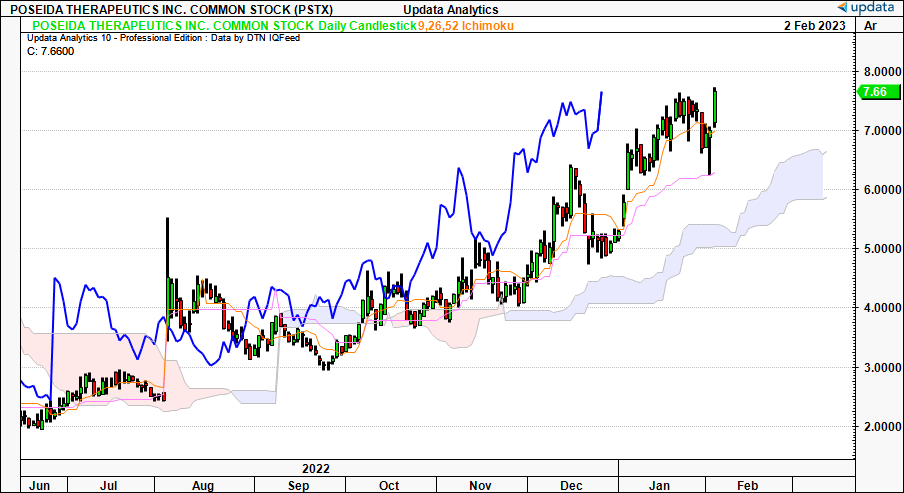

Following the announcement PSTX caught an enormous bid and has rallied in strong fashion over the last 6-months to date. It broke the longer-term resistance line in doing so and has been riding its 50DMA as support to the current day.

Exhibit 3. PSTX setting higher highs on higher lows, riding 50DMA as support to current session

{kind=link}

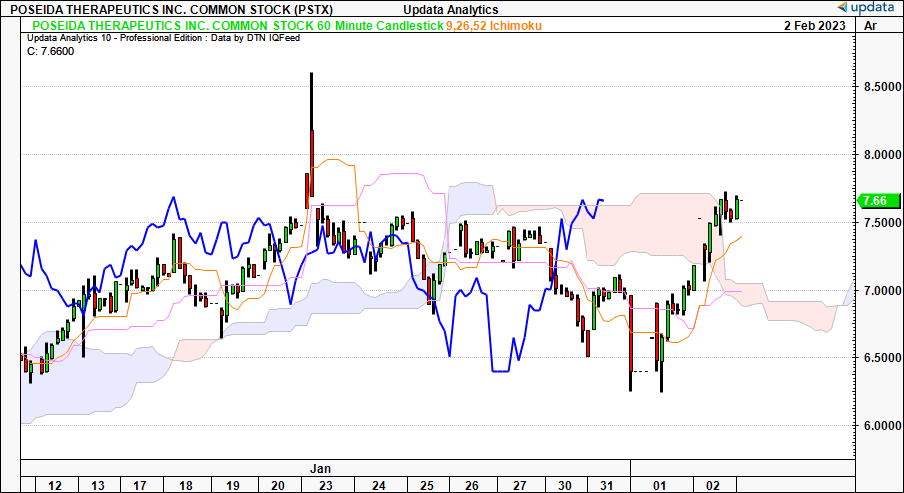

With that, we can see where we currently sit within the trend. To do this, analysis over various time horizons is essential, i.e, hourly, daily, and weekly frames. On a 60-minute cloud chart, that looks to the coming days of trade, shares have crossed back above the cloud with the lagging line have a good look above the cloud top. The cross above the cloud on this 60-minute time frame means we can trade the shorter-term targets discussed later. Near-term support has now pushed to $7.20 and we remain near-term bullish above these levels.

Exhibit 4. Bullish cross above the cloud meaning we can trade the shorter-term upside targets

{kind=link}

Looking to the daily chart, that points to price action in the coming weeks, we are in firm bullish territory. Both the price line and lagging line are pulling away from the cloud and the cloud itself is shifting upward in tandem. We could pull back to ~$6.70 by March and still be on trend, by this price structure.

