PSTX - Poseida Therapeutics' Financial And Clinical Milestones Signal Upgrade To 'Strong Buy'

2023-09-27 08:59:28 ET

Summary

- Poseida Therapeutics exhibits robust financials with Q2 2023 collaboration revenue surging to $20.01M and a recent $50M Astellas investment extending its cash runway.

- Despite stock underperformance, Poseida's diversified CAR-T pipeline shows momentum with FDA IND clearances and strategic collaborations, specifically with Roche.

- Investment recommendation shifts from "Buy" to "Strong Buy," predicated on Poseida maintaining its clinical efficacy and prudent financial management.

At a Glance

Revisiting Poseida Therapeutics (PSTX), the company continues to intrigue with its diversified cell and gene therapy pipeline and newfound financial fortitude. Q2 2023 earnings reveal a substantial boost in collaboration revenue to $20.01M, powered by a strategic payment, contrasting a net loss improvement to $27.46M from last year's $43.04M. Financial risk further diminishes with a recent $50M Astellas (ALPMF) investment, extending cash runway to nearly 22 months. Despite stock underperformance and looming market skepticism, Poseida shows clear momentum with FDA IND clearances and operational adjustments in clinical programs. Investors should note the recalibrated liquidity position and look ahead to key clinical milestones. My recommendation shifts from a "Buy" to a "Strong Buy," conditional on continued clinical and financial prudence.

Earnings Report

To begin my analysis, looking at Poseida Therapeutics' most recent earnings report for the quarter ending June 30, 2023, the first aspect that stands out is the exponential increase in collaboration revenue, from $2.7M in Q2 2022 to $20.01M in Q2 2023. However, it's noteworthy that R&D expenses remain high at $39.2M, a moderate rise from last year's $35M. General and administrative costs have slightly dipped to $8.68M from $9.24M, potentially indicating better operational efficiency. The net loss has improved year-over-year, standing at $27.46M compared to last year's $43.04M. This is a positive indicator for future earnings, especially when considering that the diluted net loss per share has narrowed to $-0.32 from $-0.69 year-over-year.

Financial Health & Liquidity

Turning to Poseida Therapeutics' balance sheet , as of June 30, 2023, the company had $49.9M in cash and cash equivalents and $164.7M in short-term investments, totaling $214.6M in liquid assets. Poseida's six-month "Net cash used in operating activities" was $71.3M, yielding a monthly cash burn of approximately $11.9M. Given these figures, Poseida would have an 18-month cash runway. However, this liquidity situation dramatically changes when factoring in the recent $50M investment from Astellas, which effectively extends the cash runway. The new total liquid asset pool would be $264.6M, providing an adjusted cash runway of roughly 22 months. Note that these estimates are based on historical data and may not be indicative of future performance.

Incorporating the recent Astellas investment, Poseida's liquidity situation improves, signaling a bolstered financial position. The company's term debt remains at $58.4M, and the additional funds could serve to mitigate risks tied to this liability. The Astellas deal, which included the purchase of 8.3M shares at $3.00 per share and a $25M one-time payment, not only strengthens Poseida's balance sheet but may also render the company more attractive for future financing opportunities. These are my personal observations, and other analysts might interpret the data differently.

Capital, Growth, Momentum, & Ownership

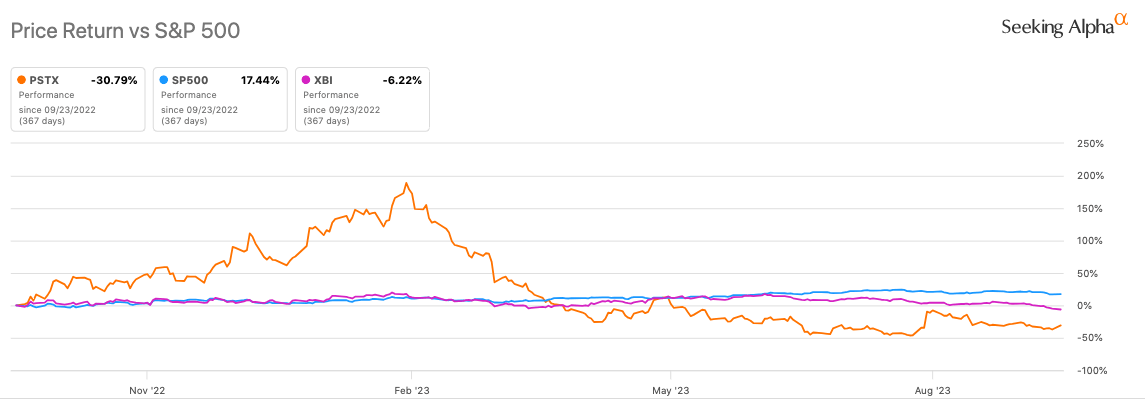

According to Seeking Alpha data, Poseida Therapeutics' capital structure (with a market capitalization near $200M) is fairly resilient given its liquidity enhancements and relatively modest term debt, providing a runway extending into late 2025. Revenue growth prospects are dampened, as analyst projections indicate a YoY decrease in sales for 2024, contrasting the positive uptick in collaboration revenue. Stock momentum is a concern: Poseida has significantly underperformed SPY across multiple timeframes, including a 1-year slide of -30.79% versus SPY's gain of +17.44%.