Exhibit 5. Bullish on medium-term time horizon

{kind=link}

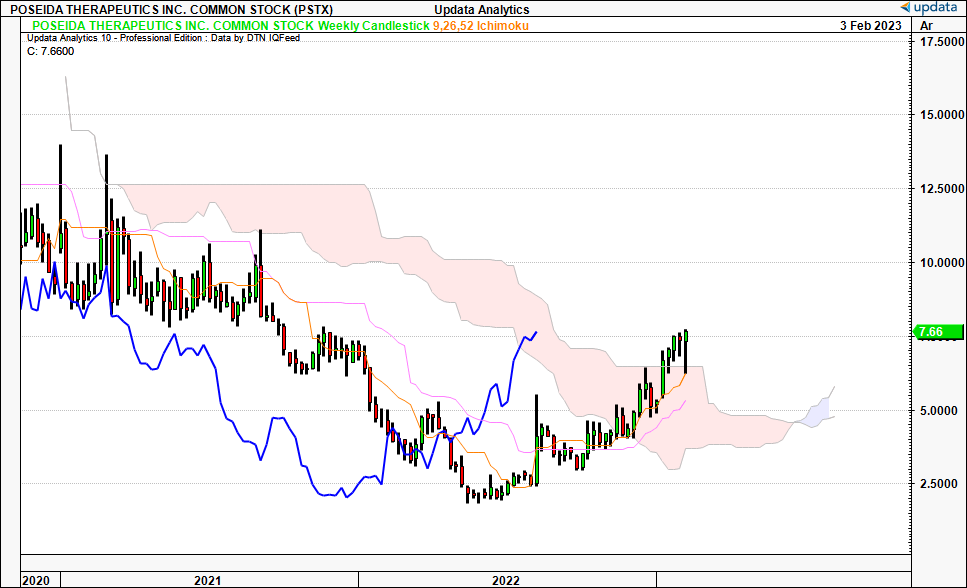

On the weekly chart, we've also seen a cross above the cloud. This looks out to the coming months. However, the lagging line has yet to have a look above the cloud top, and a push of this line above the $7.70 mark would confirm the long-term buy thesis here. Note, the stock price tested the cloud top at $6.50 earlier this week and caught demand immediately, which is a good sign in our eyes. Even a pullback to the cloud could create an interesting cup and handle setup which we'd be happy to trade off [see: Exhibit 6a].

Exhibit 6. Price line with cloud cross on weekly bars, lagging line yet to eye itself above the cloud. Looking for this to happen for long-term bullishness.

{kind=link}

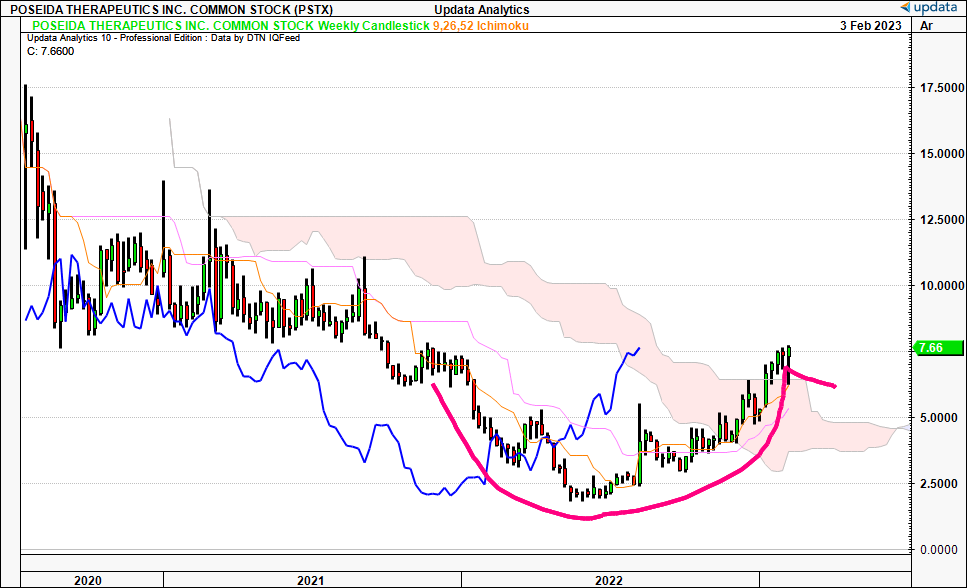

Exhibit 6a. Even a pullback to the cloud top by the end of February sets up for a cup and handle which is a bullish setup in our eyes

{kind=link}

Meanwhile, equity inflows into PSTX have been incredibly strong since the announcement, increasing in magnitude week-on-week to the current standing. This adds weight to a continuation of the trend on the weekly charts shown above, by estimation.

Exhibit 7. Weekly inflows into PSTX increasing week-on-week

{kind=link}

The quality of buyer has been a standout too, with evidence from the negative volume index ticking higher, illustrating institutional money has been actively participating in the rally. It has pushed higher in the recent weeks as volume has pulled back, adding to this thesis.

Exhibit 8. Real money helping drive the rally, adding to longer-term fund manager positioning

Data: Updata

PSTX suggested price targets for trade

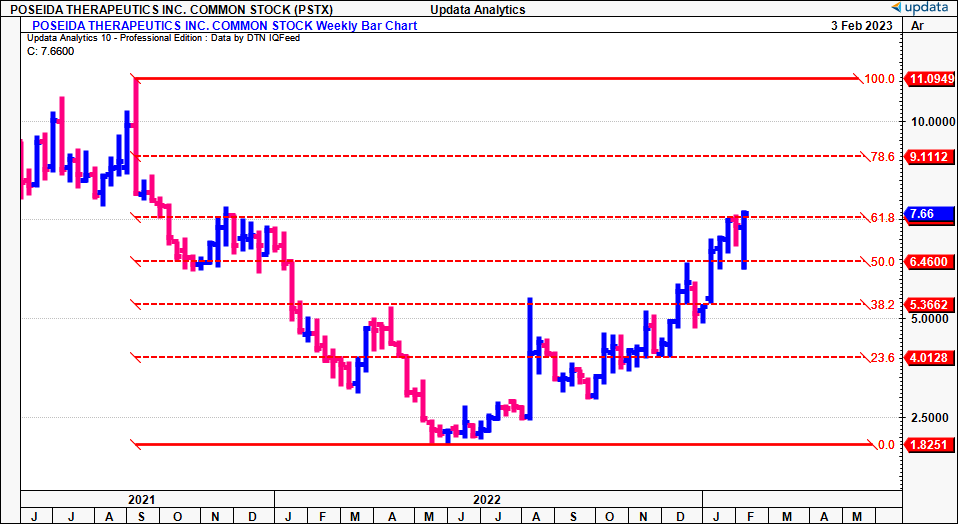

Tracing the Fibs' down from the September FY21' high to the June FY22' lows, we see the stock has reclaimed ~62% of the leg down [note, PSTX listed in FY20']. It has tested this mark over the last 3 weeks, and despite a sharp pullback to the 50% mark on the retracement, swiftly reclaimed this level once again. From here, we are looking to targets of $9.40, then $11.