{kind=link}

Ownership is diversified, with institutions holding 43.69% and corporations 27.38%, implying some degree of market trust yet an absence of a single, stabilizing majority stakeholder. Insider trading suggests modest, non-open market acquisitions without alarming dispositions, painting a cautiously optimistic insider sentiment. Short interest stands at 6.78%, suggesting a moderate but not overly concerning level of market skepticism, which warrants investor attention but isn't an immediate red flag.

Investing in microcap companies, such as Poseida Therapeutics, carries inherent risks often underestimated by retail investors. Such firms usually have limited operational histories, scarce liquidity, and are prone to price manipulation. The lack of analyst coverage can result in asymmetric information and erratic price movements. Volatility is typically high, making them not suitable for risk-averse investors. Additionally, microcaps often face the risk of "binary events," like FDA approvals, which can dramatically swing the stock in either direction. The combination of these factors can result in significant capital loss, hence thorough due diligence is imperative.

Optimizing Efficacy and Scalability in Poseida's CAR-T Trials

Poseida Therapeutics appears to be tactically iterating its allogeneic CAR-T clinical programs to adapt to emerging industry best practices and early-phase trial learnings. By modifying dosing regimens and manufacturing protocols, the company demonstrates a proactive stance on optimizing both treatment efficacy and production scalability-a non-trivial aspect often overlooked in early-phase studies but crucial for commercial viability.

The company's P-BCMA-ALLO1 and P-MUC1C-ALLO1 programs are particularly noteworthy, not just for their clinical indications but also for their partnerships with Roche (RHHBY). These collaborations could offer strategic benefits, from shared R&D costs to potential expedited routes to market. However, the limited patient availability for newer cohorts indicates a cautious approach, perhaps reflecting either methodological rigor or an awareness of operational constraints.

Furthermore, the recent FDA IND clearance for Poseida's dual CAR-T candidate, P-CD19CD20-ALLO1, represents a significant milestone. The clearance adds a layer of differentiation to Poseida's portfolio, as it targets both CD19 and CD20 to potentially overcome antigen escape -a known hurdle in CAR-T therapy. Poseida's strategic partnerships and FDA engagements suggest the company is not just advancing its pipeline but is also positioning itself adeptly in the competitive landscape of cell therapies.

My Analysis & Recommendation

In summary, Poseida Therapeutics has demonstrated marked progress in both its financials and its therapeutic pipeline. The recent surge in collaboration revenue and improved net loss are clear indicators that the firm is moving in a positive direction, despite enduring skepticism and market underperformance.

Investors should keep an eye on a few critical variables in the near term:

-

Efficacy Data from Clinical Programs: Data releases from Poseida's ongoing clinical trials, especially the dual CAR-T candidate, P-CD19CD20-ALLO1, could act as powerful catalysts. Regulatory and partnership milestones in the Roche collaboration will also be key drivers.

-

Operational Efficiency: The company must strive to further tighten its operational costs without compromising the quality and speed of drug development, to improve its financial metrics.

-

Market Re-Engagement: Given the current underperformance relative to broader indices, a key parameter to track would be how effectively Poseida can convert its pipeline promise into tangible market value. Investors should also be mindful of any changes in institutional ownership or insider activity, as they could signal market sentiment shifts.

-

Short Interest: A relatively high short interest should not be ignored, as any negative news or failure in clinical trials could trigger a sell-off, exacerbated by short positions.

-

Event-Driven Risks: As a microcap with a high-beta profile, Poseida is susceptible to binary events. While such events offer high upside potential, they also present equally elevated downside risks.

Given the confluence of Poseida's strengthened financials, increasingly promising pipeline, and strategic collaborations, I am upgrading my investment recommendation from a "Buy" to a "Strong Buy." This upgrade is contingent upon the firm maintaining its current trajectory, particularly in clinical efficacy and financial management. It is essential for potential investors to engage in meticulous due diligence to mitigate the inherent risks associated with microcap biotech investments. This is a long-term play that requires an appetite for risk and a deep understanding of both the scientific and market variables at play.

Risks to Thesis

While I've emphasized Poseida Therapeutics' diversified pipeline and improved liquidity as reasons for a "Strong Buy" recommendation, several counterpoints could alter this perspective. The CAR-T space is crowded; Poseida is up against giants like Novartis (NVS) and Gilead (GILD). Intellectual property litigation, a frequent issue in biotech, could disrupt operations. The recent FDA IND clearance is an early-stage marker, not a guarantee of commercial viability. A failure or delay in any clinical program would have an outsized impact on the stock given its microcap status. Finally, although partnerships with Astellas and Roche provide funding, they could dictate unfavorable terms in the long run, eroding profitability. High R&D expenditures further strain the balance sheet, questioning long-term sustainability. Therefore, extreme caution is warranted.

For further details see:

Poseida Therapeutics' Financial And Clinical Milestones Signal Upgrade To 'Strong Buy'