Exhibit 9. Fibonacci targets to $9.10, then $11

{kind=link}

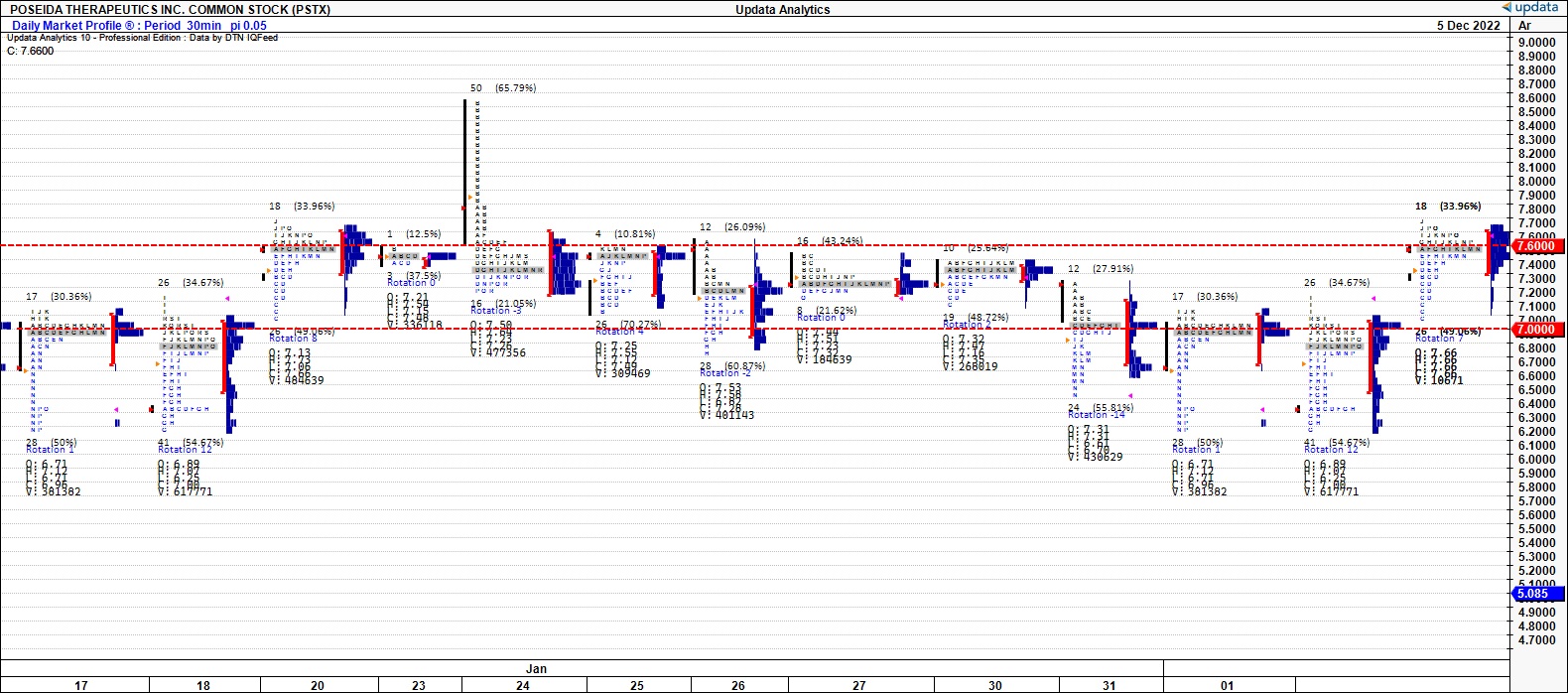

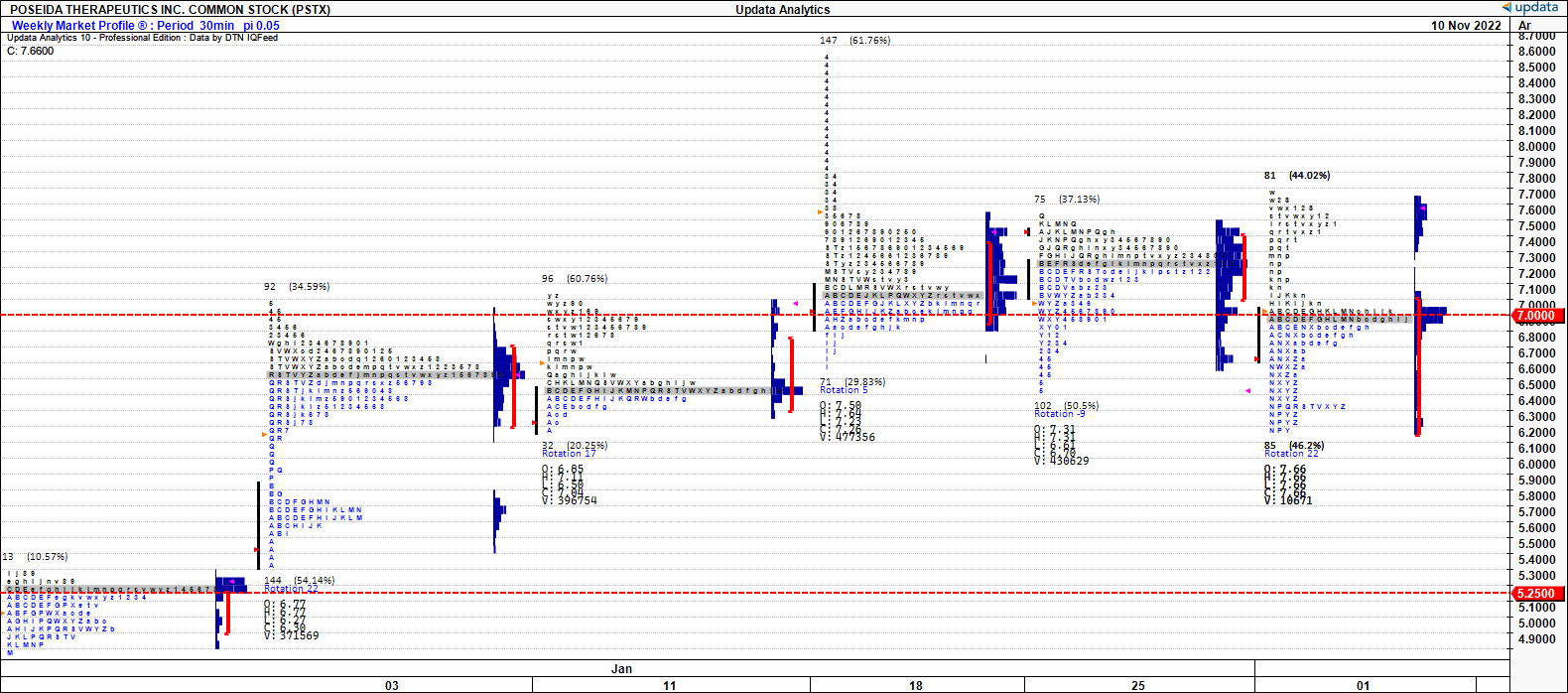

Looking at the market profile over January, first on a daily frame [Exhibit 10], then on a weekly basis [Exhibit 11], investors have found equilibrium at the $7.40 and $7 levels, respectively. Buyers have been heavily active on the intraday weakness below these levels. With each pullback, large buyers have been adding to longs with strong volume [look to the blue letters in the profile in Exhibit 10, noting where the time-price opportunity has been at each half our interval].

Exhibit 10. Market found strong equilibrium at $7-$7.40, any buys below this are well supported in the volume and subsequent price action

{kind=link}

On the weekly market profile, large buyers have been extremely active below each point of control [grey bars]. This is where the price spent the most amount of time. We've seen the market's fair value of PSTX tick higher almost each week since December. Most of the volume this week has been concentrated at the point of control, therefore, there's scope for it to re-rate back above previous marks of ~$8 with the level of buying on weakness.

Exhibit 11. Weekly market profile indicating large buyers extremely active on each pullback in weakness. This provides good support for continued re-rating

{kind=link}

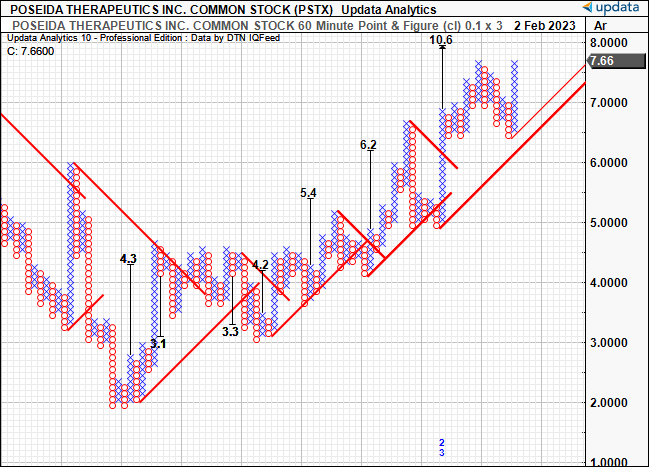

With that, we have upside targets over the coming days to weeks reaching $10.60. This is using a 0.1x3 box reversal, quite sensitive to movements, but still biasing the prevailing trend to remove short-term noise. This supports fibonacci targets above.

Exhibit 12. Near-term upside targets to $10.60

{kind=link}

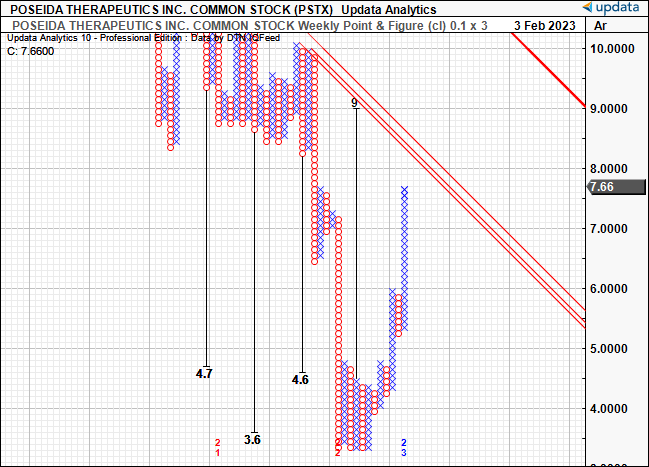

Long-term targets are supportive to $9 and have potential to rate higher if price action continues climbing. Again, this is supported by the fibonacci targets described earlier, adding to the confluence of these ranges.

Exhibit 13. Longer-term upside targets to $9, potential to rate higher if price action continues climbing

{kind=link}

In short

PSTX's rally has been spurred on by a valid catalyst in the Roche deal. Worth a potential $6Bn to PSTX, the fundamental support is there, and market generated data indicates this rally has legs to extend. We are looking to achieve a 40% return potential, with a reappraisal at ~$10.50-$11. There is confluence to these targets over the coming weeks. Should price action continue to evolve higher, we believe there's scope for additional upside targets from here. It is essential to read the risks section located at the beginning of this report. Net-net, rate buy.

For further details see:

Poseida: Buying This Rally, Playing The Roche CAR-T Collaboration